Industry Structure, Procurement and Innovation in the UK Defence Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Development of a European Defence Technological and Industrial Base 2 / 100 Annex Report September, 2009

Ref. Ares(2015)2207604 - 27/05/2015 Schoemakerstraat 97 P.O. Box 6030 2600 JA Delft The Netherlands www.tno.nl TNO report: Final T +31 15 269 54 43 F +31 15 269 54 60 [email protected] Development of a European Defence Technological and Industrial Base Annex report Date September 2009 Versie 7 Author(s) F. Bekkers (TNO) M. Butter (TNO) E. Anders Eriksson (FOI) E. Frinking (TNO) K. Hartley (CDE) D. Hoffmans (TNO) M. Leis (TNO) M. Lundmark (FOI) H. Masson (FRS) A. Rensma (TNO) G. Willemsen (TNO) Copy no. No. of copies Number of pages 101 Number of appendices Customer European Commission, DG Enterprise and Industry Projectnumber 031.12922 © European Communities, 2009 Reproduction is authorised provided the source is acknowledged The opinions expressed in this study are those of the authors and do not necessarily reflect the views of the European Commission. Final report| Development of a European Defence Technological and Industrial Base 2 / 100 Annex report September, 2009 Introduction to the report This document includes the Annexes to the report “Development of a European Defence Technological and Industrial Base”, which integrates the several outcomes of a study to obtain an in-depth understanding of consequences on the industry structure of the Europeanization of the defense-related industries and markets. The main report identifies possible initiatives for the European Commission and/or the European Defense Agency and contains policy recommendations on various levels. This Annex report includes the following sections: · Annex A: The EU defence industrial base · Annex B: Country case studies · Annex C: Key technological change driver · Annex D: Trends in innovation · Annex E: Primes and the EDTIB Final report| Development of a European Defence Technological and Industrial Base 3 / 100 Annex report September, 2009 A Annex: The EU defence industrial base Introduction1 1. -

International Customer Approvals

Feb 2019 International Customer Approvals This document reflects the approvals our products conform to, for which we have been made aware of. This is not a definitive list and we welcome you to contact us for further details of the specifications you are looking for. • AS9100 (Rev D) NQA Cert 50981 • BS EN ISO 9001-2015 NQA Cert 50981 • BS EN IS0 14001-2015 ISOQAR 8145 • Cage Code K3504 (UK) – Indestructible Paint Ltd • Cage Code 00B6 (USA) – Indestructible Inc. Manufacturing & MRO’s A list of some of the companies we have dealt with historically and currently, some of whom we have gained approvals from. • Airbus UK Ltd / Airbus SAS: 204492 • Honeywell, Phoenix Arizona PCS 5022 • Airfoil Services OSL-006/06 • Hychrome (Europe) Ltd • Allison (RR INC) PMI 200 • ITP, Spain E-200060-SA • British Aerospace PLC, Aircraft Group (BAE/AG/30539/2004) • IHI, Japan • British Aerospace PLC, Civil Aircraft, Air Weapons & Airbus • Kawasaki Heavy Industries, Japan Divisions (BAE/2256, BAE/CHE/2006) • BAE Evaluated Supplier ACO/I/LT/JJH/3244 • Lucas Western • Agusta-Westland Aerospace UK: V02007 (040/92/S) • Marconi Communications • Agusta-Westland Spa • Meggitt (Dunlop) Ltd – Aviation & Precision Rubbers Divisions • Allied Signal • Meggitt Aerospace Braking Systems, Coventry • Avions Marcel Dassault • Meggitt Thermal Systems • Boeing – McDonnell Douglas Helicopters • M.T.U Aeroengines • Bombardier – Supplier Ref: 0000109995 • Pratt & Whitney Canada • BMW – Rolls Royce • Pratt & Whitney USA • Dassault Belgique • Pratt & Whitney Singapore: F038 • Dowty -

International Customer Approvals

JULY 2021 International Customer Approvals This document reflects the approvals our products conform to, for which we have been made aware of. This is not a definitive list and we welcome you to contact us for further details of the specifications you are looking for. • AS9100 (Rev D) NQA Cert 50981 • BS EN ISO 9001-2015 NQA Cert 50981 • BS EN IS0 14001-2015 ISOQAR 8145 • Cage Code K3504 (UK) – Indestructible Paint Ltd • Cage Code 00B6 (USA) – Indestructible Inc. Manufacturing & MRO’s A list of some of the companies we have dealt with historically and currently, some of whom we have gained approvals from. • Airbus UK Ltd / Airbus SAS: 204492 • Honeywell – Normalair Garrett Ltd • Airbus Helicopters Deutschland • Honeywell, Phoenix Arizona PCS 5022 • Airbus Helicopters Marignane • Hychrome (Europe) Ltd • Airfoil Services OSL-006/06 • ITP, Spain E-200060-SA • Allison (RR INC) PMI 200 • IHI, Japan • British Aerospace PLC, Aircraft Group (BAE/AG/30539/2004) • Kawasaki Heavy Industries, Japan • British Aerospace PLC, Civil Aircraft, Air Weapons & Airbus • Lucas Western Divisions (BAE/2256, BAE/CHE/2006) • BAE Evaluated Supplier ACO/I/LT/JJH/3244 • Marconi Communications • Agusta-Westland Aerospace UK: V02007 (040/92/S) • Meggitt (Dunlop) Ltd – Aviation & Precision Rubbers Divisions • Agusta-Westland Spa • Meggitt Aerospace Braking Systems, Coventry • Allied Signal • Meggitt Thermal Systems • Avions Marcel Dassault • M.T.U Aeroengines • Boeing – McDonnell Douglas Helicopters • Pratt & Whitney Canada • Bombardier – Supplier Ref: 0000109995 • Pratt -

Rule 2.7 Announcement Pdf 0,84MB

FINAL NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OR REGULATIONS OF SUCH JURISDICTION THIS ANNOUNCEMENT CONTAINS INSIDE INFORMATION For immediate release 16 August 2021 RECOMMENDED CASH ACQUISITION of Ultra Electronics Holdings plc by Cobham Ultra Acquisitions Limited (a wholly-owned indirect subsidiary of Cobham Group Holdings Limited) to be effected by means of a Scheme of Arrangement under Part 26 of the Companies Act 2006 Summary The boards of directors of Ultra Electronics Holdings plc (“Ultra”) and Cobham Ultra Acquisitions Limited (“Cobham”), a wholly-owned indirect subsidiary of Cobham Group Holdings Limited (“Cobham Group Holdings”), are pleased to announce that they have reached agreement on the terms and conditions of a recommended all cash acquisition of the entire issued, and to be issued, ordinary share capital of Ultra (the “Acquisition”). Under the terms of the Acquisition, each Ultra Shareholder will be entitled to receive: for each Ultra Share: £35.00 in cash In addition, Ultra Shareholders will be entitled to receive, without any consequential reduction in the Consideration, the interim cash dividend of 16.2 pence per Ultra Share as announced by Ultra on 19 July 2021, which is due to be paid by Ultra on 17 September 2021 to those Ultra Shareholders who appear on the register of members of Ultra as at 27 August 2021 (the “Interim Dividend”). The price of £35.00 per Ultra Share, together with the Interim Dividend, values Ultra’s entire issued, and to be issued, ordinary share capital at approximately £2.57 billion on a fully diluted basis, and represents a premium of approximately: 1 63.1 per cent. -

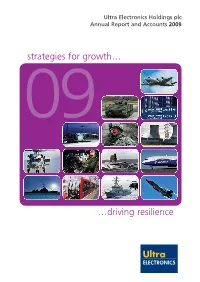

Strategies for Growth… …Driving Resilience

Ultra Electronics Holdings plc Annual Report and Accounts 2009 strategies for growth… 09 …driving resilience Annual Report and Accounts 2009 Cautionary Statement This document contains forward looking statements that are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries and sectors in which the Group operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results to differ materially from those currently anticipated. Ultra’s strategies for growth drive resilience in the Group’s financial performance. Ultra businesses constantly innovate to create solutions to customer requirements that are different from and better than those of the Group’s competitors. 1 Each US Navy MH-60R 6 Ultra supplies the cannon 11 Ultra is providing modern 10 anti-submarine warfare helicopter control electronics for the Chinese airports with advanced, has a digital sonobuoy receiver upgrade of the British Army’s integrated IT solutions 6 11 supplied by Ultra Warrior armoured vehicles 12 Ultra supplies modern high 3 7 12 2 Ultra supplies specialist sensors 7 Ultra is the world’s leading integrity nuclear reactor control and control equipment for US supplier of high capacity line of systems suitable for new build Navy warships sight tactical radio systems and upgrades to existing plant 1 4 8 13 3 Ultra is developing five separate 8 The Royal Navy’s new Astute -

Steven F. Udvar-Hazy, Chairman & CEO • ILFC Colin Stuart, Vice

SPEEDNEWS 20TH ANNUAL AVIATION INDUSTRY SUPPLIERS CONFERENCE Steven F. Udvar-Hazy, Chairman & CEO • ILFC Mr. Hazy, in 1973, founded Interlease Group, Inc., which today is known as International Lease Finance Corporation (ILFC), with a portfolio valued at more than $40b, consisting of more than 800 jet aircraft. ILFC is the largest customer of Airbus and Boeing. ILFC went public in 1983 with $220 million in assets and $8 million in profit. In 1990, ILFC was acquired by American Intl. Group, and since the acquisition, ILFC has generated a cumulative profit of $8.3b for AIG. In 1966, while an undergraduate student at UCLA, he formed Airlines Systems Research Consultants, a firm specializing in airline routes, fleet and planning analysis. His first clients included Aer Lingus, Mexicana and Air New Zealand. He later graduated from UCLA in 1968 with a BS in Economics and a minor in Intl. Relations. Mr. Hazy also serves on the Board of Directors of Skywest, Inc., and is on the Board of several foundations, educational institutions and corporations, and is the major donor for the Smithsonian National Air and Space Museum. He also has pilot type ratings in Gulfstreams, Learjets, Citations and presently is captain on the GV. Colin Stuart, Vice President-Marketing • Airbus Colin Stuart was appointed to his current position, VP-Marketing, in May 1996. His responsibilities include managing both the development and implementation of customer/product marketing activities and related marketing support services for the complete range of Airbus commercial products. He studied under the British Aerospace undergraduate apprenticeship scheme before obtaining a degree in aeronautical engineering from Bath University in 1966. -

September 2016

DAILY SERVICES AT GLOUCESTER CATHEDRAL SUNDAY NEWS 7.40am Morning Prayer (said) 8.00am Holy Communion 10.15am Sung Eucharist with Children’s Church 3.00pm Choral Evensong SEPTEMBER 2016 MONDAY - SATURDAY 8.00am Holy Communion 8.30am Morning Prayer (said) 12.30pm Holy Communion 5.30pm Choral Evensong (said Evening Prayer on Mondays) (4.30pm on Saturdays) See our website for details of services and any changes or closures. A Gift Aid scheme operates at the Cathedral, which allows the Chapter to claim back 25p per £1 for donations. Many of you do so already, and we are grateful, but if you are a visitor who pays Income Tax in the UK, you could make your donation go further by doing this. There is a Donorpoint at the West end of the Cathedral where you can use your credit card to give a donation, and this can be gift- aided as well Printed by Perpetua Press, 20 Culver Street, Newent, Glos. GL18 1DA Tel: 01531 820816 32 Gloucester Cathedral News The Editorial Team consists of: Richard Cann, Sandie Conway, Pat Foster, Barrie Glover, Mission Statement: Stephen Lake, Christopher and Maureen Smith. ‘We aim to produce a Christian magazine which is widely accessible and which informs, involves and inspires its readers.’ Editor: Maureen Smith Cathedral Chapter The next Editorial meeting is on Monday 12th September at 10.30am. Dean: The Very Reverend Stephen Lake Canons: Lay Canons: Nikki Arthy John Coates "We are happy to receive articles, handwritten or typed. We regret that, due to the limited space available, and to enable us to Dr Andrew Braddock Paul Mason continue to produce a lively, varied and informative magazine, we Jackie Searle Dame Janet Trotter can normally only accept articles of 400 words or less. -

FTSE 100 Constituent History Updated

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C. -

View Annual Report

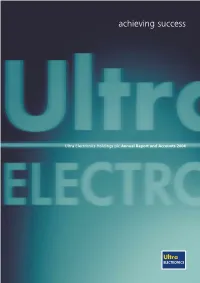

achieving success Ultra Electronics Holdings plc Annual Report and Accounts 2004 Financial Highlights achieving success 2004 2003 GROWTH TURNOVER (£m) 319.7 284.4 +12.4% ULTRA ELECTRONICS IS A GROUP OF SPECIALIST BUSINESSES DESIGNING, PROFIT BEFORE TAXATION (£m)* 39.7 34.4 +15.5% MANUFACTURING AND SUPPORTING ELECTRONIC AND ELECTROMECHANICAL SYSTEMS, SUB-SYSTEMS AND PRODUCTS FOR DEFENCE, SECURITY AND EARNINGS PER SHARE* 44.1p 38.2p +15.4% AEROSPACE APPLICATIONS WORLDWIDE. OPERATING PROFIT MARGIN* 13.3% 13.2% ULTRA, WHICH EMPLOYS 2,800 PEOPLE IN THE UK AND NORTH AMERICA, EMPLOYEES (AVERAGE NUMBER) 2,678 2,505 FOCUSES ON HIGH INTEGRITY SENSING, CONTROL, COMMUNICATION AND DISPLAY SYSTEMS WITH AN EMPHASIS ON INTEGRATED INFORMATION TECHNOLOGY SOLUTIONS. THE GROUP CONCENTRATES ON OBTAINING A TECHNOLOGICAL EDGE IN NICHE MARKETS, WITH MANY OF ITS PRODUCTS AND TECHNOLOGIES BEING MARKET LEADERS IN THEIR FIELD. Turnover Profit before taxation* ULTRA’S PRODUCTS AND SERVICES ARE USED IN AIRCRAFT, SHIPS, £319.7m £39.7m SUBMARINES, ARMOURED VEHICLES, SURVEILLANCE AND COMMUNICATION 04 04 03 03 SYSTEMS, AIRPORTS AND TRANSPORT SYSTEMS AROUND THE WORLD. 02 01 02 ULTRA ALSO PLAYS AN IMPORTANT ROLE IN SUPPORTING PRIME 00 01 00 CONTRACTORS BY UNDERTAKING SPECIALIST SYSTEM AND SUB-SYSTEM INTEGRATION USING THE COMBINED EXPERTISE OF THE GROUP BUSINESSES. Financial Highlights 01 Directors‘ Report 27 Consolidated Statement of Total £260.4m £239.5m £226.9m £284.4m £319.7m £29.9m £34.4m £39.7m £25.6m £27.1m Recognised Gains and Losses 44 Ultra Electronics At a Glance -

Cobham Plc Annual Report and Accounts 2009

Cobham plc Annual Report and Accounts 2009 The most important thing we build is trust Cobham plc Cobham Annual Report and Accounts 2009 Accounts and Report Annual The most important thing we build is trust www.cobham.com Cobham plc Brook Road, Wimborne, Dorset, BH21 2BJ England www.cobham.com T: +44 (0)1202 882 020 F: +44 (0)1202 840 523 Cobham’s products and services have been at the heart of sophisticated military and civil systems for 75 years, keeping people safe, improving communications, and enhancing the capability of land, marine, air and space platforms. The Group has four divisions employing some 12,000 people on five continents, with customers and partners in more than 100 countries. Front cover image Deployed to Iraq as a US military reserve helicopter pilot, Cobham employee Larry Kamps was protected from heat stress by wearing one of 15,000 military issue Micro Cooling Unit (MCU) systems supplied by Cobham Life Support, the Cobham business unit in which he is employed in civilian life. The MCU circulates cooling liquid through a vest worn under the uniform and has been shown to triple the effective endurance of helicopter pilots on operations. 1. Organic revenue growth is defined as revenue growth stated the integration activity originate from the Group’s strategy at constant translation exchange, excluding the incremental announcement in September 2005. The 2005 portfolio effect of acquisitions and disposals. restructuring is now substantially complete and restructuring 2. Cobham’s Technology Divisions comprise Cobham Avionics costs arising after 2009 are to be reported as part of the underlying and Surveillance, Cobham Defence Systems and Cobham result. -

Supplementary Papers

May 1968 SUPPLEMENTARY PAPERS The Non-members issue of this Journal contains the following Supplementary papers: Page Reprint price Turbulent Boundary Layers—P. Bradshaw 451-459 3s. Od. A Hydraulic Transmission System for Powered Wind-Tunnel Models —K. J. England 460-466 2s. 6d. SUMMARIES OF THESE PAPERS ARE GIVEN OVERLEAF. IF YOU REQUIRE REPRINTS OF THE PAPERS PLEASE USE THE ORDER FORM BELOW. ^< ORDER FORM MAY 1968 PUBLICATIONS DEPT., Royal Aeronautical Society 4 Hamilton Place, London W.I. Please send me the following Supplementary Paper(s) Title For which I enclose s. d. including 6d. postage (1s. 9d. if 2nd class air mail required) Name (Block letters please) Grade Address N.B. Members are reminded that they may have the non-member's Journal at the special rate ot £2 10s. Od. per annum (Graduates and Students £1 10s. Od.) but are requested to return their own copies. BRADSHAW, P. ENGLAND, K. J. Turbulent Boundary Layers A Hydraulic Transmission System for Powered Wind-Tunnel Much of a designer's time is spent in estimating or avoid Models ing the effects of turbulent boundary layers. Although crude, A hydraulic transmission system is evaluated as a drive boundary layer calculation methods suffice for predicting for wind-tunnel model propellers and fans. The system profile drag in the absence of separation, the prediction or compares favourably with existing electrical transmission avoidance of separation is a much more delicate business. systems and appears to have other applications in wind-tunnel Intuition and experience, supported by tunnel tests, are more work. trustworthy than the best theories. -

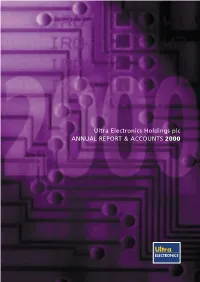

Ultra Electronics Holdings Plc ANNUAL REPORT & ACCOUNTS

Ultra Electronics Holdings plc ANNUAL REPORT & ACCOUNTS 2000 Ultra Electronics is a group of specialist businesses designing, manufacturing and supporting electronic and electromechanical systems, sub-systems and products for international defence and aerospace markets. The group, which employs 2,500 people in the UK and North America, focuses on high integrity sensing, control, communication and display systems with an increasing emphasis on integrated Information Technology solutions. The Group concentrates on obtaining a technological edge in niche markets, with many of its products and technologies being market leaders in their field. Financial Highlights 1 Ultra Electronics at a Glance 2 Chairman‘s Statement 3 Chief Executive‘s Operations Review 4 Financial Review 18 Board of Directors 22 Executives and Advisors 24 Directors‘ Report 25 Corporate Governance 32 Auditors’ Report 34 Consolidated Profit and Loss Account 36 Balance Sheets 37 Consolidated Cashflow Statement 38 Consolidated Statement of Total Recognised Gains and Losses 38 THE QUEEN’S AWARDS FOR ENTERPRISE 2000 Notes to Accounts 39 THE QUEEN’S AWARD HIPSS ULTRAQUIET THE QUEEN’S AWARD FOR TECHNOLOGICAL IN THE HUB, CABIN FOR ENTERPRISE 2000 Shareholder Analysis 61 ACHIEVEMENT POWER GENERATION AIRCRAFT CABIN FOR THE FOR NOISE AND FOR PROPELLER NOISE REDUCTION MAGICARD PRINTER Notice of Meeting 62 VIBRATION SYSTEMS DE-ICING SYSTEM AT OCEAN SYSTEMS highlightsFinancial Highlights 2000 1999 £m £m Growth Turnover 226.9 193.0 +18% Profit before taxation* 25.6 23.2 +10% Earnings per