1. Global Fleet & MRO Market Forecast Commentary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A China Perspective • Domestic COVID-19 Situation • Aerospace Landscape • Q&A This PPT Should Be Viewed in PRESENTATION Mode

Presented by Dennis Scott Ass, Chief Designer: COMAC (since August 2011) A China Perspective • Domestic COVID-19 situation • Aerospace Landscape • Q&A This PPT should be viewed in PRESENTATION mode. These views are my personal opinion [email protected] and do not reflect the position of COMAC. Private & Confidential May 2020-V3 All Rights Reserved 2020 Dennis Scott: China Perspective 1. Coronavirus Situation • China has successfully completed the Coronavirus cycle (<5 new cases/<10 new symptomless cases per day). • All businesses, schools, colleges, sports centres have re-opened. 3 vaccines undergoing trials. • Currently, only Chinese nationals/Green Card holders allowed to enter China. • Every person entering China is tested before being quarantined for 14 days. Testing widely available. Private & Confidential Dennis Scott: China Perspective 1. Coronavirus Situation • Domestic flights now back up to 80+% of pre-virus level (trains are now essentially fully operational). • Discussions ongoing with Dubai, Singapore, Thailand, Vietnam and New Zealand on how/when to re- start international flights, potentially from May 22nd (Emirates have started COVID-19 testing before check-in). • Comprehensive financial support has been provided to Chinese airlines and business in general. • Airline consolidation expected (Hainan Airlines + subsidiaries is a prime candidate). Private & Confidential • Drastic reduction/deferral of new aircraft orders and severe reduction in maintenance/after sales activities. • Aerospace supply chain facing a 30 to 50% reduction in order intake (short term). • Excess capacity and headcount is a global issue across the industry (but is not such4 a problem in China). Private & Confidential Dennis Scott: China Perspective 2. China Aviation Industry Overview • China was already a key aircraft market before COVID-19, with 25% of Airbus and Boeing production going to Chinese airlines. -

Economic Feasibility Study for a 19 PAX Hybrid-Electric Commuter Aircraft

Air s.Pace ELectric Innovative Commuter Aircraft D2.1 Economic Feasibility Study for a 19 PAX Hybrid-Electric Commuter Aircraft Name Function Date Author: Maximilian Spangenberg (ASP) WP2 Co-Lead 31.03.2020 Approved by: Markus Wellensiek (ASP) WP2 Lead 31.03.2020 Approved by: Dr. Qinyin Zhang (RRD) Project Lead 31.03.2020 D2.1 Economic Feasibility Study page 1 of 81 Clean Sky 2 Grant Agreement No. 864551 © ELICA Consortium No export-controlled data Non-Confidential Air s.Pace Table of contents 1 Executive summary .........................................................................................................................3 2 References ........................................................................................................................................4 2.1 Abbreviations ...............................................................................................................................4 2.2 List of figures ................................................................................................................................5 2.3 List of tables .................................................................................................................................6 3 Introduction ......................................................................................................................................8 4 ELICA market study ...................................................................................................................... 12 4.1 Turboprop and piston engine -

Air Line Pilots Page 5 Association, International Our Skies

March 2015 ALSO IN THIS ISSUE: » Landing Your » Known Crewmember » Sleep Apnea Air Dream Job page 20 page 29 Update page 28 Line PilOt Safeguarding Official Journal of the Air Line Pilots page 5 Association, International Our Skies Follow us on Twitter PRINTED IN THE U.S.A. @wearealpa Sponsored Airline- Career Track ATP offers the airline pilot career training solution with a career track from zero time to 1500 hours sponsored by ATP’s airline alliances. Airline Career month FAST TRACK Demand for airline pilots and ATP graduates is soaring, Pilot Program with the “1500 hour rule” and retirements at the majors. AIRLINES Airlines have selected ATP as a preferred training provider to build their pilot pipelines Private, Instrument, Commercial Multi Also available with... & Certified Flight Instructor (Single, Multi 100 Hours Multi-Engine Experience with the best training in the fastest & Instrument) time frame possible. 225 Hours Flight Time / 100 Multi 230 Hours Flight Time / 40 Multi In the Airline Career Pilot Program, your airline Gain Access to More Corporate, Guaranteed Flight Instructor Job Charter, & Multi-Engine Instructor interview takes place during the commercial phase Job Opportunities of training. Successful applicants will receive a Airline conditional offer of employment at commercial phase of training, based on building Fly Farther & Faster with Multi- conditional offer of employment from one or more of flight experience to 1500 hours in your guaranteed Engine Crew Cross-Country ATP’s airline alliances, plus a guaranteed instructor CFI job. See website for participating airlines, Experience job with ATP or a designated flight school to build admissions, eligibility, and performance requirements. -

Air Transport Industry Analysis Report

Annual Analyses of the EU Air Transport Market 2016 Final Report March 2017 European Commission Annual Analyses related to the EU Air Transport Market 2016 328131 ITD ITA 1 F Annual Analyses of the EU Air Transport Market 2013 Final Report March 2015 Annual Analyses of the EU Air Transport Market 2013 MarchFinal Report 201 7 European Commission European Commission Disclaimer and copyright: This report has been carried out for the Directorate General for Mobility and Transport in the European Commission and expresses the opinion of the organisation undertaking the contract MOVE/E1/5-2010/SI2.579402. These views have not been adopted or in any way approved by the European Commission and should not be relied upon as a statement of the European Commission's or the Mobility and Transport DG's views. The European Commission does not guarantee the accuracy of the information given in the report, nor does it accept responsibility for any use made thereof. Copyright in this report is held by the European Communities. Persons wishing to use the contents of this report (in whole or in part) for purposes other than their personal use are invited to submit a written request to the following address: European Commission - DG MOVE - Library (DM28, 0/36) - B-1049 Brussels e-mail (http://ec.europa.eu/transport/contact/index_en.htm) Mott MacDonald, Mott MacDonald House, 8-10 Sydenham Road, Croydon CR0 2EE, United Kingdom T +44 (0)20 8774 2000 F +44 (0)20 8681 5706 W www.mottmac.com Issue and revision record StandardSta Revision Date Originator Checker Approver Description ndard A 28.03.17 Various K. -

A Conceptual Design of a Short Takeoff and Landing Regional Jet Airliner

A Conceptual Design of a Short Takeoff and Landing Regional Jet Airliner Andrew S. Hahn 1 NASA Langley Research Center, Hampton, VA, 23681 Most jet airliner conceptual designs adhere to conventional takeoff and landing performance. Given this predominance, takeoff and landing performance has not been critical, since it has not been an active constraint in the design. Given that the demand for air travel is projected to increase dramatically, there is interest in operational concepts, such as Metroplex operations that seek to unload the major hub airports by using underutilized surrounding regional airports, as well as using underutilized runways at the major hub airports. Both of these operations require shorter takeoff and landing performance than is currently available for airliners of approximately 100-passenger capacity. This study examines the issues of modeling performance in this now critical flight regime as well as the impact of progressively reducing takeoff and landing field length requirements on the aircraft’s characteristics. Nomenclature CTOL = conventional takeoff and landing FAA = Federal Aviation Administration FAR = Federal Aviation Regulation RJ = regional jet STOL = short takeoff and landing UCD = three-dimensional Weissinger lifting line aerodynamics program I. Introduction EMAND for air travel over the next fifty to D seventy-five years has been projected to be as high as three times that of today. Given that the major airport hubs are already congested, and that the ability to increase capacity at these airports by building more full- size runways is limited, unconventional solutions are being considered to accommodate the projected increased demand. Two possible solutions being considered are: Metroplex operations, and using existing underutilized runways at the major hub airports. -

Sector Update – January 2021

SEVEN UK AND IRISH SECTORUPDATE AIRPORTS ACHIEVE CARBON NEUTRALITY RVLNEWS Seven British and Irish airports – including RVL Group’s home base East Midlands – have JANUARY ISSUE 11 achieved carbon neutrality, according to the Airport Carbon Accreditation Programme (ACA). The seven are: London Gatwick, London City, Manchester, East Midlands, London Stansted, Farnborough and Dublin. According to the ACA, to achieve ‘Level 3+ Neutrality’ status airports must meet a number of criteria, including determination of emissions sources within the operational boundary of the airport company; calculation of the annual carbon emissions; compilation of a carbon footprint report; provision of evidence of effective carbon management procedures; demonstration of quantified emissions reductions; and offsetting of emissions with RVL ADDS CAPACITY high quality carbon credits. WITH NEW AIRCRAFT Most airports are achieving this RVL Aviation, an RVL Group company, is set to start 2021 in a typically positive by the use of alternative energy, and enthusiastic style with a huge expansion of its cargo capacity. The East Midlands such as creating their own solar farms or using bio-energies. Other Airport based airline has taken delivery of its first Saab 3 0B freighter, as part of - 4 factors include the use of energy- a multi aircraft deal. Each Saab offers roughly four times the cargo volume and - efficient lighting and heating and payload of aircraft in RVL’s existing fleet of Reims-Cessna F406s and King Air QC switching to electric vehicles. cargo aircraft. (Link: UK Aviation News) “Our customers have been asking us for larger aircraft and we are poised to deliver them,” said RVL’s Head of Commercial, David Lacy. -

Global Aviation Holdings: the KERP Is Back

Portfolio Media. Inc. | 860 Broadway, 6th Floor | New York, NY 10003 | www.law360.com Phone: +1 646 783 7100 | Fax: +1 646 783 7161 | [email protected] Global Aviation Holdings: The KERP Is Back Law360, New York (August 06, 2012, 1:11 PM ET) -- In a recent decision[1] involving Global Aviation Holdings Inc. and its affiliated debtors (collectively, the “debtors”), the United States Bankruptcy Court for the Eastern District of New York granted the debtors' motion for approval of a key employee retention plan (the “KERP motion”) pursuant to Sections 363(b) and 503(c)(3) of Title 11 of the United States Code over the objections of both the United States Trustee for Region 2 (the “UST”) and the official committee of unsecured creditors (the “committee”). In the objections, the committee and the UST argued the debtors were seeking to pay bonuses to insiders without satisfying the requirements set forth in Section 503(c)(1) of the Bankruptcy Code. The committee and the UST also argued, that to the extent the key employee retention plan recipients turned out to be non-insiders, the debtors did not establish whether the proposed key employee retention plan payments were “justified by the facts and circumstances of the case” as required by Section 503(c)(3) of the Bankruptcy Code. The debtors operate two airlines: North American Airlines Inc. and World Airways Inc. From the outset of their bankruptcy cases, the debtors planned to move North American’s headquarters from JFK International Airport in Jamaica, N.Y., to World’s headquarters in Peachtree City, Ga., in order to consolidate operations. -

July 2020 Edition

WASHINGTON AVIATION SUMMARY JULY 2020 EDITION CONTENTS I. REGULATORY NEWS .............................................................................................. 1 II. AIRPORTS ................................................................................................................3 III. SECURITY AND DATA PRIVACY ............................................................................6 IV. TECHNOLOGY AND EQUIPMENT...........................................................................7 V. ENERGY AND ENVIRONMENT ................................................................................ 8 VI. U.S. CONGRESS.................................................................................................... ...9 VII. BILATERAL AND STATE DEPARTMENT NEWS ................................................... 14 VIII. EUROPE/AFRICA ................................................................................................... 15 IX. ASIA/PACIFIC/MIDDLE EAST ................................................................................ 17 X. AMERICAS .............................................................................................................1 9 For further information, including documents referenced, contact: Joanne W. Young Kirstein & Young PLLC 1750 K Street NW Suite 700 Washington, D.C. 20006 Telephone: (202) 331-3348 Fax: (202) 331-3933 Email: [email protected] http://www.yklaw.com The Kirstein & Young law firm specializes in representing U.S. and foreign airlines, airports, leasing companies, -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

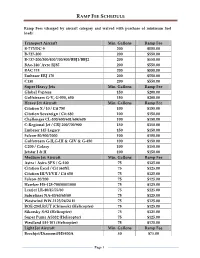

Ramp Fee Schedule

RAMP FEE SCHEDULE Ramp Fees (charged by aircraft category and waived with purchase of minimum fuel load): Transport Aircraft Min. Gallons Ramp Fee B-717/DC-9 200 $550.00 B-727-200 200 $550.00 B-737-200/300/400/700/800/BBJ1/BBJ2 200 $550.00 BAe-146/ Avro RJ85 200 $550.00 BAC 111 200 $550.00 Embraer ERJ 170 200 $550.00 C130 200 $550.00 Super Heavy Jets Min. Gallons Ramp Fee Global Express 150 $200.00 Gulfstream G-V, G-550, 650 150 $200.00 Heavy Jet Aircraft Min. Gallons Ramp Fee Citation X / 10 / Cit 750 100 $150.00 Citation Sovereign / Cit 680 100 $150.00 Challenger CL-300/600/601/604/605 100 $150.00 C-Regional Jet / CRJ 200/700/900 150 $150.00 Embraer 145 Legacy 150 $150.00 Falcon-50/900/2000 100 $150.00 Gulfstream G-II,G-III & GIV & G-450 100 $150.00 G200 / Galaxy 100 $150.00 Jetstar I & II 100 $150.00 Medium Jet Aircraft Min. Gallons Ramp Fee Astra / Astra SPX / G-100 75 $125.00 Citation Excel / Cit 560XL 75 $125.00 Citation III/VI/VII / Cit 650 75 $125.00 Falcon-20/200 75 $125.00 Hawker HS-125-700/800/1000 75 $125.00 Learjet LR-40/45/55/60 75 $125.00 Sabreliner NA-40/60/65/80 75 $125.00 Westwind WW-1123/24/24 II 75 $125.00 BOE-234LR/UT (Chinook) (Helicopter) 75 $125.00 Sikorsky S-92 (Helicopter) 75 $125.00 Super Puma AS332 (Helicopter) 75 $125.00 Westland EH-101 (Helicopter) 75 $125.00 Light Jet Aircraft Min. -

Global Fleet & Mro Market Forecast Summary

GLOBAL FLEET & MRO MARKET FORECAST SUMMARY 2017-2027 AUTHORS Tom Cooper, Vice President John Smiley, Senior Manager Chad Porter, Technical Specialist Chris Precourt, Technical Analyst For over a decade, Oliver Wyman has surveyed aviation and aerospace senior executives and industry influencers about key trends and challenges across the Maintenance, Repair, and Overhaul market. If you are responsible for maintenance and engineering activities at a carrier, aftermarket activities at an OEM, business operations at an MRO, or a lessor, you may want to participate in our survey. For more information, please contact our survey team at: [email protected]. To read last year’s survey, please see: http://www.oliverwyman.com/our-expertise/insights/2016/apr/mro-survey-2016.html . CONTENTS 1. EXECUTIVE SUMMARY 1 2. STATE OF THE INDUSTRY 5 Global Economic Outlook 7 Economic Drivers 11 3. FLEET FORECAST 17 In-Service Fleet Forecast 18 4. MRO MARKET FORECAST 31 Copyright © Oliver Wyman 1 EXECUTIVE SUMMARY EXECUTIVE SUMMARY Oliver Wyman’s 2017 assessment and 10-year outlook for the commercial airline transport fleet and the associated maintenance, repair, and overhaul (MRO) market marks the 17th year of supporting the industry with informed, validated industry data. This has become the most credible go-to forecast for many executives in the airline and MRO industry as well as for those with financial interests in the sector, such as private equity firms, investment banks and investment analysts. The global airline industry has made radical changes in the last few years and is producing strong financial results. While the degree of success varies among the world regions, favorable fuel prices and widespread capacity discipline are regarded as key elements in the 2016 record high in global profitability ($35.6 billion). -

North American Airlines Take Off by Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim

The 2017 Consumer Value Creators Series NorTh AmeriCAN AirliNeS TAke off By Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim he airline industry is dominating The Top Ten Tthe travel and tourism sector—out- Of the top ten performers on this year’s pacing hotels, cruise lines, and others in travel and tourism list, nine are in the air- the sector in terms of value creation. North line industry and seven are based in North American carriers in particular have bene- America. (See the exhibit.) That includes fited from restructuring, scale efficiencies, five US carriers: and consolidation over the past decade, giving them a strong position and lower • Hawaiian Holdings, parent company of costs in a robust market. Hawaiian Airlines (which finished first) In 2017, The Boston Consulting Group con- • Delta Air Lines (fourth) ducted its annual study of the total share- holder return (TSR) of more than 2,300 • Southwest Airlines (fifth) publicly traded companies in 33 industry sectors, including 80 companies in travel • Alaska Air Group (sixth) and tourism. (See “How Top Value Creators Outpace the Market—for Decades,” BCG • JetBlue Airways (tenth) article, July 2017.) It’s tempting to cite lower fuel costs as the From 2012 through 2016, the global travel reason for this collective strength, but and tourism sector delivered an average that’s likely a subordinate factor at best. annual return of 19%. It ranked ninth Lower fuel prices affect all carriers world- among the 33 sectors we analyzed and sec- wide, not only those in the US. ond among the five consumer segments.