WT/TPR/S/362 • Niger

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Standard Project Report 2015

Standard Project Report 2015 Reporting Period: 1 January - 31 December 2015 NIGER Provision of Humanitarian Air Services in Niger Single Countr Niger Project Number 200792 2015 Project Category Single Country Special Operation .gif Project Approval Date 05 Jan 2015 Approved budget as 31 December 2015 in USD Planned Start Date 01 Jan 2015 Capacity Dev.t and Augmentation 13,773,595 Actual Start Date 01 Jan 2015 Direct Support Costs 1,499,375 Project End Date 31 Dec 2016 Indirect Support Costs 1,069,108 Financial Closure Date n.a. Total Approved Budget 16,342,078 Standard Project Report 2015 Niger Single Country Special Operation - 200792 Operational SPR TABLE OF CONTENTS COUNTRY OVERVIEW COUNTRY BACKGROUND SUMMARY OF WFP ASSISTANCE OPERATIONAL SPR OPERATIONAL OBJECTIVES AND RELEVANCE RESULTS 'Story Worth Telling' Outputs Outcomes Sustainability, Capacity Development and Handover MANAGEMENT Partnerships Lessons Learned Standard Project Report 2015 Niger Country Overview Country Overview NER.gif 2015 Niger Standard Project Report 2015 Niger Country Overview COUNTRY BACKGROUND Niger, a landlocked, low-income and food-deficit country, ranks last of 188 countries in the 2015 Human Development Index. The population of 19.1 million is predominantly rural; nominal per capita gross domestic product stands at USD 427, and 50.3 percent live on less than USD 1.90 per day. The population growth rate is 4 percent, with 50.4 percent under 15 years. Lack of infrastructure, limited coverage of basic social services, lack of safe water and sanitation, restricted production capacity, limited access to markets, gender disparities and the urban/ rural gap hinder development. Farming supports 80 percent of the population, but crop production is limited by poor rainfall, drought, crop diseases and land degradation. -

Niger Tenere’ E Carovane Di Sale Festival Dell’Air Di Iferouane E Rito Di Possessione Bori

NIGER TENERE’ E CAROVANE DI SALE FESTIVAL DELL’AIR DI IFEROUANE E RITO DI POSSESSIONE BORI Dall’11 al 25 Febbraio 2020 Un paese con un deserto che sembra non avere mai fine e dalle tante sfaccettature. Dalle lunghe dune del Teneré alla Falesia di Tiguidit, dalle montagne dell'Aïr alle saline di Bilma e Fachi, cambiano i colori, le forme, gli sguardi nei quali si riflette la grande dignità di genti povere e fiere che tengono testa al deserto con tradizioni ancora vive IMPEGNO: Medio con 1 volo aereo interno TIPOLOGIA: tribale, culturale, naturalistico, photo expert CON ACCOMPAGNATORE DALL’ITALIA "Tuttavia, abbiamo amato il deserto. All'inizio sembra fatto di nient'altro che di vuoto e silenzio; ma solo perché non si dà agli amanti di un giorno. Il deserto per noi era ciò che nasceva in noi. Ciò che noi apprendevamo su noi stessi" Antoine de Saint-Exupéry FOCUS DEL VIAGGIO • VIAGGIO NATURALISTICO Il deserto del Teneré (l'ultima propaggine dell'immenso Sahara) ora piatto ora con dune, spazi che sembrano non avere mai fine; il cratere di Arakao, anfiteatro di roccia nel deserto a forma di granchio; Adrar Madet, montagna rocciosa nel mezzo del deserto; saline di Bilma e Fachi, piccoli crateri di forma circolare • PHOTO Portrait, Street Life, Natura & Landscape, Travel Reportage, Animali • ANIMAL SPOTTING Addax (raro ungulato), gazzella dama, pecore Barbary, dromedari, ovini, asini, zebù, giraffe/Kourè • CULTURA Agadez patrimonio Unesco con il Palazzo del Sultano e la moschea; petroglifi Dabous Giraffes”; Niamey/museo; villaggi Tuareg dalle -

Objectif Afrique N° 172

N°172 SEPTEMBRE 2019 SOMMAIRE ACTUALITE REGIONALE CREDITS CONJONCTURE BANCAIRES : ENVIRONNEMENT DES AFFAIRES BAISSE DES TAUX PROJETS ET FINANCEMENTS DEBITEURS SECTEURS D’ACTIVITES EN 2018 AGRICULTURE ET AGROALIMENTAIRE DANS LA ZONE ENERGIE ET MATIERES PREMIERES UEMOA INDUSTRIE SERVICES ENTREPRISES CARNET ET AGENDA 9EME EDITION BENIN : BURKINA FASO NIGER : VERS DU FORUM POUR FERMETURE DE : LES FEMMES LA LA REVOLUTION LA FRONTIERE DU SECTEUR REINTEGRATION VERTE EN TERRESTRE MINIER DU NIGER A AFRIQUE AVEC LE BURKINABE A SOUTENUES PAR L’ITIE (AGRF) NIGERIA ACCRA LA FRANCE SENEGAL : TANZANIE : OUGANDA : RWANDA : L’ONU, EXTENSION DU LANCEMENT PARTENAIRE DU RESE AU ACCORD DU NOUVEAU PROCHAIN ELECTRIQUE VIA COMMERCIAL SYSTEME DE LE RECOURS AUX FORUM MONDIAL AVEC LA DE L’EAU AU RADAR EN INVESTISSEMENTS SENEGAL PRIVES CHINE TANZANIE Objectif Afrique n° 172 ACTUALITE REGIONALE Le Comité de politique monétaire (CPM) de la BCEAO maintient ses principaux taux directeurs inchangés Le CPM a décidé, le 4 septembre, de maintenir inchangés le taux d'intérêt minimum de soumission aux opérations d'appels d'offres d'injection de liquidité à 2,5% et le taux d'intérêt du guichet de prêt marginal à 4,5%. Le coefficient de réserves obligatoires applicable aux banques de l'Union demeure également fixé à 3%. Le Comité souligne par ailleurs que : (i) le dynamisme de l'activité économique dans l'Union s'est renforcé au T2 2019, (ii) le déficit budgétaire s’est atténué comparativement à la même période de l'année précédente et (iii) le niveau général des prix à la consommation a reculé de 0,3% par rapport au même trimestre de 2018. -

Plan De Réponse Humanitaire Niger

CYCLE DE PROGRAMMATION HUMANITAIRE PLAN DE RÉPONSE 2021 HUMANITAIRE PUBLIÉ EN FÉVRIER 2021 NIGER 01 PLAN DE RÉPONSE HUMANITAIRE 2021 A propos Pour consulter les mises à jour les plus récentes Ce document est consolidé par OCHA au nom de l'équipe humanitaire pays et des partenaires. Le Plan de réponse humanitaire est une présentation de la réponse stratégique OCHA coordonne l'action humanitaire pour garantir que les personnes touchées par la coordonnée conçue par les agences humanitaires pour répondre crise reçoivent l'assistance et la protection aux besoins urgents des personnes touchées par la crise. Il dont elles ont besoin. Il s'emploie à surmonter est basé sur les preuves des besoins décrits dans l'aperçu des les obstacles qui empêchent l'aide humani- taire d'atteindre les personnes touchées par besoins humanitaires et y répond. les crises et assure le leadership dans la mobilisation de l'aide et des ressources au PHOTO DE COUVERTURE nom du système humanitaire. Bénéficiaire de coupon alimentaire sur le site de distribution de Diffa. Photo : IRC https://www.unocha.org/niger https://twitter.com/OCHA_Niger Les désignations employées et la présentation des éléments dans le présent rapport ne signi- fient pas l’expression d’une quelque opinion que ce soit de la Partie du Secrétariat des Nations unies concernant le statut juridique d’un pays, d’un territoire, d’une ville ou d’une zone ou de leurs autorités ou concernant la délimitation de frontières ou de limites. Humanitarian Response vise à être le site Web central pour les outils et services de gestion de l'information, permettant l'échange d'informations entre les clusters et les membres de l'IASC opérant dans une crise prolongée ou soudaine. -

Steps Needed to Approve Budget Revisions

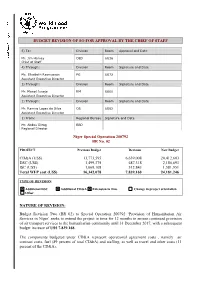

BUDGET REVISION OF SO FOR APPROVAL BY THE CHIEF OF STAFF 5) To: Division Room Approval and Date Mr. Jim Harvey OED 6G36 Chief of Staff 4) Through: Division Room Signature and Date Ms. Elisabeth Rasmusson PG 6G72 Assistant Executive Director 3) Through: Division Room Signature and Date Mr. Manoj Juneja RM 6G00 Assistant Executive Director 2) Through: Division Room Signature and Date Mr. Ramiro Lopes da Silva OS 6G62 Assistant Executive Director 1) From: Regional Bureau Signature and Date Mr. Abdou Dieng RBD Regional Director Niger Special Operation 200792 BR No. 02 PROJECT Previous Budget Revision New Budget CD&A (US$) 13,773,595 6,639,008 20,412,603 DSC (US$) 1,499,375 687,318 2,186,693 ISC (US$) 1,069,108 512,843 1,581,951 Total WFP cost (US$) 16,342,078 7,839,168 24,181,246 TYPE OF REVISION Additional DSC Additional CD&A Extension in time Change in project orientation Other NATURE OF REVISION: Budget Revision Two (BR 02) to Special Operation 200792 ‘Provision of Humanitarian Air Services in Niger’ seeks to extend the project in time for 12 months to ensure continued provision of air transport services to the humanitarian community until 31 December 2017, with a subsequent budget increase of US$ 7,839,168. The components budgeted under CD&A represent operational agreement costs , namely air contract costs, fuel (89 percent of total CD&A) and staffing, as well as travel and other costs (11 percent of the CD&A). BACKGROUND: 1. Niger remains the world’s poorest nation ranking 188th out of 188 in the United Nations Human Development Index1. -

Plan De Réponse Humanitaire NIGER PUBLIÉ EN FÉVRIER 2020 81

CYCLE DE PROGRAMME PLAN DE RÉPONSE HUMANITAIRE 2020 HUMANITAIRE PUBLIÉ EN FÉVRIER 2020 NIGER 1 PLAN DE RÉPONSE HUMANITAIRE 2020 Pour consulter les mises à jour les À propos plus récentes : Ce document est consolidé par OCHA pour le compte de l’Équipe humanitaire pays OCHA coordonne l’action humanitaire pour garantir et des partenaires humanitaires. Il présente les priorités et les paramètres de la que les personnes affectées par une crise reçoivent l’assistance et la protection dont elles ont besoin. réponse stratégique de l’Équipe humanitaire pays, basés sur une compréhension OCHA s’efforce de surmonter les obstacles partagée de la crise, énoncés dans l’Aperçu des besoins humanitaires. empêchant l’assistance humanitaire d'atteindre les Les désignations employées et la présentation des éléments dans le présent personnes affectées par des crises. En outre, OCHA rapport ne signifient pas l’expression de quelque opinion que ce soit de la part est chef de file dans la mobilisation de l’assistance et de ressources pour le compte du système du Secrétariat des Nations Unies concernant le statut juridique d’un pays, humanitaire. d’un territoire, d’une ville ou d’une zone ou de leurs autorités ou concernant la délimitation de frontières ou de limites. www.unocha.org/niger twitter.com/OCHA_Niger?lang=fr PHOTO DE COUVERTURE Personnes déplacées du site d'Awaridi, Diffa/Niger. Photo: OCHA/Niger, Décembre 2019 Humanitarian Response est destiné à être le site Web central des outils et des services de Gestion de l’information permettant l’échange d’informations entre les clusters et les membres de l’IASC intervenant dans une crise. -

Gerewol Etnie Bororo E Tuareg Il Deserto Del Tenere’

NIGER GEREWOL ETNIE BORORO E TUAREG IL DESERTO DEL TENERE’ GEREWOL – FANTASIA DI CAMMELLI DAL 9 AL 24 OTTOBRE 2021 IN 16 GIORNI/14 NOTTI • IMPEGNO ALTO • DURATA 16 GIORNI • VIAGGIO ETNICO, NATURALISTICO, CULTURALE, TRAVEL REPORTAGE, STREET LIFE, TURISMO ESPERIENZIALE, DESERT EXPERIENCE, PHOTO EXPERT • CAPO SPEDIZIONE LOCALE IN LINGUA ITALIANA In Niger ogni anno alla fine della stagione delle piogge i mandriani di bestiame Wodaabe, tradizionalmente nomadi, si riuniscono sul bordo meridionale del deserto del Sahara prima di disperdersi verso sud alla ricerca di pascoli nella stagione secca. E’ il Gerewol, incontro dei popoli nomadi, in cui trovano l’occasione ideale per celebrare nascite, trovare moglie, ricevere notizie. Nel corso dei festeggiamenti avviene una sorta di concorso di bellezza maschile (dove i ruoli sono invertiti rispetto a quelli occidentali) e tre delle donne più attraenti della tribù sono chiamate a giudicare il più bello, mentre gli uomini pretendenti si esibiscono in una danza Yake, muovendosi in cerchio ed esibendosi in base a determinati criteri: il portamento, la statura, il bianco degli occhi e dei denti, la voce. Per far risaltare questi elementi i Bororo si truccano con ocra ed adornano il capo con piume, mentre eseguono le danze tipiche della tradizione Fula. Alla fine viene eletto dalle donne il più bello, che sarà destinato a diventare il loro marito o il compagno di una notte. Ai margini di Agadez, antico crocevia di carovane e di popoli Tuareg, si susseguono sterminate cavalcate tra onde sabbiose spettacolari e il rincorrersi di dune che vanno all'assalto di castelli di roccia nel cuore dell' Aïr. -

Steps Needed to Approve Budget Revisions

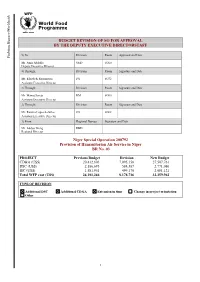

e d i w d l r o W r e g n u BUDGET REVISION OF SO FOR APPROVAL H g BY THE DEPUTY EXECUTIVE DIRECTORSTAFF n i t h g i 5) To: Division Room Approval and Date F Mr. Amir Abdulla OED 6G60 Deputy Executive Director 4) Through: Division Room Signature and Date Ms. Elisabeth Rasmusson PG 6G72 Assistant Executive Director 3) Through: Division Room Signature and Date Mr. Manoj Juneja RM 6G00 Assistant Executive Director 2) Through: Division Room Signature and Date Mr. Ramiro Lopes da Silva OS 6G62 Assistant Executive Director 1) From: Regional Bureau Signature and Date Mr. Abdou Dieng RBD Regional Director Niger Special Operation 200792 Provision of Humanitarian Air Service in Niger BR No. 03 PROJECT Previous Budget Revision New Budget CD&A (US$) 20,412,603 7,095,158 27,507,761 DSC (US$) 2,186,693 584,387 2,771,080 ISC (US$) 1,581,951 499,170 2,081,121 Total WFP cost (US$) 24,181,246 8,178,716 32,359,962 TYPE OF REVISION Additional DSC Additional CD&A Extension in time Change in project orientation Other 1 e d i w d l r o W r e g NATURE OF REVISION: n u H g 1. Budget Revision 03 to Special Operation 200792 ‘Provision of Humanitarian Air Services in n i t Niger’ takes into account the fact that WFP Niger has opted to continue operating under the h g i current project system in 2018 while transitioning to the CSP, which will be submitted in June F 2019. -

FAA Order JO 7340.2K Contractions

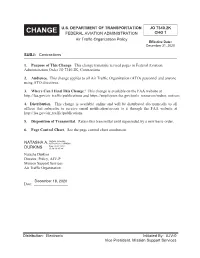

U.S. DEPARTMENT OF TRANSPORTATION JO 7340.2K CHANGE FEDERAL AVIATION ADMINISTRATION CHG 1 Air Traffic Organization Policy Effective Date: December 31, 2020 SUBJ: Contractions 1. Purpose of This Change. This change transmits revised pages to Federal Aviation Administration Order季JO季7340.2K, Contractions. 2. Audience. This change applies to all Air Traffic Organization (ATO) personnel and anyone using ATO directives. 3. Where Can I Find This Change? This change is available on the FAA website at http://faa.gov/air_traffic/publications and https://employees.faa.gov/tools_resources/orders_notices. 4. Distribution. This change is available online and will be distributed electronically to all offices that subscribe to receive email notification/access to it through the FAA website at http://faa.gov/air_traffic/publications. 5. Disposition of Transmittal. Retain this transmittal until superseded by a new basic order. 6. Page Control Chart. See the page control chart attachment. Digitally signed by NATASHA A. NATASHA A. DURKINS Date: 2020.12.18 DURKINS 15:49:13 -05'00' Natasha Durkins Director, Policy$-93 Mission Support Services Air Traffic Organization December 18, 2020 Date: __________________ Distribution: Electronic Initiated By: AJV-0 Vice President, Mission Support Services 12/31/20 JO 7340.2K CHG 1 PAGE CONTROL CHART Change 1 REMOVE PAGES DATED INSERT PAGES DATED CAM 1−1 through CAM 1−5 ............. 9/10/20 CAM 1−1 through CAM 1−3 ............ 12/31/20 3−1−1 through 3−4−1 ................... 9/10/20 3−1−1 through 3−4−1 .................. 12/31/20 Page Control Chart i 12/31/20 JO 7340.2K CHG 1 CHANGES, ADDITIONS AND MODIFICATIONS Chapter 3. -

Special Operation So 200792

WFP Niger SPECIAL OPERATION SO 200792 Country: Niger Type of project: Special Operation Title: Provision of Humanitarian Air Services in Niger Total cost (US$): US$ 7,867,513 Duration: 12 months (from 01 January 2015 to 31 December 2015) Executive Summary This Special Operation (SO) is established to provide safe, reliable, effective and efficient air transport services to the humanitarian community in Niger in 2015. Insecurity and poor infrastructure make land transportation impracticable for prompt implementation of humanitarian projects in Niger. As commercial airlines present in the country do not meet international standards, the United Nations Humanitarian Air Service (UNHAS) is vital for Non-Governmental Organizations (NGOs), United Nations (UN) agencies, donor representatives and Government counterparts to access project implementation sites. In 2015, UNHAS will provide services for approximately 165 humanitarian actors to at least eight destinations with a fleet of two aircraft. UNHAS Niger was established in 2008 and has since been essential to the overall humanitarian response in the country. The SO 200792 will be managed by the WFP Niger Country Office from 01 January 2015 to 31 December 2015 at a budgeted cost of US$ 7,867,513. The budget requirements will be raised through donor contributions (approximately 75%) and partial cost-recovery (25%) in the form of ticket sales. Fleet composition and operational routes have been determined after needs assessments and consultations with relevant stakeholders. The project will be regularly reviewed in accordance with standard procedures in order to minimize risks and ensure operational efficiency and effectiveness. Project Background 1. Niger is a landlocked, low-income and food-deficit country, ranking last out of the 187 countries in the Human Development Index1. -

Guide De L'observateur

REPUBLIQUE DU NIGER Fraternité - Travail - Progrès GUIDE DE L’OBSERVATEUR Commission Electorale Nationale Indépendante (CENI) ELECTIONS 2020-2021 -------------------------------------------------------------------------------------------------------------------------------------- Page 1 of 11 Rue ORTN, quartier Plateau, Commune I ** BP 13782 Niamey, Rép. du Niger Tél. : (227)20-33-03-86 / (227)20-33-04-67 ** www.ceniniger.org - [email protected] TABLE DES MATIERES PREAMBULE .......................................................................................................................................... 3 I. CONSIDERATIONS PRELIMINAIRES ............................................................................................ 4 1.1. PRESENTATION SOMMAIRE DE LA REPUBLIQUE DU NIGER ....................................... 4 1.2. LE CLIMAT ................................................................................................................................ 4 1.3. LA POPULATION ...................................................................................................................... 5 II. ORGANISATION ADMINISTRATIVE ............................................................................................ 5 III. ASPECTS SECURITAIRE ET SANITAIRE .................................................................................... 5 3.1. Aspect sécuritaire ........................................................................................................................ 5 3.2. Aspect sanitaire .......................................................................................................................... -

NIGER an Introduction to the Country Economy and the National Innovation System

COUNTRY OVERVIEW NIGER An Introduction to the Country Economy and the National Innovation System AID 11346 Emerging African Innovation Leaders G7 Exchange & Empowerment Program for enabling Innovation within the Next Production Revolution Work Package 1 in collaboration with COUNTRY OVERVIEW: NIGER An Introduction to the Country Economy and the National Innovation System This report describes Niger’s National Innovation System (NIS) under the lens of the Next Production Revolution (NPR). After summarizing the main characteristics of the country’s economy, it introduces the NIS players and institutions that are considered to sustain the diffusion of NPR technologies and business models across the main domestic industries. The report is primarily aimed at introducing all the members of the Emerging African Innovation Leaders project, including trainers and mentors, to the country’s economy, its potential for the NPR technologies and the NIS components that can foster the embracement of the NPR in Niger. The report content may also be of interest to local and international policymakers, enterprises and civil sector organizations that are working toward the NPR adoption in the country. The document was produced by Leonardo Rosciarelli between April and August 2018 as a researcher of Politecnico di Torino and the Energy Center Initiative. The report is part of a serie of six Country Overviews, which were designed and reviewed by the “Emerging African Innovation Leaders” research team composed by Pierluigi Leone and Leonardo Rosciarelli from Politecnico di Torino, and Emanuela Colombo, Paola Garrone, Andrea Gumina, Fabio Lamperti, Boris Mrkajic, Felipe Repetto, Nicolo’ Stevanato and Stefano Pistolese from Politecnico di Milano.