Marc Townsend, Managing Director, CBRE Vietnam Hanoi, 7Th April, 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

To Review Evidence of a Likely Secret Underground Prison Facility

From: [email protected] Date: June 2, 2009 2:53:54 PM EDT To: [email protected] Cc: [email protected], [email protected], [email protected], [email protected] Subject: Our Memorial Day LSI Request of 5/25/2009 3:44:40 P.M. EDT Sirs, We await word on when we can come to Hanoi and accompany you to inspect the prison discussed in our Memorial Day LSI Request of 5/25/2009 3:44:40 P.M. EDT and in the following attached file. As you see below, this file is appropriately entitled, "A Sacred Place for Both Nations." Sincerely, Former U.S. Rep. Bill Hendon (R-NC) [email protected] Former U.S. Rep. John LeBoutillier (R-NY) [email protected] p.s. You would be ill-advised to attempt another faked, immoral and illegal LSI of this prison like the ones you conducted at Bang Liet in spring 1992; Thac Ba in summer 1993 and Hung Hoa in summer 1995, among others. B. H. J. L. A TIME-SENSITIVE MESSAGE FOR MEMBERS OF THE SENATE SELECT COMMITTEE ON POW/MIA AFFAIRS 1991-1993: SENATOR JOHN F. KERRY, (D-MA), CHAIRMAN SENATOR HARRY REID, (D-NV) SENATOR HERB KOHL (D-WI) SENATOR CHUCK GRASSLEY (R-IA) SENATOR JOHN S. McCAIN, III (R-AZ) AND ALL U.S. SENATORS CONCERNED ABOUT THE SAFETY OF AMERICAN SERVICE PERSONNEL IN INDOCHINA AND THROUGHOUT THE WORLD: http://www.enormouscrime.com "SSC Burn Bag" TWO FORMER GOP CONGRESSMEN REVEAL DAMNING PHOTOS PULLED FROM U.S. SENATE BURN BAG IN 1992; CALL ON SEN. -

Hanoi Capital Area: 3.324,92 Sq. Km Population

Hanoi Capital Area: 3.324,92 sq. km Population: 7,448,9 thousand habitants Administrative divisions: - 10 urban districts: Hoan Kiem, Ba Dinh, Dong Da, Hai Ba Trung, Tay Ho, Thanh Xuan, Cau Giay, Long Bien, Hoang Mai, Ha Dong. - 1 city: Son Tay - 18 rural districts: Dong Anh, Soc Son, Thanh Tri, Tu Liem, Gia Lam (Hanoi); Ba Vi, Chuong My, Dan Phuong, Hoai Duc, My Duc, Phu Xuyen, Phuc Tho, Quoc Oai, Thach That, Thanh Oai. Thuong Tin, Ung Hoa (former Ha Tay province) and Me Linh (a former district of Vinh Phuc province). Ethnic groups: Viet (Kinh), Hoa, Muong, Tay, Dao... Hanoi is the capital of the Socialist Republic of Vietnam, the center of culture, politics, economy and trade of the whole country Geography Hanoi is located in the Red River Delta, in the center of North Vietnam. It is encompassed by Thai Nguyen, Vinh Phuc provinces to the north, Hoa Binh and Ha Nam to the south, Bac Giang, Bac Ninh and Hung Yen provinces to the east, Hoa Binh and Phu Tho to the west. Hanoi means "the hinterland between the rivers" (Ha: river, Noi: interior). Hanoi's territory is washed by the Red River (the portion of the Red River embracing Hanoi is approximately 40km long) and its tributaries, but there are some other rivers flowing through the capital, including Duong, Cau, Ca Lo, Day, Nhue, Tich, To Lich and Kim Nguu. Climate Hanoi is situated in a tropical monsoon zone with two main seasons. During the dry season, which lasts from October to April, it is cold and there is very little rainfall, except from January to March, when the weather is still cold but there is some light rain. -

Large-Scale Township Development in Vietnam's Hanoi Area

To members of the press November 5, 2020 Nomura Real Estate Development Co., Ltd. Participation in “Ecopark Project” Large-Scale Township Development in Vietnam’s Hanoi Area Aiming to Enhance Added Value of Project Centering on Partnership with Local Developer in Nomura’s First Entry into Hanoi Nomura Real Estate Development Co., Ltd. (head office: Shinjuku Ward, Tokyo; President and Representative Director: Seiichi Miyajima; hereinafter “Nomura”) has agreed to participate in a condominium housing project (hereinafter “the Project”) within the Ecopark Project, a large- scale development project undertaken by local developer Ecopark Corporation Joint Stock Company (hereinafter “Ecopark Corporation”) in Vietnam’s Hanoi area. Ecopark Corporation is a local developer that has been engaging in ongoing development of the Ecopark Project for over a decade and boasts one of the highest levels of brand power in the area. The Ecopark Project covers approximately 500 hectares in total, making it one of the largest township developments in Vietnam (completion of all blocks slated for 2030), and features residential, office, retail, school, park, and other urban functions combined with abundant nature spanning over 100 hectares of greenery and waterfront. In Vietnam, Nomura participated in the Phu My Hung Project* in 2015, and has since been engaging in condominium housing projects and office building projects in the Ho Chi Minh area. This will be Nomura’s first project participation in the area of Hanoi, the capital city of Vietnam. Centering on a partnership between the two companies, Nomura will contribute to further enhancing the Ecopark Project’s added value while engaging in the Project from the planning and design stages by utilizing the housing business insight cultivated in Japan to date, as well as the track record and expertise in Vietnam to date. -

Northeast-Vietnam-Hill-Tribe-Villages

Discovery Indochina Your Way! Hill Tribe Villages Northwest Vietnam Adventure Expedition – 11 Days/ 10 Nights Duration: 11 Days/ 10 Nights Depart From: Hanoi Destinations: Hanoi - Lao Cai - Sapa –Trinh Tuong - Lung Po - Y Ty – Bat Xat - Den Sang - Nhiu Co San – Sapa – Lung Khau Nhin Market – Muong Khuong - Cao Son Market – Coc Ly Market – Simacai market - Hanoi. Description: The 11 days Hill Tribe Villages Northwest Vietnam Adventure Expedition trip covers a wide range of Vietnam hill tribe villages in Northeast Vietnam, with visiting the Ha Nhi minority villages, Black Hmong minority villages, Black Lolo minority villages, Red Dao minority village, Tay and Nung minority villages. You also chance to visit many colorful ethnic minority markets, home-stay experience and immerse yourself into different culture and customs. This trip is specially designed for the ones who love adventure, deeply in love with ethnic minority village’s expedition and photography. Green Discovery Indochina Head Office Address: 17A/28 Nguyen Hong, Dong Da Dist, Hanoi,Vietnam Tel : +84 439381242 Fax: +84 439381242 Mobile:+84987184390 E-mail : [email protected] Website: www.greendiscoveryindochina.com Discovery Indochina Your Way! Brief Itinerary Tour Dates Destinations Meals Included Day 1 Hanoi – Lao Cai D Day 2 Lao Cai - Sapa B, L, D Day 3 Ta Van – Giang Ta Chai – Su Pan – Sapa B, L, D Day 4 Sapa - Muong Hum - Trinh Tuong – Lung Po – B, L, D Y Ty Day 5 Y Ty - Ngai Thau - Den Sang - Nhiu Co San B, L, D Day 6 Windy Pass – Sang Ma Sao B, L, D Day 7 Y Ty – Muong Hum – Sapa B, L Day 8 Sapa – Lung Khau Nhin Market – Muong B, L, D Khuong Day 9 Muong Khuong – Cao Son Market – Coc Ly B, L, D market Day 10 Simacai market – Lao Cai - Night train to B, L, D Hanoi Day 11 Hanoi – Arrival. -

For the Development of Hanoi

4 Health Care Service Map of Japan’s ODA projects in Hanoi Japan helped improve infrastructure for Bach Mai Hospital and Gynecology (NHOG). Moreover, Japan has helped as well as training for healthcare staff, especially doctors the National Institute of Health and Epidemics (NIHE) to A ԣ ԡ and nurses, making contribution to the improvement of build a bio-safety level-3 laboratory and worked together Japan’s ODA healthcare services for the north of Vietnam in general and with Japanese research bodies to carry out technical and Ԥ BẮC NINH for Hanoi, in particular. In addition, Japan also provided academic cooperation. Now, NIHE is actively conducting Sông Hồng Ԣ Âu Cơ FOR THE DEVELOPMENT healthcare equipment for the Vietnam National Hospital experiments on bird fl u samples, making contribution to of Pediatrics (NHP) and National Hospital for Obstetrics responding to infectious diseases in Vietnam. Ԛ Lạc Long Quân OF HANOI Ԝ A ԟ Ԟ Hồ Tây Ԡ ԛ ԝ HƯNG YÊN Bach Mai Hospital National Institute of Health and Epidemics (NIHE) ԟ Hoàng Hoa Thám Ԙ Ԟ Trần Nhật Duật Japan’s ODA key projects in Hanoi Đội Cấn ԫ Hùng Vương Hoàng Diệu Liễu Giai Amount Trần Phú Loan co-operation Fiscal year Kim Mã Nguyễn Thái Học (¥ mil.) ԙ Trần Quang Khải Lý Thái Tổ ① Hanoi drainage project for environment improvement (I), (II) 47,860 1994, 1997, 2008 ԙ Ԙ Tràng Thi Ԧ ԨHai Bà Trưng Giảng Võ ② Transport infrastructure development project in Hanoi 12,510 1998 ԙ Ga Lý Thường Kiệt Chùa Láng Hà Nội Trần Hưng Đạo ③ Hanoi urban infrastructure development project (II) 11,433 1996 ԩ Đê La Thành Hàng Bài Tôn Đức Thắng ④ Red river bridge construction project (I) ~ (IV) (including guiding lane to the ring road No. -

Tour Dossier Grand Tour of Indochina Classic Tour │27 Days│ Moderate Pace

Tour Dossier Grand Tour of Indochina Classic Tour │27 Days│ Moderate Pace This document has been designed to provide a straightforward description of the physical activities involved in sightseeing or travelling during the tour. All passengers should read this dossier to assess the physical requirements of the programme and their ability to complete the tour. Classic Tours Designed for those who wish to see the iconic sites and magnificent treasures on a fully inclusive excellent value group tour. Grand Tour of Indochina is a Moderate Pace tour. This is defined in our brochure as the following: Tours require a higher level of fitness and may include standard activities and longer periods of sightseeing. Easy walking, longer drives, climbing of stairs and in/out of boats will be necessary. Some programmes may also include light hiking or a home stay and overnight train journeys. Anyone with a good level of fitness should be able to complete this itinerary. Of course, our National Escort/Local Guides always endeavour to provide the highest level of service and assistance, but they cannot be expected to cater for customers who are unfit to complete the itinerary. Please refer to your Travel Guide for more information. Tour highlights: On our Indochina Delights itinerary, you will visit: Saigon - Vietnam’s most cosmopolitan and vibrant city. Mekong Delta - ‘Rice Basket of Vietnam’ and home to many living, working and travelling along the river. Hoi An - Discover this charming UNESCO World Heritage listed site. Hue - The country’s former capital. Hanoi - Exploration of this charming, historical centre & its French provincial influences. -

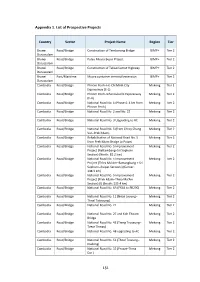

151 Appendix 1. List of Prospective Projects

Appendix 1. List of Prospective Projects Country Sector Project Name Region Tier Brunei Road/Bridge Construction of Temburong Bridge BIMP+ Tier 2 Darussalam Brunei Road/Bridge Pulau Muara Besar Project BIMP+ Tier 2 Darussalam Brunei Road/Bridge Construction of Telisai Lumut Highway BIMP+ Tier 2 Darussalam Brunei Port/Maritime Muara container terminal extension BIMP+ Tier 2 Darussalam Cambodia Road/Bridge Phnom Penh–Ho Chi Minh City Mekong Tier 1 Expressway (E-1) Cambodia Road/Bridge Phnom Penh–Sihanoukville Expressway Mekong Tier 2 (E-4) Cambodia Road/Bridge National Road No. 1 (Phase 4: 4 km from Mekong Tier 2 Phnom Penh) Cambodia Road/Bridge National Road No. 2 and No. 22 Mekong Tier 2 Cambodia Road/Bridge National Road No. 3 Upgrading to AC Mekong Tier 2 Cambodia Road/Bridge National Road No. 5 (from Chroy Chang Mekong Tier 2 Var–Prek Kdam) Cambodia Road/Bridge Rehabilitation of National Road No. 5 Mekong Tier 2 from Prek Kdam Bridge to Poipet Cambodia Road/Bridge National Road No. 5 Improvement Mekong Tier 2 Project (Battambang–Sri Sophorn Section) (North: 81.2 km) Cambodia Road/Bridge National Road No. 5 Improvement Mekong Tier 2 Project (Thlea Ma'Am–Battangbang + Sri Sophorn–Poipet Sections) (Center: 148.3 km) Cambodia Road/Bridge National Road No. 5 Improvement Mekong Tier 2 Project (Prek Kdam–Thlea Ma'Am Section) (I) (South: 135.4 km) Cambodia Road/Bridge National Road No. 6A (PK44 to PK290) Mekong Tier 2 Cambodia Road/Bridge National Road No. 11 (Neak Leoung– Mekong Tier 2 Thnal Toteoung) Cambodia Road/Bridge National Road No. -

Vietnam by Private Train

www.railwayadventures.co VIETNAM BY PRIVATE TRAIN 17 days 2 – 18 September 2013 HO CHI MINH CITY – DALAT – HOI AN – HUE – HANOI – HALONG BAY Featuring: The Reunification Express, The Dalat Railway, Steam at Thai Nguyen and the Indochina Sails on Ha Long Bay Embrace this rare opportunity to explore Vietnam by Private Train on the legendary Reunification Express – one of the world’s great rail journeys. Welcomed onto your private sleeping and restaurant cars in Ho Chi Minh City you will travel in stages enjoying Vietnam’s most iconic destinations on a 1,700 kilometre odyssey all the way north to Hanoi. The adventure includes side trips to the colourful colonial hill station city of Dalat, the ancient trading port of Hoi An, a special charter on the normally inaccessible last steam railway in Indochina and an overnight cruise on the stunning World Heritage-listed Ha Long Bay. An optional extension to the mountainous colonial hill station of Sapa, near the Chinese border, caps off this special journey. Enjoy two nights on board our private train, in two-berth compartments, a night on the luxury Indochina Sails on Ha Long Bay and the balance in luxury 4- and 5- star hotels. On the way discover the rich culture of Vietnam: its ancient kingdoms and colourful colonial past, the fascinating ethnic diversity and triumphant post-war reconstruction. Legendary food, friendly people and excellent shopping complete the experiences of this wonderful and unique railway adventure. Itinerary Day 1 – Monday 2 September 2013 – Arrive in Ho Chi Minh City (D) Suggested flights Vietnam Airlines departing Sydney: Sydney – Ho Chi Minh City 11.15am – 4.30pm Arrive Ho Chi Minh City late afternoon. -

Deks Air Travel & Tours Pte

Tour Code : DEK06HANIS Day 1: Singapore – Hanoi ( D ) Upon arrival at Noi Bai International Airport, our representative will meet you and then transfer to down town Hanoi – the city of Lakes. Dinner will be available at local restaurant before checking in hotel Overnight in Hanoi Day 2: Hanoi - Halong – Indochina Sail Cruise (B/L/D) After breakfast at the hotel, depart to Halong Bay which is well known as “World Heritage”. Most of the islands on Ha Long Bay are limestone and were formed over 500 million years ago, and are massed in the southeast and southwest. The schist islands scattered in the southeast have an average height of between 50-200m, and have a rich covering of flora. It takes around 04 hours for transfer. After the briefing and check in we have a bit of free time till lunch is served at 1:00pm. Lunch is a multi- course Vietnamese and Western set menu. Any and all dietary needs will be catered to. During lunch we cruise through the Bai Tu Long Bay, cruising through the most beautiful and quiet area in Bai Tu Long Bay and Halong Bay to visit Cua Van Fishing Village. Cua Van Floating Fishing Village (the largest fishing village on the Bay). At the village, which has a population of about 600 residents living in about 150 floating houses, guests can choose between kayaking through the village or visiting on small bamboo boats (sampans) rowed by the villagers. Back on board after visiting the village there will be free time of about one and a half hours before the Cooking Class on board will be held by our Chef and all the passengers could attend to this. -

40080-013: Ha Noi Metro Rail System Project

Environmental Monitoring Report Project Number: 40080-013 Semi - Annual Environmental Monitoring Report (July - December 2019) July 2020 VIE: Ha Noi Metro Rail System Project (Line 3: Nhon – Ha Noi Station Section) Prepared by Ha Noi Metropolitan Railway Management Board for Ha Noi People’s Committee and the Asian Development Bank. Package CS1: Consulting Services for Project Management Support (Phase 2) under Hanoi Metro Rail System Project (Line 3: Nhon – Hanoi Station Section) NOTE In this report, “$” refers to US dollars. This environmental monitoring report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Package CS1: Consulting Services for Project Management Support (Phase 2) under Hanoi Metro Rail System Project (Line 3: Nhon – Hanoi Station Section) SEMI-ANNUAL ENVIRONMENTAL MONITORING REPORT Project Number: 40080-013 Code: PMS2-MRB-SEMR-21.4 Rev 1 Reporting Period: July to December 2019 July 2020 VIE: Ha Noi Metro Rail System Project (Line 3: Nhon - Ha Noi Station Section) Prepared by: Hanoi Metropolitan Railway Management Board (with support by PMS2- TPF Getinsa Euroestudios S.L. Spain) Package CS1: Consulting -

Cambodia), 450 Machines), 22

20_194072 bindex.qxp 12/14/07 11:15 PM Page 487 Index Angkor Thom Gates ATMs (automated-teller AARP, 37 (Cambodia), 450 machines), 22. See also Abercrombie & Kent, 45, 397 Angkor Wat (Cambodia), Banks and currency exchange Absolute Asia, 45 390, 431, 456 Australia Access-Able Travel Source, 36 restaurants, 448 Cambodia visitor information, Access America, 24 shopping, 459 397 Accessible Journeys, 36 sights and attractions, consulate, 318 Accommodations 448–449 customs regulations, 59 best, 7–8 sunrise and sunset views, 454 embassy of, Hanoi, 60 Cambodia, 403–404 The Angkor What? (Siem Reap), embassy of (Phnom Penh), tips on, 54–56 462 400 AIDS Animism, 145 passports, 62 Cambodia, 400 Annam (Ho Chi Minh City), 353 Vietnam embassy and con- Vietnam, 28 Ann Tours, 80, 150, 317, 374 sulate general, 13 Airport security, 19 An Phu Tourist, 83, 204, Authentique Interiors (Ho Chi Air quality, 31 223–225, 230, 255, 289 Minh City), 354 Air travel, 17–20, 50 An Thoi, 389 Avian influenza, 30, 31 bankrupt airlines, 24 An Thoi Archipelago, 389 A-Z Queen Salute Café Alexandre Yersin Museum Antiques, 129 Travel, 81 (Nha Trang), 298–299 Hanoi, 130, 131 Allez Boo (Ho Chi Minh City), A-1 Hill (Dien Bien Phu), 165 356 Apocalypse Now (Hanoi), Ba Be Lake, 167 Alphana Jewelry (Ho Chi 137–138 Ba Be National Park, 167, 168 Minh City), 354 Apricot Gallery (Hanoi), 134 Ba Be Street (Hanoi), 136 Ambre (Phnom Penh), 421 Apsara dance, Siem Reap Bac Can, 167 American Airlines Vacations, 44 (Cambodia), 461 Bacchus Corner (Ho Chi American Express, 57 Apsara Faces (Cambodia), -

Genetic Variability of the Critically Endangered Softshell Turtle, Rafetus Swinhoei: a Preliminary Report

Genetic Variability of the Critically Endangered Softshell Turtle, Rafetus swinhoei: A Preliminary Report Minh Duc Le Centre for Natural Resources and Environmental Studies 19 Le Thanh Tong Street Hanoi, Vietnam Tel: 098-3456-098 Email: [email protected] Peter Pritchard Chelonian Research Institute 402 South Central Avenue Oviedo, Florida 32765 USA [email protected] Citation: Le, M.D. and P. Pritchard. 2009. Genetic variability of the critically endangered softshell turtle Rafetus swinhoei: A preliminary report. In the Proceedings of the First Vietnamese National Symposium on Reptiles and Amphibians, pp. 84-92. Page 1 ABSTRACT The critically endangered softshell turtle, Rafetus swinhoei, is on the verge of extinction due to anthropogenic threats. However, taxonomic status of populations throughout its range has not been evaluated thoroughly. This project aims to fill this gap of knowledge by sampling all available specimens in museums and collections around the world. Using forensic methods and a phylogenetic approach, the project attempts to reveal the population structure and genetic diversity among these populations. The results of this study will in turn be helpful to the formulation of conservation measures for this species, especially future captive breeding programs by identifying genetically distinct populations. In this report, we present our preliminary results showing the deep divergence between R. swinhoei and R. euphraticus, and that genetic divergence of R. swinhoei's populations within Vietnam is not high, although sequencing errors may confound precise interpretation. For future research, more samples from other parts of its range, especially samples from China, should be analyzed in order to fully understand population differentiation and structure of this poorly known species.