The Challenge of Rapidly Improving Transport Infrastructure in Poland

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

World Bank Document

Document of The World Bank Public Disclosure Authorized Report No: 34596 IMPLEMENTATION COMPLETION REPORT (TF-29121 FSLT-70540) ON A LOAN Public Disclosure Authorized IN THE AMOUNT OF EUR 110.0 MILLION (US$ 101.0 MILLION EQUIVALENT TO POLSKIE KOLEJE PANSTWOWE S.A. (POLISH STATE RAILWAYS S.A.) WITH THE GUARANTEE OF THE REPUBLIC OF POLAND FOR A RAILWAY RESTRUCTURING PROJECT Public Disclosure Authorized June 13, 2006 Infrastructure Department Poland and Baltic States Country Unit Europe and Central Asia Region Public Disclosure Authorized CURRENCY EQUIVALENTS (Exchange Rate Effective At Completion, December 30, 2005) Currency Unit = Polish Zloty PLN 1 = US$ 0.3099 US$ 1 = PLN 3.2265 US$ 1 = Euro 0.8391 (Exchange Rates Effective at Appraisal, January 31, 2001) PLN 1 = US$ 0.2418 US$ 1 = PLN 4.1350 US$ 1 = Euro 1.0887 FISCAL YEAR January 1 - December 31 ABBREVIATIONS AND ACRONYMS EBRD European Bank for Reconstruction and Development EIB European Investment Bank EIRR Economic Internal Rate of Return FIRR Financial Internal Rate of Return FMS Financial Management System GoP Government of Poland IAS International Accounting Standards IFAC International Federation of Accountants ISPA Instrument for Structural Policies for Pre-accession KBI Capital Investment and Privatization Office KM Warsaw Regional Railways ('Koleje Mazowiekie') KAAZ Agency for Retraining and Reemployment ('Kolejowa Agencja Aktywizacji Zawodowej') LHS Linia Hutniczo-Siarkowa (Broad-gauge Railway between Ukraine and Silesia) LRS Labor Redeployment Services MoI Ministry of Infrastructure MLSP Ministry of Labor and Social Policy MTME Ministry of Transport and Maritime Economy NLO National Labor Office PAD Project Appraisal Document PLK S.A. Polish Railway Infrastructure Joint Stock Company ('Polskie Linie Kolejowe Spolka Akcyjna') PKP Polish State Railways ('Polskie Koleje Panstwowe') PKP S.A. -

Construction of a New Rail Link from Warsaw Służewiec to Chopin Airport and Modernisation of the Railway Line No

Ex post evaluation of major projects supported by the European Regional Development Fund (ERDF) and Cohesion Fund between 2000 and 2013 Construction of a new rail link from Warsaw Służewiec to Chopin Airport and modernisation of the railway line no. 8 between Warsaw Zachodnia (West) and Warsaw Okęcie station Poland EUROPEAN COMMISSION Directorate-General for Regional and Urban Policy Directorate Directorate-General for Regional and Urban Policy Unit Evaluation and European Semester Contact: Jan Marek Ziółkowski E-mail: [email protected] European Commission B-1049 Brussels EUROPEAN COMMISSION Ex post evaluation of major projects supported by the European Regional Development Fund (ERDF) and Cohesion Fund between 2000 and 2013 Construction of a new rail link from Warsaw Służewiec to Chopin Airport and modernisation of the railway line no. 8 between Warsaw Zachodnia (West) and Warsaw Okęcie station Poland Directorate-General for Regional and Urban Policy 2020 EN Europe Direct is a service to help you find answers to your questions about the European Union. Freephone number (*): 00 800 6 7 8 9 10 11 (*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you). Manuscript completed in 2018 The European Commission is not liable for any consequence stemming from the reuse of this publication. Luxembourg: Publications Office of the European Union, 2020 ISBN 978-92-76-17419-6 doi: 10.2776/631494 © European Union, 2020 Reuse is authorised provided the source is acknowledged. The reuse policy of European Commission documents is regulated by Decision 2011/833/EU (OJ L 330, 14.12.2011, p. -

The New Warszawa Zachodnia Station Opens Tomorrow

8 December 2015 Press Release The new Warszawa Zachodnia station opens tomorrow The new Warszawa Zachodnia (Warsaw West) railway station is ready for passengers' use just one year after its construction process begun. The building, which has an area of approx. 1,300 sq m, is located in the immediate vicinity of Aleje Jerozolimskie street in Warsaw, enabling residents from Ochota, Włochy and Mokotów districts to quickly and easily reach the station. The landmark new station’s striking design including a distinctive glass dome is the result of an efficient collaboration partnership between PKP S.A., Xcity Investment, and HB Reavis, an international developer group. As of tomorrow, people travelling from the Warszawa Zachodnia railway station will be able to access this brand new building, situated at Aleje Jerozolimskie street, closer to the tracks where local connections are available. The scheme will expand on the previous facility at Tunelowa street, which will continue to serve passengers. Due to its location, the new railway station will be more easily accessible by public means of transportation. 'This is our first investment undertaken in collaboration with PKP S.A. and we hope that it is not the last as the Warszawa Zachodnia station is great success. Within less than 12 months since construction works began, the building is now ready for use. Without a doubt, passengers will appreciate its striking design, impressive glass dome and surroundings, which already look attractive but will make even more of an impact once the adjacent office buildings are completed,' said Stanislav Frnka, CEO of HB Reavis Poland. -

Implementation for Polish State Railways Group

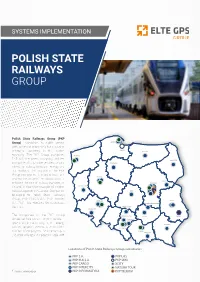

SYSTEMS IMPLEMENTATION POLISH STATE RAILWAYS GROUP Polish State Railways Group (PKP Group) combines its public service GDYNIA with activity characteristic for a modern GDAŃSK enterprise operating in the market OLSZTYN economy. The PKP Group comprises SZCZECIN PKP S.A., the parent company, and ten BIAŁYSTOK companies that provide services, among BYDGOSZCZ others, on railway transport, energy and ICT markets. The mission of the PKP Group companies is to build trust and POZNAŃ improve the image of the railway, so as to SIEDLCE enhance the role of railway transport in WARSZAWA Poland, following the example of modern ZIELONA GÓRA railways operating in Europe. Companies ŁÓDŹ belonging to Polish State Railways Group: PKP CARGO S.A., PKP Intercity WROCŁAW LUBLIN S.A., PKP Linia Hutnicza Szerokotorowa SKARŻYSKO-KAMIENNA Sp. z o.o.. CZĘSTOCHOWA WAŁBRZYCH The companies of the PKP Group TARNOWSKIE GÓRY KIELCE ZAMOŚĆ altogether hire almost 70,000 people – SOSNOWIEC specialists in the railway, IT, ICT, energy RZESZÓW and real property sectors. In terms of the KATOWICE KRAKÓW number of employees, the PKP Group is NOWY SĄCZ the second largest employer in Poland.[1] Locations of Polish State Railways Group subsidiaries. PKP S.A. PKP LHS PKP PLK S.A. PKP SKM PKP CARGO XCITY PKP INTERCITY NATURA TOUR [1] Source: www.pkp.pl PKP INFORMATYKA PKP TELKOM ET GPS Positioning system The ET GPS system is designed to monitor the position of locomotives and wagons. GPS tracker saves the object location, speed, direction of movement and information from sensors and interfaces. The data saved in the internal memory of the GPS tracker are transferred to the monitoring system. -

The PKP Group 2016 About the PKP Group 3

2016 Contents 2 1. About the PKP Group 2. Scheme of the PKP Group 3. The Main Companies of the PKP Group: • PKP S.A. • PKP PLK • PKP Cargo • PKP Intercity • PKP LHS • PKP SKM • PKP Informatyka • Xcity Investment The PKP Group 2016 About the PKP Group 3 The PKP Group was established in 2001 as a result of the restructuring process of the Polskie Koleje Państwowe (Polish State Railways) the State Owned Enterprise. Polskie Koleje Państwowe Spółka Akcyjna was established on 1 January 2001 as a result of the commercialization of the Polskie Koleje Państwowe SOE and entered into the rights and obligations of its predecessor. On the basis of the Polskie Koleje Państwowe SOE a number of companies were established in 2001 in the areas of: railway passenger transport; freight transport; railway infrastructure management; in addition, the following entities were established: • nine companies providing services for infrastructure renovations and repairs; • two companies dealing with rolling stock repairs; • three companies operating in secondary areas, such as training, pharmacy and supplies; • five companies operating in other areas related to railway services. The PKP Group 2016 About the PKP Group 4 As the result of the ownership changes, including privatization and restructuring in 2016 the PKP Group consisted of: Polskie Koleje Państwowe Spółka Akcyjna – the Parent Company in the PKP Group; PKP Intercity S.A. and PKP Szybka Kolej Miejska w Trójmieście Sp. z o.o. (also being the infrastructure manager of No. 250 Urban Line) – the passenger transport operator; PKP CARGO S.A. and PKP Linia Hutnicza Szerokotorowa Sp. z o.o. -

New Passenger Rolling Stock in Poland

Technology Jan Raczyński, Marek Graff New passenger rolling stock in Poland Rail passenger transport in Poland has been bad luck over 20 years. these investments as a result of delays caused trouble in operation Their decline was caused by insuffi cient investment both passen- and the lack of opportunities to improve the services off ered. ger rolling stock and rail infrastructure. As a result, railway off er has The best economic condition (relative high stability) are observed become uncompetitive in relation to road transport to the extent for two operators in the Warsaw region: Mazovia Railways (Koleje that part of the railway sector fell to 4%. Last years, mainly thanks Mazowieckie – commuter traffi c) and Warsaw Agglomeration Rail- to EU aid founds, condition of railway in Poland has changed for way (Szybka Kolej Miejska SKM – suburban and agglomeration traf- the better. In details, modernization of railway lines have begun, fi c) record annual growth of passengers after a few percent. They new modern rolling stock have been purchased, which can im- also carry out ambitious investment programs in purchases of new prove the rail travel quality. However, average age of the fl eet has rolling stock and Mazovia Railways also thorough modernization of already begun closer to 30 years. its fl eet. SKM is based in mostly on new rolling stock purchased in recent years and still planning new purchases. Passenger rail market Passenger transport market in Poland almost entirely is the sub- It is observed a stabilization in passengers numbers in Poland car- ject of contracts Public Service Contract (PSC) of operators with ried by railway for 10 years. -

Sieciowe Systemy Informatyczne W Polskim Transporcie Kolejowym W Okresie Przemian Ustrojowych I Technologicznych

PRACE NAUKOWE POLITECHNIKI WARSZAWSKIEJ z. 104 Transport 2014 8^ Henryk Rudowski Politechnika Warszawska, Instytut Informatyki, ^)< SIECIOWE SYSTEMY INFORMATYCZNE W POLSKIM TRANSPORCIE KOLEJOWYM W OKRESIE PRZEMIAN USTROJOWYCH I TECHNOLOGICZNYCH #B: L`hYx Streszczenie: ?B b < B? L $ ?b w wyniku tego ? GB $ = ? V = bB V < ?= = 4 = technologicznym realizowane z wykorzystaniem technologii sieci komputerowych BV=4= B ? m ICT. W pracy uB ? =<?b?=B <= ?b= b ? = < V ?b B b V = = I wieku. W tym = = = oraz automatyza= <, b zmianami nymi w G $ = L = <= = = È $ B : sieciowe systemy informatyczne, Grupa PKP 1. A W artykule przedstawiono historyczne, ?b powstania sieciowych informatycznych ? L $LBNawet w okresie PRL, bV ? b ? = sy biznesowe b = B 90 /#dowski V?otu, VbVB? ? $ Lstwowe. Zaprezentowano wybrane systemy sieciowe, czyli ? 4 $ zrealizowane w technologiach sprzed zniesienia embargo na technologie informatyczne, i zmiany w systemach < $ < B Systemy b È $ na podstawie ustawy z \ V `hhh B B ?V4 cie. L < ? b4 ? VLVÈ$ b = V B Wskazano bna za=È$= informatycznych =B 2. HISTORYCZNE, 6"%a&7!TECHNOLGICZNE +"6+%&"%!"6"a"NIA SYSTEMÓW SIECIOWYCH W PKP $, B zawsze == = ? = gdzie V systemy informatyczne. W $ L b?<BCentralnego Biura Statystyki utworzonego 1 stycznia 1958 r. Biuro to o =?L =-analitycznych. ?L b . ! V " ?L V }G~ ?V $ V = ! hh ) B analitycznymi a elektronicznymi maszynami cyfrowymi. -

Case Study: Polish Railways

Railway Reform: Toolkit for Improving Rail Sector Performance Case Study: Polish Railways Case Study Polish Railways 1 Introduction The Polish railway industry was devastated by the collapse of the planned economy in Eastern Europe and Central Asia. Traffic volumes plummeted as traditional rail customers vanished. At the same time, Government deregulated road transport, unleashing fierce competition for the remaining traffic. This led to severe financial, market, operational and asset challenges for the railway industry. Government re- sponded with well-planned railway industry reforms, consistent with the Euro- pean Union (EU) acquis communautaire295 as it relates to railways. Although the reform put in place an appropriate industry structure, the PKP Group initially lacked the leadership needed to benefit from the reforms. It was not until 2012 with the introduction of a commercially-oriented management fully sup- ported by government policymakers that the reform began to take hold and see adequate allocation of funds, financial stability among key subsidiaries, and im- provement in customer services. This case study describes these reforms, and their impact on the structure and performance of the Polish railway sector. 2 The Situation Prior to Reforms In the early 1990s, the Soviet economic system collapsed, reducing steel and coal shipments, and driving down railway freight traffic in Poland. Polish State Rail- ways, Polskie Koleje Panstwowe’s (PKP), conducted all rail sector activities in the country, including freight and passenger rail operations. During the 1990s, PKP’s freight revenues dropped by 67 percent in real dollars (Figure 1). 295 The acquis communitaire is the accumulated body of European Union (EU) law and obligations as it has evolved since 1958 to the present day. -

Chapter 9 Pkp Intercity 9.1 Present Situation and Issues

Final Report (Technical Report) The Feasibility Study of Polish State Railways S.A. (PKP S.A.) Privatization in the Republic of Poland CHAPTER 9 PKP INTERCITY 9.1 PRESENT SITUATION AND ISSUES (1) General Motorization is reducing the share of railway transport. Railways will not be able to maintain the same level of passenger volume if it continues to provide service at the present levels transport speed. Accordingly, it is imperative that the train speeds be improved if the same level of transportation volume is to be maintained. The vertical separation of PKP is presents the fundamental problem of the system itself. The railway is a system-integrated industry. The vertical separation was done as for the sake of survival, but it has resulted in sub-optimal operation. PKP Intercity was established in September 2001 as operator of Eurocity, Intercity, Express trains and some Night trains. It operates over a limited route network, providing frequent (generally regular-interval) trains over the four main routes and more restricted service on a number of others. In 2002, some 8.9 million journeys were made by the company’s services, representing 3.1 billion passenger-km. International traffic accounts for less than 10% of the company’s business. This company has the role of creating a new age for PKP passenger transport through the operation of high-speed trains on selected lines. Increasing motorization is the main cause of dwindling share of railway transportation and this casts shadows on the PKP Intercity operation too. Furthermore, the company faces the problem of extended journey times due to infrastructure maintenance backlogs as well as the competition that will arise from highway construction and potentially from EU open access beginning next year. -

11758828 01.Pdf

Final Report (Technical Report) The Feasibility Study of Polish State Railways S.A. (PKP S.A.) Privatization in the Republic of Poland TABLE OF CONTENTS PART 1 CHAPTER 1 RAILWAY POLICIES AND RAILWAY MANAGEMENT STRATEGIES ------ 1- 1 1.1 Concepts of Railway Restructuring and Privatization and Basic Principle of JICA’s Study------ 1- 1 1.1.1 Need for Restructuring and Privatizing the Polish Railways ---------------------------- 1- 1 1.1.2 Restructuring and Privatization of the Japanese National Railways ------------------ 1- 1 1.1.3 Basic Principles of JICA’s Study ---------------------------------------------------------- 1- 2 1.2 Circumstances Faced by the Polish Railways------------------------------------------------------------ 1- 3 1.2.1 Trends in Railway Demand ------------------------------------------------------------------- 1- 3 1.2.2 Changes Accompanying the Accession to EU --------------------------------------------- 1- 4 1.3 Analysis of Pending Issues--------------------------------------------------------------------------------- 1- 7 1.3.1 Overly Extended Railway Network --------------------------------------------------------- 1- 7 1.3.2 Lack of Railway Transport Services Meeting Market Need ----------------------------- 1- 9 1.3.3 Lack of Financial Resources for Settling Accumulated Debts --------------------------- 1-11 1.3.4 Legislative Organizational and Structural Aspects Hindering Railway Operation ---- 1-12 1.3.5 An Overview of Issues ------------------------------------------------------------------------ 1-13 1.3.6 -

2015 Annual Report Table of Contents

2015 Annual Report Table of contents Foreword by the President of the Management Board...........................4 Members of the Management Board and the Supervisory Board.......5 Financial result...................................................................................................6 Company assets.......................................................................................................6 Source of assets financing.......................................................................................8 Equity............................................................................................................8 External capital.........................................................................................................9 Economic-financial results......................................................................................11 Train path sales................................................................................................14 Timetable as the Company’s primary product.......................................................14 Data concerning completed international carriages..............................................15 Operation systems..................................................................................................16 Infrastructure...................................................................................................18 Rail roads...............................................................................................................18 Automatics -

Information Systems in Management of Polish Railway Companies of Pkp Group in Aspects of Technology and Economy

INFORMATION SYSTEMS IN MANAGEMENT Information Systems in Management (2015) Vol. 4 (3) 193 −204 INFORMATION SYSTEMS IN MANAGEMENT OF POLISH RAILWAY COMPANIES OF PKP GROUP IN ASPECTS OF TECHNOLOGY AND ECONOMY MICHA! HENRYK RUDOWSKI Institute of Computer Science, Warsaw University of Technology Paper presents selected management information systems in the railway industry companies arising from the transformation of the Polish State Rail- ways into PKP Group. Hardware and software solutions used by this systems and benefits of implement them are also pointed out. Takes into account the areas of financial management as well as the areas of operational manage- ment, specific for their activities. These issues are presented in the context of technology and economy. It has been proved that the organizational solu- tions imply the impossibility of efficient use of resources allocated to infor- mation systems due to consummate the benefits of consolidation, virtualiza- tion and cloud computing is impossible. Keywords: managing systems, railway industry, consolidation, virtualization, cloud computing. 1. Introduction IT is a very important part of modern enterprise and its quality and Total Cost of Ownership (TCO) may determine a competitive advantage in the market. IT solutions are particularly significant in companies on the railway market like PKP Group companies. Modern IT has a number of solutions that increase productivity and significantly lowering TCO, which is the sum of capital and operating costs. Currently the leading role is played by systems operating in the cloud environment with the ability to provide both highest availability and highest performance for the various applications while reducing costs thanks to consolidation, virtualization, automation of service delivery and management.