Economic Impact Assessment of a Single Sky Agreement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Raptor and Human – Symbolism on Diverse Continents and in Diverse Settings

11 edited bythe ZBSA and history of hunting of and history Advanced studies on the archaeology archaeology the on studies Advanced 11 11 Advanced studies on the archaeology and history of hunting edited by the ZBSA Falconry, the art of hunting with birds (Frederick II) and a living human heritage (UNESCO), has left many traces, from western Europe and northern Africa to Japan. The oldest ascertained testimonies Karl-Heinz Gersmann ∙ Oliver Grimm (eds.) belong to the first millennium BCE. The present book, a cooperation between falconers and scientists from different branches, addresses falconry and bird Raptor and human – symbolism on diverse continents and in diverse settings. falconry and bird symbolism throughout the millennia on a global scale ISBN 978-3-529-01490-1 9 783529 014901 (eds.) Grimm ∙ Oliver Gersmann Karl-Heinz symbolism bird and – falconry human and Raptor Raptor and human – falconry and bird symbolism throughout the millennia on a global scale Advanced studies on the archaeology and history of hunting, vol. 1.1–1.4 Edited by the ZBSA/Centre for Baltic and Scandinavian Archaeology in the Foundation of the Schleswig-Holstein State Museums, Schloss Gottorf, Schleswig (northern Germany) Raptor and human – falconry and bird symbolism throughout the millennia on a global scale 1 3 Edited by Karl-Heinz Gersmann and Oliver Grimm Publication in considerable extension of the workshop at the Centre for Baltic and Scandinavian Archaeology (ZBSA) in Schleswig, March 5th to 7th 2014 Cover picture: Skilled eagle master. Western Mongolia, August 2011 (photo used with the permission of Dr. Takuya Soma). Top to the left: Seal of the Danish king Knud IV (late 11th century). -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Liste-Exploitants-Aeronefs.Pdf

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX C(2009) XXX final COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) EN EN COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE COMMISSION OF THE EUROPEAN COMMUNITIES, Having regard to the Treaty establishing the European Community, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC1, and in particular Article 18a(3)(a) thereof, Whereas: (1) Directive 2003/87/EC, as amended by Directive 2008/101/EC2, includes aviation activities within the scheme for greenhouse gas emission allowance trading within the Community (hereinafter the "Community scheme"). (2) In order to reduce the administrative burden on aircraft operators, Directive 2003/87/EC provides for one Member State to be responsible for each aircraft operator. Article 18a(1) and (2) of Directive 2003/87/EC contains the provisions governing the assignment of each aircraft operator to its administering Member State. The list of aircraft operators and their administering Member States (hereinafter "the list") should ensure that each operator knows which Member State it will be regulated by and that Member States are clear on which operators they should regulate. -

Towards a Green Economy in Jordan

Towards a Green Eco nomy in Jordan A SCOPING STUDY August 2011 Study commissioned by The United Nations Environment Programme In partnership with The Ministry of Environment of Jordan Authored by Envision Consulting Group (EnConsult) Jordan Towards a Green Economy in Jordan ii Contents 1. Executive Summary ...................................................................................................... vii 2. Introduction ....................................................................................................................... 1 2.1 Objective of the Study ................................................................................................... 1 2.2 Green Economy Definition ........................................................................................... 1 2.3 Jordanian Government Commitment to Green Economy .................................... 1 3. Overarching Challenges for the Jordanian Economy............................................ 2 3.1 Unemployment ................................................................................................................. 2 3.2 Energy Security ............................................................................................................... 3 3.3 Resource Endowment and Use ................................................................................... 5 4. Key Sectors Identified for Greening the Economy ................................................. 7 4.1 Energy .................................................................................................................. -

A Critical Conceptualisation of Leadership and Organisational

A Critical Conceptualisation of Leadership And Organisational Change: The Case of Royal Jordanian Airline By Basil Obeidat Director of Studies: Dr Tom Baum Supervisor: Dr Austin Chakaodza 2020 Dedication Dedication My wife and children are dear to me. They have supported my ambition to become a qualified researcher. I am grateful for all their love and support. i | Page Acknowledgements Acknowledgements This research work has been possible with the expert direction and support provided by my Director of Studies Professor Tom Baum. Dr Austin Chakaodza provided the know-how guidance necessary to undertake PhD level research. I am grateful to them both, thank you. I should mention Professor Don Harper and Sheku Fofanah and the PhD Administration team who guided me through all the paperwork. ii | Page Abstract Abstract This present thesis is based on the critical conceptualisation of the leadership and the organisational change. Leadership is an action of the leading group of the people and company. It is a practical skill and research area that encompassing the ability of a person or company to lead other people in, team and firm. The organisational change is about the procedure of changing processes, culture, strategies and technologies of the company. It is a process under which a company make changes in its working methods and aim effectively, investigating the leadership style of the top management executives, including the Chief Executive Officer of Royal Jordanian airline to understand the factors that influence organisational cultural change within the company. There have been few studies of the Middle-Eastern situation that treats organisational cultural change in the development of an organisation in terms of the values of the company. -

MIDRMA Board/13-WP/6 3/03/2014 International Civil Aviation

MIDRMA Board/13-WP/6 3/03/2014 International Civil Aviation Organization Middle East Regional Monitoring Agency Board Thirteenth Meeting (MIDRMA Board/13) (Bahrain, 9 –12 March 2014) Agenda Item 4: RVSM Monitoring and Related Technical Issues MID STATES MINIMUM MONITORING REQUIREMENTS (Presented by MIDRMA) SUMMARY The aim of this working paper is to address the RVSM Minimum Monitoring Requirements (MMR) applicable for each MIDRMA Member State. Action by the meeting is at paragraph 3. REFERENCES − ATM/AIM/SAR SG/13 Report − ICAO Doc 9547 − ICAO doc 9937 − ICAO Annex 6 Part I − MIDANPIRG/14 Report − MID RVSM SMR 2012-2013 1. INTRODUCTION 1.1 The height-keeping performance of aircraft is a key element in ensuring the safe operations of RVSM airspace. The RVSM height monitoring standards are considered the minimum requirement needed to maintain the safety of operations in the RVSM designated airspace. 1.2 Upon changes to ICAO Annex 6, Operation of Aircraft, Parts I & II, applicable on 18 November 2010, the following standard was adopted by the International Civil Aviation Organization (ICAO): 7.2.7 The State of the Operator that has issued an RVSM approval to an operator shall establish a requirement which ensures that a minimum of two aeroplanes of each aircraft type grouping of the operator have their height-keeping performance monitored, at least once every two years or within intervals of 1000 flight hours per aeroplane, whichever period is longer. If an operator aircraft type grouping consists of a single aeroplane, monitoring of that aeroplane shall be accomplished within the specified period. -

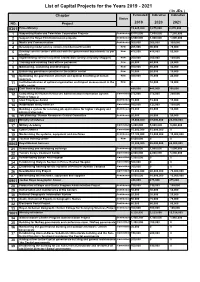

List of Capital Projects for the Years 2019 - 2021 ( in Jds ) Chapter Estimated Indicative Indicative Status NO

List of Capital Projects for the Years 2019 - 2021 ( In JDs ) Chapter Estimated Indicative Indicative Status NO. Project 2019 2020 2021 0301 Prime Ministry 13,625,000 9,875,000 8,870,000 1 Supporting Radio and Television Corporation Projects Continuous 8,515,000 7,650,000 7,250,000 2 Support the Royal Film Commission projects Continuous 3,500,000 1,000,000 1,000,000 3 Media and Communication Continuous 300,000 300,000 300,000 4 Developing model service centers (middle/nourth/south) New 205,000 90,000 70,000 5 Develop service centers affiliated with the government departments as per New 475,000 415,000 50,000 priorities 6 Implementing service recipients satisfaction surveys (mystery shopper) New 200,000 200,000 100,000 7 Training and enabling front offices personnel New 20,000 40,000 20,000 8 Maintaining, sustaining and developing New 100,000 80,000 40,000 9 Enhancing governance practice in the publuc sector New 10,000 20,000 10,000 10 Optimizing the government structure and optimal benefiting of human New 300,000 70,000 20,000 resources 11 Institutionalization of optimal organization and impact measurement in the New 0 10,000 10,000 public sector 0601 Civil Service Bureau 485,000 445,000 395,000 12 Completing the Human Resources Administration Information System Committed 275,000 275,000 250,000 Project/ Stage 2 13 Ideal Employee Award Continuous 15,000 15,000 15,000 14 Automation and E-services Committed 160,000 125,000 100,000 15 Building a system for receiving job applications for higher category and Continuous 15,000 10,000 10,000 administrative jobs. -

Anciexpo 2 0 0 7 Quaderno Tecnico Espositori

Q U A D E R N O T E C N I C O E S P O S I T O R I Bari, Fiera del Levante AAANNNCCCIII EEEXXXPPPOOO ‘‘‘000777 222444^^^ AAAsssssseeemmmbbbllleeeaaa AAAnnnnnnuuuaaallleee AAANNNCCCIII 20-21-22 giugno 2007 AAA NNN CCC III EEE XXX PPP OOO 222 000 000 777 QQQ UUU AAA DDD EEE RRR NNN OOO TTT EEE CCC NNN III CCC OOO EEE SSS PPP OOO SSS III TTT OOO RRR III Sede della Manifestazione BARI, Fiera del Levante Ingresso EDILIZIA Indirizzo Via di Maratona – 70123 BARI telefono 080.5366393 - www.fieradellevante.it Data 20/22 giugno 2007 Orari dalle 9.00 alle 19.00 (l’ingresso agli espositori è permesso un’ora prima dell’apertura della Manifestazione) Informazioni Utili STAZIONE FFSS Stazione di Bari Centrale www.trenitalia.it – call center trenitalia 892021 Aeroporto di Bari Palese “Karol Wojtyla” www.seap-puglia.it – centralino 080 5800200 COLLEGAMENTI collegamento con centro città ogni ora con autobus AMTAB n. 16 AEREI compagnie che servono l’aeroporto dalle principali città italiane: ALITALIA - AIR ONE – VOLARE WEB – BLU EXPRESS – ALPI EAGLES - EUROFLY - MYAIR A14 - uscita autostradale BARI NORD (per chi proviene da Nord) COLLEGAMENTI o uscita autostradale BARI SUD (per chi proviene da Sud) e AUTOSTRADALI seguire le indicazioni per la FIERA AMTAB - Azienda Municipalizzata Trasporti Autofiloviari Baresi SERVIZIO AUTOBUS www.amtabservizio.it Cooperativa Radiotaxi (attiva 24 ore su 24) RADIO TAXI tel. 080.5543333 - www.radiotaxibari.it HERTZ – www.hertz.it AUTONOLEGGI AVIS – www.avisautonoleggio.it SIXT – www.sixt.it MAGGIORE – www.maggiore.it SIAE DI SIAE sede di BARI COMPETENZA Corso Vittorio Emanuele, 20/a - 70122 Bari Tel. -

Queen Alia International Airport 1

Queen Alia International Airport st 1 Quarter Report 2013 Executive Summary: Positive momentum had carried through 2012 over Q1 2013 in terms of PAX, ACM and CFMs. Despite the political unrest throughout the region, AMM witnessed continuous. Moreover; AIG constantly monitors the economical and external environment changes, and their possible effect on traffic (positive/negative). • PAX: Q1 2013 had witnessed a growth of 5.56% recording 1,472,524 PAX comparing to 1,395,008 PAX recorded during the same period last year. • ACM: Q1 2013 had witnessed a growth of 3.56% recording 15,921 movements comparing to 15,373 movements recorded during the same period last year. • CFMs (Cargo): Q1 2013 had witnessed a growth of 2.97% handling 22,244 Tons comparing to 21,603 Tons handled during the same period last year. On the Routes & Network development side, positive momentum has been witnessed through Q1 2013, with additional new services, carriers and frequencies added/announced briefed on the Below table. Page 1 of 7 Queen Alia International Airport st 1 Quarter Report 2013 The below chart represents our top 15 destinations in traffic movements. Within QAIA destinations network, our most significant markets were DXB, JED, BEY, CAI and RUH collectively having ~ 543,528 PAX which is 37% of the traffic travelling in both directions. In terms of the broader market (outside the Mena), the most significant markets were IST, (BKK/KUL/HKG) and LHR collectively having ~ 145,962 PAX which is 10% of the traffic travelling in both directions. In terms of ACM, the top 5 airlines sorted in descending order were Royal Jordanian, Egypt Air, Turkish Airlines, Gulf Air and Royal Falcon. -

Entry Regulations to Jordan

Entry Regulations to Jordan Dear Trade Partners Greetings from Royal Jordanian Airlines. As received from Jordan Civil Aviation Regulatory Commission (JCARC), effective 09th of March 2021 and until 24th of March 2021 midnight, International scheduled flights are allowed to operate from/to Jordanian airports. Accordingly, the following to be applied on inbound flights: • Airlines are responsible to ensure that before boarding each passenger has negative PCR test conducted within 72 hours prior to the departure from the first embarkation airport, health insurance for Non-Jordanians, and install (AMAN Mobile App.). • Military passengers and their families are required to visit https://gateway2jordan.gov.jo to complete the required form and obtain the QR code which is mandatory for boarding • All QR code of passengers obtained before suspending valid • PCR test is required upon arrival, each passenger has to pay 28 JOD via electronic payment as follows: - Queen Alia International Airport – Amman (AMM): - https://registration.questlabjo.com/ - King Hussein International Airport – Aqaba (AQJ): - https://COVID19.biolab.jo - Amman Civil Airport – Marka (ADJ): - The amount will be collected directly in the Lab • Each passenger has to obtain a payment bill to show at check in counter before boarding, passenger who cannot pay through the links, the airline is responsible to collect the amount as EMD. • PCR test is not required for children below 5 years of age. • Diplomats and Employees of Regional and International Organizations (and their dependents -

Check-In Am Bahnhof Und Fly Rail Baggage

1/8 Check-in am Bahnhof via Zürich und Genève Check-in à la gare via Zürich et Genève Check-in alla stazione via Zürich e Genève Check-in at the railstation via Zürich and Genève Version: 26. Januar 2011 Legend HA = Handlingagent SP = Swissport, DN = Dnata Switzerland AG, AS = Airline Assistance Switzerland AG, EH = Own Handling R = Reason T = Technical, S = Security, O = Other reason WT = Weight Tolerance Y = Economy-Class, C = Business-Class, F = First-Class * = Agent Informations Infoportal/Airlines Check-in ok Restrictions Airline, Code Check-in Einschränkungen/Restrictions WT HA R Y = 2 Adria Airways JP ok SP C = 3 Aegean Airlines A3 ok 2 SP Aer Lingus EI no SP O Aeroflot Russian Airlines SU no SP S Aerolineas Argentinas AR ok 2 SP African Safari Airways ASA ok 2 DN Afriqiyah Airways 8U no DN O Air Algérie* AH ok No boardingpass 0 SP Air Baltic BT no SP T Not for USA, Canada, Pristina, Russia, Air Berlin* AB ok Cyprus; 0 DN not possible for groups 11+ Air Cairo MSC ok 2 SP AC 6821 / 6822 / 6826 / 6829 / 6832 / Air Canada AC no SP T =ok Air Dolomiti EN ok 2 SP Air Europa AEA / UX ok 2 DN Not from Zürich; not for USA, Canada, AF ok* 2 SP T Air France* Mexico; no boardingpass Air India AI ok 2 SP Air Italy I9 ok 2 DN Air Mali XG no SP O Air Malta KM ok 3 SP Y = 7 Air Mauritius MK ok Not from Zurich SP C = 10 Air Mediteranée BIE ok 2 DN Air New Zealand NZ ok 2 SP Air One AP ok 2 SP Air Seychelles HM ok Not from Zurich 3 SP Air Transat TS ok 2 SP Alitalia AZ no SP/DN T American Airlines AA no SP T ANA All Nippon Airways NH ok 2 SP Armavia -

National Strategy and Action Plan for Sustainable Consumption and Production in Jordan | 2016 - 2025

SCP National Strategy and Action Plan NATIONAL STRATEGY AND ACTION PLAN FOR SUSTAINABLE CONSUMPTION AND PRODUCTION IN JORDAN | 2016 - 2025 SwitchMed Programme is funded by the European Union SwitchMed Programme is funded by the European Union SwitchMed Programme is implemented by the United Nations Industrial Development Organisation (UNIDO) and the United Nations Environment Programme (UNEP), through the Mediterranean Action Plan (MAP) and its Regional Activity Centre for Sustainable Consumption and Production (SCP/RAC) and the Division of Technology, Industry and Economics (DTIE). For details on the SwitchMed Programme please contact [email protected] © Ministry of Environment. 2016 This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgement of the source is made. UNEP would appreciate receiving a copy of any publication that uses this publication as a source. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Ministry of Environment. Cover photo: www.shutterstock.com General disclaimers The views expressed in this document are those of the authors and do not necessarily reflect the views of the Ministry of Environment, the United Nations Environment Programme and of the European Union. The designations employed and the presentation of material in this document do not imply the expression of any opinion whatsoever on the part of UNEP and the European Union concerning the legal status of any country, territory or city or its authorities, or concerning the delimitation of its frontiers or boundaries.