Herbalife: Why I Made It a 35% Position After the Bill Ackman Bear Raid

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Carlson Order Denying Motion for Subpoena

BEFORE THE NATIONAL ADJUDICATORY COUNCIL NASD ____________________________________ : In the Matter of : : Department of Enforcement, : DECISION : Complainant, : Complaint No. CAF980002 : vs. : : John Fiero : Dated: October 28, 2002 Jersey City, NJ : : : and : : : Pembroke Pines, FL : : and : : Fiero Brothers, Inc. : New York, NY, : : : Respondents : : ____________________________________: Firm and its president appeal findings that they, in cooperation with others, manipulated the market for certain securities and engaged in coercive conduct; and that they violated NASD's affirmative determination rule. Held, findings affirmed and sanctions of bar, expulsion, and fine upheld. Appearances For the Complainant Department of Enforcement: Robert L. Furst, Esq. and Jonathan I. Golomb, NASD Department of Enforcement. For the Respondents John Fiero and Fiero Brothers, Inc.: Martin H. Kaplan and Brian D. Graifman, Gusrae, Kaplan & Bruno; Martin P. Russo, MPR Law Practice, P.C.; Lewis D. Lowenfels, Tolins & Lowenfels. - 2 - Opinion John Fiero ("Fiero") and Fiero Brothers, Inc. ("Fiero Brothers" or "the Firm") (collectively, the "Fiero Respondents") appeal a December 6, 2000 decision of an NASD Hearing Panel. The Hearing Panel held that the Fiero Respondents, in cooperation with others and through the use of collusive trading activity, manipulated the market for certain securities, in violation of Section 10(b) of the Securities Exchange Act of 1934 ("Exchange Act"), Exchange Act Rule 10b-5, and Conduct Rules 2110 and 2120 and effected short sales of securities without making the affirmative determinations required by Conduct Rule 3370, in violation of Rules 2110 and 3370. In summary, the Hearing Panel found that the manipulation violation involved the Fiero Respondents' colluding with other short sellers to drive down the prices of several small-cap securities. -

02. February.Pmd

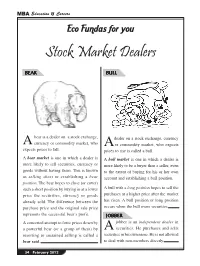

MBA Education & Careers Eco Fundas for you Stock Market Dealers BEAR BULL bear is a dealer on a stock exchange, dealer on a stock exchange, currency A currency or commodity market, who A or commodity market, who expects expects prices to fall. prices to rise is called a bull. A bear market is one in which a dealer is A bull market is one in which a dealer is more likely to sell securities, currency or more likely to be a buyer than a seller, even goods without having them. This is known to the extent of buying for his or her own as selling short or establishing a bear account and establishing a bull position. position. The bear hopes to close (or cover) such a short position by buying in at a lower A bull with a long position hopes to sell the price the securities, currency or goods purchases at a higher price after the market already sold. The difference between the has risen. A bull position or long position purchase price and the original sale price occurs when the bull owns securities. represents the successful bear’s profit. JOBBER A concerted attempt to force prices down by jobber is an independent dealer in a powerful bear (or a group of them) by A securities. He purchases and sells resorting to sustained selling is called a securities in his own name. He is not allowed bear raid. to deal with non-members directly. 34 February 2012 MBA Education & Careers ECO FUNDAS FOR YOU Stock Market Dealers CHICKEN PIG hickens are afraid to lose anything. -

The Direct Listing As a Competitor of the Traditional Ipo

The Direct Listing As a Competitor of the Traditional Ipo Research Paper – Law & Economics Course (IUS/05) Degree: Economics & Business, Dipartimento di Economia e Finanza Academic Year: 2019-2020 Name: Ludovico Morera Student Number: 216721 Supervisor: Prof. Pierluigi Matera The Direct Listing as a Competitor of the Traditional Ipo 2 Abstract In 2018, Spotify SA broke into the NYSE through an unusual direct listing, allowing it to become a publicly traded company without the high underwriting costs of a traditional Initial Public Offering that often deter companies from requesting to list. In order for such procedure to be possible, Spotify had to work closely with NYSE and SEC staff, which allowed for some amendments to their implementations of the Securities Act and the Securities Exchange Act. In this way, Spotify’s listing was done within the limits imposed by the U.S. market authorities. Several rumours concerning the direct listing arose, speculating that it may disrupt the American going public market and get past the standard firm-commitment underwriting procedures. This paper argues that these beliefs are largely wrong given the current regulatory limitations and tries to clarify for what firms direct listing is actually suitable. Furthermore, unlike the United Kingdom whose public exchanges have some experience, the NYSE faced such event for the first time; it follows that liability provisions under § 11 of the securities Act of 1933 may be attributed in different ways, especially due to the absence of an underwriter that may be held liable in case of material misstatements and omissions upon the registered documents. I find out that the direct listing can substitute the traditional IPO partially and only a restricted group of firms with some specific features could successfully do without an underwriter. -

Increased Stock Lending by Etfs and Its Effects on the Market

SSE Riga Student Research Papers 2018 : 4 (202) THE UNINTENDED CONSEQUENCES OF THE GROWTH IN ETFS: INCREASED STOCK LENDING BY ETFS AND ITS EFFECTS ON THE MARKET Authors: Grigoriţa Banaru Iryna Khomyak ISSN 1691-4643 ISBN 978-9984-822- November 2018 Riga The Unintended Consequences of the Growth in ETFs: Increased Stock Lending by ETFs and Its Effects on the Market Grigoriţa Banaru and Iryna Khomyak Supervisor: Tālis J. Putniņš November 2018 Riga Table of Contents Abstract ..................................................................................................................................... 5 1. Introduction .......................................................................................................................... 7 2. Literature Review and Hypotheses .................................................................................... 9 2.1. Short selling activity and its effects on the market efficiency ................................................ 9 2.1.1. Short interest and its positive impact on the market efficiency............................................ 9 2.1.2. Short selling and manipulation of prices ............................................................................ 11 2.2. ETFs and the equity market ................................................................................................... 12 2.2.1. The positive effects of ETFs on the market ....................................................................... 13 2.2.2. The dark side of ETFs ....................................................................................................... -

Carl Icahn Defends Ackman, Slams Lipton CNBC by Lawrence Delevingne April 23, 2014

Carl Icahn defends Ackman, slams Lipton CNBC By Lawrence Delevingne April 23, 2014 Maybe it was the martini that helped Carl Icahn publicly support longtime nemesis Bill Ackman. "I never thought I'd be defending him, but I don't think there's anything wrong with that," Icahn said of the Pershing Square Capital Management founder's bid for Allergan with Valeant during a CNBC interview Tuesday night at the IMN Active-Passive Investor Summit in New York. "We have our differences, but I never said he's not a smart guy. I think the concept of this is good. I hope it works out better for him than Herbalife did, and I think it will," Icahn added shortly after taking sips from a martini passed to him while on camera. "There's nothing wrong with making a bid for a company and using someone else's funds." Icahn added he would consider teaming up with a company to make a hostile bid for another, like Ackman. "Any activism is good as long as it's legal," the billionaire chairman of Icahn Enterprises said. Icahn also weighed in on another longtime adversary, Wachtell, Lipton, Rosen & Katz founding partner Marty Lipton. "Marty Lipton I think is just dead wrong," Icahn said of the corporate lawyer's negative views on activist investors. "Lipton continues to say 'they're short termist, they're no good.' It's like a witch doctor almost," Icahn said. "Well why? What are your facts? 'Anecdotal.' Who's giving him the anecdote? What's his evidence? You know who? Some of his clients that are paying him millions and millions of dollars. -

JC Penny's Turnaround

JC Penny’s Turnaround Case Study: Market perception and price action extremely negative. Balance sheet OK. Is there a disconnect between how a business should be run (for the long term) and “Analysts” focusing on the short term? Perception Friday 8:11 AM Ron Johnson is on the mike at the J.C. Penney (JCP) earnings CC (webcast). The embattled exec starts with a quick admission of past mistakes and an unfortunate alienation of core customers before hitting his "transformational" stride. Despite the direction the RJ rhetoric goes, the company pulling away its guidance is going to be the headline that resonates. JCP - 8.7%. 4 Comments I'm not sure what type of fairy dust RJ is sprinkling during the CC to take the stock spike back up during its premarket low but JCP is clearly in some serious trouble. No guidance?? A company going through a "transformational" change with no guidance is one that seems to be changing things and hoping for the best. The direction of the business plan continues to be murky and the failings of their marketing campaign are killing what customers they have left and turning them elsewhere. Ackman's investors may be taking it on the chin with this one. Yeah, like they did on Borders. Count me as one of the core customers that Johnson has alienated. Have cancelled my credit www.csinvesting.wordpress.com studying/teaching/investing Page 1 JC Penny’s Turnaround Can not imagine Ackman ever thought he was going to be in this for the long haul. He like many of us bought in to RJ's plan only to find out later it is flawed and will cost BILLIONS [Consumer, On the Move Editor of CSInvesting (www.csinvesting.wordpress.com): Readers should go to the blog and type in: The Sleuth Investor to read the book and view the video on how to do due diligence or scuttlebutt. -

1 1 2 FINANCIAL CRISIS INQUIRY COMMISSION 3 4 Official Transcript

1 1 2 3 FINANCIAL CRISIS INQUIRY COMMISSION 4 5 Official Transcript 6 Hearing on "The Shadow Banking System" 7 Wednesday, May 5, 2010 8 Dirksen Senate Office Building, Room 538 9 Washington, D.C. 10 9:00 A.M. 11 12 COMMISSIONERS 13 PHIL ANGELIDES, Chairman 14 HON. BILL THOMAS, Vice Chairman 15 BROOKSLEY BORN, Commissioner 16 BYRON S. GEORGIOU, Commissioner 17 HON. BOB GRAHAM, Commissioner 18 KEITH HENNESSEY, Commissioner 19 DOUGLAS HOLTZ-EAKIN, Commissioner 20 HEATHER H. MURREN, Commissioner 21 JOHN W. THOMPSON, Commissioner 22 PETER J. WALLISON, Commissioner 23 24 Reported by: JANE W. BEACH 25 PAGES 1 - 369 2 1 Session 1: Investment Banks and the Shadow Banking System: 2 PAUL FRIEDMAN, Former Chief Operating Officer of 3 Fixed Income, Bear Stearns 4 SAMUEL MOLINARO, JR., Former Chief Financial 5 Officer and Chief Operating Officer, Bear Stearns 6 WARREN SPECTOR, former President and 7 Co-Chief Operating Officer, Bear Stearns 8 9 Session 2: Investment Banks and the Shadow Banking System: 10 JAMES E. CAYNE, Former Chairman and 11 Chief Executive Officer, Bear Stearns 12 ALAN D. SCHWARTZ, Former Chief Executive Officer, 13 Bear Stearns 14 15 16 17 18 19 20 21 22 23 24 3 1 Session 3: SEC Regulation of Investment Banks: 2 CHARLES CHRISTOPHER COX, Former Chairman 3 U.S. Securities and Exchange Commission 4 WILLIAM H. DONALDSON, Former Chairman, U.S. 5 Securities and Exchange Commission 6 H. DAVID KOTZ, Inspector General 7 U.S. Securities and Exchange Commission 8 ERIK R. SIRRI, Former Director, Division of 9 Trading & Markets, U.S. -

A Record-Breaking Year for Justice

2018 Annual Report A Record-Breaking Year for Justice Affiliated with Benjamin N. Cardozo School of Law, Yeshiva University The Innocence Project was founded in 1992 by Barry C. Scheck and Peter J. Neufeld at the Benjamin N. Cardozo School of Law at Yeshiva University to assist incarcerated people who could be proven innocent through DNA testing. To date, more than 360 people in the United States have been exonerated by DNA testing, including 21 who spent time on death row. These people spent an average of 14 years in prison before exoneration and release. The Innocence Project’s staff attorneys and Cardozo clinic students provided direct representation or critical assistance in most of these cases. The Innocence Project’s groundbreaking use of DNA technology to free innocent people has provided irrefutable proof that wrongful convictions are not isolated or rare events, but instead arise from systemic defects. Now an independent nonprofit organization closely affiliated with Cardozo School of Law at Yeshiva University, the Innocence Project’s mission is to free the staggering number of innocent people who remain incarcerated and to bring substantive reform to the system responsible for their unjust imprisonment. Letter from the Co-Founders, Board Chair and Executive Director ........................................... 3 FY18 Victories ................................................................................................................................................ 4 John Nolley .................................................................................................................................................... -

WALL STREET in the AMERICAN NOVEL Wayne W. Westbrook A

WALL STREET IN THE AMERICAN NOVEL Wayne W. Westbrook A Dissertation Submitted to the Graduate School of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY August 1972 p © 1972 WAYNE WILLIAM WESTBROOK ALL RIGHTS RESERVED IH ABSTRACT Wall Street is construed to represent the American financial center, La Salle Street in Chicago, State StreetiinbBoston and Third Street in Philadelphia as well as New York's lower Manhattan district. The novels and stories considered are those in which the financial center serves a primary function, either in influencing plot, character or in providing the background and atmosphere for the main action, Both archetypal and textual analysis are applied in seeing the recurrent motifs in the novel of high finance, patterns and themes which are fully articulated and developed in the late nineteenth-century version, yet which are not found to bear an influence on later financial fiction. The reason for this is that the American literary artist has had a prejudicial view of high finance and speculation which is rooted in his cultural heritage of the Puritan opposition to playing or gaming as a way to wealth and success. The writer's attitude, therefore, is largely con demnatory, regarding an individual's involvement with the financial marketplace as a form of personal corruption, profligacy and degen eracy. Further, the idea of the sin and evil of Wall Street has as its probable historical source the volatile course that American finance has traced since the post-Civil War industrial age, in the highly cyclical and repetitive pattern of boom and bust periods. -

ADP: Driving Superior Results Through Market Leadership And

R = 249 G = 161 B = 26 R = 203 G = 67 B = 153 R = 100 G = 190 B = 235 R = 196 G = 218 ADP: Driving Superior Results Through B = 90 Market Leadership and Continuous R = 170 Innovation G = 169 B = 170 R = 189 G = 187 September 2017 B = 187 Copyright © 2017 ADP, LLC. R = 249 G = 161 Safe Harbor Statement Forward-Looking Statements B = 26 This presentation and other written or oral statements made from time to time by ADP may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements that are not historical in nature and which may be identified by the use of words like “expects,” “assumes,” “projects,” “anticipates,” “estimates,” “we believe,” “could,” “is designed to” and other words of similar meaning, are forward-looking statements. These statements are based on management’s expectations and assumptions and depend upon or refer to future events or conditions and are subject to risks and uncertainties that may cause actual results to differ materially from those expressed. Factors that R = 203 could cause actual results to differ materially from those contemplated by the forward-looking statements or that could contribute to such difference G = 67 include: ADP's success in obtaining and retaining clients, and selling additional services to clients; the pricing of products and services; compliance with existing or new legislation or regulations; changes in, or interpretations of, existing legislation or regulations; overall market, political and B = 153 economic conditions, including interest rate and foreign currency trends; competitive conditions; our ability to maintain our current credit ratings and the impact on our funding costs and profitability; security or privacy breaches, fraudulent acts, and system interruptions and failures; employment and wage levels; changes in technology; availability of skilled technical associates; and the impact of new acquisitions and divestitures. -

Pershing Square Holdings, Ltd. Intention to Float on Euronext Amsterdam

NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN OR INTO THE UNITED STATES, AUSTRALIA, CANADA, JAPAN, NEW ZEALAND OR THE REPUBLIC OF SOUTH AFRICA OR ANY OTHER JURISDICTION WHERE TO DO SO MIGHT CONSTITUTE A VIOLATION OR BREACH OF ANY APPLICABLE LAW OR REGULATION OR TO ANY NATIONAL, RESIDENT OR CITIZEN THEREOF. PLEASE SEE THE IMPORTANT NOTICE AT THE END OF THIS ANNOUNCEMENT. This announcement is an advertisement and does not constitute a prospectus for the purposes of the Prospectus Directive (as defined below) and, as such, does not constitute an offer to sell or the solicitation of an offer to purchase securities. Investors should not purchase or subscribe for any transferable securities referred to in this announcement except on the basis of information contained in the prospectus (the “Prospectus”) expected to be published by Pershing Square Holdings, Ltd. (“PSH” or the “Company”) and approved by the Netherlands Authority for the Financial Markets (Stichting Autoriteit Financële Markten) (“AFM”) in due course in connection with the admission to trading (“Admission”) of newly issued non‐ redeemable ordinary shares in the Company (the “Public Shares”) on Euronext in Amsterdam, the regulated market operated by Euronext Amsterdam N.V. (“Euronext Amsterdam”). This announcement is not an offer to sell, or a solicitation of an offer to purchase or subscribe for, any Public Shares. Public Shares may not be offered or sold in the United States absent registration or an exemption from registration. The securities described herein will be issued and sold only in accordance with all applicable laws and regulations. -

Doing Battle with Short Sellers the Conflicted Role of Blockholders In

Author’s Accepted Manuscript Doing battle with short sellers: The conflicted role of blockholders in bear raids Naveen Khanna, Richmond D. Mathews www.elsevier.com/locate/jfec PII: S0304-405X(12)00132-8 DOI: http://dx.doi.org/10.1016/j.jfineco.2012.06.006 Reference: FINEC2184 To appear in: Journal of Financial Economics Received date: 12 July 2011 Revised date: 2 November 2011 Accepted date: 3 November 2011 Cite this article as: Naveen Khanna and Richmond D. Mathews, Doing battle with short sellers: The conflicted role of blockholders in bear raids, Journal of Financial Economics, http://dx.doi.org/10.1016/j.jfineco.2012.06.006 This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and review of the resulting galley proof before it is published in its final citable form. Please note that during the production process errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain. Doing battle with short sellers: the conflicted role of blockholders in bear raids ? Naveen Khannaa, Richmond D. Mathewsb; ∗ aEli Broad College of Business, Michigan State University, East Lansing, MI, 48824, USA bRobert H. Smith School of Business, University of Maryland, College Park, MD, 20742, USA Abstract If short sellers can destroy firm value by manipulating prices down, an informed blockholder has a powerful natural incentive to protect the value of his stake by trading against them.