Indonesian Infrastructure: Stable Foundations for Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

May 2018'S Green Infrastructure Investment Opportunities

GREEN INFRASTRUCTURE INVESTMENT OPPORTUNITIES INDONESIA Published by the Climate Bonds Initiative Developed in partnership with Pembiayaan Investasi Non-Anggaran Pemerintah (PINA), a project of the National Development Planning Agency (BAPPENAS), and PT. EBA Indonesia. Green Infrastructure Investment Opportunities, Indonesia Contents This report highlights green infrastructure investment 3 Executive summary opportunities in Indonesia 4 Indonesia’s green infrastructure: an This report has been prepared to support “green”, are presented in a pipeline of opportunity for change Indonesia’s mission to develop low-carbon opportunities for investment in 2018-2019. and climate-resilient infrastructure. It Priorities for investment beyond 2019 are 5 Enabling infrastructure highlights green infrastructure investment also covered. investments will boost growth opportunities, with the aim of facilitating The report is part of a research series 7 Opportunities in global green engagement on this topic between project which will investigate green infrastructure finance owners and developers, and investors. investment opportunities in ASEAN 13 Green infrastructure investment The report is intended for a wide range (Association of Southeast Asian Nations) opportunities of stakeholders in Indonesia and abroad, member countries. including domestic and international 14 Transport In developing this report the Climate investors, companies and developers, 17 Energy Bonds Initiative consulted the Indonesian and relevant Indonesian Government 21 Water and waste -

PT INKA Company Profile

INKA www.inka.co.id INDONESIAN RAILWAY INDUSTRY INKA PT INDUSTRI KERETA API (Persero) Factory & Head Office Jl. Yos Sudarso No. 71 Madiun 63122, East Java - INDONESIA Telp. +62 351 452271-74 Fax. +62 351 452275 Email. [email protected] Website. www.inka.co.id Representative Office Taspen Tower 3rd Floor Jl. Jend Sudirman Kav 2, Jakarta - INDONESIA Telp. +62 21 25144 Fax. +62 21 2514423 Email. [email protected] Jl. Tubagus Ismail VII No. 22 B, Bandung - INDONESIA Telp/Fax. 62-22-2508167 PT Industri Kereta Api (Persero) @ptinkapersero @ptinka @pt_inka - COMPANY PROFILE - CONTENT DIRECTOR’S REMARKS 2 ABOUT PT INKA 3 PT INKA’S TRANSFORMATION 5 (MILESTONE) VISION AND MISSION 6 ACHIEVEMENTS 7 PT INKA’S WORLD BUSINESS 7 PARTNERSHIP 8 PRODUCTS 9 LOCOMOTIVE 9 PASSENERS COACH 10 SELF PROPELLED TRAINSET 11 ELECTRIC MULTIPLE UNIT 12 LIHT RAIL TRANSIT 13 FREIHT CARRIAE 14 EPORT PRODUCTS 15 Director’s Remarks CUSTOMIE PRODUCTS 16 PRODUCTION FACILITIES 17 We would like to express our gratitude to all stakeholders who have been giving the attention and support for INKA. INKA, as the railway manufacturing industry has committed to sustainably produce passenger coach, freight wagon and other high quality product. This is maintained by having technology innovation to meet the customer's demand either for the nation or worldwide. We do hope INKA and the stakeholders can BUDI NOVIANTORO simultaneously grow in the more developing business I’M PRO President Director area. Integritas Mutu Profesional INKA Committed To Excellence 1 Company Profile PT INKA (Persero) Company Profile PT INKA (Persero) 2 About INKA PT Industri Kereta Api or PT INKA incorporated on May 18, 1981 and is the first integrated railway and manufacturing company in the Southeast Asia. -

BAB II GAMBARAN UMUM PT.INKA (Persero)

BAB II GAMBARAN UMUM PT.INKA (Persero) Bab dua berisi sejarah dan perkembangan, produk perusahaan, lokasi, visi, misi, struktur organisasi, dan tempat kerja praktik. 2.1 Profil Perusahaan 2.1.1 Nama dan Logo Perusahaan Nama dari perusahaan ini adalah PT.INKA kependekan dari PT.Industri Kereta Api, Logo perusahaan dapat dilihat pada Gambar 2.1. Gambar 2.1 Logo PT INKA 2.1.2 Alamat Perusahaan Kantor PT.INKA beralamat di Jl. Yos Sudarso No. 17 Madiun Lor Manguharjo, Kota Madiun, Jawa Timur . Peta dari perusahaan PT.INKA bisa dilihat di gambar 2.2 5 6 Gambar 2.2 Peta perusahaan PT.INKA 2.1.3 Prestasi Perusahaan PT Industri Kereta api telah mendapatkan beberapa prestasi hingga tahun 2011 sebagai berikut : Bidang IT Juara III pengelola portal Executive Information System Terbaik oleh kementerian BUMN November 2011 Juara II Website dengan Marketing Communication Terbaik oleh Kementerian BUMN 2010 Juara II Website dengan User Interface terbaik oleh Kementerian BUMN 2010 7 Bidang Keuangan BUMN kategori Industri Non Keuangan yang Berpredikat Sangat Bagus dari Infobank 2011 Bidang Teknologi Emas untuk Corporate Tecnology Achievement oleh PII (Perusahaan Insinyur Indonesia) 2010 Perunggu untuk Adhicipta Rekayasa oleh PII (Persatuan Insinyur Indonesia) 2010 2.1.4 Visi Perusahaan Menjadi perusahaan kelas dunia di bidang kereta api dan transportasi perkotaan di Indonesia. 2.1.5 Misi Perusahaan Membuat solusi terintegrasi untuk kereta api dan transportasi perkotaan dengan keunggulan kompetitif dalam bisnis dan teknologi tepat guna untuk mendorong pengembangan transportasi yang berkelanjutan. 2.2 Sejarah dan Perkembangan perusahaan PT Industri Kereta Api (Persero), yang selanjutnya disingkat dengan nama INKA, atau PT INKA merupakan sebuah badan usaha milik Negara yang berdiri pada 18 Mei 1981. -

Curriculum Vitae

Curriculum Vitae A. PERSONAL INFORMATION Name : Ir. Budi Noviantoro Place/Date of Birth : Bojonegoro, November 17th 1960 Gender : Male Religion : Islam Home Address : Jl. Stasion Timur No. 12-A RT/RW : 004/002 Kel. Kebon Jeruk, Kec. Andir Kota Bandung, Jawa Barat Email address : [email protected] B. EDUCATION 1. Public Elementary School (SDN Bojonegoro, 1972) 2. Junior High School (SMP Negeri Probolinggo, 1975) 3. Senior High School (SMA Katolik Probolinggo, 1979) 4. Bachelor Degree of Civil Hydraulics (Sepuluh Nopember Institute of Technology, 1985) C. WORKING EXPERIENCE POSITION PERIOD PT INDUSTRI KERETA API (Persero) 1. President Director of PT Industri Kereta Api 15-01-2018 until present (Persero) PT KERETA API INDONESIA (Persero) 1. Managing Director of Logistic and Development 25-01-2016 until 14-01 2018 2. President Director of PT KA Logistik 04-03-2014 until 24-01-2016 3. Executive Vice President Freight Marketing & 01-09-2013 until 03-03-2014 Sales 4. Executive Vice President Subsidiary 01-06-2013 until 31-08-2013 Development 5. Executive Vice President Subsidiary 26-03-2013 until 31-05-2013 6. Executive Vice President Strategic Planning and 09-10-2012 until 25-03-2013 Business Development 7. Executive Vice President Railway Assets 24-07-2012 until 08-10-2012 8. Main Staff of President Director 21-02-2012 until 23-07-2012 9. EVP Regional Division III South Sumatra 30-07-2010 until 20-02-2012 10. EVP Strategic Planning & Business Development 03-08-2009 until 29-07-2010 11. Head of the Company's Long Term Plan 21-10-2008 until 02-08-2009 12. -

Sinergi Riset Dan Inovasi Teknologi Sarana Perkeretaapian

SINERGI RISET DAN INOVASI TEKNOLOGI SARANA PERKERETAAPIAN Hotel Aryaduta, Jakarta Selasa, 19 Februari 2019 Ir. Tri Hardono GM Pengembangan PT Industri Kereta Api (Persero) 1 PROFIL PT INDUSTRI KERETA API (PERSERO) 1 PROFIL PT INKA (PERSERO) MENJADI PERUSAHAAN KELAS DUNIA YANG UNGGUL DI BIDANG PERKERETAAPIAN DAN TRANSPORTASI PERKOTAAN DI INDONESIA 2 RANGE PRODUK LOCOMOTIVE PASSENGER EMU, DEMU, RAILBUS FREIGHT SPECIAL VEHICLE LRT COACH DMU WAGON LRT Palembang NEW LRT JABODEBEK SINGLE BUS 3 CAPAIAN EKSPOR Thailand 1998 – 70 Units Ballast Hopper Wagon 2000 – 20 Units Ballast Hopper Wagon Malaysia 1991 –Freight Wagon for KTMB 2002 – Flat Wagon and Power Car 2010 – 12 Units Passenger Car 2 Units Power Car 2 Units Dining Car Filipina Bangladesh 1996 –Locomotives 2005 – 50 Broad Gauge (BG) 2017 – 2TS Diesel Multiple Unit Carriages 2018 (On Going) – 2014 – 50 Broad Gauges (BG) 2TS -3Car DMU 100 Meter Gauges 4TS-4Car DMU (MG) Carriages 3 Locomotives 2017 – 50 BG and 200 MG 15 Passenger Coaches Australia Freight Wagon 2004 – 224 Blizzard 25 Flat Wagon Underframe Singapura 2009 – Well Wagons & Flat Wagons for Hitachi Plant Technology 4 PROFIL TINGKAT KANDUNGAN DALAM NEGERI (TKDN) LRT PALEMBANG ELECTRIC MULTIPLE UNIT PASSENGER COACH LOCOMOTIVE TKDN UP TO TKDN UP TO TKDN UP TO TKDN UP TO TKDN UP TO TKDN UP TO TKDN UP TO TARGET TKDN UP TO TARGET TKDN UP TO DMU PHILIPPINE FREIGHT WAGON DEMU MINANGKABAU MEDIUM SPEED TRAIN LRT JABODEBEK 5 PROFIL TINGKAT KANDUNGAN DALAM NEGERI (TKDN) LOCAL CONTENT KRL Bandara Soekarno-Hatta ≈ 43% UPAYA INKA DALAM MENGEJAR -

Laporan Kunjungan Kerja Spesifik Komisi V Dpr Ri Dalam Rangka Peninjauan Pt

LAPORAN KUNJUNGAN KERJA SPESIFIK KOMISI V DPR RI DALAM RANGKA PENINJAUAN PT. INKA DAN AKADEMI PERKERETAAPIAN INDONESIA DI MADIUN, PROVINSI JAWA TIMUR TANGGAL 20 APRIL S.D. 21 APRIL 2016 KOMISI V DPR-RI JAKARTA, 2016 Laporan Kunker Spesifik Komisi V DPR RI dalam Rangka Peninjauan PT. Industri Kereta Api dan Akademi Perkeretaapian Indonesia di Madiun, Provinsi Jawa Timur Tgl. 20 - 21 April 2016 Hal 1 LAPORAN KUNJUNGAN KERJA SPESIFIK KOMISI V DPR RI DALAM RANGKA PENINJAUAN PT. INDUSTRI KERETA API DAN AKADEMI PERKERETAAPIAN INDONESIA DI MADIUN, PROVINSI JAWA TIMUR TANGGAL 20 APRIL S.D. 21 APRIL 2016 I. PENDAHULUAN A. Dasar Hukum 1) Amandemen Undang-Undang Dasar 1945; pada perubahan Pertama Pasal 20, Perubahan Kedua Pasal 20 A, perubahan Ketiga Pasal 23; 2) Undang-Undang RI Nomor 42 Tahun 2014 Tentang Perubahan Terhadap Undang- Undang RI Nomor 17 Tahun 2014 Tentang Majelis Permusyawaratan Rakyat, Dewan Perwakilan Rakyat, Dewan Perwakilan Daerah, dan Dewan Perwakilan Rakyat Daerah; 3) Peraturan Dewan Perwakilan Rakyat Indonesia Nomor 1 Tahun 2014 Tentang Tata Tertib Dewan Perwakilan Rakyat Republik Indonesia. B. Maksud dan Tujuan Maksud kunjungan kerja spesifik Komisi V DPR RI adalah: 1. Untuk melaksanakan fungsi pengawasan secara spesifik melalui peninjauan secara langsung terhadap kesiapan teknologi fasilitas, sumber daya manusia dan kondisi riil industri kereta api di Madiun dalam memenuhi kebutuhan perekertaapian di tanah air dengan tetap menjamin keamanan dan keselamatan (security and safety). 2. Melaksanakan fungsi pengawasan secara spesifik melalui peinjauan langsung fasilitas dan bangunan fisik, sumber daya manusia pendidik, dan sumber daya manusia Taruna Akademi Perkeretaapian Indonesia (API) di Madiun. 3. Dengan melakukan kunjungan spesifik ini, Komisi V dapat mengetahui permasalahan- permasalahan yang dihadapi PT. -

LKP: Automatic Clamping System Side Frame Bogie Pada Kereta

6 BAB II GAMBARAN UMUM PERUSAHAAN Pada Bab ini melakukan pembahasan tentang Profil, sejarah dan perkembangan, struktur organisasi perusahaan, pengenalan unit kerja teknologi produksi, daftar kerjasama, produk pada Perusahaan PT INKA. 2.1 Profil PT. INKA 2.1.1 Nama dan Logo PT. INKA Gambar 2.1 merupakan lambang dari PT. Industri Kereta Api (Persero), yang biyasa disebut dengan PT. INKA (Persero). Gambar 2.1 Lambang PT. INKA (Sumber : http://bumn.go.id/inka ) 2.1.2 Denah Lokasi PT. INKA Gambar 2.2 merupakan gambaran denah lokasi dari PT. INKA (Persero) Madiun. 7 Gambar 2.2 Daerah Lokasi PT. INKA (Sumber : http://www.google.co.id ) 2.1.3 Alamat PT. INKA Kantor : Jl. Yos Sudarso No. 17 Madiun Lor Manguharjo, Kota Madiun, Jawa Timur – Indonesia 63122 Telp. (0351) 452271 / 452272 Fax (0351) 452275 2.1.4 Falsafah PT. INKA Profesional yang Bekerja Berlandaskan Iman dan Takwa, Menghargai Orang Lain dan Bersahabat, Menjunjung Tinggi Kejujuran, Memiliki Daya Saing Berkelanjutan, serta Menghasilkan Nilai Tambahan pada Lingkungan. 2.1.5 Visi Menjadi perusahaan kelas dunia di bidang kereta api dan transportasi perkotaan di Indonesia. 8 2.1.6 Misi Membuat solusi terintegrasi untuk kereta api dan transportasi perkotaan dengan keunggulan kompetitif dalam bisnis dan teknologi tepat guna untuk mendorong pengembangan transportasi yang berkelanjutan. 2.1.7 Nilai– nilai PT. INKA 1. Tumbuh dan Berkembang Mampu memberikan nilai tambah perusahaan secara berkelanjutan dan selalu berusaha menjadi lebih baik dibandingkan kondisi hari ini. 2. Mutu Mampu memberikan kinerja lebih dari standar. 3. Belajar Berkelanjutan Mampu meningkatkan wawasan, ilmu dan keterampilan dirinya secara berkelanjutan berdasarkan tuntutan yang sedang terjadi. -

Selamat Datang Kereta Modern Edisi 0 4 / 2 0 1 8 Halo Ceo

www.wika.co.id SELAMAT DATANG KERETA MODERN EDISI 0 4 / 2 0 1 8 HALO CEO SELAMAT DATANG KERETA MODERN embangunan infrastruktur kereta api ringan (Light Rail Transit/ PLRT) dan Mass Rapid Transit (MRT) yang menghubungkan daerah penyangga ibukota, seperti Depok, Bekasi, dan Tangerang Selatan menjadi pemandangan harian yang dijumpai oleh para urbaner (warga yang tinggal di pinggiran Jakarta). Kokoh dan tingginya tiang penyangga dan span-span penghubung menunjukkan bahwa Jakarta dan kota- kota sekitarnya itu siap memasuki babak baru tranportasi modern. Moda trasportasi itu semua didesain sedemikian rupa untuk menekan angka kemacetan ibukota sekaligus memberikan alternatif pilihan bagi TUMIYANA - Direktur Utama (CEO) para warga Jakarta dan sekitarnya untuk beralih kepada angkutan PT Wijaya Karya (Persero) Tbk. umum yang nyaman, cepat, dan ramah lingkungan. [email protected] Kehadiran moda transportasi modern menjadi sangat vital dan ditunggu kehadirannya. Bayangkan, saat ini, tidak kurang dari 18 juta kendaraan beredar di seantero Jakarta setiap harinya. Bilamana semuanya turun ke jalan bersamaan pada interval waktu yang berdekatan, seperti apa kemacetan yang akan ditimbulkan? Kompleks sekali bukan? Membangun infrastruktur kereta modern di tengah tren ekonomi dan demografi yang terus bertumbuh memang bukan pekerjaan mudah. Akan tetapi, hal ini, tidak mungkin untuk ditunda-tunda lagi. Kebutuhan dan mobilitas tinggi warga tidak bisa seluruhnya dibebankan hanya kepada kendaraan roda empat, dua, atau bahkan commuterline semata. Warga berhak mendapat pilihan transportasi yang beragam, yang memudahkan mereka untuk bergerak cepat mengikuti tuntutan waktu. Mari melihat tranportasi kereta modern, LRT dan MRT sebagai PT Wijaya Karya pelengkap yang nantinya akan mengurangi beban transportasi yang telah eksisting sebelumnya, Commuterline dan Transjakarta. -

Kebijakan Privatisasi Dalam Upaya Profitisasi Pt. Kereta Api

Sukarna Wiranta, Kebijakan Privatisasi … 753 KEBIJAKAN PRIVATISASI DALAM UPAYA PROFITISASI PT. KERETA API Sukarna Wiranta1 Abstract State owned enterprises (SOEs) as one of the country’s pillar of the country’s income through their contributions to national development. Therefore, to increase their contribution to national GDP, their capital expenditure would be further pushed the SOEs. PT. KAI as one of the BUMN in transportatiion to be privatisized by government by January 2011 which caused the controversial issues due to the does not clear the sale its share, particuarly the price which based on IPO scheme. This paper aims to explore the performance of PT. KAI (Kereta Api Indonesia), particularly PT. KCJ (Kereta Commuter Jakarta) by the IPO (Initial Procedure Obligation) scheme. Keywords: IPO Scheme, Profitation, Privatitation, KCJ’s Management. Abstrak Badan Usaha Milik Negara (BUMN) adalah salah satu pilar penting dalam pemasukan pendapatan negara melalui kinerja atau kontrubusi keuangan yang besar terhadap pembangunan nasional. Lagi pula, peningkatan kontribusinya terhadap PDB dan modalnya harus ditingkatkan supaya BUMN siap untuk meningkatkan pengeluarannya dalam upaya perbaikan sarana dan prasarana BUMN tersebut. Di sini, PT. KAI (Kereta Api Indonesia) sebagai BUMN dibidang transportasi perlu diprivatisasi dalam upaya meningkatkan modalnya tersebut guna menutupi pengeluaran- pengeluaran dalam biaya operasional serta perbaikan sarana dan prasarananya melalui skema IPO (Initial Procedure Obligation) atau PSO (Public Service Obligation). Makalah ini akan menginvestigasi kinerja PT. KAI, terutama kinerja atau pengelolaan PT. KCJ melalui skema PSO. Kata Kunci: PSO, Profitisasi, Privatisasi, Pengelolaan PT. KCJ. 1 Professor Riset bidang Sosial Ekonomi, Puslit Ekonomi, LIPI, e-mail: sukarna_22yahoo.com. 754 Jurnal Ekonomi & Kebijakan Publik, Vol. -

Ida Royani Kota Semarang Painting Dari Artis Cilik Hingga Perancang Busana

Tidak Untuk Dibawa Pulang VolumeTRACK 1 | Maret 2018 | On Train Magazine 88 MENANGKAN 10 TIKETKereta Api Kelas Eksekutif Kereta Bandara Soekarno-Hatta Menuju Bandara Tanpa Merana 28 Indahnesia 30 Globe 36 Famous Menapaki Sejarah Indian Elephants Ida Royani Kota Semarang Painting Dari artis cilik hingga perancang busana BOARDING KERETA API Terus Berdedikasi dan Melayani Para penumpang kereta api yang terhormat, PT Kereta Api Indonesia (Persero) dengan bangga menghadirkan majalah baru bertajuk OnTrack edisi perdana sebagai teman perjalanan Anda. OnTrack merupakan wajah baru In-House Magazine milik PT KAI. Kami berharap agar pembaca P mendapatkan banyak wawasan dari berbagai sajian informasi dengan Direktur Utama tampilan yang baru dan fresh, baik seputar perkeretaapian maupun informasi Edi Sukmoro lainnya yang sarat manfaat. Pada edisi perdana ini, kami menampilkan informasi terhangat seputar Direktur Komersial dan Teknologi Informasi KA Bandara Soekarno Hatta (KA Basoetta) yang peluncurannya telah diresmikan - oleh Presiden Joko Widodo pada 2 Januari 2018 lalu. KA Basoetta merupakan kereta bandara pertama di Pulau Jawa. Sebelumnya, pelayanan yang sama telah hadir sejak Juli 2013 di Sumatera Utara yang kita kenal sebagai KA Bandara Kualanamu. Sama Direktur Operasi seperti KA Bandara Kualanamu, Anak perusahaan PT KAI yakni PT Railink menjadi Slamet Suseno Priyanto operator pelayanan KA bandara di Pulau Jawa ini. PT Railink telah menyiapkan 10 trainset KA Basoetta dengan kapasitas Direktur Pengelolaan Prasarana 33.000 penumpang setiap harinya. KA Bandara ini dilengkapi berbagai fasilitas yang Muhammad Nurul Fadhila ada di stasiun dan selama perjalanan. Satu trainset terdiri dari 6 kereta yang mampu mengangkut 272 penumpang. Interior keretanya didesain seperti di pesawat, Direktur Pengelolaan Sarana penumpang dapat mengatur kemiringan kursi dan sandaran tangan. -

RIPNAS Siap Cetak-Dikompresi.Pdf

KementeriaN PERHUBUNGAN DIREKTORAT JENDERAL PERKERETAAPIAN REVIEW RENCANA INDUK PERKERETAAPIAN NASIONAL KATA PENGANTAR Transportasi mempunyai peran penting dalam mendukung pembangunan nasional. Menuju Indonesia Emas 2045 dengan visi “Berdaulat, Maju, Adil dan Makmur” diperlukan sistem transportasi yang handal sebagai pendukung roda penggerak ekonomi bangsa. Menyongsong era ke depan, menuntut pelayanan transportasi yang handal serta berwawasan lingkungan. Saat ini kapasitas layanan jalan semakin terbatas. Keterbatasan ini dapat dijawab oleh moda transportasi kereta api, di mana kereta api lebih unggul dari kapasitas angkut, kecepatan, keamanan, hemat energi dan ramah lingkungan. Rencana Induk Perkeretaapian Nasional merupakan dokumen jangka panjang yang menggambarkan satu kesatuan sistem perkeretaapian sebagai amanat Undang-Undang Nomor 23 Tahun 2007 tentang Perkeretaapian. Pada prinsipnya, penyusunan dokumen Rencana Induk Perkeretaapian Nasional yang terbit pada Desember 2018 ini adalah proses periodik pengkajian tinjau ulang. Tinjau ulang yang dilakukan mempertimbangkan perubahan lingkungan strategis. Dokumen Rencana Induk Perkeretaapian Nasional telah memuat strategi-strategi: 1) Pengembangan Jaringan Pelayanan, 2) Peningkatan Keamanan dan Keselamatan, 3) Alih Teknologi dan Pengembangan Industri, 4) Pengembangan Sumber Daya Manusia, 5) Pengembangan Kelembagaan, serta 7) Strategi Investasi dan Pendanaan. Seyogianya Rencana Induk Perkeretaapian Nasional dapat menjadi acuan seluruh stakeholders perkeretaapian nasional untuk berperan dalam perkeretaapian ke depan. Semoga perkeretaapian Indonesia semakin berjaya. Menteri Perhubungan Budi Karya Sumadi Direktorat Jenderal Perkeretaapian Nasional – Kementerian Perhubungan 2.3.4. Kebutuhan Energi Transportasi Perkeretaapian II-28 2.4. Kebijakan II-29 DAFTAR ISI 2.5. Program Utama II-29 KATA PENGANTAR BAB III Strategi Peningkatan Keselamatan dan Keamanan III-1 3.1. Pendahuluan III-1 BAB I Perkeretaapian Nasional I-1 3.2. Sasaran III-2 1.1. -

Format for Reporting Contract Agreement

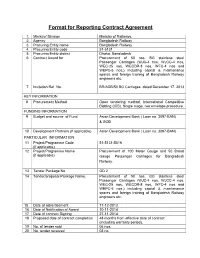

Format for Reporting Contract Agreement 1. Ministry/1 Division Ministry of Railways. 2. Agency2 Bangladesh Railway 3. Procuring Entity name Bangladesh Railway 4. Procuring3 Entity code 51-5131 5. Procuring Entity district Dhaka, Bangladesh 6. Contract Award for Procurement of 50 nos. BG stainless steel Passenger Carriages (WJC-4 nos, WJCC-4 nos, WEC-25 nos, WECDR-8 nos, WFC-4 nos and WEPC-5 nos.) including capital & maintenance spares and foreign training of Bangladesh Railway engineers etc. 7. Invitation Ref. No. BR/ADB/50 BG Carriages dated December 17, 2013 KEY INFORMATION 8 Procurement Method Open tendering method, International Competitive Bidding (ICB), Single stage, two envelops procedure. FUNDING INFORMATION 9 Budget and source of Fund Asian Development Bank ( Loan no. 3097-BAN) & GOB 10 Development Partners (if applicable) Asian Development Bank ( Loan no. 3097-BAN) PARTICULAR INFORMATION 11 Project/Programme Code 51-5131-5016 (if applicable) 12 Project/Programme Name Procurement of 100 Meter Gauge and 50 Broad (if applicable) Gauge Passenger Carriages for Bangladesh Railway. 13 Tender Package No. GD 2 14 Tender/proposal Package Name. Procurement of 50 nos. BG stainless steel Passenger Carriages (WJC-4 nos, WJCC-4 nos, WEC-25 nos, WECDR-8 nos, WFC-4 nos and WEPC-5 nos.) including capital & maintenance spares and foreign training of Bangladesh Railway engineers etc. 15 Date of advertisement 17-12-2013 16 Date of Notification of Award 10-11-2014 17 Date of contract Signing 27-11-2014 18 Proposed date of contract completion 48 months from effective date of contract (including warranty period). 19 No.