The Alternative Uptick Rule

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Comment Letter

The Honorable Mary Schapiro Chairman, U.S. Securities and Exchange Commission Subject: S7-08-09 Proposed Amendments to SHO Date: 21 September 2009 Dear Chairman Schapiro, The Commission has taken an important step in focusing on the alternative uptick rule as the approach to solving the short sale problem. It is simple to understand, easy to implement, requires virtually no technology costs, reduces compliance to making certain that short sales are properly marked, and most importantly, prevents short selling from proactively driving the price of a stock lower. Not only does it faithfully replicate the old uptick rule it improves upon it by making each and every short sale a liquidity providing transaction. As best as I can determine, the Commission is proposing the alternative uptick rule be permanently implemented on a market wide basis. However, as the discussion switched back forth between the proposed uptick, modified uptick and alternative uptick rules, and what was then and what is now, it was not entirely clear to me as to whether its implementation would be based on a circuit breaker e.g. (10,15 or 20%). Imposing any circuit breaker would be a serious mistake. It will neither solve the problem Congress has with not returning to the uptick rule nor allay the public investor’s distrust of the market and its belief that short selling drives stock prices lower. That mistake will be realized in the next significant downturn in the market and the Commission will be back before Congress having to prove that short selling was not a contributing factor. -

Are Short Selling Restrictions Effective?

Are Short Selling Restrictions Effective?∗ Yashar H. Barardehi Andrew Bird Stephen A. Karolyi Thomas G. Ruchti November 30, 2018 Abstract We exploit SEC Rule 201 to study the price and trading effects of short selling restric- tions. The policy requires exchanges to implement an uptick rule until the next day's market close for stocks that cross a −10% intraday return threshold, generating rare quasi-experimental variation in short selling restrictions. On average, these restrictions increase daily returns by 30.6 bps, reduce seller-initiated volume by 4.5%, and increase off-exchange volume by 1.7%. These direct effects, which contrast with the extant literature, are concentrated in down markets, suggesting that the rule is most effective in periods of most concern to regulators. However, consistent with the substitution of potential short sales, we find significant offsetting spillover effects for peer stocks. Together, our findings yield new and timely policy implications and contribute to our understanding of short seller behavior. JEL Classification: G12, G14. Keywords: short selling, uptick rule, securities regulation, Rule 201, short-sale restrictions ∗We are grateful for comments received from Rui Albuequerque, Torben Andersen, Kelley Bergsma, Dan Bernhardt, Julio Crego, Arthur Denzau, Hans Degryse, Brent Glover, Peter Haslag, Burton Hollifield, Eric Hughson, Olivia Huseman, Tim Johnson, Nikolaos Karagiannis, Daniel Karney, Stefan Lewellen, Zhi Li, Vitaly Meursault, Nate Neligh, Lars Nord´en,Dave Porter, John Ritter, Michael Schneider, Duane Seppi, Timothy Shields, Esad Smajlbegovic (discussant), Dustin Tracy, Marc Weidenmier, Andrew Zhang, and seminar participants at Carnegie Mellon University, Chapman University, Ohio University, Oklahoma, and SAFE Market Microstructure 2018. -

Banyan Asset Management, Inc

“Capitulation” Market Commentary – October 2008 By Frank C. Fontana, CFA President, Banyan Asset Management, Inc. Written September 30, 2008 – www.banyan-asset.com The final reading of Gross Domestic Product (GDP) shows that the value of goods and services produced in the U.S. grew 2.8% in the second quarter. On its own, this GDP figure indicates a modestly growing economy. Of course, the second quarter ended June 30, so effects of the recent financial market volatility will not show up in GDP until the third quarter, which ended today. The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales”. The NBER tends to work on delay, however. For example, it declared on November 26, 2001, roughly eight months after the fact, that the U.S. economy entered a recession in March 2001. At Banyan Asset Management, our hypothesis is that the turmoil occurring in the U.S. economy has its roots going back to the 1990s. Technology brought tremendous gains in productivity in the 1990s, which led to a boom in the stock prices of growing technology companies. This bubble burst in mid-2000 while the benchmark Fed Funds rate was 6.5%. Because of the recession in 2001 and the September 11, 2001 terrorist attacks, the Fed had to lower the Fed Funds rate drastically to boost the economy, finally settling at 1.0% by June 2003. -

Carlson Order Denying Motion for Subpoena

BEFORE THE NATIONAL ADJUDICATORY COUNCIL NASD ____________________________________ : In the Matter of : : Department of Enforcement, : DECISION : Complainant, : Complaint No. CAF980002 : vs. : : John Fiero : Dated: October 28, 2002 Jersey City, NJ : : : and : : : Pembroke Pines, FL : : and : : Fiero Brothers, Inc. : New York, NY, : : : Respondents : : ____________________________________: Firm and its president appeal findings that they, in cooperation with others, manipulated the market for certain securities and engaged in coercive conduct; and that they violated NASD's affirmative determination rule. Held, findings affirmed and sanctions of bar, expulsion, and fine upheld. Appearances For the Complainant Department of Enforcement: Robert L. Furst, Esq. and Jonathan I. Golomb, NASD Department of Enforcement. For the Respondents John Fiero and Fiero Brothers, Inc.: Martin H. Kaplan and Brian D. Graifman, Gusrae, Kaplan & Bruno; Martin P. Russo, MPR Law Practice, P.C.; Lewis D. Lowenfels, Tolins & Lowenfels. - 2 - Opinion John Fiero ("Fiero") and Fiero Brothers, Inc. ("Fiero Brothers" or "the Firm") (collectively, the "Fiero Respondents") appeal a December 6, 2000 decision of an NASD Hearing Panel. The Hearing Panel held that the Fiero Respondents, in cooperation with others and through the use of collusive trading activity, manipulated the market for certain securities, in violation of Section 10(b) of the Securities Exchange Act of 1934 ("Exchange Act"), Exchange Act Rule 10b-5, and Conduct Rules 2110 and 2120 and effected short sales of securities without making the affirmative determinations required by Conduct Rule 3370, in violation of Rules 2110 and 3370. In summary, the Hearing Panel found that the manipulation violation involved the Fiero Respondents' colluding with other short sellers to drive down the prices of several small-cap securities. -

02. February.Pmd

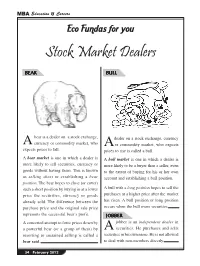

MBA Education & Careers Eco Fundas for you Stock Market Dealers BEAR BULL bear is a dealer on a stock exchange, dealer on a stock exchange, currency A currency or commodity market, who A or commodity market, who expects expects prices to fall. prices to rise is called a bull. A bear market is one in which a dealer is A bull market is one in which a dealer is more likely to sell securities, currency or more likely to be a buyer than a seller, even goods without having them. This is known to the extent of buying for his or her own as selling short or establishing a bear account and establishing a bull position. position. The bear hopes to close (or cover) such a short position by buying in at a lower A bull with a long position hopes to sell the price the securities, currency or goods purchases at a higher price after the market already sold. The difference between the has risen. A bull position or long position purchase price and the original sale price occurs when the bull owns securities. represents the successful bear’s profit. JOBBER A concerted attempt to force prices down by jobber is an independent dealer in a powerful bear (or a group of them) by A securities. He purchases and sells resorting to sustained selling is called a securities in his own name. He is not allowed bear raid. to deal with non-members directly. 34 February 2012 MBA Education & Careers ECO FUNDAS FOR YOU Stock Market Dealers CHICKEN PIG hickens are afraid to lose anything. -

The Direct Listing As a Competitor of the Traditional Ipo

The Direct Listing As a Competitor of the Traditional Ipo Research Paper – Law & Economics Course (IUS/05) Degree: Economics & Business, Dipartimento di Economia e Finanza Academic Year: 2019-2020 Name: Ludovico Morera Student Number: 216721 Supervisor: Prof. Pierluigi Matera The Direct Listing as a Competitor of the Traditional Ipo 2 Abstract In 2018, Spotify SA broke into the NYSE through an unusual direct listing, allowing it to become a publicly traded company without the high underwriting costs of a traditional Initial Public Offering that often deter companies from requesting to list. In order for such procedure to be possible, Spotify had to work closely with NYSE and SEC staff, which allowed for some amendments to their implementations of the Securities Act and the Securities Exchange Act. In this way, Spotify’s listing was done within the limits imposed by the U.S. market authorities. Several rumours concerning the direct listing arose, speculating that it may disrupt the American going public market and get past the standard firm-commitment underwriting procedures. This paper argues that these beliefs are largely wrong given the current regulatory limitations and tries to clarify for what firms direct listing is actually suitable. Furthermore, unlike the United Kingdom whose public exchanges have some experience, the NYSE faced such event for the first time; it follows that liability provisions under § 11 of the securities Act of 1933 may be attributed in different ways, especially due to the absence of an underwriter that may be held liable in case of material misstatements and omissions upon the registered documents. I find out that the direct listing can substitute the traditional IPO partially and only a restricted group of firms with some specific features could successfully do without an underwriter. -

Increased Stock Lending by Etfs and Its Effects on the Market

SSE Riga Student Research Papers 2018 : 4 (202) THE UNINTENDED CONSEQUENCES OF THE GROWTH IN ETFS: INCREASED STOCK LENDING BY ETFS AND ITS EFFECTS ON THE MARKET Authors: Grigoriţa Banaru Iryna Khomyak ISSN 1691-4643 ISBN 978-9984-822- November 2018 Riga The Unintended Consequences of the Growth in ETFs: Increased Stock Lending by ETFs and Its Effects on the Market Grigoriţa Banaru and Iryna Khomyak Supervisor: Tālis J. Putniņš November 2018 Riga Table of Contents Abstract ..................................................................................................................................... 5 1. Introduction .......................................................................................................................... 7 2. Literature Review and Hypotheses .................................................................................... 9 2.1. Short selling activity and its effects on the market efficiency ................................................ 9 2.1.1. Short interest and its positive impact on the market efficiency............................................ 9 2.1.2. Short selling and manipulation of prices ............................................................................ 11 2.2. ETFs and the equity market ................................................................................................... 12 2.2.1. The positive effects of ETFs on the market ....................................................................... 13 2.2.2. The dark side of ETFs ....................................................................................................... -

1 1 2 FINANCIAL CRISIS INQUIRY COMMISSION 3 4 Official Transcript

1 1 2 3 FINANCIAL CRISIS INQUIRY COMMISSION 4 5 Official Transcript 6 Hearing on "The Shadow Banking System" 7 Wednesday, May 5, 2010 8 Dirksen Senate Office Building, Room 538 9 Washington, D.C. 10 9:00 A.M. 11 12 COMMISSIONERS 13 PHIL ANGELIDES, Chairman 14 HON. BILL THOMAS, Vice Chairman 15 BROOKSLEY BORN, Commissioner 16 BYRON S. GEORGIOU, Commissioner 17 HON. BOB GRAHAM, Commissioner 18 KEITH HENNESSEY, Commissioner 19 DOUGLAS HOLTZ-EAKIN, Commissioner 20 HEATHER H. MURREN, Commissioner 21 JOHN W. THOMPSON, Commissioner 22 PETER J. WALLISON, Commissioner 23 24 Reported by: JANE W. BEACH 25 PAGES 1 - 369 2 1 Session 1: Investment Banks and the Shadow Banking System: 2 PAUL FRIEDMAN, Former Chief Operating Officer of 3 Fixed Income, Bear Stearns 4 SAMUEL MOLINARO, JR., Former Chief Financial 5 Officer and Chief Operating Officer, Bear Stearns 6 WARREN SPECTOR, former President and 7 Co-Chief Operating Officer, Bear Stearns 8 9 Session 2: Investment Banks and the Shadow Banking System: 10 JAMES E. CAYNE, Former Chairman and 11 Chief Executive Officer, Bear Stearns 12 ALAN D. SCHWARTZ, Former Chief Executive Officer, 13 Bear Stearns 14 15 16 17 18 19 20 21 22 23 24 3 1 Session 3: SEC Regulation of Investment Banks: 2 CHARLES CHRISTOPHER COX, Former Chairman 3 U.S. Securities and Exchange Commission 4 WILLIAM H. DONALDSON, Former Chairman, U.S. 5 Securities and Exchange Commission 6 H. DAVID KOTZ, Inspector General 7 U.S. Securities and Exchange Commission 8 ERIK R. SIRRI, Former Director, Division of 9 Trading & Markets, U.S. -

ICI Webinar: Trading

Current Market Structure Issues in the U.S. Equity Markets // November 3, 2009 Davis Polk & Wardwell LLP CURRENT MARKET STRUCTURE ISSUES IN THE U.S. EQUITY MARKETS1 I. The Framework of the Equity Trading Markets. The regulatory framework governing the U.S. equity markets was given its current shape by the SEC’s adoption of Regulation ATS in December 1998 and Regulation NMS in June 2005. These regulations revised and codified a series of rules adopted by the SEC in the years surrounding the enactment of the Securities Act Amendments of 1975 (the “1975 Amendments”). The regulations also built on a structure of self-regulatory organization rules, including rules of the exchanges and the Financial Industry Regulatory Authority (“FINRA”), which was formed in 2007 through the merger of the National Association of Securities Dealers, Inc. (“NASD”), and the member regulation functions of the New York Stock Exchange (“NYSE”). II. Regulation ATS. The SEC adopted Regulation ATS and accompanying Rule 3b-16 to update the scheme of exchange regulation devised by Congress in 1934 in an era in which order interaction and price discovery functions were best fulfilled by trading on physical exchange floors. Exchange Act Release No. 40760 (December 8, 1998) (adopting Regulation ATS and Rule 3b-16) (the “Regulation ATS Adopting Release”). A. The Securities Exchange Act of 1934 (the “Exchange Act”) codified the then prevalent system of exchanges operating as membership organizations that established trading rules and imposed broker-dealer capital, business -

Informed Trading and Co-Illiquidity

Informed Trading and Co-Illiquidity Søren Hvidkjær∗ Massimo Massay Aleksandra Rze´znikz February 23, 2019 Abstract We study the link between informed trading and co-movement in liquidity. We argue that investors concerned with liquidity and fire sale shocks respond to an increase in informed trading by shifting their portfolios away from stocks with high information asymmetry. Their rebalancing results in a substitution in ownership away from the very same investors that induce financial fragility and co-movement in liquidity. This reduces co-illiquidity of the affected stocks. We exploit a unique natural experiment that increases the incentives of informed traders to trade. Our results suggest that informed traders reduce the exposure to co-movement in liq- uidity: one of the major problems during the latest global financial crisis. Keywords: Short-sales constraints, liquidity, commonality, informed trading JEL classification: G12, G14, G15 We thank Ben Sand, Michael Roberts, and brown bag participants at the Schulich School of Business and Vienna University of Economics and Business. ∗Copenhagen Business School, e-mail: sh.fi@cbs.dk. yINSEAD, e-mail: [email protected]. zWirtschaftsuniversit¨at Wien, e-mail: [email protected]. 1 Introduction The last decades have seen the parallel rise of both informed trading and liquidity trading. The first trend { the rise of informed trading { is linked to the development of new technologies and new data that has concentrated trading power in the hands of few relatively more informed investors (e.g., short sellers, hedge funds). While their trade has made the market more efficient, still it has also increased the amount of information asymmetry due to the trade of more informed investors. -

WALL STREET in the AMERICAN NOVEL Wayne W. Westbrook A

WALL STREET IN THE AMERICAN NOVEL Wayne W. Westbrook A Dissertation Submitted to the Graduate School of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY August 1972 p © 1972 WAYNE WILLIAM WESTBROOK ALL RIGHTS RESERVED IH ABSTRACT Wall Street is construed to represent the American financial center, La Salle Street in Chicago, State StreetiinbBoston and Third Street in Philadelphia as well as New York's lower Manhattan district. The novels and stories considered are those in which the financial center serves a primary function, either in influencing plot, character or in providing the background and atmosphere for the main action, Both archetypal and textual analysis are applied in seeing the recurrent motifs in the novel of high finance, patterns and themes which are fully articulated and developed in the late nineteenth-century version, yet which are not found to bear an influence on later financial fiction. The reason for this is that the American literary artist has had a prejudicial view of high finance and speculation which is rooted in his cultural heritage of the Puritan opposition to playing or gaming as a way to wealth and success. The writer's attitude, therefore, is largely con demnatory, regarding an individual's involvement with the financial marketplace as a form of personal corruption, profligacy and degen eracy. Further, the idea of the sin and evil of Wall Street has as its probable historical source the volatile course that American finance has traced since the post-Civil War industrial age, in the highly cyclical and repetitive pattern of boom and bust periods. -

Shorting Restrictions, Liquidity, and Returns

Shorting restrictions, liquidity, and returns Charles M. Jones Columbia University September 2006 This paper Helps us understand the historical context underlying the uptick rule. Examines three discrete events from the U.S. in the 1930’s that made shorting more difficult or more expensive: 1931 prohibition of short sales on downticks 1932 requirement that brokers get written permission to lend shares 1938 SEC uptick rule Measures time‐series and cross‐sectional effects on: returns volatility liquidity Shorting in the 1920s Popular among professional traders in the U.S. Shorting and share lending were highly developed, with little regulatory oversight or restrictions. no uptick rule no requirement to locate shares before shorting minimum margins set by the exchange or by the broker Near the close each day, NYSE members got together in the “loan crowd” at a post on the floor of the exchange to borrow and lend shares. Centralized market probably reduced search costs. A 1930s timeline of shorting restrictions Short sellers were blamed for the stock market crash. Beginning in 1930: political pressure to rein in or even ban shorting; many holders urged not to lend out their shares for shorting. 21 Sep 1931: all short sales prohibited on the NYSE for two days as emergency measure when England abandons gold standard 21 Sep 1931: NYSE requires daily short interest reports from all members 6 Oct 1931: all short sales prohibited below last sale price 1 Apr 1932: brokers required to get written signatures from investors allowing hypothecation. Late spring 1932: US Senate releases list of biggest shorts 8 Feb 1938: SEC imposes strict uptick rule 1 Apr 1932: written permission to lend Previously any stock held in “street name” could be lent to shorts (no distinction between cash and margin accounts).