Ziggo Group Holding B.V. Annual Report for the Year Ended

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Broadband Services and Local Loop Unbundling in the Netherlands Nico Van Eijk, Institute for Information Law

Broadband Services and Local Loop Unbundling in the Netherlands Nico van Eijk, Institute for Information Law This article describes the availability of broadband services in the ABSTRACT Netherlands. This particularly concerns broadband services for the consumer/end user such as access to the Internet. We will first discuss the new telecommunications act before dealing with current market relations and regulation of the (until 15 December 2000). This means telecommunications sector. This is followed by a description of the most significant deci- that — in accordance with the Euro- sions of the independent supervisory body, the Independent Post and Telecommunications pean directives — KPN has special obli- Authority, as related to broadband services. gations concerning interconnection and other forms of special access to its net- work. KPN is also responsible for pro- viding universal service (primarily he Netherlands has always been keen to take the traditional voice telephony service). On the expiration of the T lead in liberalizing the telecommunications sector. statutorily prescribed period of two years, whether KPN is still Nevertheless, it was not until the end of 1998 that Dutch leg- in the same position will again need to be established. It is islation satisfied all the underlying principles of European implicitly assumed that the operators of broadcasting networks telecommunications regulations. (the legal term for cable television networks) have significant This does not diminish the fact that, in the previous peri- market power regarding the transmission of programming. od, important liberalizations had occurred. In 1996–1997 all The market position of KPN is thus also at issue in regard to restrictions to offering telecommunications services — with the question of whether local differences in rates for public voice the exception of voice telephony — were discontinued. -

TV Channel Distribution in Europe: Table of Contents

TV Channel Distribution in Europe: Table of Contents This report covers 238 international channels/networks across 152 major operators in 34 EMEA countries. From the total, 67 channels (28%) transmit in high definition (HD). The report shows the reader which international channels are carried by which operator – and which tier or package the channel appears on. The report allows for easy comparison between operators, revealing the gaps and showing the different tiers on different operators that a channel appears on. Published in September 2012, this 168-page electronically-delivered report comes in two parts: A 128-page PDF giving an executive summary, comparison tables and country-by-country detail. A 40-page excel workbook allowing you to manipulate the data between countries and by channel. Countries and operators covered: Country Operator Albania Digitalb DTT; Digitalb Satellite; Tring TV DTT; Tring TV Satellite Austria A1/Telekom Austria; Austriasat; Liwest; Salzburg; UPC; Sky Belgium Belgacom; Numericable; Telenet; VOO; Telesat; TV Vlaanderen Bulgaria Blizoo; Bulsatcom; Satellite BG; Vivacom Croatia Bnet Cable; Bnet Satellite Total TV; Digi TV; Max TV/T-HT Czech Rep CS Link; Digi TV; freeSAT (formerly UPC Direct); O2; Skylink; UPC Cable Denmark Boxer; Canal Digital; Stofa; TDC; Viasat; You See Estonia Elion nutitv; Starman; ZUUMtv; Viasat Finland Canal Digital; DNA Welho; Elisa; Plus TV; Sonera; Viasat Satellite France Bouygues Telecom; CanalSat; Numericable; Orange DSL & fiber; SFR; TNT Sat Germany Deutsche Telekom; HD+; Kabel -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

OPTA Analyst Meeting

OPTA analyst meeting January 23, 2008 Programme • 13.00 The main developments on the electronic communications and postal markets, by –Johan Keetelaar and Christa Cramer (electronic communications) –Symen Formsma (postal affairs) • Questions (also through internet) • 14.00 End of meeting Market developments • Convergence • Bundling • Recommendation • Market analyses Increase in bundles • Triple play: mostly cable • Dual play fixed+bb: DSL Increase digital telephony 6.000.000 5.000.000 4.000.000 3.000.000 2.000.000 1.000.000 • 42% of consumer0 telephony now digital • Over 5% fixed consumer telephony WLR within one year • 17.7% mobile onlyQ10 households5 Q205 Q305 Q405 Q106 Q206 Q306 PSTN/ISDN Q406 WLR Q107 Digital Telephony Total telephony Q207 Q307 Q3 2007, Te lecompaper Mobile retail market shares Q307 Q306 KPN 4% 11% 6% Vodafone 14% 49% T-Mobile (incl. Orange) Orange 26% 22% KPN SP's, MVNO's Vodafone 47% T-Mobile (incl. Orange) SP's, MVNO's 21% • Merger T-Mobile/Orange • Growth of service providers • Postpaid 47%, up from 44% Q306 • Over 18.9 mln customers Q3 2007, Telecompaper Broadcast retail market shares 6% 2% Zesko (@Hom e, Casema, Multikabel) (cable) 11% UPC (cable) 3% Delta (cable) 2% 44% CAIW (cable) 2% Other cable Canal Digitaal (satellite) KPN (m os tly DVB-T, s om e IPTV) 30% Tele2 (IPTV) • 81% cable, compared to 87% in Q306 Q3 2007, Telecompaper Steady growth of digital TV 40% 35% 30% 25% 20% 15% 10% 5% 0% Q403 Q104 • From 29% Q306 toQ2 38%04 Q307 (of all RTV subscriptions) • Digital cable includesCable analogueQ304 signal -

Internal Memorandum

Non-confidential version text which has been removed from the confidential version is marked [business secrets] or [XXX] as the case may be Case handlers: Tormod S. Johansen, Brussels, 11 July 2007 Runa Monstad Tel: (+32)(0)2 286 1841/1842 Case No: 13114 e-mail: [email protected] Event No: 436086 By fax (+47 22 83 07 95) and courier Viasat AS Care of: BA-HR Advokatfirma Att: Mr. Helge Stemshaug Postboks 1524 Vika N-0117 Oslo Norway Dear Mr. Stemshaug, Case COM 13114 (former case COM 020.0173) - Viasat/TV2/Canal Digital Norge (please quote this reference in all correspondence) I refer to the application of Viasat AS dated 30 July 2001, pursuant to Article 3 of Chapter II of Protocol 41 to the Agreement between the EFTA States on the Establishment of a Surveillance Authority and a Court of Justice (hereinafter “Surveillance and Court Agreement”), regarding alleged infringements of Articles 53 and 54 of the Agreement on the European Economic Area (hereinafter “EEA Agreement” or “EEA”) by TV2 Gruppen AS and Canal Digital Norge AS. By this letter I inform you that, pursuant to Article 7(1) of Chapter III of Protocol 4 to the Surveillance and Court Agreement,2 the Authority considers that, for the reasons set out below and on the basis of the information in its possession, there are insufficient grounds for acting on your complaint. 1 As applicable before the entry into force of the Agreement amending Protocol 4 of 24 September 2004 (e.i.f. 20.5.2005). 2 As applicable after the entry into force of the Agreement amending Protocol 4 of 3 December 2004 (e.i.f. -

Analysys Mason Report on Developments in Cable for Superfast Broadband

Final report for Ofcom Future capability of cable networks for superfast broadband 23 April 2014 Rod Parker, Alex Slinger, Malcolm Taylor, Matt Yardley Ref: 39065-174-B . Future capability of cable networks for superfast broadband | i Contents 1 Executive summary 1 2 Introduction 5 3 Cable network origins and development 6 3.1 History of cable networks and their move into broadband provision 6 3.2 The development of DOCSIS and EuroDOCSIS 8 4 Cable network elements and architecture 10 4.1 Introduction 10 4.2 Transmission elements 10 4.3 Description of key cable network elements 13 4.4 Cable access network architecture 19 5 HFC network implementation, including DOCSIS 3.0 specification 21 5.1 Introduction 21 5.2 HFC performance considerations 21 5.3 Delivery of broadband services using DOCSIS 3.0 24 5.4 Limitations of DOCSIS 3.0 specification 27 5.5 Implications for current broadband performance under DOCSIS 3.0 30 6 DOCSIS 3.1 specification 33 6.1 Introduction 33 6.2 Reference architecture 34 6.3 PHY layer frequency plan 35 6.4 PHY layer data encoding options 37 6.5 MAC and upper layer protocol interface (MULPI) features of DOCSIS 3.1 39 6.6 Development roadmap 40 6.7 Backwards compatibility 42 6.8 Implications for broadband service bandwidth of introducing DOCSIS 3.1 43 6.9 Flexibility of DOCSIS 3.1 to meet evolving service demands from customers 47 6.10 Beyond DOCSIS 3.1 47 7 Addressing future broadband growth with HFC systems – expanding DOCSIS 3.0 and migration to DOCSIS 3.1 49 7.1 Considerations of future broadband growth 49 7.2 Key levers for increasing HFC data capacity 52 7.3 DOCSIS 3.0 upgrades 53 7.4 DOCSIS 3.1 upgrades 64 7.5 Summary 69 Ref: 39065-174-B . -

Press Release

Press Release M7 GROUP CONTRACTS ADDITIONAL SES CAPACITY FOR HD BROADCASTING AT 23.5 DEGREES EAST FOR CZECH REPUBLIC AND SLOVAKIA Luxembourg, November 13, 2014 – SES S.A. (NYSE Euronext Paris and Luxembourg Stock Exchange: SESG) announced today that Luxembourg-based satellite television provider M7 Group has contracted additional capacity and extended an existing capacity contract at ASTRA 23.5 degrees East. M7 Group will be utilising the additional capacity to further expand the HD channel offering of Skylink, the M7-owned Direct-to-Home (DTH) television platform for the Czech Republic and Slovakia. Reaching over two million DTH homes, Skylink is the market-leading satellite television platform in these countries. “With the Czech and Slovak market now rapidly moving to HD viewing, it is critical to meet the growing consumer demand for HD content and thereby maintain our market-leading position. This new capacity agreement with SES will enable us to do so,” said Jaromir Glisnik, Member of the Board of M7 Group. “We are pleased to be able to support M7’s plans to grow its audiences, and remain committed to help them do so on a pan-European level,” said Norbert Hoelzle, Senior Vice President of Europe, Commercial at SES. For further information please contact: Markus Payer Corporate Communications Tel : +352 710 725 500 [email protected] Follow us on: Twitter: https://twitter.com/SES_Satellites LinkedIn: http://www.linkedin.com/company/ses Facebook: https://www.facebook.com/SES.YourSatelliteCompany YouTube: http://www.youtube.com/SESVideoChannel Blog: http://www.ses.com/blog SES Pictures are available under: http://www.ses.com/4245221/library About M7 Group M7 Group SA, based in Luxembourg, is one of Europe’s fastest growing operators of satellite and IP-based TV platforms: Canal Digitaal and Online.nl in the Netherlands, TV Vlaanderen in Flanders and TéléSAT in French speaking Belgium, AustriaSat/HD Austria in Austria, Skylink for the Czech and Slovak market and AustriaSat Hungary for the Hungarian market. -

12/FINAL Working Party on Telecommunication And

Unclassified DSTI/ICCP/TISP(2005)12/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development 07-Apr-2006 ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP/TISP(2005)12/FINAL Working Party on Telecommunication and Information Services Policies MULTIPLE PLAY: PRICING AND POLICY TRENDS English - Or. English JT03207142 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI/ICCP/TISP(2005)12/FINAL FOREWORD This report was presented to the Working Party on Telecommunication and Information Services Policies in December 2005 and was declassified by the Committee for Information, Computer and Communications Policy in March 2006. The report was prepared by Mr. Yoshikazu Okamoto and Mr. Taylor Reynolds of the OECD’s Directorate for Science, Technology and Industry. It is published under the responsibility of the Secretary- General of the OECD. © OECD/OCDE 2006 2 DSTI/ICCP/TISP(2005)12/FINAL TABLE OF CONTENTS MAIN POINTS.............................................................................................................................................. 6 Regulatory issues........................................................................................................................................ 7 INTRODUCTION -

Condensed Combined Financial Statements March 31, 2021 THE

Condensed Combined Financial Statements March 31, 2021 THE VIRGIN MEDIA GROUP 1550 Wewatta Street, Suite 1000 Denver, Colorado 80202 United States THE VIRGIN MEDIA GROUP TABLE OF CONTENTS Page Number FINANCIAL STATEMENTS Condensed Combined Balance Sheets as of March 31, 2021 and December 31, 2020 (unaudited)............................. 1 Condensed Combined Statements of Operations for the Three Months Ended March 31, 2021 and 2020 (unaudited).................................................................................................................................................................. 3 Condensed Combined Statements of Comprehensive Earnings for the Three Months Ended March 31, 2021 and 2020 (unaudited)......................................................................................................................................................... 4 Condensed Combined Statements of Equity for the Three Months Ended March 31, 2021 and 2020 (unaudited)...... 5 Condensed Combined Statements of Cash Flows for the Three Months Ended March 31, 2021 and 2020 (unaudited).................................................................................................................................................................. 7 Notes to Condensed Combined Financial Statements (unaudited)................................................................................ 9 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.............................................................................................................................................................. -

Vodafone Group and Liberty Global Announce Intention to Appoint Two Senior Executives for Their Proposed Netherlands Joint Venture

Vodafone Group and Liberty Global announce intention to appoint two senior executives for their proposed Netherlands joint venture Jeroen Hoencamp to be appointed Chief Executive and Ritchy Drost to be appointed Chief Financial Officer upon completion of transaction Denver, Colorado and London, United Kingdom ‐ 19 July 2016: Vodafone Group Plc (LSE: VOD) and Liberty Global plc (NASDAQ: LBTYA, LBTYB and LBTYK) today announced their intention to appoint Jeroen Hoencamp as Chief Executive and Ritchy Drost as Chief Financial Officer of the two companies’ proposed 50‐50 joint venture business combining Vodafone Netherlands and Ziggo*. The merger is subject to approval by the relevant competition authorities. Jeroen Hoencamp is currently the Chief Executive of Vodafone UK. A Dutch citizen, he has led Vodafone’s UK business since September 2013 and was previously Chief Executive of Vodafone Ireland. Before that, he spent 12 years in a number of senior executive roles (including Sales Director and Enterprise Business Unit Director) with Vodafone Netherlands. Earlier in his career he worked in senior marketing and sales positions with Canon Southern Copy Machines, Inc. in the USA and Thorn EMI/Skala Home Electronics in The Netherlands. He is a former officer in the Royal Dutch Marine Corps. In anticipation of the joint venture closing, Vodafone Group also announced that Jeroen Hoencamp will assume the position of Chief Executive of Vodafone Netherlands, effective 1 September 2016. Ritchy Drost is currently Chief Financial Officer of Ziggo, a position he has held since September 2015. Over a 17‐year career with Liberty Global he has held a number of senior management positions including Chief Financial Officer, European Broadband Operations and Managing Director and Chief Financial Officer of UPC Netherlands, Liberty’s predecessor Dutch cable operation. -

TX-NR636 AV RECEIVER Advanced Manual

TX-NR636 AV RECEIVER Advanced Manual CONTENTS AM/FM Radio Receiving Function 2 Using Remote Controller for Playing Music Files 15 TV operation 42 Tuning into a Radio Station 2 About the Remote Controller 15 Blu-ray Disc player/DVD player/DVD recorder Presetting an AM/FM Radio Station 2 Remote Controller Buttons 15 operation 42 Using RDS (European, Australian and Asian models) 3 Icons Displayed during Playback 15 VCR/PVR operation 43 Playing Content from a USB Storage Device 4 Using the Listening Modes 16 Satellite receiver / Cable receiver operation 43 CD player operation 44 Listening to Internet Radio 5 Selecting Listening Mode 16 Cassette tape deck operation 44 About Internet Radio 5 Contents of Listening Modes 17 To operate CEC-compatible components 44 TuneIn 5 Checking the Input Format 19 Pandora®–Getting Started (U.S., Australia and Advanced Settings 20 Advanced Speaker Connection 45 New Zealand only) 6 How to Set 20 Bi-Amping 45 SiriusXM Internet Radio (North American only) 7 1.Input/Output Assign 21 Connecting and Operating Onkyo RI Components 46 Slacker Personal Radio (North American only) 8 2.Speaker Setup 24 About RI Function 46 Registering Other Internet Radios 9 3.Audio Adjust 28 RI Connection and Setting 46 DLNA Music Streaming 11 4.Source Setup 29 iPod/iPhone Operation 47 About DLNA 11 5.Listening Mode Preset 32 Firmware Update 48 Configuring the Windows Media® Player 11 6.Miscellaneous 32 About Firmware Update 48 DLNA Playback 11 7.Hardware Setup 33 Updating the Firmware via Network 48 Controlling Remote Playback from a PC 12 8.Remote Controller Setup 39 Updating the Firmware via USB 49 9.Lock Setup 39 Music Streaming from a Shared Folder 13 Troubleshooting 51 Operating Other Components Using Remote About Shared Folder 13 Reference Information 57 Setting PC 13 Controller 40 Playing from a Shared Folder 13 Functions of REMOTE MODE Buttons 40 Programming Remote Control Codes 40 En AM/FM Radio Receiving Function Tuning into stations manually 2. -

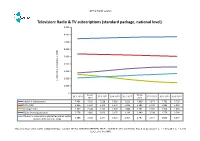

Television: Radio & TV Subscriptions (Standard Package, National Level) 9.000

OPTA Public version Television: Radio & TV subscriptions (standard package, national level) 9.000 8.000 7.000 6.000 5.000 4.000 3.000 2.000 number of subscriptionsof number x 1,000 1.000 0 31-12- 31-12- 30-9-2010 31-3-2011 30-6-2011 30-9-2011 31-3-2012 30-6-2012 30-9-2012 2010 2011 Total RTV subscriptions 7.454 7.500 7.538 7.590 7.623 7.669 7.677 7.702 7.730 Total cable 5.366 5.334 5.291 5.271 5.226 5.182 5.129 5.083 5.033 Analogue cable 2.587 2.448 2.265 2.095 1.888 1.741 1.592 1.504 1.434 Digital (+ analogue) cable 2.778 2.886 3.026 3.176 3.338 3.440 3.538 3.579 3.599 Other RTV subscriptions (digital terrestrial, digital 2.088 2.166 2.247 2.319 2.397 2.487 2.547 2.620 2.697 satellite, IPTV over DSL, FttH) Based on figures from CAIW, CANALDIGITAAL, COGAS, DELTA, KPN, REGGEFIBER, TELE2, T-MOBILE, UPC and ZIGGO. Based on questions 5_A_1_1 through 5_A_1_5 and 5_A_1_8 of the SMM. OPTA Public version Television: Churn based on radio & TV subscriptions (standard package, national level) 5% 4% 3% 2% % of number%of subscriptions 1% 0% 30-9-2010 31-12-2010 31-3-2011 30-6-2011 30-9-2011 31-12-2011 31-3-2012 30-6-2012 30-9-2012 Adds 3,1% 3,2% 3,1% 3,0% 3,3% 3,9% 3,8% 3,3% 3,2% Disconnects 2,7% 2,5% 2,8% 2,7% 2,9% 3,3% 3,4% 3,1% 3,0% Based on figures from CAIW, CANALDIGITAAL, COGAS, DELTA, KPN, REGGEFIBER, TELE2, UPC and ZIGGO.