A N N U a L R E P O R T 2 0

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Broadband Services and Local Loop Unbundling in the Netherlands Nico Van Eijk, Institute for Information Law

Broadband Services and Local Loop Unbundling in the Netherlands Nico van Eijk, Institute for Information Law This article describes the availability of broadband services in the ABSTRACT Netherlands. This particularly concerns broadband services for the consumer/end user such as access to the Internet. We will first discuss the new telecommunications act before dealing with current market relations and regulation of the (until 15 December 2000). This means telecommunications sector. This is followed by a description of the most significant deci- that — in accordance with the Euro- sions of the independent supervisory body, the Independent Post and Telecommunications pean directives — KPN has special obli- Authority, as related to broadband services. gations concerning interconnection and other forms of special access to its net- work. KPN is also responsible for pro- viding universal service (primarily he Netherlands has always been keen to take the traditional voice telephony service). On the expiration of the T lead in liberalizing the telecommunications sector. statutorily prescribed period of two years, whether KPN is still Nevertheless, it was not until the end of 1998 that Dutch leg- in the same position will again need to be established. It is islation satisfied all the underlying principles of European implicitly assumed that the operators of broadcasting networks telecommunications regulations. (the legal term for cable television networks) have significant This does not diminish the fact that, in the previous peri- market power regarding the transmission of programming. od, important liberalizations had occurred. In 1996–1997 all The market position of KPN is thus also at issue in regard to restrictions to offering telecommunications services — with the question of whether local differences in rates for public voice the exception of voice telephony — were discontinued. -

Internal Memorandum

Non-confidential version text which has been removed from the confidential version is marked [business secrets] or [XXX] as the case may be Case handlers: Tormod S. Johansen, Brussels, 11 July 2007 Runa Monstad Tel: (+32)(0)2 286 1841/1842 Case No: 13114 e-mail: [email protected] Event No: 436086 By fax (+47 22 83 07 95) and courier Viasat AS Care of: BA-HR Advokatfirma Att: Mr. Helge Stemshaug Postboks 1524 Vika N-0117 Oslo Norway Dear Mr. Stemshaug, Case COM 13114 (former case COM 020.0173) - Viasat/TV2/Canal Digital Norge (please quote this reference in all correspondence) I refer to the application of Viasat AS dated 30 July 2001, pursuant to Article 3 of Chapter II of Protocol 41 to the Agreement between the EFTA States on the Establishment of a Surveillance Authority and a Court of Justice (hereinafter “Surveillance and Court Agreement”), regarding alleged infringements of Articles 53 and 54 of the Agreement on the European Economic Area (hereinafter “EEA Agreement” or “EEA”) by TV2 Gruppen AS and Canal Digital Norge AS. By this letter I inform you that, pursuant to Article 7(1) of Chapter III of Protocol 4 to the Surveillance and Court Agreement,2 the Authority considers that, for the reasons set out below and on the basis of the information in its possession, there are insufficient grounds for acting on your complaint. 1 As applicable before the entry into force of the Agreement amending Protocol 4 of 24 September 2004 (e.i.f. 20.5.2005). 2 As applicable after the entry into force of the Agreement amending Protocol 4 of 3 December 2004 (e.i.f. -

12/FINAL Working Party on Telecommunication And

Unclassified DSTI/ICCP/TISP(2005)12/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development 07-Apr-2006 ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP/TISP(2005)12/FINAL Working Party on Telecommunication and Information Services Policies MULTIPLE PLAY: PRICING AND POLICY TRENDS English - Or. English JT03207142 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI/ICCP/TISP(2005)12/FINAL FOREWORD This report was presented to the Working Party on Telecommunication and Information Services Policies in December 2005 and was declassified by the Committee for Information, Computer and Communications Policy in March 2006. The report was prepared by Mr. Yoshikazu Okamoto and Mr. Taylor Reynolds of the OECD’s Directorate for Science, Technology and Industry. It is published under the responsibility of the Secretary- General of the OECD. © OECD/OCDE 2006 2 DSTI/ICCP/TISP(2005)12/FINAL TABLE OF CONTENTS MAIN POINTS.............................................................................................................................................. 6 Regulatory issues........................................................................................................................................ 7 INTRODUCTION -

NGN in the Netherlands: the Market and Regulation Geneva, 8 September 2008

NGN in The Netherlands: the market and regulation Geneva, 8 September 2008 Jilles van den Beukel Chief Regulatory Officer KPN +31653420780 [email protected] Business case of NGN is not proven yet; Legacy regulation has high impact on business case It should not be automatically extended to NGN 2 Market developments 3 Dynamic market situation 18% Mobile-only households 75% Broadband penetration High VoIP penetration The Netherlands is ‘competition champion’ of Europe Existing operators are consolidating On top of existing service providers, Fibre to the home operators are emerging new entrants with other business models Amsterdam 4 Marketshares The NL TV Internet Voice Cable Cable Cable VOIP Kabel 83% 40% 19% 6% 0% 44% 16% 60% ADSL DVB-T IP TV VOIP POTS KPN Internet 11% 16% 5% Other TV Other Internet Other VOIP Other (a.o. satellite) (ADSL) (DSL-Providers) Market Shares Consumer Market in % (indicative/management estimates) 5 Tariffs in the Multiplay market Telfort Casema UPC € 19,95 € 69,95 € 60,00 tot 20 Mb/s 20 Mb/s 24 Mb/s € 9,95 voice incl Voice include voice Tele2 Compleet Tele2 Compleet BelGratisAltijd Internetsnelheid Tot 20Mb/s Tot 20Mb/s Bellen Bellen tegen voordelige Tele2 tarieven. GRATIS naar vaste nummers in Nederland Actie € 14,95 p/mnd € 24,95 p/mnd eerste 6 maanden Abonnement € 29,95 p/mnd € 39,95 p/mnd 6 Next steps: FttC and FttH? 7 Change of mindshift KPN • Market developments: – High churn to cable; – Television is crucial for Multiplay; – IP-technology Lead to Upgrade of the network: Business Model: – VDSL -

The Effects of the Cord-Cutting Counterpublic

Utrecht University The Effects of The Cord-Cutting Counterpublic How the Dynamics of Resistance and Resilience between the Cord-Cutters and the Television Distribution Industry Are Redefining Television Eleonora Maria Mazzoli Academic Year 2014-2015 Page intentionally left blank Utrecht University The Effects of the Cord-Cutting Counterpublic How the Dynamics of Resistance and Resilience between the Cord-Cutters and the Television Distribution Industry Are Redefining Television Master Thesis Eleonora Maria Mazzoli 4087186 RMA Media and Performance Studies Words: 37600 Supervisor: Prof. Dr. William Uricchio Second Reader: Prof. Dr. Eggo Müller Academic Year: 2014-2015 Cover picture by TechgenMag.com © 2015 by Eleonora Maria Mazzoli All rights reserved Page intentionally left blank To my parents, Donatella and Piergiovanni, and to my little sister, Elena “La televisiun, la g'ha na forsa de leun; la televisiun, la g'ha paura de nisun.” “Television is as strong as a lion; Television fears nobody.” Enzo Jannacci. La Televisiun.1975. Page intentionally left blank Table of Content Abstract 1 Preface: Television as A Cross-Media Techno-Cultural Form 2 1. Introduction - Cord-Cutting 101: A Revolution Has Begun 5 1.1. Changing Habits in a Changing Ecosystem 5 1.2. The Question of the Cord-Cutting Counterpublic 8 1.3. Methodology: Sources, Approach and Structure 11 1.4. Relevance 15 2. The Cutters within a Cross-Media Television Ecosystem 17 2.1. Re-working of the U.S. Television Distribution Platforms 18 2.2. Legitimating Newfound Watching Behaviours 23 2.3. Proactive Viewers, Cord-Killers, Digital Pirates: Here Come the Cord-Cutters 25 3. -

Liberty Global Plc Nasdaq: LBTYA, LBTYB, LBTYK

September 16, 2014 Volume XL, Issue VII & VIII Liberty Global plc Nasdaq: LBTYA, LBTYB, LBTYK Dow Jones Indus: 17,131.97 S&P 500: 1,998.98 Russell 2000: 1,150.97 Trigger: No Index Component: NA Type of Situation: Business Value, Consumer Franchise Price (LBTYK): $ 41.98 Shares Outstanding (MM): 779 Fully Diluted (MM) (% Increase): 829 (6%) Average Daily Volume (MM): 3.4 Market Cap (MM): $ 33,063 Enterprise Value (MM): $ 74,513 Percentage Closely Held: John Malone 3% econ., 28% voting 52-Week High/Low: $ 45.98/38.27 Trailing Twelve Months Price/Earnings: NM Price/Stated Book Value: 2.9x Long-Term Debt (MM): $ 40,739 Introduction Implied Upside to Estimate of Liberty Global plc (“Liberty Global,” “Liberty,” Intrinsic Value: 37% “LGI” or the “Company”) is the largest international Dividend: NA operator of cable systems with 24.5 million unique Payout NA customers. Under the direction of cable pioneer John Malone, Liberty Global has grown from a holding Yield NA company with investments in independent global cable Net Revenue Per Share: and programming at the time of its separation from TTM $ 19.36 Liberty Media in 2004 into the largest operator of cable 2013 $ NA systems in Europe. This has been accomplished 2012 $ NA through several reasonably-priced acquisitions that 2011 $ NA produced increasingly large synergies through network co-location, sales/marketing and central office sharing, Earnings Per Share: and capex savings, among other benefits. TTM $ NA Today, Liberty is the #1 operator in 9 of the 12 2013 $ NA countries or territories it operates in and has invested 2012 $ NA heavily to maintain best in class broadband network 2011 $ NA speeds and advanced video offerings. -

Unclassified DSTI/ICCP/CISP(2009)9/FINAL

Unclassified DSTI/ICCP/CISP(2009)9/FINAL Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 23-Mar-2010 ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP/CISP(2009)9/FINAL Working Party on Communication Infrastructures and Services Policy DEVELOPMENTS IN CABLE BROADBAND NETWORKS English - Or. English JT03280592 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI\ICCP\CISP(2009)9/FINAL FOREWORD The Working Party on Communication Infrastructures and Services Policy (CISP) discussed this report at its meeting in December 2009. CISP agreed to forward the document for declassification by the Committee for Information, Computer and Communications Policy (ICCP). The ICCP Committee agreed to make the report public in March 2010. The report was prepared by Mr. Hyun-Cheol CHUNG of the OECD’s Directorate for Science, Technology and Industry. It is published under the responsibility of the Secretary-General of the OECD. © OECD 2010/OCDE 2010 2 DSTI\ICCP\CISP(2009)9/FINAL MAIN FINDINGS The position of cable operators within the pay TV market has changed drastically in recent years. Although video service remains core to the cable industry’s business model, cable TV’s market share has been dropping significantly with intense competition from direct broadcast satellite services (DBS), Internet protocol Television (IPTV) services, digital terrestrial television services (DTT) and finally from over-the-top (OTT) service providers that supply video over an existing data connection from a third party. -

Providence Equity Partners and the Carlyle Group Sell Casema to Cinven and Warburg Pincus for €2.1 Billion

Providence Equity Partners and The Carlyle Group sell Casema to Cinven and Warburg Pincus for €2.1 Billion Paris, London and The Hague, July 18, 2006 – The Carlyle Group, Providence Equity Partners and GMT Communications Partners (the “Sponsors”) today announced that they have signed a definitive agreement with Cinven and Warburg Pincus under which Cinven and Warburg Pincus will acquire Casema for €2.1 billion. Casema is a leading provider of cable, Internet and telephony services to residential and business customers in the Netherlands. The Company is the third largest cable operator in the country, passing 1.5 million homes. The Company’s current customer base represents approximately 21% of all Dutch households. The Sponsors acquired Casema in January 2003 from France Telecom, with Providence and Carlyle each owning 46% of the Company and GMT 8%. Under the ownership of the Sponsors and management of Chief Executive Officer Jos Molenkamp who joined shortly after the acquisition, Casema invested in excess of €250 million in its network and infrastructure. The Company has been transformed from a utility-like analog television provider into the leading “triple play” operator in the Netherlands, offering digital television, broadband internet and telephony to the Dutch consumers. As of June 30, 2006, the Company had 1.3 million television subscribers (of which 112,000 subscribed to digital packages), 400,000 broadband internet and 136,000 telephony subscribers. Additionally, Casema has achieved revenue growth of 10% annually since 2002 and approximately doubled EBITDA, while increasing its headcount to approximately 1,050 from 750 employees at the end of 2002. -

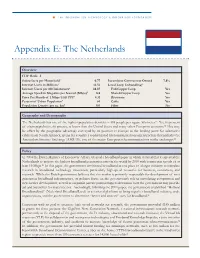

Appendix E: the Netherlands

THE INFORMATION TECHNOLOGY & INNOVATION FOUNDATION Appendix E: The Netherlands Overview ITIF Rank: 4 Subscribers per Household1 0.77 Incumbent Government Owned 7.8% Internet Users in Millions2 14.54 Local Loop Unbundling:3 Internet Users per 100 Inhabitants4 88.87 Full Copper Loop Yes Average Speed in Megabits per Second (Mbps)5 8.8 Shared Copper Loop Yes Price Per Month of 1 Mbps USD PPP6 4.31 Bitstream Yes Percent of Urban Population7 66 Cable Yes Population Density per sq. km8 393 Fiber No Geography and Demography The Netherlands has one of the highest population densities – 393 people per square kilometer.9 Yet, its percent of urban population, 66 percent, is lower than the United States and many other European countries.10 This may be offset by the geographic advantage conveyed by its position in Europe as the landing point for submarine cables from North America, giving the country a sophisticated telecommunications infrastructure that includes the Amsterdam Internet Exchange (AMS-IX), one of the major European telecommunications traffi c exchanges.11 Policy In 2004 the Dutch Ministry of Economic Affairs released a broadband paper in which it stated that it expected the Netherlands to achieve the highest broadband penetration rates in the world by 2010 with connection speeds of at least 10 Mbps.12 In this paper, the government envisioned broadband as one piece of a larger initiative to stimulate research in broadband technology innovation, particularly high-speed networks for business, consumers, and research. While the Dutch government believes that the market is primarily responsible for development of next generation broadband infrastructure, its policies focus on the government’s role in stimulating competition and new service development, as well as on public-private partnerships to determine how the government may provide aid and incentives for social sectors. -

Understanding the Dynamics of Broadband Markets a Comparative

Understanding the Dynamics of Broadband Markets A comparative case study of Flanders and the Netherlands Marlies Van der Wee(1), Sofie Verbrugge(1), Wolter Lemstra(2) Ghent University - IBBT University of Technology Delft Research Group Broadband Communication Section Economics of Infrastructures Networks (IBCN) Department Technology, Policy and Department of Information Technology Management (INTEC) Jaffalaan 5 Gaston Crommenlaan 8 bus 201, NL-2628 BX Delft B-9050 Gent, Belgium The Netherlands Phone: +32 9 33 14 900 Phone: +31152782695 Fax: +32 9 33 14 899 Fax: +31152787925 Abstract The Digital Agenda for Europe sets out clear goals for providing high speed broadband to all its residents, but leaves the implementation of this plan to the individual Member States. Because of large economic, cultural and political differences, the roads to realizing these ambitious goals are varying in between these Member States. This paper investigates the dynamics of fixed broadband markets in two neighboring regions: Flanders, the northern part of Belgium, and the Netherlands. The historical developments in telecom markets in both regions are highly similar and resulted in both areas in a duopoly between the incumbent, operating DSL on the former telephone network, and one or more cable operators, using the DOCSIS technology to offer broadband on the former analogue television network. However, in the race towards realizing the Digital Agenda goals, it comes down to the small differences in between both regions: the existence of housing organizations in the Netherlands has led to quite some Fiber- to-the-Home deployment, whereas in Flanders, the traditional operators use evolutionary upgrades of both DSL and DOCSIS to realize the European targets. -

Fixed Broadband Deployment in the Netherlands: Success and Failure in Policy and Technology Or the Paradox of Successful Competition Van Eijk, N.; Doorenspleet, H

UvA-DARE (Digital Academic Repository) Fixed Broadband deployment in the Netherlands: Success and failure in policy and technology or the paradox of successful competition van Eijk, N.; Doorenspleet, H. Publication date 2014 Document Version Submitted manuscript Published in 25th European Regional Conference of the International Telecommunications Society (ITS), Brussels, Belgium, 22-25 June 2014 Link to publication Citation for published version (APA): van Eijk, N., & Doorenspleet, H. (2014). Fixed Broadband deployment in the Netherlands: Success and failure in policy and technology or the paradox of successful competition. In 25th European Regional Conference of the International Telecommunications Society (ITS), Brussels, Belgium, 22-25 June 2014 (pp. 101372). EconPapers. http://EconPapers.repec.org/RePEc:zbw:itse14:101372 General rights It is not permitted to download or to forward/distribute the text or part of it without the consent of the author(s) and/or copyright holder(s), other than for strictly personal, individual use, unless the work is under an open content license (like Creative Commons). Disclaimer/Complaints regulations If you believe that digital publication of certain material infringes any of your rights or (privacy) interests, please let the Library know, stating your reasons. In case of a legitimate complaint, the Library will make the material inaccessible and/or remove it from the website. Please Ask the Library: https://uba.uva.nl/en/contact, or a letter to: Library of the University of Amsterdam, Secretariat, -

Broadband and Telephony Services Over Cable Television Networks”, OECD Digital Economy Papers, No

Please cite this paper as: OECD (2003-11-07), “Broadband and Telephony Services Over Cable Television Networks”, OECD Digital Economy Papers, No. 77, OECD Publishing, Paris. http://dx.doi.org/10.1787/232788646665 OECD Digital Economy Papers No. 77 Broadband and Telephony Services Over Cable Television Networks OECD Unclassified DSTI/ICCP/TISP(2003)1/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development 07-Nov-2003 ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP/TISP(2003)1/FINAL Working Party on Telecommunication and Information Services Policies BROADBAND AND TELEPHONY SERVICES OVER CABLE TELEVISION NETWORKS English - Or. English JT00153297 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI/ICCP/TISP(2003)1/FINAL FOREWORD In June 2003 this report was presented to the Working Party on Telecommunications and Information Services Policy (TISP) and was recommended to be made public by the Committee for Information, Computer and Communications Policy (ICCP). The report was prepared by Mr. Sam Paltridge of the OECD’s Directorate for Science, Technology and Industry. It is published on the responsibility of the Secretary-General of the OECD. Copyright OECD, 2003 Applications for permission to reproduce or