International Political Economy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Carlson Order Denying Motion for Subpoena

BEFORE THE NATIONAL ADJUDICATORY COUNCIL NASD ____________________________________ : In the Matter of : : Department of Enforcement, : DECISION : Complainant, : Complaint No. CAF980002 : vs. : : John Fiero : Dated: October 28, 2002 Jersey City, NJ : : : and : : : Pembroke Pines, FL : : and : : Fiero Brothers, Inc. : New York, NY, : : : Respondents : : ____________________________________: Firm and its president appeal findings that they, in cooperation with others, manipulated the market for certain securities and engaged in coercive conduct; and that they violated NASD's affirmative determination rule. Held, findings affirmed and sanctions of bar, expulsion, and fine upheld. Appearances For the Complainant Department of Enforcement: Robert L. Furst, Esq. and Jonathan I. Golomb, NASD Department of Enforcement. For the Respondents John Fiero and Fiero Brothers, Inc.: Martin H. Kaplan and Brian D. Graifman, Gusrae, Kaplan & Bruno; Martin P. Russo, MPR Law Practice, P.C.; Lewis D. Lowenfels, Tolins & Lowenfels. - 2 - Opinion John Fiero ("Fiero") and Fiero Brothers, Inc. ("Fiero Brothers" or "the Firm") (collectively, the "Fiero Respondents") appeal a December 6, 2000 decision of an NASD Hearing Panel. The Hearing Panel held that the Fiero Respondents, in cooperation with others and through the use of collusive trading activity, manipulated the market for certain securities, in violation of Section 10(b) of the Securities Exchange Act of 1934 ("Exchange Act"), Exchange Act Rule 10b-5, and Conduct Rules 2110 and 2120 and effected short sales of securities without making the affirmative determinations required by Conduct Rule 3370, in violation of Rules 2110 and 3370. In summary, the Hearing Panel found that the manipulation violation involved the Fiero Respondents' colluding with other short sellers to drive down the prices of several small-cap securities. -

The King's Nation: a Study of the Emergence and Development of Nation and Nationalism in Thailand

THE KING’S NATION: A STUDY OF THE EMERGENCE AND DEVELOPMENT OF NATION AND NATIONALISM IN THAILAND Andreas Sturm Presented for the Degree of Doctor of Philosophy of the University of London (London School of Economics and Political Science) 2006 UMI Number: U215429 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U215429 Published by ProQuest LLC 2014. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 I Declaration I hereby declare that the thesis, submitted in partial fulfillment o f the requirements for the degree of Doctor of Philosophy and entitled ‘The King’s Nation: A Study of the Emergence and Development of Nation and Nationalism in Thailand’, represents my own work and has not been previously submitted to this or any other institution for any degree, diploma or other qualification. Andreas Sturm 2 VV Abstract This thesis presents an overview over the history of the concepts ofnation and nationalism in Thailand. Based on the ethno-symbolist approach to the study of nationalism, this thesis proposes to see the Thai nation as a result of a long process, reflecting the three-phases-model (ethnie , pre-modem and modem nation) for the potential development of a nation as outlined by Anthony Smith. -

02. February.Pmd

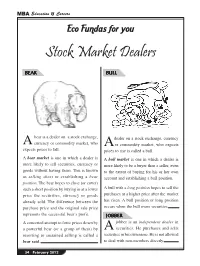

MBA Education & Careers Eco Fundas for you Stock Market Dealers BEAR BULL bear is a dealer on a stock exchange, dealer on a stock exchange, currency A currency or commodity market, who A or commodity market, who expects expects prices to fall. prices to rise is called a bull. A bear market is one in which a dealer is A bull market is one in which a dealer is more likely to sell securities, currency or more likely to be a buyer than a seller, even goods without having them. This is known to the extent of buying for his or her own as selling short or establishing a bear account and establishing a bull position. position. The bear hopes to close (or cover) such a short position by buying in at a lower A bull with a long position hopes to sell the price the securities, currency or goods purchases at a higher price after the market already sold. The difference between the has risen. A bull position or long position purchase price and the original sale price occurs when the bull owns securities. represents the successful bear’s profit. JOBBER A concerted attempt to force prices down by jobber is an independent dealer in a powerful bear (or a group of them) by A securities. He purchases and sells resorting to sustained selling is called a securities in his own name. He is not allowed bear raid. to deal with non-members directly. 34 February 2012 MBA Education & Careers ECO FUNDAS FOR YOU Stock Market Dealers CHICKEN PIG hickens are afraid to lose anything. -

The Direct Listing As a Competitor of the Traditional Ipo

The Direct Listing As a Competitor of the Traditional Ipo Research Paper – Law & Economics Course (IUS/05) Degree: Economics & Business, Dipartimento di Economia e Finanza Academic Year: 2019-2020 Name: Ludovico Morera Student Number: 216721 Supervisor: Prof. Pierluigi Matera The Direct Listing as a Competitor of the Traditional Ipo 2 Abstract In 2018, Spotify SA broke into the NYSE through an unusual direct listing, allowing it to become a publicly traded company without the high underwriting costs of a traditional Initial Public Offering that often deter companies from requesting to list. In order for such procedure to be possible, Spotify had to work closely with NYSE and SEC staff, which allowed for some amendments to their implementations of the Securities Act and the Securities Exchange Act. In this way, Spotify’s listing was done within the limits imposed by the U.S. market authorities. Several rumours concerning the direct listing arose, speculating that it may disrupt the American going public market and get past the standard firm-commitment underwriting procedures. This paper argues that these beliefs are largely wrong given the current regulatory limitations and tries to clarify for what firms direct listing is actually suitable. Furthermore, unlike the United Kingdom whose public exchanges have some experience, the NYSE faced such event for the first time; it follows that liability provisions under § 11 of the securities Act of 1933 may be attributed in different ways, especially due to the absence of an underwriter that may be held liable in case of material misstatements and omissions upon the registered documents. I find out that the direct listing can substitute the traditional IPO partially and only a restricted group of firms with some specific features could successfully do without an underwriter. -

Increased Stock Lending by Etfs and Its Effects on the Market

SSE Riga Student Research Papers 2018 : 4 (202) THE UNINTENDED CONSEQUENCES OF THE GROWTH IN ETFS: INCREASED STOCK LENDING BY ETFS AND ITS EFFECTS ON THE MARKET Authors: Grigoriţa Banaru Iryna Khomyak ISSN 1691-4643 ISBN 978-9984-822- November 2018 Riga The Unintended Consequences of the Growth in ETFs: Increased Stock Lending by ETFs and Its Effects on the Market Grigoriţa Banaru and Iryna Khomyak Supervisor: Tālis J. Putniņš November 2018 Riga Table of Contents Abstract ..................................................................................................................................... 5 1. Introduction .......................................................................................................................... 7 2. Literature Review and Hypotheses .................................................................................... 9 2.1. Short selling activity and its effects on the market efficiency ................................................ 9 2.1.1. Short interest and its positive impact on the market efficiency............................................ 9 2.1.2. Short selling and manipulation of prices ............................................................................ 11 2.2. ETFs and the equity market ................................................................................................... 12 2.2.1. The positive effects of ETFs on the market ....................................................................... 13 2.2.2. The dark side of ETFs ....................................................................................................... -

The Natural Resources Trap: Private Investment Without Public

The Natural Resources Trap Private Investment without Public Commitment edited by William Hogan and Federico Sturzenegger The MIT Press Cambridge, Massachusetts London, England ( 2010 Massachusetts Institute of Technology All rights reserved. No part of this book may be reproduced in any form by any elec- tronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from the publisher. For information about special quantity discounts, please e-mail special_sales@mitpress .mit.edu This book was set in Palatino on 3B2 by Asco Typesetters, Hong Kong. Printed and bound in the United States of America. Library of Congress Cataloging-in-Publication Data The natural resources trap : private investment without public commitment / edited by William Hogan and Federico Sturzenegger. p. cm. Includes bibliographical references and index. ISBN 978-0-262-01379-6 (hbk. : alk. paper) 1. Natural resources—Government policy. 2. Natural resources—Law and legislation. 3. Investments, Foreign. 4. Public—private sector cooperation. I. Hogan, William W. II. Sturzenegger, Federico. HC85.N36 2010 333.7—dc22 2009029574 10987654321 Index Adelman, Morris A., 18, 429, 461n28 Venezuela and, 415, 437–438, 442–444, Adler, Michael, 97 448–452, 455–458, 463n45 Agency issues Arellano, Cristina, 77 contract theory, 63–65 Argentina, xii, 7, 34, 36, 338, 368, 416 GRAB function and, 199, 220 Administrative Emergency Law and, 387 oil production contracts and, 229–231, Alsogaray, Alvaro, and, 389–390 235, 237–238, -

1 1 2 FINANCIAL CRISIS INQUIRY COMMISSION 3 4 Official Transcript

1 1 2 3 FINANCIAL CRISIS INQUIRY COMMISSION 4 5 Official Transcript 6 Hearing on "The Shadow Banking System" 7 Wednesday, May 5, 2010 8 Dirksen Senate Office Building, Room 538 9 Washington, D.C. 10 9:00 A.M. 11 12 COMMISSIONERS 13 PHIL ANGELIDES, Chairman 14 HON. BILL THOMAS, Vice Chairman 15 BROOKSLEY BORN, Commissioner 16 BYRON S. GEORGIOU, Commissioner 17 HON. BOB GRAHAM, Commissioner 18 KEITH HENNESSEY, Commissioner 19 DOUGLAS HOLTZ-EAKIN, Commissioner 20 HEATHER H. MURREN, Commissioner 21 JOHN W. THOMPSON, Commissioner 22 PETER J. WALLISON, Commissioner 23 24 Reported by: JANE W. BEACH 25 PAGES 1 - 369 2 1 Session 1: Investment Banks and the Shadow Banking System: 2 PAUL FRIEDMAN, Former Chief Operating Officer of 3 Fixed Income, Bear Stearns 4 SAMUEL MOLINARO, JR., Former Chief Financial 5 Officer and Chief Operating Officer, Bear Stearns 6 WARREN SPECTOR, former President and 7 Co-Chief Operating Officer, Bear Stearns 8 9 Session 2: Investment Banks and the Shadow Banking System: 10 JAMES E. CAYNE, Former Chairman and 11 Chief Executive Officer, Bear Stearns 12 ALAN D. SCHWARTZ, Former Chief Executive Officer, 13 Bear Stearns 14 15 16 17 18 19 20 21 22 23 24 3 1 Session 3: SEC Regulation of Investment Banks: 2 CHARLES CHRISTOPHER COX, Former Chairman 3 U.S. Securities and Exchange Commission 4 WILLIAM H. DONALDSON, Former Chairman, U.S. 5 Securities and Exchange Commission 6 H. DAVID KOTZ, Inspector General 7 U.S. Securities and Exchange Commission 8 ERIK R. SIRRI, Former Director, Division of 9 Trading & Markets, U.S. -

Book Reviews

Vanderbilt Law Review Volume 8 Issue 2 Issue 2 - A Symposium on Article 14 Unemployment Insurance 2-1955 Book Reviews Lloyd P. Stryker (reviewer) Howard J. Graham (reviewer) Follow this and additional works at: https://scholarship.law.vanderbilt.edu/vlr Part of the Commercial Law Commons, Insurance Law Commons, and the Labor and Employment Law Commons Recommended Citation Lloyd P. Stryker (reviewer) and Howard J. Graham (reviewer), Book Reviews, 8 Vanderbilt Law Review 525 (2019) Available at: https://scholarship.law.vanderbilt.edu/vlr/vol8/iss2/14 This Symposium is brought to you for free and open access by Scholarship@Vanderbilt Law. It has been accepted for inclusion in Vanderbilt Law Review by an authorized editor of Scholarship@Vanderbilt Law. For more information, please contact [email protected]. BOOK REVIEWS THE AMERICAN LAWYER By Albert P. Blaustein and Charles 0. Porter, with Charles T. Duncan. Chicago: The University of Chicago Press, 1954. Pp. xiii, 360. $5.50. It is a refreshing thing to come across a book like that written by Albert P. Blaustein and Charles 0. Porter, with Charles T. Duncan, and the University of Chicago Press should be complimented for pub- lishing so valuable a volume. It might have been a very" dull and tedious book but it is not. Indeed, it is a singularly able performance. In it will be found a simple, well written and scholarly account of the legal profession. I have been delighted with its clarity, its insight and its good style. A survey by the authors of this book was espoused by the Carnegie Foundation and the American Bar Association at a cost of a quarter of a million dollars. -

WALL STREET in the AMERICAN NOVEL Wayne W. Westbrook A

WALL STREET IN THE AMERICAN NOVEL Wayne W. Westbrook A Dissertation Submitted to the Graduate School of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY August 1972 p © 1972 WAYNE WILLIAM WESTBROOK ALL RIGHTS RESERVED IH ABSTRACT Wall Street is construed to represent the American financial center, La Salle Street in Chicago, State StreetiinbBoston and Third Street in Philadelphia as well as New York's lower Manhattan district. The novels and stories considered are those in which the financial center serves a primary function, either in influencing plot, character or in providing the background and atmosphere for the main action, Both archetypal and textual analysis are applied in seeing the recurrent motifs in the novel of high finance, patterns and themes which are fully articulated and developed in the late nineteenth-century version, yet which are not found to bear an influence on later financial fiction. The reason for this is that the American literary artist has had a prejudicial view of high finance and speculation which is rooted in his cultural heritage of the Puritan opposition to playing or gaming as a way to wealth and success. The writer's attitude, therefore, is largely con demnatory, regarding an individual's involvement with the financial marketplace as a form of personal corruption, profligacy and degen eracy. Further, the idea of the sin and evil of Wall Street has as its probable historical source the volatile course that American finance has traced since the post-Civil War industrial age, in the highly cyclical and repetitive pattern of boom and bust periods. -

The Rearguard of Freedom: the John Birch Society and the Development

The Rearguard of Freedom: The John Birch Society and the Development of Modern Conservatism in the United States, 1958-1968 by Bart Verhoeven, MA (English, American Studies), BA (English and Italian Languages) Thesis submitted to the University of Nottingham for the degree of Doctor of Philosophy at the Faculty of Arts July 2015 Abstract This thesis aims to investigate the role of the anti-communist John Birch Society within the greater American conservative field. More specifically, it focuses on the period from the Society's inception in 1958 to the beginning of its relative decline in significance, which can be situated after the first election of Richard M. Nixon as president in 1968. The main focus of the thesis lies on challenging more traditional classifications of the JBS as an extremist outcast divorced from the American political mainstream, and argues that through their innovative organizational methods, national presence, and capacity to link up a variety of domestic and international affairs to an overarching conspiratorial narrative, the Birchers were able to tap into a new and powerful force of largely white suburban conservatives and contribute significantly to the growth and development of the post-war New Right. For this purpose, the research interrogates the established scholarship and draws upon key primary source material, including official publications, internal communications and the private correspondence of founder and chairman Robert Welch as well as other prominent members. Acknowledgments The process of writing a PhD dissertation seems none too dissimilar from a loving marriage. It is a continuous and emotionally taxing struggle that leaves the individual's ego in constant peril, subjugates mind and soul to an incessant interplay between intense passion and grinding routine, and in most cases should not drag on for over four years. -

Doing Battle with Short Sellers the Conflicted Role of Blockholders In

Author’s Accepted Manuscript Doing battle with short sellers: The conflicted role of blockholders in bear raids Naveen Khanna, Richmond D. Mathews www.elsevier.com/locate/jfec PII: S0304-405X(12)00132-8 DOI: http://dx.doi.org/10.1016/j.jfineco.2012.06.006 Reference: FINEC2184 To appear in: Journal of Financial Economics Received date: 12 July 2011 Revised date: 2 November 2011 Accepted date: 3 November 2011 Cite this article as: Naveen Khanna and Richmond D. Mathews, Doing battle with short sellers: The conflicted role of blockholders in bear raids, Journal of Financial Economics, http://dx.doi.org/10.1016/j.jfineco.2012.06.006 This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting galley proof before it is published in its final citable form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain. Doing battle with short sellers: the conflicted role of blockholders in bear raids ? Naveen Khannaa, Richmond D. Mathewsb; ∗ aEli Broad College of Business, Michigan State University, East Lansing, MI, 48824, USA bRobert H. Smith School of Business, University of Maryland, College Park, MD, 20742, USA Abstract If short sellers can destroy firm value by manipulating prices down, an informed blockholder has a powerful natural incentive to protect the value of his stake by trading against them. -

Great Deformation: the Corruption of Capitalism in America

4/C PROCESS + PANTONE 8402 GRITTY MATTE UV 100#PAPER. ECONOMICS / BUSINESS $35.00 / $38.00 can IN THE WORDS OF DAVID STOCKMAN THE GREAT DEFORMATION is a searing look at Washington’s craven response to the recent myriad of financial crises and fiscal cliffs. It counters conven- ER D “ At the heart of the Great Deformation is a rogue central bank tional wisdom with an eighty-year revisionist history of how LAN G N E that has abandoned every vestige of sound money.” the American state—especially the Federal Reserve—has fallen ARYL ARYL C prey to the politics of crony capitalism and the ideologies of fiscal stimulus, monetary central planning, and financial bail- DAVID A. STOCKMAN was elected as a “ In the years after 1980, America had undergone the equivalent of outs. These forces have left the public sector teetering on the Michigan congressman in 1976 and joined the Reagan White a national leveraged buyout...[and was] now saddled with edge of political dysfunction and fiscal collapse and have caused House in 1981. Serving as budget director, he was one of the America’s private enterprise foundation to morph into a spec- more in combined public and private debt.” key architects of the Reagan Revolution plan to reduce taxes, $30 trillion ulative casino that swindles the masses and enriches the few. cut spending, and shrink the role of government. He joined Defying right- and left-wing boxes, David Stockman Salomon Brothers in 1985 and later became one of the early The Corruption of Capitalism provides a catalogue of corrupters and defenders of sound partners of the Blackstone Group.