Build King Holdings Limited Build King

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

EVS Customer Notice

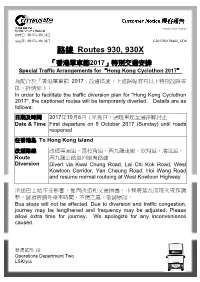

*C201702176a02* 發佈日: 2017年10月3日 張貼至: 2017年10月8日 C201702176a02_ODII 路線 Routes 930, 930X 「香港單車節2017」特別交通安排 Special Traffic Arrangements for“Hong Kong Cyclothon 2017” 為配合於「香港單車節 2017」改道措施,上述路線將有以下特別改路安 排,詳情如下: In order to facilitate the traffic diversion plan for “Hong Kong Cyclothon 2017”, the captioned routes will be temporarily diverted. Details are as follows: 日期及時間 2017年10月8日(星期日)頭班車起至道路解封止 Date & Time First departure on 8 October 2017 (Sunday) until roads reopened 往香港島 To Hong Kong Island 改道路線 改經葵涌道、荔枝角道、西九龍走廊、欣翔道、海泓道、 Route 西九龍公路返回原有路線 Diversion Divert via Kwai Chung Road, Lai Chi Kok Road, West Kowloon Corridor, Yan Cheung Road, Hoi Wang Road and resume normal routeing at West Kowloon Highway 沿途巴士站不受影響,惟因改道和交通擠塞,車程將延長而班次或作調 整,請預留額外乘車時間,不便之處,敬請原諒。 Bus stops will not be affected. Due to diversion and traffic congestion, journey may be lengthened and frequency may be adjusted. Please allow extra time for journey. We apologize for any inconvenience caused. 營運貳部 啟 Operations Department Two LSK/ycc *C201702177a02* 發佈日: 2017年10月3日 張貼至: 2017年10月8日 C201702177a02_ODII 路線 Routes 962B, 962X, 967, 969, N962, N969 「香港單車節2017」特別交通安排 Special Traffic Arrangements for“Hong Kong Cyclothon 2017” 為配合於「香港單車節 2017」改道措施,上述路線將有以下特別改路安排,詳情如下: In order to facilitate the traffic diversion plan for “Hong Kong Cyclothon 2017”, the captioned routes will be temporarily diverted. Details are as follows: 日期及時間 2017年10月8日(星期日)頭班車起至道路解封止 Date & Time First departure on 8 October 2017 (Sunday) until roads reopened 往香港島 To Hong Kong Island 改道路線 改經屯門公路、荃灣路、葵涌道、荔枝角道、西九龍走廊、欣翔道、 Route 海泓道、西九龍公路返回原有路線 Diversion Divert via Tuen Mun Road, Tsuen Wan Road, Kwai Chung Road, Lai Chi Kok Road, West Kowloon Corridor, Yan Cheung Road, Hoi Wang Road and resume normal routeing at West Kowloon Highway 沿途巴士站不受影響,惟因改道和交通擠塞,車程將延長而班次或作調整,請預留 額外乘車時間,不便之處,敬請原諒。 Bus stops will not be affected. -

1. the Meeting Was Resumed at 9:15 A.M. on 26.10.2016. 2. The

1. The meeting was resumed at 9:15 a.m. on 26.10.2016. 2. The following Members and the Secretary were present at the resumed meeting: Permanent Secretary for Development Chairman (Planning and Lands) Mr Michael W.L. Wong Professor S.C. Wong Vice-Chairman Mr Lincoln L.H. Huang Mr Ivan C.S. Fu Mr Sunny L.K. Ho Mr Dominic K.K. Lam Dr F.C. Chan Mr David Y.T. Lui Mr Peter K.T. Yuen Mr Wilson Y.W. Fung Mr Alex T.H. Lai Professor T.S. Liu Ms Sandy H.Y. Wong Mr Franklin Yu Chief Traffic Engineer (New Territories West) Transport Department Mr Samson S.S. Lam Principal Environmental Protection Officer (Regional Assessment) Environmental Protection Department Mr Louis P.L. Chan Assistant Director/Regional 3, Lands Department Mr Edwin W.K. Chan - 2 - Agenda Item 1 (Continued) [Open Meeting (Presentation and Question Sessions only)] Presentation and Question Sessions (Continued) 3. The Chairman said that the meeting was a continuation of the hearing of the representations and comments in respect of the draft Tsing Yi Outline Zoning Plan (Tsing Yi OZP) No. S/TY/27 commenced on 25.10.2016. 4. The Secretary said that Members’ declaration of interests as shown on the PowerPoint were reported on the first hearing session on 25.10.2016 (Paragraphs 4 and 5 of the minutes of 25.10.2016). No further declaration of interests had been received from Members since then. 5. The following government’s representatives, further representers, representers, commenters and their representatives were invited to the meeting at this point: Government representatives Planning Department (PlanD) Mr Lawrence Y.C. -

Examination of Estimates of Expenditure 2018-19 Reply Serial No

Examination of Estimates of Expenditure 2018-19 Reply Serial No. TH B( T) 26 3 CONTROLLING OFFICER’S REPLY (Question Serial No. 6090) Head: (60) Highways Department Subhead (No. & title): (-) Not Specified Programme: (1) Capital Projects Controlling Officer: Director of Highways (Daniel K W CHUNG) Director of Bureau: Secretary for Transport and Housing Question: Regarding the statement under the Programme of expanding and improving the road network in order to meet the growth in traffic demand, serving new development areas and facilitating the movement of people and goods both within the territory and across the boundary in accordance with approved programmes, please advise this Committee on: (1) the road network with expansion and improvement completed in each year over the past three financial years in table form, including the names of roads involved, the total traffic capacity increased, the total road length increased, the expenditure involved for expansion and improvement of road network (covering the total number of construction workers engaged); (2) the road network with expansion and improvement planned for the coming financial years, including the names of roads involved, the total traffic capacity increased, the road length increased, the expenditure involved for expansion and improvement of road network (covering the total number of construction workers engaged). Asked by: Hon LUK Chung-hung (Member Question No. (LegCo use): 56) Reply: (1) The titles of the projects completed in financial years 2015-16, 2016-17 and 2017-18 -

Fare Table for KMB Bus Routes 15 May 2011 Kowloon Services Route No

Page 1 Fare Table For KMB Bus Routes 15 May 2011 Kowloon Services Route No. Route Non A/C Fare A/C Fare 1 Star Ferry ÅÆ Chuk Yuen Estate / $5.20 Nathan Road to Star Ferry / $4.60 Mong Kok Road to Chuk Yuen Estate / $4.80 1A Star Ferry ÅÆ Sau Mau Ping (Central) $4.60 $6.50 Kwun Tong (Yue Man Square) to Star Ferry $4.60 $6.20 Prince Edward Road East(San Po Kong) to Star Ferry $4.60 $5.20 Nathan Road to Star Ferry $3.90 $4.60 Mong Kok Road to Sau Mau Ping (Central) $4.60 $6.20 Kwun Tong Road (Lower Ngau Tau Kok Estate) to Sau Mau Ping (Central) $4.60 $5.20 Kwun Tong Road (Yue Man Square) to Sau Mau Ping (Central) $3.30 $4.10 2 Star Ferry ÅÆ So Uk / $4.40 2A Mei Foo ÅÆ Lok Wah / $5.20 Ngau Tau Kok Road to Lok Wah / $4.60 Lai Chi Kok Road / Nathan Road Junction to Mei Foo / $4.60 2B Chuk Yuen Estate ÅÆ Cheung Sha Wan / $4.40 2C Yau Yat Tsuen Æ Tsim Sha Tsui [Circular] / $4.40 2D Tung Tau Estate ÅÆ Chak On Estate / $4.40 2E Kowloon City Ferry ÅÆ Pak Tin $3.30 $4.60 2F Cheung Sha Wan ÅÆ Tsz Wan Shan(North) / $5.20 Wong Tai Sin Station to Tsz Wan Shan (North) / $4.60 3B Hung Hom Ferry Concourse ÅÆ Tsz Wan Shan (Central) / $4.60 3C China Ferry Terminal ÅÆ Tsz Wan Shan (North ) $3.90 $5.20 Nathan Road to China Ferry Terminal $3.90 $4.60 Argyle Street to Tsz Wan Shan (North ) $3.90 $4.80 Wong Tai Sin Station to Tsz Wan Shan (North ) $3.30 $4.60 3D Kwun Tong (Yue Man Square) ÅÆTsz Wan Shan (Central) $3.30 $4.60 3M Tsz Wan Shan (North) ÅÆ Choi Wan / $3.90 Clear Water Bay Road (outside Choi Hung Station) to Choi Wan / $3.50 3Pz#◇▽ Tsz Wan Shan (South) -

BUILD KING HOLDINGS LIMITED (Incorporated in Bermuda with Limited Liability) (Stock Code: 00240)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. BUILD KING HOLDINGS LIMITED (Incorporated in Bermuda with limited liability) (Stock Code: 00240) ANNOUNCEMENT OF RESULTS FOR THE YEAR ENDED 31 DECEMBER 2009 FINANCIAL PERFORMANCE HIGHLIGHTS Percentage of increase in equity** per share 73% Equity HK$151 million Equity per share HK16 cents Group revenue and share of revenue of jointly controlled entities HK$1,035 million Profit attributable to owners of the Company HK$64 million ** equity refers to equity attributable to owners of the Company 1 RESULTS The board of directors (the “Board”) of Build King Holdings Limited (the “Company”) announces the audited consolidated statement of comprehensive income of the Company and its subsidiaries (the “Group”) for the year ended 31 December 2009 and the consolidated statement of financial position of the Group as at 31 December 2009 together with the comparative figures for 2008 as follows: CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2009 2009 2008 Notes HK$’000 HK$’000 Revenue 3 822,072 751,130 Cost of sales __________(742,916) __________(783,611) Gross profit (loss) 79,156 (32,481) Other income 3,865 36,221 Increase (decrease) in fair value of held-for-trading -

Note for Public Works Subcommittee of Finance Committee

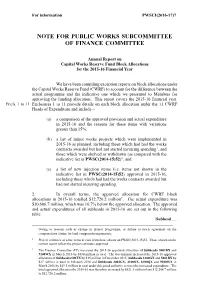

For information PWSCI(2018-19)3 NOTE FOR PUBLIC WORKS SUBCOMMITTEE OF FINANCE COMMITTEE Annual Report on Capital Works Reserve Fund Block Allocations for the 2016-17 Financial Year We have been compiling exception reports on block allocations under the Capital Works Reserve Fund (CWRF) to account for the difference between the actual programme and the indicative one which we presented to Members for approving the funding allocation. This report covers the 2016-17 financial year. Encls. 1 to 11 Enclosures 1 to 11 provide details on each block allocation under the 11 CWRF Heads of Expenditure and include – (a) a comparison of the approved provision and actual expenditure in 2016-17 and the reasons for those items with variations greater than 15%; (b) a list of minor works projects which were implemented in 2016-17 as planned, including those which had had the works contracts awarded but had not started incurring spending1, and those which were shelved or withdrawn (as compared with the indicative list in PWSC(2015-16)48)2; and (c) a list of new injection items (i.e. items not shown in the indicative list in PWSC(2015-16)48) approved in 2016-17, including those which had had the works contracts awarded but had not started incurring spending. 2. In overall terms, the approved allocation for CWRF block allocations in 2016-17 totalled $12,944.2 million3. The actual expenditure was $10,359.8 million, which was 20% below the approved allocation. The approved and actual expenditures of all subheads in 2016-17 are set out in the following table – /Subhead .... -

檔號︰HAD K&T DC/13/9/52A 07 Pt

Ref. No.: HAD K&T DC/13/9/23A/17/Pt.1 Minutes of the 2nd Meeting of the Traffic and Transport Committee (2017) of Kwai Tsing District Council Date: 13 April 2017 Time: 2:34 p.m. – 4:23 p.m. Venue: Kwai Tsing District Office Conference Room Attendee Time of Arrival (p.m.) Time of Departure (p.m.) Mr TSUI Hiu-kit (Chairman) Start of meeting End of meeting Miss KWOK Fu-yung Start of meeting End of meeting (Vice-chairman) Mr CHAN Siu-man, Simon Start of meeting 3:41 Mr CHOW Wai-hung, Rayman Start of meeting End of meeting Mr CHOW Yick-hay, BBS, JP Start of meeting End of meeting Miss CHU Lai-ling Start of meeting End of meeting Mr HUI Kei-cheung 3:03 End of meeting Mr LAM Siu-fai Start of meeting 3:42 Ms LAU Mei-lo 2:36 3:44 Mr LEE Chi-keung, Alan, MH Start of meeting End of meeting Mr LEUNG Chi-shing 3:07 End of meeting Mr LEUNG Kam-wai 2:42 End of meeting Mr LEUNG Tsz-wing, Dennis 4:16 End of meeting Mr LEUNG Wai-man, MH Start of meeting 3:36 Mr LI Sai-lung Start of meeting 3:27 Miss LO Yuen-ting Start of meeting End of meeting Ms MAK Mei-kuen, Alice, BBS, JP Start of meeting 3:09 Mr NG Ka-chiu 2:36 End of meeting Mr NG Kim-sing 2:46 End of meeting Mr PAU Ming-hong Start of meeting End of meeting Ms TAM Wai-chun, MH Start of meeting End of meeting Mr TANG Shui-wah 2:46 End of meeting Mr WONG Bing-kuen 3:00 4:17 Mr WONG Yiu-chung, MH 2:36 End of meeting Mr CHAN Dik-sau Start of meeting End of meeting Mr CHAN Man-luen-ying Start of meeting End of meeting Mr Elson CHOW Start of meeting End of meeting 1 Mr LEUNG Kong-ming Start of meeting 3:44 Mr LI Man-ka 2:42 Start of meeting Mr YIP Pui-lam Start of meeting Start of meeting In Attendance Mr WU Tin-yau, Gordon Assistant District Officer (Kwai Tsing), Kwai Tsing District Office Mr CHAN Chi-ming Senior Engineer (Special Duties), Transport Department Ms LO Shuet-yee Engineer (Special Duties)2, Transport Department Mr TANG Kam-kee Senior Engineer (Covered Walkway)1, Highways Department Mr.TANG Yiu-key Project Coordinator (Covered Walkway)1-1, Highways Department Mr. -

Cb(1)2110/10-11(10)

CB(1)2110/10-11(10) 11 May, 2011 Clerk to Bills Committee on Motor Vehicles (First Registration Tax) (Amendment) Bill 2011 Legislative Council Secretariat 3rd floor Citibank Tower 3 Garden Road, Central, Hong Kong Dear Sir/Madam, Re: Bills Committee on Motor Vehicles (First Registration Tax) (Amendment) Bill 2011 We are writing in support of the government’s proposal to increase the first registration tax (FRT) for private cars to cope with the surge in the number of private vehicles. Overarching Principles for Transport Policies in Hong Kong Hong Kong benefits immensely from an excellent public transport system, which is renowned for its quality and ability to accommodate the mobility need for the city. Not only does public transport provide nearly ubiquitous coverage for the territory, it also carries over 90% of Hong Kong’s 11 million daily trips. Due to the success of this public transport system, private car ownership and usage remain non-essential for the majority, which leads to manifold benefits – reducing the need for extensive highway infrastructure expansion, curbing growth in vehicular emissions, and contributing to the long-term sustainability of Hong Kong. Indeed, sustaining the quality of our public transport system is a key policy objective for Hong Kong, as was recognized in the first White Paper on internal transport policy in 1979, reiterated in the second White Paper on Transport Policy in 1990, and again at the conclusion of the third Comprehensive Transport Studies “Hong Kong Moving Ahead” in 1999. Pillars contributing to the success of our public transport system include managing road usage such as controlling the growth in number of vehicles and giving priority to public transport, as set out in the 1990 White Paper. -

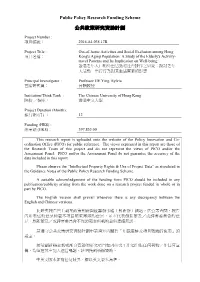

Research Report Is Uploaded Onto the Website of the Policy Innovation and Co- Ordination Office (PICO) for Public Reference

Public Policy Research Funding Scheme 公共政策研究資助計劃 Project Number : 項目編號: 2016.A4.035.17B Project Title : Out-of-home Activities and Social Exclusion among Hong 項目名稱: Kong's Aging Population: A Study of the Elderly's Activity- travel Patterns and Its Implication on Well-being 香港老年人口的外出活動和社會排斥之研究:探討老年 人活動─出行行為對其生活質素的影響 Principal Investigator : Professor HE Ying, Sylvia 首席研究員: 何穎教授 Institution/Think Tank : The Chinese University of Hong Kong 院校 /智庫: 香港中文大學 Project Duration (Month): 推行期 (月) : 12 Funding (HK$) : 總金額 (HK$): 397,853.00 This research report is uploaded onto the website of the Policy Innovation and Co- ordination Office (PICO) for public reference. The views expressed in this report are those of the Research Team of this project and do not represent the views of PICO and/or the Assessment Panel. PICO and/or the Assessment Panel do not guarantee the accuracy of the data included in this report. Please observe the “Intellectual Property Rights & Use of Project Data” as stipulated in the Guidance Notes of the Public Policy Research Funding Scheme. A suitable acknowledgement of the funding from PICO should be included in any publication/publicity arising from the work done on a research project funded in whole or in part by PICO. The English version shall prevail whenever there is any discrepancy between the English and Chinese versions. 此研究報告已上載至政策創新與統籌辦事處(創新辦)網站,供公眾查閱。報告 內所表達的意見純屬本項目研究團隊的意見,並不代表創新辦及/或評審委員會的意 見。創新辦及/或評審委員會不保證報告所載的資料準確無誤。 請遵守公共政策研究資助計劃申請須知內關於「知識產權及項目數據的使用」的 規定。 接受創新辦全數或部分資助的研究項目如因研究工作須出版任何刊物/作任何宣 傳,均須在其中加入適當鳴謝,註明獲創新辦資助。 -

Note for Public Works Subcommittee of Finance Committee

For information PWSCI(2013-14)6 NOTE FOR PUBLIC WORKS SUBCOMMITTEE OF FINANCE COMMITTEE Annual Report on Capital Works Reserve Fund Block Allocations for the 2012-13 Financial Year We have been compiling exception reports on block allocations under the Capital Works Reserve Fund (CWRF) to account for the difference between the actual programme and the indicative one which we presented to Members for approving the funding allocation. This report covers the 2012-13 financial year. Encls. 1 to 11 Enclosures 1 to 11 provide details on each block allocation under the 11 CWRF Heads of Expenditure and include – (a) a comparison of the approved provision and actual expenditure in 2012-13 and the reasons for those items with variations greater than 15%; (b) a list of minor works projects which were implemented in 2012-13 as planned, including those which had had the works contracts awarded but had not started incurring spending, and those which were shelved or withdrawn (as compared with the indicative list in PWSC(2011-12)33); and (c) a list of new injection items (i.e. items not shown in the indicative list in PWSC(2011-12)33) approved in 2012-13, including those which had had the works contracts awarded but had not started incurring spending. 2. In overall terms, the approved allocation for CWRF block allocations in 2012-13 totalled $11,557.8 million1. The actual expenditure was $10,400.7 million, which was 10% below the approved allocation. ------------------------- Financial Services and the Treasury Bureau October 2013 ——————————————————————————————————— 1 The Finance Committee approved in January 2013 the creation of a new block allocation Subhead 6101TX and an allocation of $2.4 million for 2012-13. -

Note for Public Works Subcommittee of Finance Committee

For information PWSCI(2016-17)7 NOTE FOR PUBLIC WORKS SUBCOMMITTEE OF FINANCE COMMITTEE Annual Report on Capital Works Reserve Fund Block Allocations for the 2015-16 Financial Year We have been compiling exception reports on block allocations under the Capital Works Reserve Fund (CWRF) to account for the difference between the actual programme and the indicative one which we presented to Members for approving the funding allocation. This report covers the 2015-16 financial year. Encls. 1 to 11 Enclosures 1 to 11 provide details on each block allocation under the 11 CWRF Heads of Expenditure and include – (a) a comparison of the approved provision and actual expenditure in 2015-16 and the reasons for those items with variations greater than 15%; (b) a list of minor works projects which were implemented in 2015-16 as planned, including those which had had the works contracts awarded but had not started incurring spending1, and those which were shelved or withdrawn (as compared with the indicative list in PWSC(2014-15)52)2; and (c) a list of new injection items (i.e. items not shown in the indicative list in PWSC(2014-15)52) approved in 2015-16, including those which had had the works contracts awarded but had not started incurring spending. 2. In overall terms, the approved allocation for CWRF block allocations in 2015-16 totalled $12,726.2 million3. The actual expenditure was $10,606.7 million, which was 16.7% below the approved allocation. The approved and actual expenditures of all subheads in 2015-16 are set out in the following table – /Subhead .... -

Circular Is Important and and Is Important This Circular the Proposed Acquisition of of the Proposed Acquisition the Proposed Whitewash Resolution

CIRCULAR DATED 28 AUGUST 2017 MAPLETREE LOGISTICS TRUST THIS CIRCULAR IS IMPORTANT AND (Constituted in the Republic of Singapore pursuant to a trust deed dated 5 July 2004 (as amended)) REQUIRES YOUR IMMEDIATE ATTENTION CIRCULAR DATED 28 AUGUST 2017 Singapore Exchange Securities Trading Limited (the “SGX-ST”) CIRCULAR TO UNITHOLDERS IN RELATION TO: takes no responsibility for the accuracy of any statements or opinions made, or reports contained, in this Circular. If you are 1. THE PROPOSED ACQUISITION OF in any doubt as to the action you should take, you should consult your stockbroker, bank manager, solicitor, accountant or other MAPLETREE LOGISTICS HUB TSING YI, professional adviser immediately. HONG KONG SAR WHICH IS AN INTERESTED If you have sold or transferred all your units in Mapletree PERSON TRANSACTION; AND Logistics Trust (“MLT”, and the units in MLT, the “Units”), you should immediately forward this Circular, together with the 2. THE PROPOSED WHITEWASH RESOLUTION. Notice of Extraordinary General Meeting and the accompanying Proxy Form in this Circular, to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or IMPORTANT DATES AND TIMES FOR UNITHOLDERS transfer was effected for onward transmission to the purchaser or transferee. Last date and time 10 September 2017 for lodgement of (Sunday) at 3.30pm This Circular does not constitute an offer of securities in the Proxy Forms United States or any other jurisdiction. Any proposed issue of new Units described in this Circular will not be