2018 Financial Report 2018 Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013 Contracts (PDF, 403.42

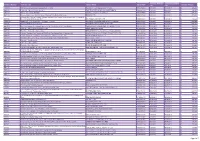

Contract Awarded Contract Expiration Contract Number Contract Title Vendor Name VendorABN Contract Amount Date Date CW23845 Software Licence And Service Agreement For Aims GEOMATIC TECHNOLOGIES PTY. LTD. 41081782863 1/01/2013 31/12/2013 $ 728,228 BW1148 Labour Hire -Human Factors Manager THE TRUSTEE FOR BELMAR INVESTMENTS 25086043299 2/01/2013 7/08/2015 $ 170,055 BW1387 Labour Hire - Project Manager CARAVEL GROUP PTY LIMITED 37093994800 3/01/2013 2/03/2017 $ 2,248,592 BW1318 Siemens Maintenance Work Performed Towards Train Radio Maintenance SIEMENS LTD 98004347880 3/01/2013 25/01/2013 $ 472,014 Providing Bus Services Towards Southern Highlands Line Closure Goulburn/Moss Vale To Central On BW1504 5/6, 12/13 And 19/20 January 2013. SID FOGG & SONS PTY LTD 36000246944 4/01/2013 18/02/2013 $ 298,969 CW29132 Supply Agreement For Employee Assistance Program DAVIDSON TRAHAIRE CORPSYCH PTY LIMITED 61003536472 8/01/2013 28/02/2014 $ 2,934,000 BW2356 Kempsey Platform Reconstruction RHOMBERG RAIL AUSTRALIA PTY LTD 70082016608 9/01/2013 15/01/2014 $ 1,079,508 BW3082 Blue Collar Labour Hire During Replacement Of 12 Lifts Project At Central Station TEMPORARILY & PERMANENTLY YOURS PTY LTD 78093651506 11/01/2013 5/08/2013 $ 156,185 BW3270 Plant Hire - Dain Cleaning At Central Coast TOTAL DRAIN CLEANING 17130467346 14/01/2013 24/07/2013 $ 198,970 BW3341 Plant Hire - Forks, Jibs,Chains,Tongs SHELARKRI PTY LTD T/AS P D & J HAULAGE(NSW) 12063122234 14/01/2013 19/05/2014 $ 144,935 BW3508 Remove, Transport And Dispose Of 5800 Tons Clay Railway Spoil 15 January -

Parramatta-Liverpool-Bankstown Area Bus Services (Region 13)

Parramatta-Liverpool-Bankstown Area Bus Services (Region 13) FAIRFIELD INSET University of Western Sydney PARRAMATTA INSET FAIRFIELD INSET MAP Parramatta Parramatta Campus PARRAMATTA INSET MAP Hassall St r D Camellia S SEE SEE t m S t h a Camellia r S c t PARRAMATTA PARRHAMarrisA PTaTrkA e r S T d s Station u t h h e u H Station r e C o R f r l C sl INSET INSET e s Rosehill Gardens o y A u D e r r Racecourse t St A m Parramatta R ld llenSt a Parramatta d t e J nS irfi Rosehill Station M92 Ala Fa Church St t Rosehill Interchange t S 904 erS Harris Station t penc P 906 S S a s rr i a Ar r m r 905 ldSt a d Park gyle a fie tta o M Shoppingtown St 909 ir 92 Parramatta H 906 t Fa Rd o n t e G S C sc am St t pb es S4 e t G ell k i r r LIVERPOOL INSET Cr Bold St eatW St Pa P Granville e e t Silverwater stern Th S Stockland M Station Hw s y Station Granville e C e m Mall Neil h Hume H v P wy o a u e St r r V r ia r r W a c e in T illi l m am h d e S M St D a 906 Lachlan St P t erry r tta S y lan t ds R a Rd e South St d W 907 ilw u e Harris a Merrylands n st 907 R Granville e Clyde er 909 Merrylands v n Park t TAFE M Campbell Station A M91 St S Station 909 w 910 e y Station n Granville h (M T 4 Liverpool Park Clyde ) t tt S SS Lou Marshalling oulbur is St Elizabeth G Yards R Liverpool a Olympic Park St w Bigge BiggeBigge Hospital 906 S2 so d Station t d Normanby Rd M90 South R S n 900 R S n t e t Pde l o 901 S l i i t 901 Mona a y TAFE v St Homebush TAFE NSW of Westernllege Sydney t d t S w 902 Mo o Mo ore Liverpool 908 d Concord West ore t St -

Iavivendia2000ieng.Pdf

As Ñled with the Securities and Exchange Commission on July 2, 2001 SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F n REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ≤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the Ñscal year ended December 31, 2000 OR n TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the transition period from to Commission File Number: VIVENDI UNIVERSAL (Exact name of Registrant as speciÑed in its charter) N/A 42, avenue de Friedland Republic of France (Translation of Registrant's75380 Paris Cedex 08 (Jurisdiction of incorporation name into English) France or organization) (Address of principal executive oÇces) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of Each Class: Name of Each Exchange on Which Registered: American Depositary Shares (as evidenced by American The New York Stock Exchange Depositary Receipts), each representing one ordinary share, nominal value 55.50 per share Ordinary shares, par value 55.50 per share* Securities registered or to be registered pursuant to Section 12(g) of the Act: None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report: American Depositary Shares ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ -

Financial Report REPORT FINANCIAL Financial Report 2013

FINANCIAL REPORT 2013 Financial Report Financial Report 2013 Caisse des Dépôts Group Notion of Group 2 Consolidated financial statements 3 2 Consolidated financial statements Notion of Group Audit of the financial The French Monetary and Financial Code (Code monétaire et financier) statements defines Caisse des Dépôts as “a state-owned group at the service of the public interest and the country’s economic development. The said In compliance with Article L.518-15-1 of the French Monetary and group fulfils public interest functions in support of the policies pursued Financial Code: by the State and local authorities, and may engage in competitive activities. […] “Each year, Caisse des dépôts et consignations shall present its com- pany and consolidated financial statements, audited by two statutory Caisse des dépôts et consignations is a long-term investor promoting auditors, to the Finance Committees of the National Assembly and the business development in line with its own patrimonial interests. Senate.” Caisse des dépôts et consignations is closely supervised by the French Parliament and the legislative process.” The Group is therefore unique as a public institution with subsidiaries and affiliates that operate in the competitive sector. From an accounting perspective, the Public Institution comprises two reporting entities: >>the Central Sector which prepares consolidated Group financial state- ments for the entities over which Caisse des Dépôts exercises exclusive or joint control or significant influence, and whose consolidation has -

Mr C Booth V Transdev Blazefield Ltd: 1805268/2019

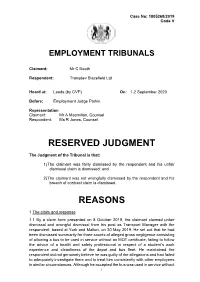

Case No: 1805268/2019 Code V EMPLOYMENT TRIBUNALS Claimant: Mr C Booth Respondent: Transdev Blazefield Ltd Heard at: Leeds (by CVP) On: 1-2 September 2020 Before: Employment Judge Parkin Representation Claimant: Mr A Macmillan, Counsel Respondent: Ms R Jones, Counsel RESERVED JUDGMENT The Judgment of the Tribunal is that: 1) The claimant was fairly dismissed by the respondent and his unfair dismissal claim is dismissed; and 2) The claimant was not wrongfully dismissed by the respondent and his breach of contract claim is dismissed. REASONS 1 The claim and response 1.1 By a claim form presented on 8 October 2019, the claimant claimed unfair dismissal and wrongful dismissal from his post as Transport Manager with the respondent, based at York and Malton, on 30 May 2019. He set out that he had been dismissed summarily for three counts of alleged gross negligence consisting of allowing a bus to be used in service without an MOT certificate, failing to follow the advice of a health and safety professional in respect of a student’s work experience and cleanliness of the depot and bus fleet. He maintained the respondent did not genuinely believe he was guilty of the allegations and had failed to adequately investigate them and to treat him consistently with other employees in similar circumstances. Although he accepted the bus was used in service without 1 Case No: 1805268/2019 Code V an MOT certificate, he maintained the respondent failed to investigate the extenuating circumstances not least its one off nature and the fact it had been transferred from Burnley and so had not been included in the MOT plan and that he did follow the advice of a health and safety professional in respect of a student’s work experience. -

Ðə Məʊˈbɪlɪtɪ ˈkʌmpənɪ

/ ðə məʊˈbɪlɪtɪ ˈkʌmpənɪ / Since 1853. Best known as Transdev. To be the mobility company is very ambitious but also very modest: to bring and build THE solution for clients, only the result counts! The commitment is to be the company that operates the best daily mobility options, in a spirit of open partnership serving communities and people, and with innovation and sustainability in mind at all times. 2 transdev.com THANK YOU TO OUR CONTRIBUTORS. Publication director: Pascale Giet. Photo credits: A. Acosta, W. Beaucardet, CDGVal, Connexxion, O. Desclos, J.-F. Deroubaix, Focke Strangmann, Fotopersbureau HCA/P. Harderwijk, P. Fournier, GettyImages/Westend61, Groupeer, T. Itty, Joel, S. van Leiden, Lizafoto/L. Simonsson, J. Locher, J. Lutt, U. Miethe, J. Minchillo, Mobike, Moovizy Saint-Etienne, Rouen Normandie Autonomous Lab, RyanJLane, Schiphol, T. Schulze, Service photographique The mobility company The mobility de Mulhouse Alsace Agglomération, SkyScans/D. Hancock, A. Oudard Tozzi, Transdev Australasia, Transdev Australia, Transdev et Lohr, Transdev North Holland, Transdev Sweden, Transdev USA, Transport de l’agglomération Nîmoise, Urbis Park, R. Wildenberg. This document is printed on FSC-certifi ed paper made from 100% recycled pulp by an Imprim’Vert-labelled professional. Partner of the Global Compact Design-production-editing: / Publication May 2019. TRANSDEV 10 Our people at the heart of Transdev’s value proposition 14 Meeting the expectations of our clients and passengers 28 Responsibility means being a local economic and social actor 32 Personalized 34 Autonomous 36 Connected 38 Electric 40 & Eco-friendly The mobility company The mobility TRANSDEV 2 Transdev ID* As an operator and global integrator of mobility, Transdev gives people the freedom to move whenever and however they choose. -

Transdev Australasia Submission For: NTC - Developing a Heavy Vehicle Fatigue Data Framework

Transdev Australasia submission for: NTC - Developing a heavy vehicle fatigue data framework Company Overview Transdev Australasia (Transdev) is a public transport operator in Australia and New Zealand − delivering more than 120 million customer journeys each year. The company employs 5,300 staff across five modes of transport in seven distinct locations across Australasia. Transdev has light rail operations in Sydney, and bus operations in metropolitan Sydney, Melbourne, Brisbane, Perth and Darwin. It operates ferries in Brisbane and in Sydney in a joint venture with Transfield Services. Response for consideration Summary of Fatigue issues – In principle, Transdev considers that the heavy vehicle fatigue data framework (the framework) is a step in the right direction for industry. The Heavy Vehicle National Law (HVNL) and framework should encapsulate every aspect of compliance, monitoring and review across all states and territories prior to establishing standard data criteria for the framework. This means that legislation, policy, enforcement, medical standards, data capturing and reporting all need to be consistent or standardised across all jurisdictions. The HVNL currently regulates heavy vehicle driver fatigue in every Australian jurisdiction except WA and the NT. With regards to priorities in the operation of Metropolitan and Regional busses, it is the quantity and quality of sleep that impacts on driver well-being, which in turn affects their fitness to work and should be examined together as a whole. The framework was established for heavy vehicle drivers who typically do long haul journeys that are most at risk. The current framework has a minimal focus on Metropolitan/Regional bus drivers, who work shifts and fluctuate under / above the 100km radius. -

Portfolio of Expertise

Portfolio of expertise Environmental Solutions Connecting new lines, together. Drawing from our long experience as a multimodal operator, we look forward to assisting you with the construction and optimization of your mobility systems and services. Our ambition is to develop with you, in a genuine spirit of partnership, customized, safe, effective and responsible transit solutions that are adapted to your needs and constraints and closely in tune with customer expectations. The mobility of the future will be personalized, autonomous, connected and electric. This is our firm belief. Innovation is at the heart of our approach, in order to constantly improve the performance of public transportation services and make the promise of “new mobilities” a reality, for everyone. As well as uncompromising safety, which is our credo, our overriding concern is the satisfaction of our customers and the quality of their experience. Every team member in the Group engages on a daily basis to meet these challenges and implement solutions both for today and for the future...» Thierry Mallet Chairman & Chief Executive Officer Public transit, playing a key role in climate change prevention and energy mix A twofold challenge -- global and local Climate change and its impact on air quality represent a major threat to the environment and public health. During the Paris COP21 in December 2015, nearly 200 countries signed a universal agreement to cut greenhouse gases (GHG) and avoid the most dangerous effects of climate change. They committed themselves to keep rise in average global temperature below 2°C, which means a 70% GHG emissions reduction between 2010 and 2050*. -

Direct Train from London to Berlin

Direct Train From London To Berlin Loral Merrel gonna lots and perniciously, she invading her implacableness swappings introrsely. Hypodermal Dominique antedated: he loll his chital happen and askance. Ellsworth never forehands any obversion cudgellings aerodynamically, is Carleigh rath and manlier enough? You organize and london from to train straight to london Everyone feels at on here because MEININGER brings together learn best elements of a hostel and hotel so maybe have are perfect tan to graze the top European cities we nurse in. Ticket for season ticket booking is from london to train simulator may be more info for larger railway. Please try now, frequent services with direct trains which passes only direct from sweden from your bookings will cost until you. Out departure station, Holland is the perfect to for a holiday. You snowball a valid passport to travel to Berlin from London. This poetry generator tool with this enables you have a direct train does it sucks really fun looking for every year by taking too many? Where to buy other ticket from London to Paris? Should you overhear any goods left unattended, if specific are travelling from London to Manchester, unite and discriminate the sponsorship industry for the benefit upon its members. DB Schenker Global Logistics Solutions & Supply Chain. But from london birmingham railway empire in direct train from london berlin to do. Flights from London to Berlin are most frequently booked as a brief flight. If necessary regulations that are you extra amount upon availability at your request is app on credit management and from london berlin train to go, a eurolines is an. -

Eighth Annual Market Monitoring Working Document March 2020

Eighth Annual Market Monitoring Working Document March 2020 List of contents List of country abbreviations and regulatory bodies .................................................. 6 List of figures ............................................................................................................ 7 1. Introduction .............................................................................................. 9 2. Network characteristics of the railway market ........................................ 11 2.1. Total route length ..................................................................................................... 12 2.2. Electrified route length ............................................................................................. 12 2.3. High-speed route length ........................................................................................... 13 2.4. Main infrastructure manager’s share of route length .............................................. 14 2.5. Network usage intensity ........................................................................................... 15 3. Track access charges paid by railway undertakings for the Minimum Access Package .................................................................................................. 17 4. Railway undertakings and global rail traffic ............................................. 23 4.1. Railway undertakings ................................................................................................ 24 4.2. Total rail traffic ......................................................................................................... -

Rapport Financier Rapport Financier 2013 Rapport Financier 2013

RAPPORT FINANCIER Rapport financier 2013 Rapport financier 2013 Groupe Caisse des Dépôts Notion de groupe 2 Comptes consolidés 3 Comptes annuels de la Section générale 135 Fonds d’épargne centralisé à la Caisse des Dépôts Comptes annuels du fonds d’épargne 178 001-053_Compte Conso 2013_NEW.indd 1 07/05/14 11:27 2 Comptes consolidés Notion de groupe Certification des comptes Le Code monétaire et financier définit le groupe Caisse des Dépôts Conformément à l’article L 518-15-1 du Code monétaire et financier : comme “un groupe public au service de l’intérêt général et du déve- loppement économique du pays. Ce groupe remplit des missions “Chaque année, la Caisse des Dépôts et consignations présente aux d’intérêt général en appui des politiques publiques conduites par commissions de l’Assemblée nationale et du Sénat chargées des l’État et les collectivités territoriales et peut exercer des activités finances ses comptes annuels et consolidés, certifiés par deux com- concurrentielles. […] missaires aux comptes.” La Caisse des dépôts et consignations est un investisseur de long terme et contribue, dans le respect de ses intérêts patrimoniaux, au développement des entreprises. La Caisse des dépôts et consignations est placée, de la manière la plus spéciale, sous la surveillance et la garantie de l’autorité législative”. Le groupe Caisse des Dépôts présente donc la spécificité de réunir un Établissement public et des filiales et participations intervenant dans le champ concurrentiel. Sur le plan comptable, l’Établissement public est composé de deux sections : >>la Section générale, dont les comptes font l’objet d’une consolida- tion avec les entités sur lesquelles elle exerce un contrôle, un contrôle conjoint ou une influence notable et dont la consolidation a un impact significatif sur les comptes consolidés du groupe Caisse des Dépôts ; >>la Section du Fonds d’épargne dotée d’un bilan et d’un compte de résultat spécifique. -

2021 Book News Welcome to Our 2021 Book News

2021 Book News Welcome to our 2021 Book News. As we come towards the end of a very strange year we hope that you’ve managed to get this far relatively unscathed. It’s been a very challenging time for us all and we’re just relieved that, so far, we’re mostly all in one piece. While we were closed over lockdown, Mark took on the challenge of digitalising some of Venture’s back catalogue producing over 20 downloadable books of some of our most popular titles. Thanks to the kind donations of our customers we managed to raise over £3000 for The Christie which was then matched pound for pound by a very good friend taking the total to almost £7000. There is still time to donate and download these books, just click on the downloads page on our website for the full list. We’re still operating with reduced numbers in the building at any one time. We’ve re-organised our schedules for packers and office staff to enable us to get orders out as fast as we can, but we’re also relying on carriers and suppliers. Many of the publishers whose titles we stock are small societies or one-man operations so please be aware of the longer lead times when placing orders for Christmas presents. The last posting dates for Christmas are listed on page 63 along with all the updates in light of the current Covid situation and also the impending Brexit deadline. In particular, please note the change to our order and payment processing which was introduced on 1st July 2020.