Luxembourg Annual Report (ABBL)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Supervised Entities (As of 1 September 2020)

List of supervised entities Cut-off date for changes: 1 September 2020 Number of significant entities directly supervised by the ECB: 114 This list displays the significant supervised entities, which are directly supervised by the ECB (part A) and the less significant supervised entities which are indirectly supervised by the ECB (Part B). Based on Article 2(20) of Regulation (EU) No 468/2014 of the European Central Bank of 16 April 2014 establishing the framework for cooperation within the Single Supervisory Mechanism between the European Central Bank and national competent authorities and with national designated authorities (OJ L 141, 14.5.2014, p. 1 - SSM Framework Regulation) a ‘supervised entity’ means any of the following: (a) a credit institution established in a participating Member State; (b) a financial holding company established in a participating Member State; (c) a mixed financial holding company established in a participating Member State, provided that the coordinator of the financial conglomerate is an authority competent for the supervision of credit institutions and is also the coordinator in its function as supervisor of credit institutions (d) a branch established in a participating Member State by a credit institution which is established in a non-participating Member State. The list is compiled on the basis of significance decisions which have been adopted and notified by the ECB to the supervised entity and that have become effective up to the cut-off date. A. List of significant entities directly supervised by the ECB Country of LEI Type Name establishment Grounds for significance MFI code for branches of group entities Belgium Article 6(5)(b) of Regulation (EU) No 1 LSGM84136ACA92XCN876 Credit Institution AXA Bank Belgium SA ; AXA Bank Belgium NV 1024/2013 CVRWQDHDBEPUUVU2FD09 Credit Institution AXA Bank Europe SCF France 2 549300NBLHT5Z7ZV1241 Credit Institution Banque Degroof Petercam SA ; Bank Degroof Petercam NV Significant cross-border assets 54930017BFF0C5RWQ245 Credit Institution Banque Degroof Petercam France S.A. -

Listing Prospectus Dated 21 October 2020 1 QUINTET PRIVATE BANK

Listing prospectus dated 21 October 2020 QUINTET PRIVATE BANK (EUROPE) S.A. (formerly KBL European Private Bankers S.A.) (Incorporated with limited liability in Luxembourg) €125,000,000 7.5 per cent. Fixed Rate Resettable Callable Perpetual Additional Tier 1 Capital Notes The issue price of the €125,000,000 7.5 per cent. Fixed Rate Resettable Callable Perpetual Additional Tier 1 Capital Notes (the “Notes”) of Quintet Private Bank (Europe) S.A. (the “Issuer” or “Quintet”) is 100 per cent. of their principal amount. The Notes will, subject to certain interest cancellation provisions described in Condition 3 (Interest Cancellation) in “Terms and Conditions of the Notes” (the “Conditions” and each, a “Condition”), bear interest on their Prevailing Principal Amount (as defined in Condition 17 (Interpretation)) on a non-cumulative basis from (and including) 23 October 2020 (the “Issue Date”) to (but excluding) 23 January 2026 (the “First Reset Date”) at a fixed rate of 7.5 per cent. per annum. Interest will be payable semi-annually in arrear on 23 January and 23 July of each year commencing on 23 January 2021 (each an “Interest Payment Date”). The rate of interest will reset on the First Reset Date and each date which falls five, and each multiple of five, years after the First Reset Date) (each, a “Reset Date”). The Issuer may elect, at its sole and absolute discretion, to cancel (in whole or in part) the payment of interest on the Notes otherwise scheduled to be paid on an Interest Payment Date. Furthermore, interest shall be cancelled (in -

Q U I N T E T Pillar Ill: Report 2019

Q U I N T E T P R I V A T E B A N K Pillar Ill: Report 2019 Quintet Private Bank (Europe) S.A. – Pillar 3 – 2019 Contents Glossary ................................................................................................................................................................. 5 Note to readers ...................................................................................................................................................... 6 Introduction ........................................................................................................................................................... 7 1. List of Subsidiaries & Associates ........................................................................................................... 9 2. Corporate governance & decision structure ......................................................................................... 9 2.1 Corporate Culture ............................................................................................................................ 9 2.1.1 Board & Executive Committees: structure and key governance principles................................... 9 Risk Management approach at Quintet ............................................................................................................... 12 3. Five lines of defence ........................................................................................................................... 12 4. Risk Control function ......................................................................................................................... -

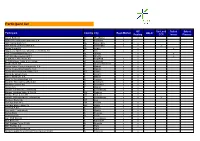

Participant List

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

DATA PROTECTION NOTICE May 2018 Version the Following Data

DATA PROTECTION NOTICE May 2018 version The following data protection notice applies to the online offering of Advanzia Bank S.A., a Luxembourg financial institution registered in the Luxembourg companies' register under the number B 109 476 and with the following contact details: Advanzia Bank S.A. 9, rue Gabriel Lippmann 5365 Munsbach, Luxembourg Tel. 0800 880 2120 Fax 00352 263875 699 [email protected] www.advanzia.com Advanzia Bank S.A. ("we", "us" or "our") collects and processes information about natural persons, who are our customers or those of partner banks, for whom we issue credit cards ("you" or "your"). This data protection notice provides information about what information we collect, how and why we process it, and with whom we share it. This notice applies to all aforementioned natural persons, regardless of their place of residence and the type of service or product, offered by us. The data protection notice should be read along with the general terms and conditions, which are notified to you at the beginning of the business relationship and which describe the product we offer. We must collect and process certain information about you in order to conclude and execute a contract with you, as well as to maintain our contractual relationship. Unless you provide us with such information, we may not be able to enter into, execute or fulfil any contract with you. We will notify you of the rejection of your application or termination of the contract that may result from your refusal to provide us with certain information or to exercise your statutory rights. -

Uebersicht Der Unterverwahrer.Xlsx

Übersicht der Unterverwahrer der DZ PRIVATBANK S.A. Stand: 28.06.2021 Markt Lagerstelle Unterverwahrer Beziehungsstatus ÄGYPTEN HSBC BANK EGYPT SAE ARGENTINIEN CLEARSTREAM BANKING S.A. LUXEMBOURG AUSTRALIEN BNP PARIBAS SECURITIES SERVICES S.A. AUSTRALIA BRANCH BANGLADESH STANDARD CHARTERED BANK DHAKA BRANCH BELGIEN EUROCLEAR BANK SA/NV BENIN STANDARD CHARTERED BANK COTE D'IVOIRE SA BRASILIEN BANCO BNP PARIBAS BRASIL S.A. BRASILIEN CITIBANK EUROPE PLC LUXEMBOURG BRANCH Citibank Sao Paulo BULGARIEN CLEARSTREAM BANKING S.A. LUXEMBOURG Eurobank EFG Bulgaria AD Sofia BURKINA-FASO STANDARD CHARTERED BANK COTE D'IVOIRE SA CHILE CITIBANK EUROPE PLC LUXEMBOURG BRANCH Banco de Chile DÄNEMARK NORDEA DANMARK, filial af Nordea Bank Abp Finland DEUTSCHLAND DZ BANK AG DEUTSCHE ZENTRAL-GENOSSENSCHAFTSBANK Deutsche WertpapierService Bank AG Muttergesellschaft DEUTSCHLAND DZ BANK AG DEUTSCHE ZENTRAL-GENOSSENSCHAFTSBANK diverse, abhängig vom Markt Muttergesellschaft DEUTSCHLAND DZ PRIVATBANK S.A. NIEDERLASSUNG STUTTGART DZ BANK AG DEUTSCHE ZENTRAL-GENOSSENSCHAFTSBANK Niederlassung der DZ PRIVATBANK S.A. ELFENBEINKUESTE STANDARD CHARTERED BANK COTE D'IVOIRE SA ESTLAND CLEARSTREAM BANKING S.A. LUXEMBOURG AS SEB Pank, Tallinn FINNLAND NORDEA BANK ABP FRANKREICH EUROCLEAR BANK SA/NV GHANA STANDARD CHARTERED BANK GHANA PLC GRIECHENLAND CITIBANK EUROPE PLC LUXEMBOURG BRANCH Citibank Europe Plc Athen Branch GROSSBRITANNIEN CITIBANK NA LONDON BRANCH GUINEA BISSAU STANDARD CHARTERED BANK COTE D'IVOIRE SA HONGKONG STANDARD CHARTERED BANK (HK) LTD. INDIEN STANDARD CHARTERED BANK MUMBAI BRANCH INDONESIEN PT BANK HSBC INDONESIA IRLAND REPUBLIK CITIBANK NA LONDON BRANCH IRLAND REPUBLIK EUROCLEAR BANK SA/NV W/ IRLAND ISLAND ISLANDSBANKI HF. ISRAEL BANK HAPOALIM B.M. ITALIEN BNP PARIBAS SECURITIES SERVICES MILANO BRANCH ITALIEN CITIBANK EUROPE PLC JAPAN MUFG BANK LTD JORDANIEN STANDARD CHARTERED BANK AMMAN BRANCH KANADA CITIBANK CANADA KENIA STANDARD CHARTERED BANK KENYA LTD KOLUMBIEN CITIBANK EUROPE PLC LUXEMBOURG BRANCH Cititrust Colombia S.A. -

Banking Automation Bulletin | Media Pack 2021

Banking Automation BULLETIN Media Pack 2021 Reaching and staying in touch with your commercial targets is more important than ever Curated news, opinions and intelligence on Editorial overview banking and cash automation, self-service and digital banking, cards and payments since 1979 Banking Automation Bulletin is a subscription newsletter Independent and authoritative insights from focused on key issues in banking and cash automation, industry experts, including proprietary global self-service and digital banking, cards and payments. research by RBR The Bulletin is published monthly by RBR and draws 4,000 named subscribers of digital and printed extensively on the firm’s proprietary industry research. editions with total, monthly readership of 12,000 The Bulletin is valued by its readership for providing independent and insightful news, opinions and 88% of readership are senior decision makers information on issues of core interest. representing more than 1,000 banks across 106 countries worldwide Regular topics covered by the Bulletin include: Strong social media presence through focused LinkedIn discussion group with 8,500+ members • Artificial intelligence and machine learning and Twitter @RBRLondon • Biometric authentication 12 issues per year with bonus distribution at key • Blockchain and cryptocurrency industry events around the world • Branch and digital transformation Unique opportunity to reach high-quality • Cash usage and automation readership via impactful adverts and advertorials • Deposit automation and recycling • Digital banking and payments Who should advertise? • Financial inclusion and accessibility • Fintech innovation Banking Automation Bulletin is a unique and powerful • IP video and behavioural analytics advertising medium for organisations providing • Logical, cyber and physical bank security solutions to retail banks. -

Life After PSD2

52 Hogan Lovells Open everything and improved security: life after PSD2 PSD2 is a significant piece of legislation, aimed at disrupting the traditional banking and payment services market, improving competition and promoting innovation. One of the ways it does this is by forcing providers to allow access to customer accounts to disruptors who can offer new services to customers by exploiting the wealth of information which can be obtained through access to customers’ account information. Nearly two years after PSD2 first came into force, how is this brave new era of open banking working out for both sides? What might the next twelve months bring? We provide a snapshot of the current state of play and some crystal ball gazing from our European and UK teams below. It’s not just about disruption though. PSD2 also were potential issues at all stages of payment looks to protect consumers by imposing a higher transactions, impacting retailers, card issuers, level of security for online activity and card merchant acquirers and the major card schemes. payments. This now requires “strong customer A concerted lobbying effort to delay full authentication” or “SCA”– involving 2 out of 3 implementation for online transactions resulted in elements of possession, knowledge or inherence – an EBA opinion, published in June 2019, setting for example, confirming a card payment by typing out a structure for national regulators to allow a in a one-time password sent to a mobile phone. degree of tolerance (or “supervisory flexibility”) Whilst the implementation date for these new for delayed implementation of SCA in their requirements was set for 14 September 2019, it jurisdictions. -

BEST EXECUTION & BROKER SELECTION POLICY Appendix 2 To

BEST EXECUTION & BROKER SELECTION POLICY Appendix 2 to the GTC I. PURPOSE This document defines the Best Execution and Broker Selection Policy of Quintet Private Bank (Europe) S.A. (“the Bank”). The Bank shall take all sufficient steps to obtain the best possible result for its Clients as required by Directive 2014/65/EU of 15 May 2014 on markets in financial Instruments (“hereinafter MiFID II”) when: • executing Client orders; • dealing on own account with Clients; • transmitting Client orders to other entities (brokers) for execution (reception and transmission of Client orders); and • making an investment decision within the framework of discretionary portfolio management and transmitting an order for execution to another entity (brokers). For this purpose, the Bank shall draw up: • A Best Execution Policy (for the execution of orders and dealing on own account with Clients) which includes execution venues where the Bank executes Client orders. • A Best Selection Policy (for RTO and portfolio management) which includes entities (brokers) where the Bank places or transmits client orders for execution. The Best Execution and Broker Selection Policy is appended to the Bank’s GTC and is available on the Bank’s website (www.quintet.com). Where a Client makes reasonable and proportionate requests for information about the Best Execution and Best Selection Policy and how it is reviewed, the Bank shall answer clearly and within a reasonable time. II. SCOPE a. CLIENTS TO WHICH THIS POLICY APPLIES MiFID II distinguishes three categories of Clients: • Private Clients (retail Clients); • Professional Clients are persons who are considered to have the experience, knowledge and expertise to make their own investment decisions and properly assess the risks that they incur; • Eligible counterparties which include regulated financial institutions (e.g. -

RABO 296 Broch EACB P5.Indd

Co-operative banks: Catalysts for economic and social cohesion in Europe 1 Co-operative Banks: Catalysts for economic and social cohesion in Europe Impressum: European Association of Cooperative Banks (EACB) Contact: E-mail : [email protected] • Telephone: (+ 32 )2 230 11 24 • Web: www.eurocoopbanks.coop © Copyright March 2007: European Association of Co-operative Banks 2 Co-operative Banks: Catalysts for economic and social cohesion in Europe The European Association of Co-operative Banks The Association of Co-operative Banks was established in 1970. It represents, promotes and defends the interests of its members and co-operative banks in general. In this role, the Association is the offi cial spokesman vis-à-vis the European institutions. With a view to fulfi lling these objectives, the mission of the Association is: • To provide information to members on all initiatives and measures taken by the European Union that affect the banking sector; • To organize an exchange of views and experiences and to co-ordinate member organisations’ positions on issues of common interest; • To carry out effi cient and active lobbying of European institutions; • To develop positions on issues of common interest. The European Association of Co-operative Banks fosters co- operation between co-operative banking groups. Furthermore, with the other representative co-operative organisations, the Association promotes the spirit of co-operation throughout the banking sector and beyond. In order to fulfi l these goals, the Association is one of the founding members of the European Banking Industry Committee (EBIC), the European Payments Council (EPC), the former European Committee for Banking Standards (ECBS) and the European Financial Reporting Advisory Group (EFRAG). -

CONVENTUM SICAV with Multiple Sub-Funds Under Luxembourg Law

Annual report including audited financial statements as at 31st December 2020 CONVENTUM SICAV with multiple sub-funds under Luxembourg law R.C.S. Luxembourg B70125 No distribution notices have been submitted for the Sub-Funds named below, which means that shares of these Sub- Funds may not be distributed to investors based within the territorial validity of the German “Kapitalanlagegesetzbuch (KAGB)” (Investment Code): - CONVENTUM - Institutional Fund - CONVENTUM - MultiAssets - CONVENTUM - Fortuna Royale 1 - CONVENTUM - Fortuna Royale 2 - CONVENTUM - Fortuna Royale 3 - CONVENTUM - Echium - CONVENTUM - FensiFund - CONVENTUM - Mekks - CONVENTUM - Prime Selection - CONVENTUM - Createrra Progress World Equities - CONVENTUM - Createrra Multi Assets Index Fund - CONVENTUM - Dynamic Opportunities - CONVENTUM - Income Opportunites - CONVENTUM - Equity Opportunities - CONVENTUM - Waterlily W Flexible Equity Fund - CONVENTUM - Alluvium Global Fund This report is the English translation of the audited annual including audited financial statements respectively unaudited semi- annual report in French. In case of a discrepancy of content and/or meaning between the French and English versions the French one shall prevail. Subscriptions can only be made on the basis of the complete prospectus accompanied by the articles of incorporation and the fact sheets of each of the sub-funds or based on the key investor information document ("KIID"). The complete prospectus may only be distributed if accompanied by the last annual report and the last semi-annual -

General Terms and Conditions Applicable from 1 December 2020

General Terms and Conditions applicable from 1 December 2020 QUINTET PRIVATE BANK (EUROPE) S.A. | R.C.S. LUXEMBOURG B 6395 | SWIFT KBLXLULL 43, boulevard Royal | L-2955 Luxembourg | Grand-Duché de Luxembourg 1 December 2020 T +352 47 97 1 | F +352 47 97 73 900 | W www.quintet.com Contents INTRODUCTION 1. Presentation of the Bank 5 2. Subject of the General Terms and Conditions 5 Part 1 – GENERAL POINTS 3. Relationship of trust 6 4. Authorised bank signatures 6 5. Provisions against money laundering, financing of terrorism and market abuse 6 5.1 Identification of the Client 6 5.1.1. Clients who are natural / legal persons 6 5.1.2. Association or grouping without a legal personality 6 5.1.3. Economic beneficiary 6 5.1.4. Updating of data 7 5.1.5. Inadequate documentation 7 5.2. Client behaviour 7 5.3 Provisions on market abuse 7 5.4 Additional communications 7 6. Banking secrecy 8 7. Obligations specific to the Client 8 8. International cooperation 9 8.1. Cooperation in criminal matters 9 8.2. Cooperation in tax matters 9 8.2.1. Withholding tax 9 8.2.2. Cooperation in the matter of the exchange of information on request 9 8.2.3. Cooperation in the matter of the exchange of information 9 9. Communication with the Bank 10 9.1 Languages of communication 10 9.2. Means of communication 10 10. Correspondence 10 10.1. Sending of correspondence 10 10.2. Domiciliation of correspondence 11 11. Proof 11 12. Complaints 11 13.