Expert Commentary GECF Member Countries Shifting Towards Less Carbon Intensity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Case M.9837 — BP/Sinopec Fuel Oil Sales/BP Sinopec Marine Fuels) Candidate Case for Simplified Procedure

C 6/16 EN Offi cial Jour nal of the European Union 8.1.2021 Prior notification of a concentration (Case M.9837 — BP/Sinopec Fuel Oil Sales/BP Sinopec Marine Fuels) Candidate case for simplified procedure (Text with EEA relevance) (2021/C 6/13) 1. On 22 December 2020, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — BP Plc. (United Kingdom), — Sinopec Fuel Oil Sales Co. Ltd (People’s Republic of China), controlled by China Petrochemical Corporation (People’s Republic of China), — BP Sinopec Marine Fuels Pte. Ltd. BP Plc. and Sinopec Fuel Oil Sales Co. Ltd acquire within the meaning of Article 3(1)(b) and 3(4) of the Merger Regulation joint control of BP Sinopec Marine Fuels Pte. Ltd. The concentration is accomplished by way of contract. 2. The business activities of the undertakings concerned are: — for BP Plc.: exploration, production and marketing of crude oil and natural gas; refining, marketing, supply and transportation of petroleum products; production and supply of petrochemicals and related products; and supply of alternative energy, — for Sinopec Fuel Oil Sales Co. Ltd: providing oil products and service to domestic and international trading vessels, — BP Sinopec Marine Fuels Pte. Ltd: wholesale and retail supply of bunker fuels in Europe, Asia and the Middle East. 3. On preliminary examination, the Commission finds that the notified transaction could fall within the scope of the Merger Regulation. However, the final decision on this point is reserved. Pursuant to the Commission Notice on a simplified procedure for treatment of certain concentrations under the Council Regulation (EC) No 139/2004 (2) it should be noted that this case is a candidate for treatment under the procedure set out in the Notice. -

Patronage of Vladimir Putin

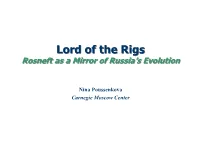

LLorord of the d of the RiRigsgs RosRosnenefftt a as s a a MMiirrrror oor off Rus Russisia’sa’s Ev Evololututiionon Nina Poussenkova Carnegie Moscow Center PortPortrraiaitt of of RosneRosneft ft E&P Refining Marketing Projects Yuganskneftegas Komsomolsk Purneftegas Altainefteproduct Sakhalin 3, 4, 5 Sakhalinmorneftegas Tuapse Kurgannefteproduct Vankor block of fields Severnaya Neft Yamalnefteproduct West Kamchatka shelf Polar Lights Nakhodkanefteproduct Black and Azov Seas Sakhalin1 Vostoknefteproduct Kazakhstan Vankorneft Arkhangelsknefteproduct Algiers Krasnodarneftegas Murmansknefteproduct CPC Stavropolneftegas Smolensknefteproduct VostochnoSugdinsk block Grozneft Artag Verkhnechonsk KabardinoBalkar Fuel Co Neftegas Karachayevo Udmurtneft Cherkessknefteproduct Kubannefteproduct Tuapsenefteproduct Stavropoliye ExYuganskneftegas: 2004 oil production (21 mt) – 4.7% of Russia’s total CEO – S.Bogdanchikov BoD Chairman – I.Sechin Proved oil reserves – 4.8% of Russia’s total With Yuganskneftegas: > 75% owned by the state Rosneftegas 2006 oil production (75 mt) – 15% of Russia’s total 9.44% YUKOS >14% sold during IPO Proved oil reserves – 20% of Russia’s total RoRosnesneftft’s’s Saga Saga 1985 1990 1992 1995 2000 2005 2015 KomiTEK Sibneft LUKOIL The next ONACO target ??? Surgut TNK Udmurtneft The USSR Slavneft Ministry of Rosneftegas the Oil Rosneft Rosneft Rosneft Rosneft Rosneft Industry 12 mt 240 mt 20 mt 460 mt 75 mt 595 mt VNK 135 mt Milestones: SIDANCO 1992 – start of privatization Severnaya Neft 1998 – appointment of S.Bogdanchikov -

Sinopec Oilfield Service Corporation

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this announcement, makes no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Sinopec Oilfield Service Corporation (a joint stock limited company established in the People’s Republic of China) (Stock code: 1033) Proposed Election of the Directors of the 10th Session of the Board and the Non-employee Representative Supervisors of the 10th Session of the Supervisory Committee The tenure of office of the ninth session of the board of directors and the supervisory committee of Sinopec Oilfield Service Corporation (the “Company”) will soon expire. The board of directors (the “Board”) of the Company announces that: 1. The following candidates are proposed to be elected as the directors (not include independent non-executive directors) of the 10th Session of the Board: Mr. Chen Xikun Mr. Yuan Jianqiang Mr. Lu Baoping Mr. Fan Zhonghai Mr. Wei Ran Mr. Zhou Meiyun 2. The following candidates are proposed to be elected as the independent non-executive directors of the 10th Session of the Board: Mr. Chen Weidong Mr. Dong Xiucheng Mr. Zheng Weijun 1 3. The following candidates are proposed to be elected as the non-employees representative supervisors of the 10th Session of the Supervisory Committee of the Company (the "Supervisory Committee"): Mr. Ma Xiang Mr. Du Jiangbo Ms. Zhang Qin Mr. Zhang Jianbo The information of each of the above proposed candidates for directors of the Company (the "Director") and the non-employee representative supervisors of the Company (the " Non-employee Representative Supervisor") is set out below: Information of the Proposed Directors (1) Mr. -

Process Technologies and Projects for Biolpg

energies Review Process Technologies and Projects for BioLPG Eric Johnson Atlantic Consulting, 8136 Gattikon, Switzerland; [email protected]; Tel.: +41-44-772-1079 Received: 8 December 2018; Accepted: 9 January 2019; Published: 15 January 2019 Abstract: Liquified petroleum gas (LPG)—currently consumed at some 300 million tonnes per year—consists of propane, butane, or a mixture of the two. Most of the world’s LPG is fossil, but recently, BioLPG has been commercialized as well. This paper reviews all possible synthesis routes to BioLPG: conventional chemical processes, biological processes, advanced chemical processes, and other. Processes are described, and projects are documented as of early 2018. The paper was compiled through an extensive literature review and a series of interviews with participants and stakeholders. Only one process is already commercial: hydrotreatment of bio-oils. Another, fermentation of sugars, has reached demonstration scale. The process with the largest potential for volume is gaseous conversion and synthesis of two feedstocks, cellulosics or organic wastes. In most cases, BioLPG is produced as a byproduct, i.e., a minor output of a multi-product process. BioLPG’s proportion of output varies according to detailed process design: for example, the advanced chemical processes can produce BioLPG at anywhere from 0–10% of output. All these processes and projects will be of interest to researchers, developers and LPG producers/marketers. Keywords: Liquified petroleum gas (LPG); BioLPG; biofuels; process technologies; alternative fuels 1. Introduction Liquified petroleum gas (LPG) is a major fuel for heating and transport, with a current global market of around 300 million tonnes per year. -

Analiza Efikasnosti Naftnih Kompanija U Srbiji Efficency Analysis of Oil Companies in Serbia

________________________________________________________________________ 79 Analiza efikasnosti naftnih kompanija u Srbiji Efficency Analysis of Oil Companies in Serbia prof. dr. sc. Radojko Lukić Ekonomski fakultet u Beogradu [email protected] Ključne reči: ekspolatacija sirove nafte i gasa, Abstract tržišno učešće, efikasnost poslovanja, financijske Lately, significant attention has been paid to the performanse, održivo izveštavanje evolution of the performance of oil companies around Key words: exploration of crude oil and gas, market the world, by individual regions and countries. Bearing share, business efficiency, financial performance, susta- this in mind, relying on the existing theoretical and inable reporting methodological and empirical results, this paper analyzes the efficiency of operations, financial perfor- mance and sustainable reporting of oil companies in Sažetak Serbia, with special emphasis on the Petroleum Industry of Serbia (NIS). The results of the survey show signifi- U poslednje vreme značajna se pažnja poklanja cant role of mining, i.e. oil companies in creating addi- evoluaciji performansi naftnih kompanija u svetu, tional value of the entire economy of Serbia. Concer- po pojedinim regionima i zemljama. Imajući to u ning the Petroleum Industry of Serbia, it has a signi- vidu, oslanjajući se na postojeće teorijsko-metodo- ficant place in the production and trade of petroleum loške i empirijske rezultate, u ovom radu se analizi- products in Serbia. For these reasons, the efficiency of raju efikasnosti poslovanja, finansijske performanse operations, financial performance and maintenance of i održivo izveštavanje naftnih kompanija u Srbiji, s the Petroleum Industry of Serbia has been complexly posebnim osvrtom na Naftnu industriju Srbije (NIS). analyzed. In this respect, according to many indicators, Rezultati istraživanja pokazuju značajnu ulogu rudar- it is at a satisfactory level in relation to the average of the stva, odnosno naftnih kompanija u kreiranju dodatne world’s leading oil companies. -

The Annual World Petroleum & Petrochemical Event

The Annual World Petroleum & Petrochemical Event The largest private exhibition company in China Top 10 Exhibition Companies in China Top 10 Influential Companies in China Exhibition Industry Vice-president Unit of China Convention and Exhibition Society Vice-chairman Unit of Exhibition Committee of China Chamber of International Commerce Zhenwei Exhibition, founded in 2000 and listed on New Three Board market on November 24, 2015 (innovation-layer enterprise, The significantly influential exhibitions held by Zhenwei Exhibition stock code: 834316), is the largest private exhibition company in China, one of the earliest Chinese members of UFI (Union of China International Petroleum & Petrochemical Technology and Equipment Exhibition (cippe) International Fairs), and vice-president unit of China Convention and Exhibition Society. Zhenwei Exhibition has developed into China (Tianjin) International Industrial Expo (CIEX) the industry-leading comprehensive service provider of global exhibition focusing on convention and exhibition and integrating exhibition & convention, digital information and e-commerce. Tianjin International Robot Exhibition (CIRE) Shanghai International New Energy Vehicle Industry Expo (NEVE) Headquartered in Binhai New Area, Tianjin and owns Tianjin Zhenwei, Beijing Zhenwei, Guangzhou Zhenwei, Xinjiang Zhenwei, Xi'an Zhenwei, Chengdu Zhenwei and Beijing Zhongzhuang Runda Exhibition. In 2015, Zhenwei Exihibition and Xinjiang China International Electric Vehicle Supply Equipments Fair (EVSE) International Expo Administration -

Foreign Investment in the Oil Sands and British Columbia Shale Gas

Canadian Energy Research Institute Foreign Investment in the Oil Sands and British Columbia Shale Gas Jon Rozhon March 2012 Relevant • Independent • Objective Foreign Investment in the Oil Sands and British Columbia Shale Gas 1 Foreign Investment in the Oil Sands There has been a steady flow of foreign investment into the oil sands industry over the past decade in terms of merger and acquisition (M&A) activity. Out of a total CDN$61.5 billion in M&A’s, approximately half – or CDN$30.3 billion – involved foreign companies taking an ownership stake. These funds were invested in in situ projects, integrated projects, and land leases. As indicated in Figure 1, US and Chinese companies made the most concerted efforts to increase their profile in the oil sands, investing 2/3 of all foreign capital. The US and China both invested in a total of seven different projects. The French company, Total SA, has also spread its capital around several projects (four in total) while Royal Dutch Shell (UK), Statoil (Norway), and PTT (Thailand) each opted to take large positions in one project each. Table 1 provides a list of all foreign investments in the oil sands since 2004. Figure 1: Total Oil Sands Foreign Investment since 2003, Country of Origin Korea 1% Thailand Norway 6% UK 7% 2% US France 33% 18% China 33% Source: Canoils. Foreign Investment in the Oil Sands and British Columbia Shale Gas 2 Table 1: Oil Sands Foreign Investment Deals Year Country Acquirer Brief Description Total Acquisition Cost (000) 2012 China PetroChina 40% interest in MacKay River 680,000 project from AOSC 2011 China China National Offshore Acquisition of OPTI Canada 1,906,461 Oil Corporation 2010 France Total SA Alliance with Suncor. -

Media Release Chevron Lummus Global LLC Sinopec Selects UFR

Media Release Sinopec selects UFR technology from Chevron Lummus Global for its Qingdao Refinery Richmond, CA, March, 2005 – Sinopec Qingdao Refining & Chemical Co., Ltd. signed a license agreement with Chevron Lummus Global LLC (CLG) for applying UpFlow Reactor (UFR) technology to the new resid hydrotreating plant. The 2.6 million ton per year (TPA) resid hydrotreating plant is part of a 10 million TPA grassroots refinery to be located in Qingdao, China. Sinopec plans to start the unit up by the second quarter of 2008. Sinopec’s Senior Vice President, Mr. Cao Xianghong, commented at the signing ceremony in Beijing that “The signing for introducing UFR technology shows both parties have gone ahead another step for the existing good relationship between Sinopec and CLG.” CLG’s Joint Managing Director, Dr. Mal Maddock, stated that “In resid hydroprocessing, this is the second unit adopting CLG’s UFR technology by Sinopec, after the successful application of CLG’s VRDS and UFR technologies in Sinopec Qilu. We view this as a very strategic award and hope to use it as a springboard for future broader cooperation with Sinopec on resid hydroprocessing and other technology areas, such as lube hydroprocessing and hydrocracking.” Chevron Lummus Global LLC M. B. Principe Postal Address: Telephone: Telefax: 1515 Broad Street 973-893-2953 973-893-2412 Bloomfield, NJ 07003 Page 2 CLG will provide a reactor design package, follow-up technical support during the detailed engineering design, training prior to start-up, and start-up support during the commissioning of UFR and the guarantee test run. CLG's state-of-the-art UFR technology has a lower initial pressure drop than a typical downflow guard reactor. -

Big Oil's Oily Grasp

Big Oil’s Oily Grasp The making of Canada as a Petro-State and how oil money is corrupting Canadian politics Daniel Cayley-Daoust and Richard Girard Polaris Institute December 2012 The Polaris Institute is a public interest research organization based in Canada. Since 1997 Polaris has been dedicated to developing tools and strategies to take action on major public policy issues, including the corporate power that lies behind public policy making, on issues of energy security, water rights, climate change, green economy and global trade. Polaris Institute 180 Metcalfe Street, Suite 500 Ottawa, ON K2P 1P5 Phone: 613-237-1717 Fax: 613-237-3359 Email: [email protected] www.polarisinstitute.org Cover image by Malkolm Boothroyd Table of Contents Introduction 1 1. Corporations and Industry Associations 3 2. Lobby Firms and Consultant Lobbyists 7 3. Transparency 9 4. Conclusion 11 Appendices Appendix A, Companies ranked by Revenue 13 Appendix B, Companies ranked by # of Communications 15 Appendix C, Industry Associations ranked by # of Communications 16 Appendix D, Consultant lobby firms and companies represented 17 Appendix E, List of individual petroleum industry consultant Lobbyists 18 Appendix F, Recurring topics from communications reports 21 References 22 ii Glossary of Acronyms AANDC Aboriginal Affairs and Northern Development Canada CAN Climate Action Network CAPP Canadian Association of Petroleum Producers CEAA Canadian Environmental Assessment Act CEPA Canadian Energy Pipelines Association CGA Canadian Gas Association DPOH -

THE ROLE of CHINA in BRAZILIAN OIL and GAS INDUSTRY Prof

THE ROLE OF CHINA IN BRAZILIAN OIL AND GAS INDUSTRY Prof. Edmar de Almeida Energy Economics Group Institute of Economics Federal University of Rio de Janeiro FIESP–LETS, São Paulo, 20 May 2014 PLAN OF THE PRESENTATION ►Introduction ►Chinese participation in Brazilian oil and gas industry ►Chinese direct investment in Brazilian oil and gas ►Chinese oil-for-loan in Brazil ►Bilateral cooperation for trade and investment ►Conclusion: future role of China in Brazil oil and gas 2 INTRODUCTION ► Brazil is a latecomer for Chinese trade and investment: the country was not an important target for Chinese oil companies internationalization until recently ► The Presalt discovery positioned Brazil as an important opportunity for Chinese internationalization ► As Chinese companies familiarize with Brazil, they tend to identify new business opportunities ► Brazil’s dependence on Chinese investment and trade tends to increase 3 Chinese Participation in Brazilian Oil and Gas Industry 4 CHINESE PARTICIPATION IN BRAZILIAN OIL AND GAS INDUSTRY ► Until 2005, Chinese presence in Brazilian oil and gas was very timid ► 2005: Sinopec enters the Brazilian market offering engineering and EPC services, participating in the GASENE Project ► 2009: Petrobras borrows 10 billion dollars from Chinese Development Bank to be repaid with oil exports ► 2010: − Presal Discovery drives Sinopec to acquire stakes in Galp and Repsol − Sinochem start to explore in Brazil ► 2013: China National Petroleum Corporation (CNPC) e China National Offshore Oil Corporation (CNOOC) win 10% -

Renewable Energy in the GCC Countries Resources, Potential, and Prospects

Renewable Energy in the GCC Countries Resources, Potential, and Prospects Renewable Energy in the GCC Countries Resources, Potential, and Prospects Imen Jeridi Bachellerie Gulf Research Center The cover image shows the Beam Down Pilot Project at Masdar City. Photo Credit: Masdar City Gulf Research Center E-mail: [email protected] Website: www.grc.net First published March 2012 Gulf Research Center © Gulf Research Center 2012 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of the Gulf Research Center. ISBN: 978-9948-490-05-0 The opinions expressed in this publication are those of the author alone and do not necessarily state or reflect the opinions or position of the Gulf Research Center or the Friedrich-Ebert-Stiftung. By publishing this volume, the Gulf Research Center (GRC) seeks to contribute to the enrichment of the reader’s knowledge out of the Center’s strong conviction that ‘knowledge is for all.’ Dr. Abdulaziz O. Sager Chairman Gulf Research Center About the Gulf Research Center The Gulf Research Center (GRC) is an independent research institute founded in July 2000 by Dr. Abdulaziz Sager, a Saudi businessman, who realized, in a world of rapid political, social and economic change, the importance of pursuing politically neutral and academically sound research about the Gulf region and disseminating the knowledge obtained as widely as possible. The Center is a non-partisan think-tank, education service provider and consultancy specializing in the Gulf region. -

10Th Volume, No

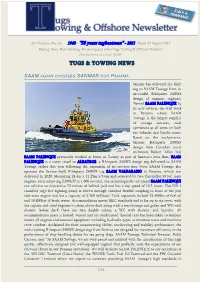

22nd Volume, No. 66 1963 – “58 years tugboatman” - 2021 Dated 22 August 2021 Buying, Sales, New building, Renaming and other Tugs Towing & Offshore Industry Distribution twice a week 18,600+ TUGS & TOWING NEWS SAAM AGAIN CHOOSES SANMAR FOR PANAMA Sanmar has delivered the third tug to SAAM Towage from its successful RAmparts 2400SX design of compact tugboats. Named SAAM PALENQUE by its new owners, she will work in Panama where SAAM Towage is the largest supplier of towage services, with operations at all ports on both the Atlantic and Pacific coasts. Based on the exclusive-to- Sanmar RAmparts 2400SX design from Canadian naval architects Robert Allan Ltd, SAAM PALENQUE previously worked at Izmir in Turkey as part of Sanmar’s own fleet. SAAM PALENQUE is a sister vessel to ALBATROS, a RAmparts 2400SX design tug delivered to SAAM Towage earlier this year following the expansion of its services into Peru. SAAM Towage also operates the Sanmar-built RAmparts 2400SX tug SAAM VALPARAISO in Panama, which was delivered in 2020. Measuring 24.4m x 11.25m x 5.6m and powered by two Caterpillar 3516C main engines, each achieving 2,100kW at 1,600 rev/min, the technologically-advanced SAAM PALENQUE can achieve an impressive 72 tonnes of bollard pull and has a top speed of 12.5 knots. The FiFi 1 classified tug’s fire-fighting pump is driven through clutched flexible coupling in front of the port side main engine and has a capacity of 2,700 m3/hour. Tank capacities include 72,400ltrs of fuel oil and 10,800ltrs of fresh water.