RESEARCH REPORT October 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Carlson Order Denying Motion for Subpoena

BEFORE THE NATIONAL ADJUDICATORY COUNCIL NASD ____________________________________ : In the Matter of : : Department of Enforcement, : DECISION : Complainant, : Complaint No. CAF980002 : vs. : : John Fiero : Dated: October 28, 2002 Jersey City, NJ : : : and : : : Pembroke Pines, FL : : and : : Fiero Brothers, Inc. : New York, NY, : : : Respondents : : ____________________________________: Firm and its president appeal findings that they, in cooperation with others, manipulated the market for certain securities and engaged in coercive conduct; and that they violated NASD's affirmative determination rule. Held, findings affirmed and sanctions of bar, expulsion, and fine upheld. Appearances For the Complainant Department of Enforcement: Robert L. Furst, Esq. and Jonathan I. Golomb, NASD Department of Enforcement. For the Respondents John Fiero and Fiero Brothers, Inc.: Martin H. Kaplan and Brian D. Graifman, Gusrae, Kaplan & Bruno; Martin P. Russo, MPR Law Practice, P.C.; Lewis D. Lowenfels, Tolins & Lowenfels. - 2 - Opinion John Fiero ("Fiero") and Fiero Brothers, Inc. ("Fiero Brothers" or "the Firm") (collectively, the "Fiero Respondents") appeal a December 6, 2000 decision of an NASD Hearing Panel. The Hearing Panel held that the Fiero Respondents, in cooperation with others and through the use of collusive trading activity, manipulated the market for certain securities, in violation of Section 10(b) of the Securities Exchange Act of 1934 ("Exchange Act"), Exchange Act Rule 10b-5, and Conduct Rules 2110 and 2120 and effected short sales of securities without making the affirmative determinations required by Conduct Rule 3370, in violation of Rules 2110 and 3370. In summary, the Hearing Panel found that the manipulation violation involved the Fiero Respondents' colluding with other short sellers to drive down the prices of several small-cap securities. -

02. February.Pmd

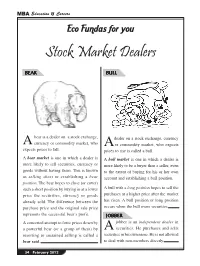

MBA Education & Careers Eco Fundas for you Stock Market Dealers BEAR BULL bear is a dealer on a stock exchange, dealer on a stock exchange, currency A currency or commodity market, who A or commodity market, who expects expects prices to fall. prices to rise is called a bull. A bear market is one in which a dealer is A bull market is one in which a dealer is more likely to sell securities, currency or more likely to be a buyer than a seller, even goods without having them. This is known to the extent of buying for his or her own as selling short or establishing a bear account and establishing a bull position. position. The bear hopes to close (or cover) such a short position by buying in at a lower A bull with a long position hopes to sell the price the securities, currency or goods purchases at a higher price after the market already sold. The difference between the has risen. A bull position or long position purchase price and the original sale price occurs when the bull owns securities. represents the successful bear’s profit. JOBBER A concerted attempt to force prices down by jobber is an independent dealer in a powerful bear (or a group of them) by A securities. He purchases and sells resorting to sustained selling is called a securities in his own name. He is not allowed bear raid. to deal with non-members directly. 34 February 2012 MBA Education & Careers ECO FUNDAS FOR YOU Stock Market Dealers CHICKEN PIG hickens are afraid to lose anything. -

The Direct Listing As a Competitor of the Traditional Ipo

The Direct Listing As a Competitor of the Traditional Ipo Research Paper – Law & Economics Course (IUS/05) Degree: Economics & Business, Dipartimento di Economia e Finanza Academic Year: 2019-2020 Name: Ludovico Morera Student Number: 216721 Supervisor: Prof. Pierluigi Matera The Direct Listing as a Competitor of the Traditional Ipo 2 Abstract In 2018, Spotify SA broke into the NYSE through an unusual direct listing, allowing it to become a publicly traded company without the high underwriting costs of a traditional Initial Public Offering that often deter companies from requesting to list. In order for such procedure to be possible, Spotify had to work closely with NYSE and SEC staff, which allowed for some amendments to their implementations of the Securities Act and the Securities Exchange Act. In this way, Spotify’s listing was done within the limits imposed by the U.S. market authorities. Several rumours concerning the direct listing arose, speculating that it may disrupt the American going public market and get past the standard firm-commitment underwriting procedures. This paper argues that these beliefs are largely wrong given the current regulatory limitations and tries to clarify for what firms direct listing is actually suitable. Furthermore, unlike the United Kingdom whose public exchanges have some experience, the NYSE faced such event for the first time; it follows that liability provisions under § 11 of the securities Act of 1933 may be attributed in different ways, especially due to the absence of an underwriter that may be held liable in case of material misstatements and omissions upon the registered documents. I find out that the direct listing can substitute the traditional IPO partially and only a restricted group of firms with some specific features could successfully do without an underwriter. -

Increased Stock Lending by Etfs and Its Effects on the Market

SSE Riga Student Research Papers 2018 : 4 (202) THE UNINTENDED CONSEQUENCES OF THE GROWTH IN ETFS: INCREASED STOCK LENDING BY ETFS AND ITS EFFECTS ON THE MARKET Authors: Grigoriţa Banaru Iryna Khomyak ISSN 1691-4643 ISBN 978-9984-822- November 2018 Riga The Unintended Consequences of the Growth in ETFs: Increased Stock Lending by ETFs and Its Effects on the Market Grigoriţa Banaru and Iryna Khomyak Supervisor: Tālis J. Putniņš November 2018 Riga Table of Contents Abstract ..................................................................................................................................... 5 1. Introduction .......................................................................................................................... 7 2. Literature Review and Hypotheses .................................................................................... 9 2.1. Short selling activity and its effects on the market efficiency ................................................ 9 2.1.1. Short interest and its positive impact on the market efficiency............................................ 9 2.1.2. Short selling and manipulation of prices ............................................................................ 11 2.2. ETFs and the equity market ................................................................................................... 12 2.2.1. The positive effects of ETFs on the market ....................................................................... 13 2.2.2. The dark side of ETFs ....................................................................................................... -

1 1 2 FINANCIAL CRISIS INQUIRY COMMISSION 3 4 Official Transcript

1 1 2 3 FINANCIAL CRISIS INQUIRY COMMISSION 4 5 Official Transcript 6 Hearing on "The Shadow Banking System" 7 Wednesday, May 5, 2010 8 Dirksen Senate Office Building, Room 538 9 Washington, D.C. 10 9:00 A.M. 11 12 COMMISSIONERS 13 PHIL ANGELIDES, Chairman 14 HON. BILL THOMAS, Vice Chairman 15 BROOKSLEY BORN, Commissioner 16 BYRON S. GEORGIOU, Commissioner 17 HON. BOB GRAHAM, Commissioner 18 KEITH HENNESSEY, Commissioner 19 DOUGLAS HOLTZ-EAKIN, Commissioner 20 HEATHER H. MURREN, Commissioner 21 JOHN W. THOMPSON, Commissioner 22 PETER J. WALLISON, Commissioner 23 24 Reported by: JANE W. BEACH 25 PAGES 1 - 369 2 1 Session 1: Investment Banks and the Shadow Banking System: 2 PAUL FRIEDMAN, Former Chief Operating Officer of 3 Fixed Income, Bear Stearns 4 SAMUEL MOLINARO, JR., Former Chief Financial 5 Officer and Chief Operating Officer, Bear Stearns 6 WARREN SPECTOR, former President and 7 Co-Chief Operating Officer, Bear Stearns 8 9 Session 2: Investment Banks and the Shadow Banking System: 10 JAMES E. CAYNE, Former Chairman and 11 Chief Executive Officer, Bear Stearns 12 ALAN D. SCHWARTZ, Former Chief Executive Officer, 13 Bear Stearns 14 15 16 17 18 19 20 21 22 23 24 3 1 Session 3: SEC Regulation of Investment Banks: 2 CHARLES CHRISTOPHER COX, Former Chairman 3 U.S. Securities and Exchange Commission 4 WILLIAM H. DONALDSON, Former Chairman, U.S. 5 Securities and Exchange Commission 6 H. DAVID KOTZ, Inspector General 7 U.S. Securities and Exchange Commission 8 ERIK R. SIRRI, Former Director, Division of 9 Trading & Markets, U.S. -

WALL STREET in the AMERICAN NOVEL Wayne W. Westbrook A

WALL STREET IN THE AMERICAN NOVEL Wayne W. Westbrook A Dissertation Submitted to the Graduate School of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY August 1972 p © 1972 WAYNE WILLIAM WESTBROOK ALL RIGHTS RESERVED IH ABSTRACT Wall Street is construed to represent the American financial center, La Salle Street in Chicago, State StreetiinbBoston and Third Street in Philadelphia as well as New York's lower Manhattan district. The novels and stories considered are those in which the financial center serves a primary function, either in influencing plot, character or in providing the background and atmosphere for the main action, Both archetypal and textual analysis are applied in seeing the recurrent motifs in the novel of high finance, patterns and themes which are fully articulated and developed in the late nineteenth-century version, yet which are not found to bear an influence on later financial fiction. The reason for this is that the American literary artist has had a prejudicial view of high finance and speculation which is rooted in his cultural heritage of the Puritan opposition to playing or gaming as a way to wealth and success. The writer's attitude, therefore, is largely con demnatory, regarding an individual's involvement with the financial marketplace as a form of personal corruption, profligacy and degen eracy. Further, the idea of the sin and evil of Wall Street has as its probable historical source the volatile course that American finance has traced since the post-Civil War industrial age, in the highly cyclical and repetitive pattern of boom and bust periods. -

Doing Battle with Short Sellers the Conflicted Role of Blockholders In

Author’s Accepted Manuscript Doing battle with short sellers: The conflicted role of blockholders in bear raids Naveen Khanna, Richmond D. Mathews www.elsevier.com/locate/jfec PII: S0304-405X(12)00132-8 DOI: http://dx.doi.org/10.1016/j.jfineco.2012.06.006 Reference: FINEC2184 To appear in: Journal of Financial Economics Received date: 12 July 2011 Revised date: 2 November 2011 Accepted date: 3 November 2011 Cite this article as: Naveen Khanna and Richmond D. Mathews, Doing battle with short sellers: The conflicted role of blockholders in bear raids, Journal of Financial Economics, http://dx.doi.org/10.1016/j.jfineco.2012.06.006 This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting galley proof before it is published in its final citable form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain. Doing battle with short sellers: the conflicted role of blockholders in bear raids ? Naveen Khannaa, Richmond D. Mathewsb; ∗ aEli Broad College of Business, Michigan State University, East Lansing, MI, 48824, USA bRobert H. Smith School of Business, University of Maryland, College Park, MD, 20742, USA Abstract If short sellers can destroy firm value by manipulating prices down, an informed blockholder has a powerful natural incentive to protect the value of his stake by trading against them. -

Great Deformation: the Corruption of Capitalism in America

4/C PROCESS + PANTONE 8402 GRITTY MATTE UV 100#PAPER. ECONOMICS / BUSINESS $35.00 / $38.00 can IN THE WORDS OF DAVID STOCKMAN THE GREAT DEFORMATION is a searing look at Washington’s craven response to the recent myriad of financial crises and fiscal cliffs. It counters conven- ER D “ At the heart of the Great Deformation is a rogue central bank tional wisdom with an eighty-year revisionist history of how LAN G N E that has abandoned every vestige of sound money.” the American state—especially the Federal Reserve—has fallen ARYL ARYL C prey to the politics of crony capitalism and the ideologies of fiscal stimulus, monetary central planning, and financial bail- DAVID A. STOCKMAN was elected as a “ In the years after 1980, America had undergone the equivalent of outs. These forces have left the public sector teetering on the Michigan congressman in 1976 and joined the Reagan White a national leveraged buyout...[and was] now saddled with edge of political dysfunction and fiscal collapse and have caused House in 1981. Serving as budget director, he was one of the America’s private enterprise foundation to morph into a spec- more in combined public and private debt.” key architects of the Reagan Revolution plan to reduce taxes, $30 trillion ulative casino that swindles the masses and enriches the few. cut spending, and shrink the role of government. He joined Defying right- and left-wing boxes, David Stockman Salomon Brothers in 1985 and later became one of the early The Corruption of Capitalism provides a catalogue of corrupters and defenders of sound partners of the Blackstone Group. -

The Alternative Uptick Rule

Seton Hall University eRepository @ Seton Hall Law School Student Scholarship Seton Hall Law 2013 The Alternative Uptick Rule - Restoring Short Selling as an Asset to the Market and Striking a Regulatory Balance Between Those That Favor or Oppose Regulation David Max Fleischer Follow this and additional works at: https://scholarship.shu.edu/student_scholarship Recommended Citation Fleischer, David Max, "The Alternative Uptick Rule - Restoring Short Selling as an Asset to the Market and Striking a Regulatory Balance Between Those That Favor or Oppose Regulation" (2013). Law School Student Scholarship. 386. https://scholarship.shu.edu/student_scholarship/386 The Alternative Uptick Rule-Restoring Short Selling as an Asset to the Market and Striking a Regulatory Balance between Those That Favor or Oppose Regulation By David Max.Fleischer.;"'f I. Introduction The majority of stock holders 1 purchase and hold stocks with an expectation that the stock will gain value over time.2 Imagine that you purchased shares of stock in the company Bear Stearns in the year 2008, or perhaps had held these shares for years. During the week of March 11, 2008 to March 17, 2008 the value of Bear Stearns stock dropped from $62.97 to $2.00 per share.3 You would expect that everyone who held this stock suffered some level ofloss financially. The expectation is that all the holders of the security lost between $.01 per share up to $60.97 per share. Imagine hearing that not of all the holders of Bear Stearns lost money, some holders of Bear Steams stock actually made a huge profit on this decline ofvalue! Some investors may have made a mirrored dollar of profit for each dollar that declined. -

Pricing and Performance of Initial Public Offerings in the United States 1St Edition Pdf, Epub, Ebook

PRICING AND PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN THE UNITED STATES 1ST EDITION PDF, EPUB, EBOOK Arvin Ghosh | 9781351496759 | | | | | Pricing and Performance of Initial Public Offerings in the United States 1st edition PDF Book Financial Times. Your Money. Your review was sent successfully and is now waiting for our team to publish it. Industrial and Commercial Bank of China. In particular, merchants and bankers developed what we would today call securitization. The Internet Bubble. However, due to transit disruptions in some geographies, deliveries may be delayed. Gregoriou, Greg Private shareholders may hold onto their shares in the public market or sell a portion or all of them for gains. In the US, clients are given a preliminary prospectus, known as a red herring prospectus , during the initial quiet period. In this timely volume on newly emerging financial mar- kets and investment strategies, Arvin Ghosh explores the intriguing topic of initial public offerings IPOs of securities, among the most significant phenomena in the United States stock markets in recent years. Although IPO offers many benefits, there are also significant costs involved, chiefly those associated with the process such as banking and legal fees, and the ongoing requirement to disclose important and sometimes sensitive information. Role of the Underwriters. In some situations, when the IPO is not a "hot" issue undersubscribed , and where the salesperson is the client's advisor, it is possible that the financial incentives of the advisor and client may not be aligned. View all volumes in this series: Quantitative Finance. Retrieved 4 March Literature Review and Data Source. -

Hedge Funds and Systemic Risk

CHILDREN AND FAMILIES The RAND Corporation is a nonprofit institution that EDUCATION AND THE ARTS helps improve policy and decisionmaking through ENERGY AND ENVIRONMENT research and analysis. HEALTH AND HEALTH CARE This electronic document was made available from INFRASTRUCTURE AND www.rand.org as a public service of the RAND TRANSPORTATION Corporation. INTERNATIONAL AFFAIRS LAW AND BUSINESS NATIONAL SECURITY Skip all front matter: Jump to Page 16 POPULATION AND AGING PUBLIC SAFETY SCIENCE AND TECHNOLOGY Support RAND Purchase this document TERRORISM AND HOMELAND SECURITY Browse Reports & Bookstore Make a charitable contribution For More Information Visit RAND at www.rand.org Explore the RAND Corporation View document details Limited Electronic Distribution Rights This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non-commercial use only. Unauthorized posting of RAND electronic documents to a non-RAND website is prohibited. RAND electronic documents are protected under copyright law. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents for commercial use. For information on reprint and linking permissions, please see RAND Permissions. This product is part of the RAND Corporation monograph series. RAND monographs present major research findings that address the challenges facing the public and private sectors. All RAND mono- graphs undergo rigorous peer review to ensure high standards for research quality and objectivity. Hedge Funds and Systemic Risk Lloyd Dixon, Noreen Clancy, Krishna B. Kumar C O R P O R A T I O N The research described in this report was supported by a contribution by Christopher D. -

Copyrighted Material

Index Access, 87 Bank accounts, 75 Accounting fi rms, 69 Bankruptcy, 27–28, 53 Active trader, 7 Bank trust departments, 20 Aduddell Industries, Inc. Baruch College, 103 (ADDL), 127–129, Bear raid, 13 132–133 Bidding up shares, 104 Advice, getting and giving, 3–6, BigCharts.com, 37 36, 70–71, 166 Biotech companies, 152, 153 Airline stocks, 157–159 Biotech stocks, 19 Alcatel, 23 Bluefi re Associates, 106 Amazon, 104 Boiler rooms, 165 American Airlines Corp. (AMR), Boredom, 81 157–158 Breaking the back of a American Express, 164 stock, 16 American Stock Exchange Brokerage fi rms, 19, 20, (AMEX), 7, 141, 142, 154 76–78, 130 Amgen, 153 Broker-dealer, 3, 12 Amsterdam Stock Exchange Bucket shops, 165 (Beurs), 86 Budweiser, 164 Analyst, 5, 7,COPYRIGHTED 15, 25, 71, 91 Buffett, MATERIAL Warren, 164 Aptimus, Inc. (APTM), Bulletin board, 34, 144 109–121 Business condition, 13 initial public offering, 114 Business media, 90–91, 140 tender offer, 114–115, Business news, 113 117–119 Buy-and-hold strategy, 4, 75 Assets, 53, 54, 151 Buybacks, 13, 112–119 169 JJWBK198_Index[169-174].inddWBK198_Index[169-174].indd 169169 66/5/08/5/08 33:45:58:45:58 PPMM 170 Index Buying, 85, 137 Day-trading, 5 Buying power, reserving, 81 Dealers, 129, 130 Debt, 13, 53 Call options, 60, 61 Decimal pricing, vii Canada, 86 Delta Air Lines, 159 Capitalization, 13, 57, 101, Desirability of company, 111 111, 152 Diversifi ed portfolio, 18, 155 Carbontronics, 144 Downside exposure, 117 Cash holdings, 13, 151–153 Downside trading, 7 Certifi cates of deposit (CDs), 8, 75, 88 Electronic access, 4, 36, 137 Chapter 11 bankruptcy, 143 Electronic communications China, 33, 86 network (ECN), 77, 78, 105, Clean shell, 54, 55, 125 116, 128 Clinton Administration, 143 Electronic sorting and scanning CNBC, vii, 89 systems, 37 CNN, 91 Electronic trading, 3, 5 Coca-Cola, 7, 164 Employee stock ownership Cohen, Steven A., 93 plans, 152 Commodity exchange, vii England, 86 Common stock, 113 Equities markets, 4 Compensation, 113 Exchanges, vii, 7 Computerization, 167 eXegenics, Inc.