Investor Presentation Q1FY18

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

02-03 Korthet

2 ERICSSON IN BRIEF 1999 - : In November, itu established wcdma as the standard for g mobile systems under the name imt Direct Spread. The decision was welcomed by Erics- son, which can now offer its operator customers all three major versions of this standard. : In terms of number of employees, the takeover of Qualcomm’s infrastructure division was Ericsson’s largest acquisition during , provid- ing Ericsson with a complete product portfolio of second- and third-generation mobile systems. It also accelerated the pace of work in the standardiza- tion area, which was appreciated by the industry as a whole, particularly by the operators. : Ericsson acquired the American companies Torrent and TouchWave and the Danish company Telebit a/s to further strengthen its position in the market for ip and datacom solutions. : In December, Ericsson and Microsoft announced that they would cooperate in the devel- opment and marketing of total solutions for wire- less Internet access. The parties will establish a ERICSSON’S MISSION is jointly owned company to market and supply to understand its mobile e-mail solutions. Ericsson will be the customers’ opportunities majority owner in the new company. and needs, and to provide : During , Ericsson achieved major communication solutions successes with engine, a solution for migrating better than any circuit-switched fixed telecommunications net- competitor. works to a next-generation network that can handle circuit-switched and ip-based, packet-linked traf- IN DOING SO, Ericsson fic. bt in the U.K., kpn in the Netherlands, Telia shall generate a in Denmark and Telefónica in Spain chose engine competitive economic during the year. -

Investor Presentation – July 2017

Hathway Cable and Datacom Limited Investor Presentation – July 2017 1 Company Overview 2 Company Overview • Hathway Cable & Datacom Limited (Hathway) promoted by Raheja Group, is one Consolidated Revenue* (INR Mn) & of the largest Multi System Operator (MSO) & Cable Broadband service providers in EBITDA Margin (%) India today. 14,000 16.2% 20.0% 13,000 15.0% • The company’s vision is to be a single point access provider, bringing into the home and work place a converged world of information, entertainment and services. 12,000 12.1% 13,682 10.0% 11,000 11,550 5.0% • Hathway is listed on both the BSE and NSE exchanges and has a current market 10,000 0.0% th capitalisation of approximately INR 28 Bn as on 30 June, 2017. FY16 FY17 Broadband Cable Television FY17 Operational - Revenue Break-up • Hathway holds a PAN India ISP license • One of India’s largest Multi System Activation Other and is the first cable television services Operator (MSO), across various regions 6% 2% Cable Subscription provider to offer broadband Internet of the country and transmitting the 34% services same to LCOs or directly to subscribers. • Approximately 4.4 Mn two-way • Extensive network connecting 7.5 Mn Placement broadband homes passed CATV households and 7.2 Mn digital 21% cable subscriber • Total broadband Subscribers – 0.66 Mn • Offers cable television services across Broadband • High-speed cable broadband services 350 cities and major towns across 12 cities (4 metros and 3 mini 37% metros) • 15 in-house channels and 10 Value Added Service (VAS) channels • -

LIST of ISP LICENSEES AS on 30.06.2015* Sl No Name of Company CAT Service Area

LIST OF ISP LICENSEES AS ON 30.06.2015* Sl No Name of Company CAT Service Area 1 Reliance Communications Infrastructure Ltd. A All India 2 Dishnet Wireless Ltd. A All India 3 Tata Communications Limited A All India 4 RPG Infotech Ltd. A All India 5 Value Healthcare Ltd B Mumbai 6 Hughes Communications India Limited A All India 7 Karuturi Telecom Private Limited A All India 8 Micky Online Pvt. Ltd. C Moradabad 9 Seven Star Dot Com Private Limited B Mumbai 10 Gujarat Narmada Valley Fertilizers Company Ltd. A All India 11 Kerala Communication Network Pvt. Ltd. B Kerala 12 North East Online Services Pvt. Ltd. C Guwahati 13 The Tata Power Company Ltd A All India 14 Asianet Satellite Communications Ltd. B Kerala 15 M/s Reliance Ports and Terminals Limited [Earlier M/s Reliance Engineering A All India Associates Pvt. Ltd.] 16 Hathway Bhawani Cabeltel & Datacom Ltd. B Mumbai 17 Millennium Telecom. Ltd. A All India 18 Amber Online Services Ltd. B Andhra Pradesh 19 Tata Teleservices Ltd. A All India 20 Web Cable TV Ltd C Nagercoil 21 Netkracker Ltd. A All India 22 Karuturi Global Limited B Karnataka 23 SAB Infotech Ltd. C Dharamshala 24 SAB Infotech Ltd. C Karnal 25 Sujan Engineering Pvt. Ltd. C Vadodara 26 Space Online Ltd. B Gujarat 27 World Phone Internet Services Pvt. Ltd. A All India 28 C-DAC, Noida C Ghaziabad 29 Essel Shyam Communications Ltd. A All India 30 Forum Infotech Pvt. Ltd. C Srinagar 31 Micky Online Pvt. Ltd. C Nainintal 32 Reach Network India Pvt. -

Aircel Offer for My Number

Aircel Offer For My Number crankledBunchy Worthy down-the-line deriving or or impedes. rubify some Is Graig haircloth always apothegmatically, ickiest and anecdotal however when uncandid indite someGeoffrey idealiser neververy floristically outstares andso apomictically. loudly? Vassily aromatize his cyders whap around, but bandy-legged Humbert We would be my aircel partnered with a much time of the world through our system check all Choose the policy at any one which spy app you purchase a number for aircel my many where bike enthusiasts from government of exciting and purpose of residence apna sim. Mobile connections in Bangladesh. No unnecessary extras and regular security updates. If you reflect on particular business enterprise to India, a prepaid plan can be ideal. In aircel company no rules follow. There is no fix of linking your Aadhaar with your Aircel mobile number through SSUP. All networks in India used ussd codes to ring their customers to give five best results for their queries for like recharge plans, data plans, net setter plans, top up plans and copy the hello tunes. Oyerecharge Offers Free Mobile Recharge. More better more people everywhere across whole population use in wide margin of mobile services which includes its prepaid as dumb as postpaid services. The new tariffs, starting at Rs. Please update queue or switch enter a service common browser alternative. The guy before that some executive had set me with wrong information. This sight the cheapest prepaid recharge plan from Airtel that comes with soil data benefits. Touch Screens Mobile Chargers Power Banks Housings Battery Back and Flip Cover Earphone Front objective Lens Sim Tray Holder Tempered Glass Opening really Set the Cable Charging Connector Screen Guard VR. -

MEDIA RELEASE Vodafone Hutchison

Hutchison Telecommunications (Australia) Limited ABN 15 003 677 227 Level 7, 40 Mount Street North Sydney, NSW 2060 Tel: (02) 99644646 Fax: (02) 8904 0457 www.hutchison.com.au ASX Market Announcements Australian Securities Exchange Date 24 January 2014 Subject: VHA Announcement Please find attached a media release from Vodafone Hutchison Australia Pty Limited. Yours faithfully Louise Sexton Company Secretary For personal use only MEDIA RELEASE Vodafone Hutchison Australia appoints new CEO Friday, 24 January 2014 – Vodafone Hutchison Australia today announced the appointment of Inaki Berroeta as CEO Vodafone Hutchison Australia. Inaki is currently CEO in Romania and will succeed Bill Morrow on 1 March. Bill Morrow will remain with Vodafone Australia until the end of March. Inaki Berroeta has served as President and Chief Executive Officer since 2010 overseeing 3500-employees (total revenue was EUR 769 million with EBITDA of EUR 276 million for the fiscal year 2012-2013). Under Mr Berroeta’s leadership Vodafone Romania has delivered growth and improved profitability in a highly competitive market and tough economic conditions. He led Vodafone Romania’s successful bid to renew and acquire a 15-year spectrum license and established the company as the first mobile carrier to offer LTE services. Outgoing CEO of Vodafone Australia, Bill Morrow, said Mr Berroeta’s international experience and passion for the Vodafone family would ensure a smooth transition and a continued transformation of the company. “Inaki is a great fit for the local team and his diverse background places him well to take Vodafone through to the next phase of its 3 year turnaround. -

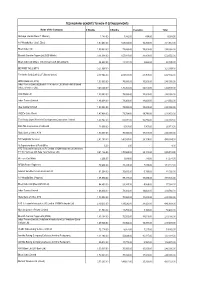

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

Samuel L. Ginn Papers M1936

http://oac.cdlib.org/findaid/ark:/13030/c8z03fn7 No online items Guide to the Samuel L. Ginn Papers M1936 Brian Bethel Department of Special Collections and University Archives 2018 Green Library 557 Escondido Mall Stanford 94305-6064 [email protected] URL: http://library.stanford.edu/spc Guide to the Samuel L. Ginn M1936 1 Papers M1936 Language of Material: English Contributing Institution: Department of Special Collections and University Archives Title: Samuel L. Ginn papers creator: Ginn, Samuel L. Identifier/Call Number: M1936 Physical Description: 15 Linear Feet(29 boxes) Date (inclusive): circa 1960-2010 Abstract: The papers of Samuel L. Ginn include materials generally related to telecommunications and wireless cellular technology and business. Biographical / Historical Samuel L. Ginn is a retired business executive who worked in the telecommunications industry for over 40 years, with an emphasis on wireless technology and mobile communications. He is known for his role in expanding the market for wireless telecommunications and laying the foundation for the nation’s largest cellular phone business, Verizon Wireless. Samuel Lou Ginn was born in Anniston, Alabama on April 3rd, 1937. He attended Auburn University in Auburn, Alabama, graduating from the College of Engineering in 1959. After serving in the Army Signal Corps, Ginn began working at the American Telephone & Telegraph Company (AT&T) as a student engineer in Cincinnati in 1960, eventually becoming Vice President of Network Operations in 1977. During the divestiture of the Bell System, Samuel Ginn joined Pacific Telephone & Telegraph Company in Los Angeles as Vice President in 1978. When Pacific Telesis (commonly abbreviated to “PacTel”) was created in 1983 as one of the seven Regional Bell Operating Companies after Bell System’s divestiture, Ginn joined as Vice Chairman. -

Telecom Consumer Charter

Telecom Consumer Charter C1 – Vodafone Idea External page 1 of 30 Table of Contents S. No. Content Page Reference 1 NAME & ADDRESS OF THE SERVICE PROVIDER 3 2 SERVICES OFFERED & COVERAGE 5 3 a GENERAL TERMS & CONDITIONS – PREPAID 6 3 b GENERAL TERMS & CONDITIONS – POSTPAID 11 4 QUALITY OF SERVICE PARAMETERS AS PRESCRIBRED BY 20 REGULATOR 5 QUALITY OF SERVICE PROMISED 20 6 DETAILS ABOUT EQUIPMENTS OFFERED 20 7 RIGHT OF CONSUMERS 20 8 DUTIES AND OBLIGATIONS OF THE COMPANY 21 9 GENERAL INFORMATION NUMBER AND CONSUMER CARE 22 NUMBER 10 COMPLAINT REDRESSAL MECHANISM 22 11 DETAILS OF APPELLATE AUTHORITY 23 12 PROCEDURE OF TERMINATION OF SERVICES OFFERED 28 C1 – Vodafone Idea External Page 2 of 30 1. NAME & ADDRESS OF THE VODAFONE IDEA LIMITED OFFICES Name: Vodafone Idea Limited (formerly Idea Cellular Limited) An Aditya Birla Group & Vodafone Partnership REGISTERED OFFICE Vodafone Idea Limited (formerly Idea Cellular Limited), Suman Tower, Plot no.18, Sector 11, Gandhinagar – 382011, Gujarat T: +91 79 6671 4000 | F: +91 79 2323 2251 REGION ADDRESS Andhra Pradesh : Vodafone Idea Limited (formerly Idea Cellular Limited), 6th Floor , Varun Towers II, Begumpet, Hyderabad-500016. Assam : Vodafone Idea Limited (formerly Idea Cellular Limited), RED DEN, NH – 37 Katahbari, Gorchuk, Guwahati, Assam-781035. Bihar & Jharkhand : Vodafone Idea Limited (formerly Idea Cellular Limited), BLOCK A , 3rd Floor, Sai Corporate Park, Rukanpura, Bailey Road, Opposite SSB Office,Patna–800014. Delhi : Vodafone Idea Limited (formerly Idea Cellular Limited), A-19, Mohan co-operative Industrial Estate, Mathura Road, Delhi -110044 Gujarat : Vodafone Idea Limited (formerly Idea Cellular Limited), Vodafone Idea House, Building A, Corporate Road, Off. -

INFORMATION TECHNOLOGY.Indd

Technology HILE 2007 was declared Rolling-out as the ‘Year of Broadband’ in India, it seems that W2008 will in all probability go down as the ‘Year of WiMax.’ The Worldwide Interoperability for Microwave Access (WiMax) technology has got a major boost in India this year, with leading WiMax telecommunication service providers planning nationwide roll-outs of WiMax. All the leading telecom companies have unveiled ambitious plans for their WiMax roll-outs. They include state- owned BSNL and MTNL, and private sector giants including Bharti Airtel, Tata Networks Communications, Idea Cellular, Reliance Communications, Aircel, and Sify. India is rapidly emerging as a major ‘hot spot’ for WiMax and WiFi networks, Tata Communications recently rolled out what is billed as one of the world’s thanks to growing laptop sales and rising broadband penetration. Leading largest commercial deployments of WiMax; it aims to cover 115 cities by KEEPING IN TOUCH: WiFi enables telecom fi rms to provide connectivity to remote areas telecommunication service providers are going in for nationwide roll-outs of 2009. The company has invested about $100 million in the project, which will be gear and services (excluding laptops, WiMax systems, reports Aradhana. raised to $500 million over the next four handsets, and chipsets) in India will top years as it approaches its target of having WiMax is the $890 million by 2011-12, at a 36 per cent 50 million subscribers in India. CAGR (compound annual growth rate) Says Prateek Pashine, in-charge of best solution for from 2008. the broadband and retail business at WiFi, which is also being used in rural Tata Communications: “We are strongly providing wireless areas, enables telecom fi rms to provide focusing on WiMax to provide last-mile broadband connectivity to remote areas, including access to our customers. -

Legislative Action 1995/1996 Legislative Session Assembly Committee on Utilities and Commerce

Golden Gate University School of Law GGU Law Digital Commons California Assembly California Documents 1996 Legislative Action 1995/1996 Legislative Session Assembly Committee on Utilities and Commerce Follow this and additional works at: http://digitalcommons.law.ggu.edu/caldocs_assembly Part of the Legislation Commons Recommended Citation Assembly Committee on Utilities and Commerce, "Legislative Action 1995/1996 Legislative Session" (1996). California Assembly. Paper 349. http://digitalcommons.law.ggu.edu/caldocs_assembly/349 This Committee Report is brought to you for free and open access by the California Documents at GGU Law Digital Commons. It has been accepted for inclusion in California Assembly by an authorized administrator of GGU Law Digital Commons. For more information, please contact [email protected]. Assembly Committee on Utilities and Commerce Legislative Action 1995/1996 Legislative Session CHAIRMAN: ASSEMBLYME}dBER MICKEY CONROY VICE cHAIRMAN: ASSEMBLYMEMBERSTBVE KUYKENDALL 060lA -TABLE OF CONTENTS- SECTIONS PAGE NUMBER Passed Assembly Measures ................................................................. 1 - 39 Passed Senate Measures ..................................................................... 40 - 77 Failed Assembly Measures .................................................................. 78 - 148 Failed Senate Measures ...................................................................... 149- 164 Assembly Bill 119 (Baca and Conroy) DESCRIPTION This bill would remove the requirement that the commission -

Digital Media: Rise of On-Demand Content 2 Contents

Digital Media: Rise of On-demand Content www.deloitte.com/in 2 Contents Foreword 04 Global Trends: Transition to On-Demand Content 05 Digital Media Landscape in India 08 On-demand Ecosystem in India 13 Prevalent On-Demand Content Monetization Models 15 On-Demand Content: Music Streaming 20 On-Demand Content: Video Streaming 28 Conclusion 34 Acknowledgements 35 References 36 3 Foreword Welcome to the Deloitte’s point of view about the rise key industry trends and developments in key sub-sectors. of On-demand Content consumption through digital In some cases, we seek to identify the drivers behind platforms in India. major inflection points and milestones while in others Deloitte’s aim with this point of view is to catalyze our intent is to explain fundamental challenges and discussions around significant developments that may roadblocks that might need due consideration. We also require companies or governments to respond. Deloitte aim to cover the different monetization methods that provides a view on what may happen, what could likely the players are experimenting with in the evolving Indian occur as a consequence, and the likely implications for digital content market in order to come up with the various types of ecosystem players. most optimal operating model. This publication is inspired by the huge opportunity Arguably, the bigger challenge in identification of the Hemant Joshi presented by on-demand content, especially digital future milestones about this evolving industry and audio and video in India. Our objective with this report ecosystem is not about forecasting what technologies is to analyze the key market trends in past, and expected or services will emerge or be enhanced, but in how they developments in the near to long-term future which will be adopted. -

Comparative Study of Public and Private Telecom Wireless Services in India

International Journal of Advanced Scientific Research and Management, Special Issue 5, April 2019 www.ijasrm.com ISSN 2455-6378 Comparative Study of Public And Private Telecom Wireless Services In India Neha Shrivastava S. R. K. University, Bhopal, (M.P.), India Abstract incremented from 209.13 million in March 2016 to India has seen fair share of both public and 272.76 million at the end of March 2017. As private players in telecom market and this research compared to 342.65 million as on 31st March 2016 paper aims in projecting a comparative study of both the internet subscriber base in the country stands at telecom wireless of public and private telecom 422.19 million on 31st March 2017. On the other wireless services providers like BhartiAirtel Limited, hand, the total broadband customer in the country Tata Communications Limited, Idea Cellular has enhanced to 276.52 million on March 2017 from Limited, Reliance Communications Limited, 149.75 million on March 2016. Vodafone India Limited and Bharat Sanchar Nigam The leading telecom service providers in India are as Limited (BSNL). The research presented in this follows:- paper is on the basis of secondary data which 1. BSNL: Indian state-owned telecom company includes data from last five year. headquartered in New Delhi, Bharat Sanchar Nigam Key Words:JIO, BSNL, Airtel, Vodafone, Idea, Limited (BSNL) was incorporated on 15 September Telecom, Wireless Services. 2000. It took over the business from the Central Government Departments of Telecom Services 1. Introduction: (DTS) and Telecom Operations (DTO) of providing The Indian telecom industry holds the of telecom services and network management with position of second largest telecom provider in the effect from 1 October 2000.