Pork Farms / Kerry Foods: Summary of Hearing with Tesco on 11 March 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uk Licensed Products Nov 2020

UK LICENSED PRODUCTS NOV 2020 Product Brand Product Name Company number Alara Wholefoods Alara Wholefoods OATS-GB-001-009 Organic Gluten Free Scottish Oats Porridge Ltd Green's Beers GB-004-001 Discovery Greens Beers Green's Beers GB-004-002 Dry Hopped Lager Green's Beers GB-004-003 Pilsner Green's Beers GB-004-004 Golden Ale Green's Beers GB-004-005 Blond Green's GB-004-007 Dark Ale Green's Beers GB-004-007 Dark Green's Beers GB-004-008 India Pale Ale Green's Beers GB-004-009 Tripel Green's Beers GB-004-010 Dubbel Lovemore GB-006-002 Apple and Sultana cookies x2 Welsh Hills Bakery Lovemore GB-006-005 Chocolate Brownie Slices x2 Lovemore GB-006-006 Chocolate Brownie Slice Lovemore GB-006-007 Chocolate Chip Cookies Lovemore GB-006-008 Chocolate Chip Cookies Lovemore GB-006-010 Deep Filled Mince Pies Lovemore GB-006-011 Digestive Biscuits Lovemore GB-006-014 Gingerbread Men Lovemore GB-006-017 Lemon Cake Slices Lovemore GB-006-018 Fruit Cake mini slice Lovemore GB-006-019 Fruit Cake Slices Lovemore GB-006-021 Apple Pies Lovemore GB-006-022 Cherry Bakewells Lovemore GB-006-023 Chocolate Celebration Cake Lovemore GB-006-024 Chocolate Muffins Lovemore GB-006-025 Crispbreads Lovemore GB-006-026 Custard Creams Lovemore GB-006-027 Double Chocolate Cookies Lovemore GB-006-028 Jammy Wheels Lovemore GB-006-029 Chocolate Cake mini slice Lovemore GB-006-030 Madeira Cake mini slice Lovemore OATS-GB-006-031 Oat Crunch Cookies Lovemore GB-006-032 O'Chocos Lovemore GB-006-033 Shortbread Fingers Welsh Hills Bakery GB-006-034 Dundee Welsh Hills Bakery GB-006-036 -

01691 668004 Our Food Range Frozen Food Page 5 Contents Buffet Range Page 6 - 11 Fish & Seafood Page 12 - 16

The Little Food Company Ltd 01691 668004 www.littlefoodcompany.co.uk Our Food Range Frozen Food Page 5 Contents Buffet Range Page 6 - 11 Fish & Seafood Page 12 - 16 Poultry & Game Page 17 - 23 Red Meat Page 24 - 29 Vegetarian Range Page 30 -33 Pastry & Savoury Goods Page 34 - 38 Welcome To Morning Goods Page 39 - 43 The Little Food Company Bread & Pizza Page 44 - 52 For over 18 years The Little Food Company has been supplying hotels, pubs, Dairy & Egg Page 53 - 54 restaurants, tearooms, colleges, hospitals and schools etc. We have a fleet of multi-temperature vehicles, a great telesales team, an experienced field sales Potato Products Page 55 - 59 team and an answerphone service that helps take orders 24 hours a day. Fruit & Vegetables Page 60 - 62 Based in Oswestry, a small market town on the Shropshire and Mid Wales border, we care passionately about what we do and we distribute throughout Cakes, Gateaus & Desserts Page 63 - 73 Shropshire, Cheshire, Herefordshire, the West Midlands, North Wales, Liverpool and Manchester. Chilled & Fresh Foods Page 75 We pride ourselves on having a strong range of great quality food for our Deli Meats & Speciality Cheese Page 76 - 78 selected customers and supplement these with regular special offers and monthly promotions via our website. Fresh From The Butcher Page 79 - 83 This brochure represents a selection of what we have to offer and whilst all Dry Store Foods Page 85 these lines are available at the time of printing there may be changes as we are constantly looking for new ideas. -

Psychological Science

Psychological Science http://pss.sagepub.com/ Sensory-Specific Satiety Is Intact in Amnesics Who Eat Multiple Meals Suzanne Higgs, Amy C. Williamson, Pia Rotshtein and Glyn W. Humphreys Psychological Science 2008 19: 623 DOI: 10.1111/j.1467-9280.2008.02132.x The online version of this article can be found at: http://pss.sagepub.com/content/19/7/623 Published by: http://www.sagepublications.com On behalf of: Association for Psychological Science Additional services and information for Psychological Science can be found at: Email Alerts: http://pss.sagepub.com/cgi/alerts Subscriptions: http://pss.sagepub.com/subscriptions Reprints: http://www.sagepub.com/journalsReprints.nav Permissions: http://www.sagepub.com/journalsPermissions.nav Downloaded from pss.sagepub.com at University of Aberdeen on August 24, 2010 PSYCHOLOGICAL SCIENCE Research Report Sensory-Specific Satiety Is Intact in Amnesics Who Eat Multiple Meals Suzanne Higgs, Amy C. Williamson, Pia Rotshtein, and Glyn W. Humphreys University of Birmingham ABSTRACT—What is the relationship between memory and Despite these intriguing findings, little is known about the appetite? We explored this question by examining prefer- mechanisms underlying multiple-meal eating in amnesia. ences for recently consumed food in patients with amnesia. Because the procedure in previous studies has been to offer the Although the patients were unable to remember having same meals in succession, one explanation is that the usual eaten, and were inclined to eat multiple meals, we found decline in palatability and intake of a food that has been eaten to that sensory-specific satiety was intact in these patients. satiety is disrupted in amnesia (Rolls, Rolls, Rowe, & Sweeney, The data suggest that sensory-specific satiety can occur in 1973). -

Port, Sherry, Sp~R~T5, Vermouth Ete Wines and Coolers Cakes, Buns and Pastr~Es Miscellaneous Pasta, Rice and Gra~Ns Preserves An

51241 ADULT DIETARY SURVEY BRAND CODE LIST Round 4: July 1987 Page Brands for Food Group Alcohol~c dr~nks Bl07 Beer. lager and c~der B 116 Port, sherry, sp~r~t5, vermouth ete B 113 Wines and coolers B94 Beverages B15 B~Bcuits B8 Bread and rolls B12 Breakfast cereals B29 cakes, buns and pastr~es B39 Cheese B46 Cheese d~shes B86 Confect~onery B46 Egg d~shes B47 Fat.s B61 F~sh and f~sh products B76 Fru~t B32 Meat and neat products B34 Milk and cream B126 Miscellaneous B79 Nuts Bl o.m brands B4 Pasta, rice and gra~ns B83 Preserves and sweet sauces B31 Pudd,ngs and fru~t p~es B120 Sauces. p~ckles and savoury spreads B98 Soft dr~nks. fru~t and vegetable Ju~ces B125 Soups B81 Sugars and artif~c~al sweeteners B65 vegetables B 106 Water B42 Yoghurt and ~ce cream 1 The follow~ng ~tems do not have brand names and should be coded 9999 ~n the 'brand cod~ng column' ~. Items wh~ch are sold loose, not pre-packed. Fresh pasta, sold loose unwrapped bread and rolls; unbranded bread and rolls Fresh cakes, buns and pastr~es, NOT pre-packed Fresh fru~t p1es and pudd1ngs, NOT pre-packed Cheese, NOT pre-packed Fresh egg dishes, and fresh cheese d1shes (ie not frozen), NOT pre-packed; includes fresh ~tems purchased from del~catessen counter Fresh meat and meat products, NOT pre-packed; ~ncludes fresh items purchased from del~catessen counter Fresh f1sh and f~sh products, NOT pre-packed Fish cakes, f1sh fingers and frozen fish SOLD LOOSE Nuts, sold loose, NOT pre-packed 1~. -

Putney Pies House Salad (V)

All meals are freshly cooked to order so there may be a wait. PIES If you want fast food we are not for you. Our pies are made by hand in our kitchen from putney locally sourced fresh ingredients daily. menumenu PIES SMALL PLATES / STARTERS served with mash and gravy ............................................. £14.95 salads Small / Large served with hand cut triple cooked chips ............................ £15.95 vegetarian/vegan dishes are included in this section Market Salad (Vegan) .............................. £4.95/£8.95 CHILDREN'S MENU with maple syrup & mustard dressing Jumbo Sausage Rolls (3 pieces) ........... £6.95 Steak & Ale Pie in Shortcrust Pastry Case Mini Shepherds Pie ................................. £7.25 (1 piece of traditional sausage meat with thyme, steak beef, ale, onion and thyme Putney Pies House Salad (V) ........... £6.95/£10.95 1 piece with sausage meat, cranberry & pistachio, Chicken, Portobello Mushrooms & Leek Pie with new potatoes, baby gems, green beans, Bangers & Mash ....................................... £5.95 1 piece with sausage meat, apricot and sage) in Shortcrust Pastry Case olives, boiled egg, cherry tomatoes served with a french vinaigrette Veggie Bangers & Mash (V) ..................... £5.95 chicken thigh, portobello mushrooms, leeks, onion, cream Vegetarian Jumbo Sausage Rolls (V) £6.95 - optional oven baked salmon - extra £5 (3 pieces) Beef Bourguignon in Short Crust Pastry Case - optional oven baked chicken breast - extra £5 Fish Cake with Chips ............................... £5.95 -

Kinross-Shire

Kinross Newsletter Founded in 1977 by Mrs Nan Walker, MBE Published by Kinross Newsletter Limited, Company No. SC374361 Issue No 388 August 2011 www.kinrossnewsletter.org ISSN 1757-4781 DEADLINE CONTENTS for the September Issue From the Editor ............................................................ 2 2.00 pm, Monday Letters ......................................................................... 2 22 August 2011 News and Articles ........................................................ 5 for publication on Police Box...................................................................15 Community Councils....................................................16 Saturday 3 September 2011 Club & Community Group News .................................21 Sport ..........................................................................30 Contributions for inclusion in the Out & About................................................................37 Newsletter Gardens Open. .............................................................39 The Newsletter welcomes items from clubs, Congratulations and Thanks..........................................40 community organisations and individuals for Kinross High School Awards ........................................41 publication. This is free of charge (we only Church Information......................................................43 charge for commercial advertising - see Playgroups & Nurseries................................................45 below right). All items may be subject to Notices........................................................................46 -

92 AUGUST Shelford Tommy

#92 AUGUST Shelford Tommy Nottingham has always boasted its fair share of characters, legends and eccentrics. People like Benjamin Mayo, and more recent contenders like Frank Robinson, affectionately known as Xylophone Man, will go down in local history... But there’s one from the eighteenth century who, “to his extraordinary powers, a servant girl was although quite a local celebrity in his day, is in the kitchen, about to dress some fish; not long generally forgotten in 2017. taken from the river but apparently dead. When she was about to cut off the head of one of them, His real name was James Burne, though he Tommy, at the instant she laid her knife on the was nicknamed “Shelford Tommy.” In 1931, J fish’s neck, uttered, in a plaintive voice, ‘Don’t cut Holland Walker described Tommy as “an itinerant my head off.’ ventriloquist [who] earned a precarious existence by giving exhibitions of his capabilities with an “The girl, upon this, being much alarmed, and ill-made ventriloquial dummy.” knowing not whence the voice proceeded, hastily drew the knife from the little fish and stood for Tommy was recorded as “carrying in his pocket, some time in motionless amazement. At length, an ill-shaped doll, with a broad face, which he however, recovering herself, and not seeing the apparently exhibited at public-houses, on fair fish stir, had courage to proceed to her business, days, race days and market days.” The gazing and took up the knife a second time, to sever the crowd would gather round to see this wooden head of the fish from the body. -

Aldi, West Ewell Date of Visit: 28.07.18

Store and location: Aldi, West Ewell Date of visit: 28.07.18 Brand Product Sugar reduction category Calorie reduction category soft drinks levy Entrance No promotions in entrance Gondola Ends Store layout does not include gondola ends Trolley checkout area The Foodie market Quinoa bars (Coco & cashew) Biscuits n/a The Foodie market Quinoa bars (Goki & cranberry) Biscuits n/a Passions Popcorn (sweet) Sweet Confectionary n/a Passions Popcorn (sweet & salted) Sweet Confectionary n/a Wrigleys Extra chewing gum (peppermint) n/a n/a Wrigleys Extra chewing gum (spearmint) n/a n/a Wrigleys Extra chewing gum (cool breeze) n/a n/a Wrigleys Extra chewing gum (extra white) n/a n/a Passion Deli Pea snacks (sea salt & vingar) n/a Crisps and savoury snacks Passion Deli Pea snacks (sweet chilli) n/a Crisps and savoury snacks The Foodie market Hike protein bars (Cacao) Biscuits n/a The Foodie market Hike protein bars (Berry) Biscuits n/a Dominion Complimints (strongmint) - sugar free n/a n/a Dominion Complimints (spearmint) - sugar free n/a n/a Dominion Complimints (strongmint) - sugar free n/a n/a Passions Deli Red Lentil Snacks (Tangy tomoto) n/a Crisps and savoury snacks Passions Deli Red Lentil Snacks (barbecue) n/a Crisps and savoury snacks Foodie Market Flatbread thin bites (multi-seed) n/a Savoury biscuits, crackers and crispbreads Foodie Market Flatbread thin bites (cheddar & cracked black pepper) n/a Savoury biscuits, crackers and crispbreads Foodie Market Flatbread thin bites (sweet chilli) n/a Savoury biscuits, crackers and crispbreads Dominion -

Appendices and Glossary

Appendices and glossary Appendix A: Terms of reference and conduct of the inquiry Appendix B: Industry background Appendix C: The companies Appendix D: The Transaction Appendix E: Jurisdiction Appendix F: The counterfactual Appendix G: Competitive effects Appendix H: Tender data Appendix I: Analysis of capacity Appendix J: Barriers to entry Glossary APPENDIX A Terms of reference and conduct of the inquiry Terms of reference 1. On 5 January 2015, the CMA referred the completed acquisition by Pork Farms Caspian Limited of the chilled savoury pastry business of Kerry Foods Limited for an in-depth (phase 2) merger investigation: 1. In exercise of its duty under section 22(1) of the Enterprise Act 2002 (the Act) the Competition and Markets Authority (CMA) believes that it is or may be the case that: (a) a relevant merger situation has been created, in that: (i) enterprises carried on by or under the control of Pork Farms Group Limited (formerly named Poppy Acquisition Limited) have ceased to be distinct from the chilled savoury pastry business carried on by or under the control of Kerry Foods Limited; and (ii) the condition specified in section 23(1)(b) of the Act is satisfied; and (b) the creation of that situation has resulted, or may be expected to result, in a substantial lessening of competition within a market or markets in the United Kingdom for goods or services, including in: (i) the branded, own label and convenience retail segments of the supply of cold pies; (ii) the own label and convenience retail segments of the supply of sausage rolls, pasties and slices (when considered in combination), and the branded, own label and convenience retail segments of the supply of sausage rolls (when considered individually); and (iii) the own label retail segment of the supply of hot pies. -

Pork Farms / Kerry Foods: Summary of Hearing with Samworth on 4 March 2015

PORK FARMS CASPIAN / KERRY FOODS MERGER INQUIRY Summary of hearing with Walker and Sons, Ginsters of Cornwall and Tamar Foods, divisions of Samworth Brothers Limited on 4 March 2015 Background 1. Samworth Brothers (Samworth) said it was a privately owned business operating primarily in the manufacture of chilled food. Samworth ran a number of operating divisions which all had a high degree of autonomy. 2. Samworth explained that within the CSP market it operated three main divisions which supplied a wide range of major retailers: (a) Walker and Son (Walkers) predominantly manufactured own-label and branded pork pies ([]% of output). (b) Tamar Foods (Tamar) predominantly manufactured slices and pasties. (c) Ginsters of Cornwall (Ginsters) predominantly manufactured the Ginsters Brand ([]%), although there was some own-label production ([]%). Other divisions within the Samworth Group manufactured some branded product for Ginsters. 3. Samworth explained that one Division would respond to tenders for limited business.1 In tenders for cross category business Samworth would try to create the best customer proposition for the retailer, presenting a single offer. Samworth said that it tried to avoid duplicating investment around the Group by taking into account which Division / site: (a) should lead the negotiation as they had a trading relationship with the retailer, even if the product would be manufactured elsewhere in the Group; (b) specialised in manufacture of the particular product; and 1 For example, if the tender was for cold pies, then Tamar would respond. (c) had the capacity to handle the potential new business. 4. Samworth explained that, within savoury pastry, [] at that time. -

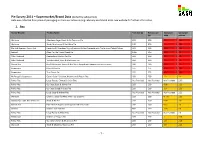

Full Supermarket Data

Pie Survey 2011 – Supermarket/Brand Data (Sorted by salt/portion) Data was collected from product packaging in store and online during February and March 2011. See website for further information. 1. Pies Brand/ Retailer Product Name Pack Size (g) Portion size Salt (g) per Salt (g) per (g) 100g portion Waitrose Aberdeen Angus Steak & Ale Top crust Pie 600 300 0.9 2.69 Waitrose Steak, Mushroom & Red Wine Pie 540 270 1 2.69 Marks & Spencer Gastro Pub (main for 1) Aberdeen Angus Steak and Stilton Pie made with Tuxford and Tebutt Stilton 260 260 1.03 2.68 Iceland (Meal for the Family) Steak Pie 1400 350 0.8 2.6 Alfie Chadwick Cumberland Chicken Pot Pie 260 260 1.0 2.5 Alfie Chadwick Yorkshire Beef, Beer & Mushroom Pie 260 260 1.0 2.5 Dorset Pies Beef, Mushroom, Bacon & Red Wine topped with caramelised onion scone 280 280 0.9 2.5 Pieminister Moo & Blue Pie 275 275 0.9 2.43 Pieminister Thai Chook Pie 275 275 0.9 2.43 McDougall's Uppercrust Gastro Style 2 Chicken, Mushroom & Bacon Pies 400 200 1.2 2.4 Pukka Pies Large Potato, Cheese & Onion Pies Not Provided Not Provided Not Provided 2.35 Pukka Pies Our Best Steak & Kidney Pie 200 200 0.98 2.33 Pukka Pies Our Best Baked All Steak Pie 200 200 1.0 2.33 Pukka Pies Large Steak & Kidney Pies Not Provided Not Provided Not Provided 2.33 Waitrose Chicken, Bacon & White Wine Top crust Pie 600 300 0.775 2.33 Sainsbury's Taste The Difference Steak & Ale Pie 250 250 0.93 2.31 Dorset Pies Ham Hock & Apple Cider topped with herb scone 280 280 0.8 2.3 Glenfell Chicken and Ham Pie 680 170 1.25 2.3 Pukka Pies -

Report Title

The Midlands Engine Science and Innovation Audit Volume 2: Supporting Annexes 30 September 2016 Science and Innovation Audit Volume 2: Supporting Annexes Contents Annex A: Organisations responding to the e-consultation ................................................. 1 Annex B: Midlands Engine Innovation Group Vision ........................................................... 2 Annex C: Theme-level data ..................................................................................................... 3 Annex D: Thematic workshop notes .................................................................................... 13 Annex E: Further Sci-Val data .............................................................................................. 32 Annex F: Long list of assets ................................................................................................. 46 Annex G: Case examples ...................................................................................................... 68 Annex H: Detailed market priority templates ...................................................................... 78 Annex I: E-consultation responses ...................................................................................... 98 Annex J: Driving competitiveness through our Enabling Competencies ...................... 109 Annex K: Innovation networks and behaviours ............................................................... 112 Science and Innovation Audit Volume 2: Supporting Annexes Annex A: Organisations responding