0518 Plant-Based Feature

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

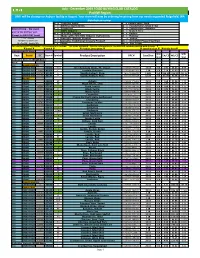

December 2019 FOOD BUYING CLUB CATALOG Pacnw Region UNFI Will Be Closing Our Auburn Facility in August

July - December 2019 FOOD BUYING CLUB CATALOG PacNW Region UNFI will be closing our Auburn facility in August. Your store will now be ordering/receiving from our newly expanded Ridgefield, WA distribution center. n = Contains Sugar F = Foodservice, Bulk s = Artificial Ingredients G = Foodservice, Grab n' Go BASICS Pricing = the lowest 4 = Sulphured D = Foodservice, Supplies _ = 100% Organic K = Gluten Free price at the shelf per unit. H = 95%-99% Organic b = Kosher (Except for FIELD DAY items) : = Made with 70%-94% Organic Ingredients d = Holiday * "DC" Column T = Specialty, Natural Product , = Vegan NO CODE= All Warehouses U = Specialty, Traditional Grocery Product m = NonGMO Project Verified W = PacNW - Seattle, WA C = Ethnic w = Fair Trade For placing a SPECIAL ORDER - It is necessary to include: *THE PAGE NUMBER, Plus the information in the BOLDED columns marked with Arrows "▼" * ▼Brand ▼ ▼Item # ▼ ▼ Product Description ▼ ▼ Case/Unit Size ▼ ▼Whlsle Price▼ Indicates BASICS Items WS/ SRP/ Dept Brand DC Item # Symbols Product Description UPC # Case/Size EA/CS WS/CS Brand Unit Unit Indicates Generic BULK Items BULK BULK BAKINGBAKING GOODSGOODS BULK BAKING GOODS 05451 HKnw Dk Chocolate Chips, FT, Vegan 026938-073442 10 LB EA 6.91 69.06 8.99 BULK BAKING GOODSUTWR 40208 F Lecithin Granules 026938-402082 5 LB EA 7.18 35.90 9.35 BULK BAKING GOODSGXUTWR 33140 F Vanilla Extract, Pure 767572-831288 1 GAL EA 336.90 336.90 439.45 BULK BAKING GOODSGUTWR 33141 F Vanilla Extract, Pure 767572-830328 32 OZ EA 95.08 95.08 123.99 BULK BEANSBEANS BULK -

NON-DAIRY MILKS 2018 - TREND INSIGHT REPORT It’S on the Way to Becoming a $3.3 Billion Market, and Has Seen 61% Growth in Just a Few Years

NON-DAIRY MILKS 2018 - TREND INSIGHT REPORT It’s on the way to becoming a $3.3 billion market, and has seen 61% growth in just a few years. Non-dairy milks are the clear successor to cow (dairy) milk. Consumers often perceive these products as an answer to their health and wellness goals. But the space isn’t without challenges or considerations. In part one of this two- part series, let’s take a look at the market, from new product introductions to regulatory controversy. COW MILK ON THE DECLINE Cow milk (also called dairy milk) has been on the decline since 2012. Non-dairy milks, however, grew 61% in the same period. Consumers are seeking these plant-based alternatives that they believe help them feel and look better to fulfill health and wellness goals. Perception of the products’ health benefits is growing, as consumers seek relief from intolerance, digestive issues and added sugars. And the market reflects it. Non-dairy milks climbed 10% per year since 2012, a trend that’s expected to continue through 2022 to become a $3.3 billion-dollar market.2 SOY WHAT? MEET THE NON-DAIRY MILKS CONSUMERS CRAVE THREE TREES UNSWEETENED VANILLA ORGANIC ALMONDMILK Made with real Madagascar vanilla ALMOND MILK LEADS THE NON-DAIRY MILK bean, the manufacturer states that the CATEGORY WITH 63.9% MARKET SHARE drink contains more almonds, claims to have healthy fats and is naturally rich and nourishing with kitchen-friendly ingredients. As the dairy milk industry has leveled out, the non-dairy milk market is growing thanks to the consumer who’s gobbling up alternatives like almond milk faster than you can say mooove. -

"Research for Rural Development 2020"

ONLINE ISSN 2255-923X Research for Rural Development 2018 ISSN 1691-4031 35 Latvia University of Life Sciences and Technologies Volume Annual 26th International Scientific Conference Research for Rural Development 2020 Volume 2 Latvia University of Life Sciences and Technologies RESEARCH FOR RURAL DEVELOPMENT 2020 Annual 26th International Scientific Conference Proceedings Volume 35 Jelgava 2020 LATVIA UNIVERSITY OF LIFE SCIENCES AND TECHNOLOGIES ONLINE ISSN 2255-923X RESEARCH FOR RURAL DEVELOPMENT 2020 May, 2020 ISSN 1691-4031 http://www2.llu.lv/research_conf/proceedings.htm ORGANISING TEAM Ausma Markevica, Mg.sc.paed., Mg.sc.soc., Mg.sc.ing., Research coordinator, Research and Project Development Center, Latvia University of Life Sciences and Technologies Zita Kriaučiūniene, Dr.biomed., associate professor, Vytautas Magnus University, Agriculture Academy, Lithuania Nadežda Karpova-Sadigova, Mg.sc.soc., Head of Document Management Department, Latvia University of Life Sciences and Technologies SCIENTIFIC COMMITTEE Chairperson Zinta Gaile, professor, Dr.agr., Latvia University of Life Sciences and Technologies Members Irina Arhipova, vice-rector for science, professor Dr.sc.ing., Latvia University of Life Sciences and Technologies Andra Zvirbule, Dr.oec., professor, Latvia University of Life Sciences and Technologies Gerald Assouline, associate professor, Dr.sc. soc., Director of QAP Decision, Grenoble, France Inga Ciproviča, professor, Dr.sc.ing., Latvia University of Life Sciences and Technologies Signe Bāliņa, professor, Dr.oec., University -

Terminology Tempest in the Dairy Case David Sprinkle Research Director, Packaged Facts

PACKAGED FACTS ON OPPORTUNITIES IN FOOD INDUSTRY DISRUPTION Terminology Tempest in the Dairy Case David Sprinkle Research Director, Packaged Facts The recent European Union Court of Justice ruling against marketing of non-dairy soy/ soya products in dairy terms (such as soy “milk” or tofu “butter”) was the right call, narrowly speaking. From the consumer protection viewpoint, however, it’s not clear that much justice was served. Nor is the European dairy industry likely to benefit significantly, as is the case with parallel initiatives taking place in the U.S. EU Ruling Against Soyfoods Marketed in Dairy Terms Since 2013, European Union law has specified that dairy terms such as milk, cheese, yogurt, and butter are restricted to animal products. With logic that fails to leap out, at least on this side of the Atlantic, EU regulators baked in exceptions for dairy analog products including almond milk and coconut milk, which are relatively new as packaged dairy alternative beverages. Ice “cream,” similarly, was allowed for non-dairy alternatives. The EU regulators left soy “milk” out in the cold, even though soy milk has been marketed in Europe as well as the U.S. for a century. While marketers of soy-based dairy analogs were officially barred from using dairy terminology for their products, enforcement of this restriction has been lax, as in the parallel case in the U.S. This led the main consumer protection organizational alliance in Germany (funded by the Federal Ministry With logic that fails to of Consumer Affairs, Nutrition, and Agriculture) to leap out, EU regulators file a case in German courts against Tofu Town—a baked in exceptions for German food manufacturer that (as the company name almond and coconut proactively gives away) markets soy-based foods. -

Don't Cry Over Plant-Based Milk: Why the Use of the Term “Milk” on Non-Dairy Beverages Does Not Constitute “Misbranded” Under the Federal Food, Drug, and Cosmetic Act

Mancinelli, Michael 5/10/2020 For Educational Use Only DON'T CRY OVER PLANT-BASED MILK: WHY THE USE..., 14 J. Health &... 14 J. Health & Biomedical L. 481 Journal of Health & Biomedical Law 2018 Note Giuliana D'Esopo 1 Copyright © 2018 by Journal of Health & Biomedical Law; Giuliana D'Esopo DON'T CRY OVER PLANT-BASED MILK: WHY THE USE OF THE TERM “MILK” ON NON-DAIRY BEVERAGES DOES NOT CONSTITUTE “MISBRANDED” UNDER THE FEDERAL FOOD, DRUG, AND COSMETIC ACT Of course, the global economy couldn't very well function without this wall of ignorance and the indifference it breeds. This is why the American food industry and its international counterparts fight to keep their products from telling even the simplest stories ... about how they were produced. The more knowledge people have about the way their food is produced, the more likely it is that their values-and not just ‘value'- will inform their purchasing decisions. 2 I. Introduction In December of 2016, Congress launched an effort to prevent nondairy drink manufacturers from labeling their products as “milk.” 3 Thirty-two members of the House signed a letter to the Commissioner of the U.S. Food and Drug Administration (“FDA”) claiming that plant-based manufacturers are misleading consumers, and describing nondairy products as “unable to match the nutritional makeup of the product they mimic.” 4 Though dairy consumption has long played a role in society, drinking dairy milk is a fairly new practice beginning in the late nineteenth century. 5 As demand dictates supply, dairy farms became industrial businesses with federal approval to increase milk production by extraordinary means, including injecting cows with various genetically- *482 engineered growth hormones such as bovine growth hormone (“rBST” or “rBGH”). -

Dairy Downfall

DAIRY DOWN For decades, the mechanizedFALL and brutal dairy industry has had a stranglehold on billions of animals—and the American public. But the tides are changing. Investigative journalist Rachel Krantz uncovers what’s driving the plant-based milk revolution, and how Big Dairy is doing everything it can to stop the inevitable takeover. 30 VegNews JULY+AUGUST 2018 Seventy years ago, men in white uniforms delivered glass bottles full of cows’ milk directly to Americans’ doorsteps. At the time, the USDA recommended teenagers consume a minimum of three servings of dairy a day; adults, at least two. Advertising campaigns in the late 20th surplus cheese. It is estimated that the market for plant- century established the myth that milk Yet the size of the dairy lobby—and based milks will reach $35 billion by 2024— was essential to building strong bones and politicians’ fears of alienating voters an astounding 16.6 percent increase from getting enough vitamin D—falsehoods that in the heartland—ensures its political 2013—and industry research forecasts that are still pervasive today. Because of the influence. The subsidization of dairy by the vegan cheese market will only continue dairy industry’s long-standing financial the government is evident in the USDA’s to surge in the next five years. ties with the government, dairy has had massive marketing campaigns to boost “With non-dairy milk, you have an immense influence on the American milk and cheese sales, and the funneling complexity of taste, variety, and these consumer’s perception of health. Today, of dairy products into public school lunch incredibly creamy, amazing products,” that grip is finally slipping. -

August 2021 Ridgefield Region Food Buying Club Note: See Last Page for Symbols, Abbreviations and Warehouse Codes

August 2021 Ridgefield Region Food Buying Club Note: See last page for symbols, abbreviations and warehouse codes. n = Contains Sugar F = Foodservice, Bulk s = Artificial Ingredients G = Foodservice, Grab n' Go 4 = Sulphured D = Foodservice, Supplies _ = 100% Organic K = Gluten Free H = 95%-99% Organic b = Kosher : = Made with 70%-94% Organic Ingredients d = Holiday T = Specialty, Natural Product , = Vegan U = Specialty, Traditional Grocery Product m = NonGMO Project Verified C = Ethnic w = Fair Trade ***THE PAGE NUMBER, Plus the information in BOLDED columns with Arrows "▼", are necessary for placing a Special Order.*** ▼Brand ▼ ▼Item #▼ ▼ Product Description ▼ ▼ Case/Unit Size ▼Whlsle Price▼ Pack/ CS/ DEPT BRAND ITEM # SYMBOL DESCRIPTION UPC Sale Each $ Disc % Disc Size EA BULK BULK GOLDEN TEMPLE BULK Granolas BULK 04078 F Cherry Vanilla 075070-415740 25 LB EA 80.87 3.23 7.57 8.6% BULK 27633 bn Chocolate Chunk Hazelnut 075070-108628 25 LB EA 80.87 3.23 7.57 8.6% BULK 04084 FJb Coconut Almond, WF 075070-415108 25 LB EA 80.87 3.23 7.57 8.6% BULK 04092 F French Vanilla Almond 075070-415252 25 LB EA 80.87 3.23 7.57 8.6% BULK 04094 F Ginger Snap 075070-415276 25 LB EA 80.87 3.23 7.57 8.6% BULK 04087 Fb Maple Almond, CF, WF 075070-415146 25 LB EA 80.87 3.23 7.57 8.6% BULK 04091 Fb Maple Pecan Dream 075070-415436 25 LB EA 80.87 3.23 7.57 8.6% BULK 69081 Pumpkin Flax 075070-108611 25 LB EA 80.87 3.23 7.57 8.6% BULK 04079 nF Strawberry Vanilla Hemp 075070-415771 25 LB EA 80.87 3.23 7.57 8.6% BULK 04088 Fb Super Nutty Crisp Crunchy, WF 075070-415207 -

Middle East & Africa Dairy Alternatives Market Companies Profiles, Size

+44 20 8123 2220 [email protected] Middle East & Africa Dairy Alternatives Market Companies Profiles, Size, Share, Growth, Trends and Forecast to 2025 https://marketpublishers.com/r/MCA2CC94CFDEN.html Date: August 2018 Pages: 100 Price: US$ 2,500.00 (Single User License) ID: MCA2CC94CFDEN Abstracts Middle East & Africa dairy alternatives market is expected register a healthy CAGR in the forecast period 2018 to 2025. The new market report contains data for historic year 2016, the base year of calculation is 2017 and the forecast period is 2018 to 2025. Prominent factors driving the growth of this market consist of rising cases of lactose intolerance among the population, Increased awareness and acceptance of plant based milk, changing dietary preference of consumers due to Increasing health concerns, new product launches and innovations in the dairy alternative products, in dairy alternatives are fuel the growth of dairy alternatives market. The key market players for Middle East & Africa dairy alternatives market are listed below: BLUE DIAMOND GROWERS Danone Hain Celestial Sunopta Sanitarium Health and Wellbeing EARTH'S OWN FOOD COMPANY Inc. Middle East & Africa Dairy Alternatives Market Companies Profiles, Size, Share, Growth, Trends and Forecast to... +44 20 8123 2220 [email protected] Oatly AB GRUPO LECHE PASCUAL SA PURE HARVEST KITE HILL VALSOIA SPA PACIFIC FOODS OF OREGON, LLC. VITASOY INTERNATIONAL HOLDINGS LIMITED Ripple Food The Middle East & Africa dairy alternatives market is segmented into: Products Type Type Formulation Application Nutritive Component Brand Distribution Channel On the basis of product type the Middle East & Africa dairy alternatives market is Middle East & Africa Dairy Alternatives Market Companies Profiles, Size, Share, Growth, Trends and Forecast to.. -

The Plant-Based REVOLUTION March 2018

32 Pleasant Street Sherborn, MA 01770 www.silverwoodpartners.com CONSUMER The Plant-Based REVOLUTION March 2018 Jonathan Hodson-Walker Lars Hem 508.651.2194 508.651.2110 [email protected] [email protected] Gwendalyn Moore Chuck Slotkin 508.651.8134 508.651.2194 [email protected] [email protected] MEMBER FINRA AND SIPC SILVERWOOD PARTNERS A specialized boutique investment bank focused on transaction advisory across three core industries TECHNOLOGY CONSUMER HEALTHCARE • Mobile & Wireless • Food and Beverage Products • HC Information Technology • LOHAS • Internet of Things (IoT) • HC Information Services • Natural • Big Data & Analytics • Organic • Technology Enabled Services • Augmented & Virtual Reality • Functional • Outsourced Medical Device • Artificial Intelligence • Active Lifestyle Products Technology • Media & Consumer Technology • Performance Apparel • OTC/Consumer/Pharma • Sports Equipment COPYRIGHT SILVERWOOD PARTNERS 2001-2018 PAGE 2 SPECIALIZED INVESTMENT BANK – GLOBAL FOCUS Silverwood combines Tier I transaction advisory capabilities with a global focus: • Clients and active contacts in the Americas, Europe and Asia Pacific • Deep expertise in cross border transactions – understand the complexities and intricacies involved in executing complex, cross border deals Representative Silverwood Engagements and Clients COPYRIGHT SILVERWOOD PARTNERS 2001-2018 PAGE 3 THE SILVERWOOD INVESTMENT BANKING TEAM Jonathan Hodson-Walker Lars E. Hem Founder, Managing Partner Managing Director • 25+ -

Uprooting Tradition: What Plant-Based Alternatives Mean for the Future of Protein

Uprooting tradition: What plant-based alternatives mean for the future of protein EQUITY RESEARCH | MAY 12, 2021 For Required Non-U.S. Analyst and Conflicts Disclosures, see page 45. RBC Consumer Equity H Team Click here for contributing C analysts' contact information R A E S May 12, 2021 E RBC Europe Limited Emma Letheren (Analyst) R RBC Imagine™: Uprooting tradition James Edwardes Jones (Analyst) Y What plant-based alternatives mean for the future of protein RBC Capital Markets, LLC T I Our view: Consumers are increasingly shifting to meat and dairy alternatives. Cell-based options are Nik Modi (Analyst) some way from proper commercialisation but plant-based products have taken root. They still only Mehra Romezi (Senior U Associate) represent a fraction of consumption but the direction of travel is clear; as consumers' environmental and Steven Shemesh (AVP) Q health concerns mount and innovation provides more appealing alternatives, plant-based penetration E RBC Dominion Securities will increase rapidly. Inc. Irene Nattel (Analyst) A 2019 Euromonitor survey found that almost 50% of consumers globally restrict their animal product Alex Carette (Senior consumption. We think COVID-19 has exacerbated this, drawing attention to environmental and health Associate) Martin Gravel concerns while lockdown prompted extensive consumer trial. Plant-based meat and dairy growth rates almost doubled in North America and Western Europe in 2020. We’ve interviewed 10 leaders in the space (see p 33) and immersed ourselves in NGO, IGO and academic research to evaluate the plant-based opportunity. While we expect the future of protein will be diverse, we think plant-based alternatives are the immediate disruptors. -

Prod Type Category Description Brand UPC Pk Size Description

Prod Type Category Description Brand UPC Pk Size Description Bulk BULK COATED COCOMELS 0085361000302 1/10 LB COCOMEL,OG2,SEA SALT BITS Bulk BULK COATED COCOMELS 0085361000397 1/10 LB COCOMEL,OG2,SEA SALT Bulk BULK COATED SUNRIDGE FARMS 0008670001630 20/LB CHOCO MALT BALLS, DBLE Bulk BULK COATED SUNRIDGE FARMS 0008670050926 10/# MALT BALLS,MILK CHOC Bulk BULK COATED WHOLESOME 0001251153010 10/LB CANDY,DELISH FISH,OG2 Bulk BULK DRIED FRUIT BULK DRIED FRUIT 0002693877871 5/# COCONUT,SHREDDED,MEDIUM Bulk BULK DRIED FRUIT BULK DRIED FRUIT 0002693830997 5/# APRICOTS,OG2,TRKISH,UNSUL Bulk BULK DRIED FRUIT BULK DRIED FRUIT 0002693831256 5/# PRUNES,OG1,PITTED BULK FLOURS- Bulk SWEETNRS-BAKING SU BOB'S RED MILL 0003997810237 1/25 LB MIX,WAFF & PANCKE,HMESTL BULK FLOURS- BULK FLOURS AND Bulk SWEETNRS-BAKING SU BAKING INGRED 0002693862410 50/# FLOUR,OG1,UNBL WW W/GERM BULK FLOURS- Bulk SWEETNRS-BAKING SU BULK GRAINS 0002693877953 5/# TVP,NON-GMO BULK FLOURS- Bulk SWEETNRS-BAKING SU GINGER PEOPLE 0073402725120 1/25.4 LB CRYSTLZD GINGER,OG2,DICED BULK FLOURS- GREAT RIVER ORGANIC Bulk SWEETNRS-BAKING SU MILLING 0068476521025 25/LB FLOUR,OG1,SPELT,WHOLE GRN BULK FLOURS- GREAT RIVER ORGANIC Bulk SWEETNRS-BAKING SU MILLING 0068476527025 25/LB CORNMEAL,OG1 BULK FLOURS- GREAT RIVER ORGANIC Bulk SWEETNRS-BAKING SU MILLING 0068476540025 25/LB SPRING WHEAT,OG1,HRD RED BULK FLOURS- GREAT RIVER ORGANIC Bulk SWEETNRS-BAKING SU MILLING 0068476555025 25/LB FLR,OG1,WG,HULLED SPELT BULK FLOURS- GREAT RIVER ORGANIC Bulk SWEETNRS-BAKING SU MILLING 0068476569025 25/LB -

Download Report

1 Full Legal Disclaimer This research presentation expresses our research opinions. You should assume that as of the publication date of any presentation, report or letter, Spruce Point Capital Management LLC (“SPCM”) (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our subscribers and clients has a short position in all stocks (and are long/short combinations of puts and calls on the stock) covered herein, including without limitation Oatly Group AB (“OTLY”) and therefore stand to realize significant gains in the event that the price declines. Following publication of any presentation, report or letter, we intend to continue transacting in the securities covered therein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation. All expressions of opinion are subject to change without notice, and Spruce Point Capital Management does not undertake to update this report or any information contained herein. Spruce Point Capital Management, subscribers and/or consultants shall have no obligation to inform any investor or viewer of this report about their historical, current, and future trading activities. This research presentation expresses our research opinions, which we have based upon interpretation of certain facts and observations, all of which are based upon publicly available information, and all of which are set out in this research presentation. Any investment involves substantial risks, including complete loss of capital. There can be no assurance that any statement, information, projection, estimate, or assumption made reference to directly or indirectly in this presentation will be realized or accurate. Any forecasts, estimates, and examples are for illustrative purposes only and should not be taken as limitations of the minimum or maximum possible loss, gain, or outcome.