SEC Enforcement Actions and Issuer Litigation in the Context of a “Short Attack”

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Comment Letter

The Honorable Mary Schapiro Chairman, U.S. Securities and Exchange Commission Subject: S7-08-09 Proposed Amendments to SHO Date: 21 September 2009 Dear Chairman Schapiro, The Commission has taken an important step in focusing on the alternative uptick rule as the approach to solving the short sale problem. It is simple to understand, easy to implement, requires virtually no technology costs, reduces compliance to making certain that short sales are properly marked, and most importantly, prevents short selling from proactively driving the price of a stock lower. Not only does it faithfully replicate the old uptick rule it improves upon it by making each and every short sale a liquidity providing transaction. As best as I can determine, the Commission is proposing the alternative uptick rule be permanently implemented on a market wide basis. However, as the discussion switched back forth between the proposed uptick, modified uptick and alternative uptick rules, and what was then and what is now, it was not entirely clear to me as to whether its implementation would be based on a circuit breaker e.g. (10,15 or 20%). Imposing any circuit breaker would be a serious mistake. It will neither solve the problem Congress has with not returning to the uptick rule nor allay the public investor’s distrust of the market and its belief that short selling drives stock prices lower. That mistake will be realized in the next significant downturn in the market and the Commission will be back before Congress having to prove that short selling was not a contributing factor. -

Barry Minkow

Barry Minkow Barry Jay Minkow (born March 17, 1967) is a former businessman, pastor and convicted felon. While still in high school, he founded ZZZZ Best (pronounced Zee Best), which appeared to be an immensely successful carpet-cleaning and restoration company. However, it was actually a front to attract investment for a massive Ponzi scheme. It collapsed in 1987, costing investors and lenders $100 million—one of the largest investment frauds ever perpetrated by a single person, as well as one of the largest accounting frauds in history. The scheme is often used as a case study of accounting fraud. After being released from jail, Minkow became a preacher and a fraud investigator, and spoke at schools about ethics. This all came to an end in 2011, when he admitted to helping deliberately drive down the stock price of homebuilder Lennar and was ordered back to prison. At first, Minkow struggled to meet basic expenses. Two banks closed his business account because California law didn't allow minors to sign binding contracts, including checks. He was also plagued by customer complaints and demands for payment from suppliers. At times, he found it difficult even to meet payroll. Faced with a shortage of operating capital, he financed his business via check kiting, stealing and selling his grandmother's jewelry, staging break-ins at his offices, and running up fraudulent credit card charges. After that, Minkow branched into the "insurance restoration" business. With the help of Tom Padgett, an insurance claims adjuster, Minkow forged numerous documents claiming that ZZZZ Best was involved in numerous restoration projects for Padgett's company. -

![Gary Zeune: [00:00:00] Every Fraud That We Talk About Is a Situation Where Really Smart People to Do Really Stupid Stuff](https://docslib.b-cdn.net/cover/5148/gary-zeune-00-00-00-every-fraud-that-we-talk-about-is-a-situation-where-really-smart-people-to-do-really-stupid-stuff-55148.webp)

Gary Zeune: [00:00:00] Every Fraud That We Talk About Is a Situation Where Really Smart People to Do Really Stupid Stuff

Gary Zeune: [00:00:00] Every fraud that we talk about is a situation where really smart people to do really stupid stuff. Peter Margaritis: [00:00:17] Welcome to Change Your Mindset Podcast, formerly known as Improv is No Joke, where it's all about believing that strong communication skills are the best way in delivering your technical accounting knowledge and growing your business. An effective way of building stronger communication skills is by embracing the principles of applied improvisation. Peter Margaritis: [00:00:37] Your host is Peter Margaritis, CPA, a.k.a. The Accidental Accountant. And he will interview financial professionals and business leaders to find their secret in building stronger relationships with their clients, customers, associates, and peers, all the while growing their businesses. So, let's start the show. Peter Margaritis: [00:01:04] Welcome to Episode 21. My guest today is Gary Zeune, CPA. And his consulting practice provide CPAs, attorneys, and executives with hands-on experience in fraud, auditing, and corporate strategy performance improvement. Prior to forming his consulting practice, Gary was an Assistant Vice President of Corporate Finance at the Ohio Company, a Columbus, Ohio investment banking firm. Peter Margaritis: [00:01:30] He also spent more than five years in treasury and Finance at Wendy's International where he was responsible for mergers and acquisitions, financial and SEC reporting, and corporate finance. Gary has the only speaker bureau in the country specializing in white-collar criminals, The Pros and The Cons. His 40 plus ex-con speakers tell their stories of how and why they embezzled, took kickbacks, and cooked the books to the tune of $2.7 billion. -

Julian Robertson: a Tiger in the Land of Bulls and Bears

STRACHMAN_FM_pages 6/29/04 11:35 AM Page i Julian Robertson A Tiger in the Land of Bulls and Bears Daniel A. Strachman John Wiley & Sons, Inc. STRACHMAN_FM_pages 6/29/04 11:35 AM Page i Julian Robertson A Tiger in the Land of Bulls and Bears Daniel A. Strachman John Wiley & Sons, Inc. STRACHMAN_FM_pages 6/29/04 11:35 AM Page ii Copyright © 2004 by Daniel A. Strachman. All rights reserved. Published by John Wiley & Sons, Inc., Hoboken, New Jersey. Published simultaneously in Canada. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permis- sion of the Publisher, or authorization through payment of the appropriate per- copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, 978-750-8400, fax 978-646-8600, or on the web at www. copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, 201-748-6011, fax 201-748-6008. Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifically disclaim any implied warranties of merchantability or fit- ness for a particular purpose. -

Are Short Selling Restrictions Effective?

Are Short Selling Restrictions Effective?∗ Yashar H. Barardehi Andrew Bird Stephen A. Karolyi Thomas G. Ruchti November 30, 2018 Abstract We exploit SEC Rule 201 to study the price and trading effects of short selling restric- tions. The policy requires exchanges to implement an uptick rule until the next day's market close for stocks that cross a −10% intraday return threshold, generating rare quasi-experimental variation in short selling restrictions. On average, these restrictions increase daily returns by 30.6 bps, reduce seller-initiated volume by 4.5%, and increase off-exchange volume by 1.7%. These direct effects, which contrast with the extant literature, are concentrated in down markets, suggesting that the rule is most effective in periods of most concern to regulators. However, consistent with the substitution of potential short sales, we find significant offsetting spillover effects for peer stocks. Together, our findings yield new and timely policy implications and contribute to our understanding of short seller behavior. JEL Classification: G12, G14. Keywords: short selling, uptick rule, securities regulation, Rule 201, short-sale restrictions ∗We are grateful for comments received from Rui Albuequerque, Torben Andersen, Kelley Bergsma, Dan Bernhardt, Julio Crego, Arthur Denzau, Hans Degryse, Brent Glover, Peter Haslag, Burton Hollifield, Eric Hughson, Olivia Huseman, Tim Johnson, Nikolaos Karagiannis, Daniel Karney, Stefan Lewellen, Zhi Li, Vitaly Meursault, Nate Neligh, Lars Nord´en,Dave Porter, John Ritter, Michael Schneider, Duane Seppi, Timothy Shields, Esad Smajlbegovic (discussant), Dustin Tracy, Marc Weidenmier, Andrew Zhang, and seminar participants at Carnegie Mellon University, Chapman University, Ohio University, Oklahoma, and SAFE Market Microstructure 2018. -

Banyan Asset Management, Inc

“Capitulation” Market Commentary – October 2008 By Frank C. Fontana, CFA President, Banyan Asset Management, Inc. Written September 30, 2008 – www.banyan-asset.com The final reading of Gross Domestic Product (GDP) shows that the value of goods and services produced in the U.S. grew 2.8% in the second quarter. On its own, this GDP figure indicates a modestly growing economy. Of course, the second quarter ended June 30, so effects of the recent financial market volatility will not show up in GDP until the third quarter, which ended today. The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales”. The NBER tends to work on delay, however. For example, it declared on November 26, 2001, roughly eight months after the fact, that the U.S. economy entered a recession in March 2001. At Banyan Asset Management, our hypothesis is that the turmoil occurring in the U.S. economy has its roots going back to the 1990s. Technology brought tremendous gains in productivity in the 1990s, which led to a boom in the stock prices of growing technology companies. This bubble burst in mid-2000 while the benchmark Fed Funds rate was 6.5%. Because of the recession in 2001 and the September 11, 2001 terrorist attacks, the Fed had to lower the Fed Funds rate drastically to boost the economy, finally settling at 1.0% by June 2003. -

Fairfax Financial Holdings Limited

FAIRFAX FINANCIAL HOLDINGS LIMITED To Our Shareholders: Last year we told you that we had an excellent year building intrinsic value even though it was not obvious in the numbers. This year was even better but it was completely masked by hedging losses and unrealized mark to market losses caused by fluctuations in the market price of our investments. Our insurance and reinsurance companies had an outstanding year in 2013 with a combined ratio of 92.7% with excellent reserving and a record underwriting profit of $440 million(1). We also realized $1.4 billion of net gains from our investment portfolio (predominantly from our common stock portfolio). Excluding all hedging losses and before mark to market fluctuations in our investment portfolio, we earned $1.9 billion in pre-tax income. Including all hedging losses and mark to market fluctuations in our investment portfolio, we reported a $565 million after-tax loss for 2013. We expect the unrealized mark to market losses to reverse in the future (as of February 28, 2014, we had an unrealized mark to market gain in our investment portfolio of more than $1 billion – after tax, this would have eliminated our net loss in 2013). The table below shows all this clearly: 2013 Results Underwriting profit 440 Investment income and other 382 Operating income 822 Runoff (excluding investment gains and losses) 77 Interest expense (211) Corporate overhead and other (125) Pre-tax income excluding net investment gains (losses) 563 Realized investment gains 1,380 Pre-tax income including realized investment gains 1,943 Unrealized investment losses (mostly from bonds) (962) Hedging losses (1,982) Pre-tax loss (1,001) Income tax recovery 436 Net loss (565) So all in, the result was a net loss of $565 million and a 7.8% decrease in book value (adjusted for the $10 per share dividend paid) to $339 per share. -

Carlson Order Denying Motion for Subpoena

BEFORE THE NATIONAL ADJUDICATORY COUNCIL NASD ____________________________________ : In the Matter of : : Department of Enforcement, : DECISION : Complainant, : Complaint No. CAF980002 : vs. : : John Fiero : Dated: October 28, 2002 Jersey City, NJ : : : and : : : Pembroke Pines, FL : : and : : Fiero Brothers, Inc. : New York, NY, : : : Respondents : : ____________________________________: Firm and its president appeal findings that they, in cooperation with others, manipulated the market for certain securities and engaged in coercive conduct; and that they violated NASD's affirmative determination rule. Held, findings affirmed and sanctions of bar, expulsion, and fine upheld. Appearances For the Complainant Department of Enforcement: Robert L. Furst, Esq. and Jonathan I. Golomb, NASD Department of Enforcement. For the Respondents John Fiero and Fiero Brothers, Inc.: Martin H. Kaplan and Brian D. Graifman, Gusrae, Kaplan & Bruno; Martin P. Russo, MPR Law Practice, P.C.; Lewis D. Lowenfels, Tolins & Lowenfels. - 2 - Opinion John Fiero ("Fiero") and Fiero Brothers, Inc. ("Fiero Brothers" or "the Firm") (collectively, the "Fiero Respondents") appeal a December 6, 2000 decision of an NASD Hearing Panel. The Hearing Panel held that the Fiero Respondents, in cooperation with others and through the use of collusive trading activity, manipulated the market for certain securities, in violation of Section 10(b) of the Securities Exchange Act of 1934 ("Exchange Act"), Exchange Act Rule 10b-5, and Conduct Rules 2110 and 2120 and effected short sales of securities without making the affirmative determinations required by Conduct Rule 3370, in violation of Rules 2110 and 3370. In summary, the Hearing Panel found that the manipulation violation involved the Fiero Respondents' colluding with other short sellers to drive down the prices of several small-cap securities. -

Redacted Complaint

Case 4:20-cv-00311-SDJ Document 60 Filed 06/24/21 Page 1 of 76 PageID #: 1944 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF TEXAS SHERMAN DIVISION HOLLIS M. GREENLAW, TODD F. ETTER, CARA D. OBERT, BENJAMIN L. WISSINK, UMT HOLDINGS, L.P., UDF HOLDINGS, L.P., UNITED DEVELOPMENT FUNDING, L.P., UNITED DEVELOPMENT FUNDING III, L.P., UNITED DEVELOPMENT FUNDING IV, UNITED DEVELOPMENT FUNDING INCOME FUND V, UNITED MORTGAGE TRUST, and UNITED DEVELOPMENT FUNDING LAND OPPORTUNITY FUND, L.P., Plaintiffs, v. No. _____________________ DAVID KLIMEK, JAMES NICHOLAS BUNCH, JURY DEMANDED CHRISTINE L. EDSON, a/k/a Christy Edson, and DOES 1-10, Defendants. COMPLAINT AND JURY DEMAND Case 4:20-cv-00311-SDJ Document 60 Filed 06/24/21 Page 2 of 76 PageID #: 1945 TABLE OF CONTENTS SUMMARY ................................................................................................................................... 1 SUBJECT MATTER JURISDICTION ......................................................................................... 9 VENUE .......................................................................................................................................... 9 PLAINTIFFS .................................................................................................................................. 9 DEFENDANTS ............................................................................................................................ 13 RELEVANT PERSONS AND ENTITIES ................................................................................. -

02. February.Pmd

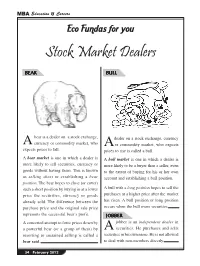

MBA Education & Careers Eco Fundas for you Stock Market Dealers BEAR BULL bear is a dealer on a stock exchange, dealer on a stock exchange, currency A currency or commodity market, who A or commodity market, who expects expects prices to fall. prices to rise is called a bull. A bear market is one in which a dealer is A bull market is one in which a dealer is more likely to sell securities, currency or more likely to be a buyer than a seller, even goods without having them. This is known to the extent of buying for his or her own as selling short or establishing a bear account and establishing a bull position. position. The bear hopes to close (or cover) such a short position by buying in at a lower A bull with a long position hopes to sell the price the securities, currency or goods purchases at a higher price after the market already sold. The difference between the has risen. A bull position or long position purchase price and the original sale price occurs when the bull owns securities. represents the successful bear’s profit. JOBBER A concerted attempt to force prices down by jobber is an independent dealer in a powerful bear (or a group of them) by A securities. He purchases and sells resorting to sustained selling is called a securities in his own name. He is not allowed bear raid. to deal with non-members directly. 34 February 2012 MBA Education & Careers ECO FUNDAS FOR YOU Stock Market Dealers CHICKEN PIG hickens are afraid to lose anything. -

Home Insurance Policy

Home Insurance Policy Comprehensive Plan Simple Documentation Home is where the heart is Home is where the heart is. There are no truer words than these. Our entire life revolves around our home. Besides being an investment of our life's savings, home is also the place of our dreams. Alive with countless warm memories. Samuel Johnson's words ring true here “To be happy at home is the ultimate result of all ambition”. However, specified natural calamities and man-made dangers can threaten the security of your home. Painful as it can be we need to secure it and provide for re-creating it, in case of damage due to unforseen circumstances. This is one of the reasons why you will appreciate Home Insurance Policy of ICICI Lombard. We endeavor to guarantee absolute peace of mind from all uncertainties in your day-to-day life with this unique policy. We are committed to being by your side in your time of need. What does the policy cover? The insurance for your home can be broadly divided into 2 parts : • Structure Cover - This is for the structure of your home. The compensation under this cover will be paid to repair damages to the structure caused by specified natural and man-made calamities • Contents Cover - This is for the possessions you have inside your home. If these are damaged or burgled, then the insurance covers the loss you incur for the same You can take either one of these covers individually or opt for both to make sure you are covered comprehensively. -

Summary of Investments by Type

COMMON INVESTMENT FUNDS Schedule of Investments September 30, 2017 SUMMARY OF INVESTMENTS BY TYPE Cost Market Value Fixed Income Investments $ $ Short-term investments 27,855,310 27,855,310 Bonds 173,219,241 174,637,768 Mortgage-backed securities 29,167,382 28,915,537 Emerging markets debt 9,619,817 11,462,971 Bank loans - high income fund 23,871,833 23,908,105 Total Fixed Income Investments 263,733,583 266,779,691 Equity-Type Investments Mutual funds Domestic 9,284,694 13,089,028 International 18,849,681 21,226,647 Common stocks Domestic 149,981,978 192,057,988 International 225,506,795 259,856,181 Total Equity-Type Investments 403,623,148 486,229,844 Alternative Investments Funds of hedge funds 38,264,990 46,646,700 Real estate trust fund 6,945,440 10,204,969 Total Alternatives Investments 45,210,430 56,851,669 TOTAL INVESTMENTS 712,567,160 809,861,204 Page 1 of 34 COMMON INVESTMENT FUNDS Schedule of Investments September 30, 2017 SUMMARY OF INVESTMENTS BY FUND Cost Market Value Fixed Income Fund $ $ Short-term investments 6,967,313 6,967,313 Bonds 140,024,544 141,525,710 Mortgage-backed securities 27,878,101 27,642,277 Emerging markets debt 9,619,817 11,462,971 Bank loans - high income fund 23,871,833 23,908,105 208,361,608 211,506,377 Domestic Core Equity Fund Short-term investments 4,856,385 4,856,385 Common stocks 131,222,585 167,989,561 Futures - 19,895 Private placement 4,150 4,150 136,083,120 172,869,991 Small Cap Equity Fund Short-term investments 2,123,629 2,123,629 Mutual funds 9,284,694 13,089,028 Common stocks 18,755,243