ASX FXJ 2012.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lord Justice Leveson Speech: Hold the Front Page

THE RT. HON. LORD JUSTICE LEVESON HOLD THE FRONT PAGE: NEWS-GATHERING IN A TIME OF CHANGE UNIVERSITY OF MELBOURNE, AUSTRALIA 12 DECEMBER 2012 Introduction 1. It is a real privilege to have been asked to give this public lecture and, echoing the Vice Chancellor, I am pleased to acknowledge that we are standing on the land of the Wurundjeri people and to pay respect to their Elders and families past and present. I would also like to thank the Centre for Advanced Journalism at the University of Melbourne for the invitation. I am delighted to be here. 2. I hope you will forgive me for providing some context to what I am about to say. As you are aware, I have spent the last 17 months engaged in an Inquiry into the culture, practices and ethics of the press. The Report was published nearly a fortnight ago, on 29 November 2012, and, as I have said before, it may be that some of you are hoping that I will elaborate. If you are, I am afraid that you are going to be disappointed. When I launched the Report, which must be read in the context of the Terms of Reference for the Inquiry, I said this: ‘I believe that the Report can and must speak for itself; to that end, I will be making no further comment. Nobody will be speaking for me about its contents either now or in the future.’ 3. The reason is very simple. I treat the Report as a judgment and judges simply do not enter into discussion about judgments they have given; they do not respond 1 to comment, however misconceived; neither do they seek to correct error. -

Social Media Thought Leaders Updated for the 45Th Parliament 31 August 2016 This Barton Deakin Brief Lists

Barton Deakin Brief: Social Media Thought Leaders Updated for the 45th Parliament 31 August 2016 This Barton Deakin Brief lists individuals and institutions on Twitter relevant to policy and political developments in the federal government domain. These institutions and individuals either break policy-political news or contribute in some form to “the conversation” at national level. Being on this list does not, of course, imply endorsement from Barton Deakin. This Brief is organised by categories that correspond generally to portfolio areas, followed by categories such as media, industry groups and political/policy commentators. This is a “living” document, and will be amended online to ensure ongoing relevance. We recognise that we will have missed relevant entities, so suggestions for inclusions are welcome, and will be assessed for suitability. How to use: If you are a Twitter user, you can either click on the link to take you to the author’s Twitter page (where you can choose to Follow), or if you would like to follow multiple people in a category you can click on the category “List”, and then click “Subscribe” to import that list as a whole. If you are not a Twitter user, you can still observe an author’s Tweets by simply clicking the link on this page. To jump a particular List, click the link in the Table of Contents. Barton Deakin Pty. Ltd. Suite 17, Level 2, 16 National Cct, Barton, ACT, 2600. T: +61 2 6108 4535 www.bartondeakin.com ACN 140 067 287. An STW Group Company. SYDNEY/MELBOURNE/CANBERRA/BRISBANE/PERTH/WELLINGTON/HOBART/DARWIN -

Scheme Booklet Registered with Asic

QMS Media Limited 214 Park Street South Melbourne, VIC 3205 T +61 3 9268 7000 www.qmsmedia.com ASX Release 13 December 2019 SCHEME BOOKLET REGISTERED WITH ASIC QMS Media Limited (ASX:QMS) refers to its announcement dated 12 December 2019 in which it advised that the Federal Court had made orders approving: • the dispatch of a Scheme Booklet to QMS shareholders in relation to the previously announced Scheme of Arrangement with Shelley BidCo Pty Ltd, an entity controlled by Quadrant Private Entity and its institutional partners (Scheme); and • the convening of meetings of QMS shareholders to consider and vote on the Scheme. The Scheme Booklet has been registered today by the Australian Securities and Investments Commission. A copy of the Scheme Booklet, including the Independent Expert's Report and the notices of the Scheme Meetings, is attached to this announcement and will be dispatched to QMS' shareholders before Thursday 19 December 2019. Key events and indicative dates The key events (and expected timing of these) in relation to the approval and implementation of the Scheme are as follows: Event Date Scheme Booklet dispatched to QMS shareholders Before Thursday 19 December 2019 General Scheme Meeting 10.00am on Thursday 6 February 2020 Rollover Shareholders Scheme Meeting Thursday 6 February (immediately following the General Scheme Meeting) Second Court Hearing Monday 10 February 2020 Effective Date Tuesday 11 February 2020 Scheme Record Date 5.00pm on Friday 14 February 2020 Implementation Date Friday 21 February 2020 Note: All dates following the date of the General Scheme Meeting and the Rollover Shareholders Scheme Meeting are indicative only and, among other things, are subject to all necessary approvals from the Court and any other regulatory authority and satisfaction or (if permitted) waiver of all conditions precedent in the Scheme Implementation Deed. -

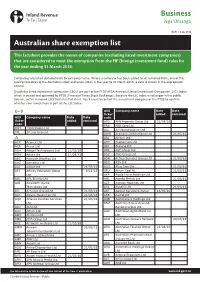

Australian Share Exemption List

Business Ngā Ūmanga IR871 | June 2016 Australian share exemption list This factsheet provides the names of companies (excluding listed investment companies) that are considered to meet the exemption from the FIF (foreign investment fund) rules for the year ending 31 March 2016. Companies are listed alphabetically by company name. Where a company has been added to, or removed from, one of the qualifying indices of the Australian stock exchange (ASX) in the year to 31 March 2016, a date is shown in the appropriate column. Qualifying listed investment companies (LICs) are part of the FTSE AFSA Australia Listed Investment Companies (LIC) Index which is owned and operated by FTSE (Financial Times Stock Exchange). Because the LIC index is no longer in the public domain, we’ve removed LICs from this factsheet. You’ll need to contact the investment company or the FTSE to confirm whether your investment is part of the LIC Index. 0–9 ASX Company name Date Date ticker added removed ASX Company name Date Date code ticker added removed APD APN Property Group Ltd 21/03/16 code ARB ARB Corp Ltd ONT 1300 Smiles Ltd ALL Aristocrat Leisure Ltd 3PL 3P Learning Ltd AWN Arowana International Ltd 21/03/16 A ARI Arrium Ltd ACX Aconex Ltd AHY Asaleo Care Ltd ACR Acrux Ltd AIO Asciano Ltd ADA Adacel Technologies Ltd 21/03/16 AFA ASF Group Ltd ADH Adairs Ltd 21/09/15 ASZ ASG Group Ltd ABC Adelaide Brighton Ltd ASH Ashley Services Group Ltd 21/03/16 AHZ Admedus Ltd ASX ASX Ltd ADJ Adslot Ltd 21/03/16 AGO Atlas Iron Ltd 21/03/16 AFJ Affinity Education Group 2/12/15 -

Federal Court of Australia

FEDERAL COURT OF AUSTRALIA Fairfax Media PublicatÍons Pty Ltd v Reed International Books Australia Pty Lrd [2010] FCA 984 Citation: Fairfax Media Publications Pty Ltd v Reed International Books Australia Pty Ltd [2010] FCA 984 Parties: FAIRF'AX MEDIA PUBLICATIONS PTY LTD (ACN 003 357 720) v REED INTERNATIONAL BOOKS AUSTRALIA pTy LTD (ACN 001 002 357) T/A LEXIS.NEXIS File number: NSD 1306 of 2007 Judge: BENNETT J Date ofjudgment: 7 September 2010 Catchwords: COPYRIGHT - respondent reproduces headlines and creates abstracts of arlicles in the applicant's newspaper - whether reproduction of headlines constitutes copyright infringernent - whether copyright subsists in individual newspaper headlines, in an article with its headline, in the compilation of all the articles and headlines in a newspaper edition and in the compilation of the edition as a whole - literary work - copyright protection for titles - use of headline as citation to article - policy considerations - originality - authorship - whether presumption of originality for anonymous works available - whether work ofjoint authorship - whether the headlines constitute a substantial part of each compilation - whether the work of writing headlines is part of the work of compilation - whether fair dealing for the pu{pose of or associated with reporting news ESTOPPEL - whether applicant estopped from asserting copyright infringement by respondent - applicant has known for many years that heacllines of the applicant,s newspaper are reproduced in the abstracting service - applicant had -

NEWSLETTER ISSN 1443-4962 No

AUSTRALIAN NEWSPAPER HISTORY GROUP NEWSLETTER ISSN 1443-4962 No. 70 December 2012 Publication details Compiled for the Australian Newspaper History Group by Rod Kirkpatrick, 38 Gingham Street, Glenella, Qld, 4740. Ph. +61-7-4942 7005. Email: [email protected] Contributing editor and founder: Victor Isaacs, of Canberra. Back copies of the Newsletter and some ANHG publications can be viewed online at: http://www.amhd.info/anhg/index.php Deadline for the next Newsletter: 22 February 2013. Subscription details appear at end of Newsletter. [Number 1 appeared October 1999.] Ten issues had appeared by December 2000 and the Newsletter has since appeared five times a year. 1 – CURRENT DEVELOPMENTS: NATIONAL & METROPOLITAN 70.1.1 NEWS AND PAY TV News Limited has won its battle for control of Consolidated Media Holdings. It will now own 50 per cent of Foxtel and 100 per cent of Fox Sports. Telstra owns the other 50 per cent of Foxtel. The Australian Competition and Consumer Commission opposed a rival bid for ConsMedia by Kerry Stokes’s Seven Group, which already owned 25 per cent. Stokes was expected to receive a $500 million windfall from the News deal. Darren Davidson and Damon Kitney reported (Australian, 12 October 2012, p.21) that Stokes was understood to have been “eyeing News’s Perth newspaper, the Sunday Times, to create a seven-day news operation’ in conjunction with Seven’s West Australian. News had not put the Sunday paper up for sale but might be willing to listen to a potential offer, sources told the Australian. On 31 October, 91.91 per cent of ConsMedia shareholders voted in favour of accepting the News Limited offer (Australian, 1 November 2012, p.23). -

Framing the NBN: an Analysis of Newspaper Representations

Framing the NBN: An Analysis of Newspaper Representations Rowan Wilken, Swinburne University of Technology Jenny Kennedy, University of Melbourne Michael Arnold, University of Melbourne Martin Gibbs, University of Melbourne Bjorn Nansen, University of Melbourne Abstract The National Broadband Network (NBN), Australia’s largest public infrastructure project, was initiated to deliver universal access to high-speed broadband. Since its announcement, the NBN has attracted a great deal of media coverage, coupled with at times divisive political debate around delivery models, costs and technologies. In this article we report on the results of a pilot study of print media coverage of the NBN. Quantitative and qualitative content analysis techniques were used to examine how the NBN was represented in The Age and The Australian newspapers during the period from 1 July 2008 to 1 July 2013. Our findings show that coverage was overwhelmingly negative and largely focused on the following: potential impacts on Telstra; lack of a business plan, and of cost-benefit analysis; problems with the rollout; cost to the federal budget; and implications for business stakeholders. In addition, there were comparatively few articles on potential societal benefits, applications and uses, and, socio-economic implications. Keywords: National Broadband Network, media representations, The Age, The Australian, newspaper coverage, content analysis Introduction The success of the National Broadband Network (NBN) in fulfilling its ambition to provide high-speed broadband to every business and household in the country, grow the digital economy, and support digital inclusion will be shaped by how it is understood, adopted, and appropriated by end-users. Since the project was announced on 7 April 2009 by the then- Labor Federal Government, the NBN has attracted a great deal of media coverage, coupled with, at times, divisive political debate around the model, costs and technology best fit for purpose. -

Fairfax Media’S Digital Transformation

Case Study Cloudinary Delivers Simplified Image Management Workflow for Fairfax Media’s Digital Transformation “Cloudinaryhasanumberofcustomersthatweconsiderpeers,sowefeltconfidentinits capabilities and ability to scale to support our reader base. In addition, Cloudinary offered functionality that addressed our need to deliver content to different devices, across various channels, as well as enabling us to render images dynamically to support different image formats or aspect ratios in the future.” –Damian Cronan, CTO, Fairfax Media Solution The Cloudinary API enabled dynamic URL-based manipulations to original high-quality images, eliminating the need for the editorial team to manually create and store multiple variants of every image and streamlining the publishing workflow. Results 25% Reductioninfilesize LEADING Three millionimagesoptimized for performance MULTI-PLATFORM MEDIA COMPANY Faster time to market with improved productivity – both for the engineering team and editorial staff Get started for free: www.cloudinary.com © 2018 Cloudinary. All rights reserved. Case Study Company Fairfax Media Limited [ASX:FXJ] is one of the largest media companies in Australia and New Zealand that engages audiencesandcommunitiesviaprintanddigitalmedia.ItincludesrecognizablemastheadsincludingThe Australian Financial Review, The Sydney Morning Herald and The Age. Fairfax Media operates numerous news and information websites, as well as tablet and smartphone apps, for online news sites. The Challenge: Future-Proof Image Management In2016,FairfaxMediabeganawide-rangingdigitaltransformationofitsnewsorganization,whichincludedstreamlining -

Privacy - Fairfax Media Limited

Privacy - Fairfax Media Limited PRIVACY You have come through to this page from a website which is published by a subsidiary of Fairfax Media Limited. In this policy, "us", "we" or "our" means Fairfax Media Limited (ABN 15 008 663 161) and its related bodies corporate, partnerships and joint venture entities. This policy sets out: • what is considered personal information; • what personal information we collect and hold; • how we collect, hold, use or disclose personal information; • the purposes for which we collect personal information; • what happens if we are not able to collect personal information; • how to seek access to and correct your personal information; • whether we disclose personal information outside Australia; and • how to contact us. We are bound by the Australian Privacy Principles contained in the Privacy Act 1988 (Cth) (subject to exemptions that apply to us under that Act). However, due to the nature of some of our business activities, from time to time, we will handle personal information relying on the media exemption in the Act where appropriate. Where we do so, we will ensure that we comply with the Australian Press Council Privacy Standards. We may also rely on related bodies corporate, employee records and other exemptions in the Act. If you require more information on the collection and use of personal information in the course of journalism, please visit the Australian Press Council Privacy Standards at www.presscouncil.org.au/privacy-principles. We may, from time to time, review and update this policy, including taking account of new or amended laws, new technology and/or changes to our operations. -

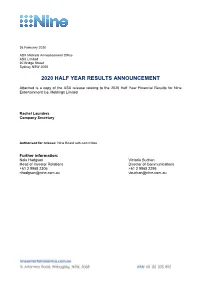

2020 Half Year Results Announcement

26 February 2020 ASX Markets Announcement Office ASX Limited 20 Bridge Street Sydney NSW 2000 2020 HALF YEAR RESULTS ANNOUNCEMENT Attached is a copy of the ASX release relating to the 2020 Half Year Financial Results for Nine Entertainment Co. Holdings Limited Rachel Launders Company Secretary Authorised for release: Nine Board sub-committee Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] NINE ENTERTAINMENT CO. FY20 INTERIM RESULTS 26 February 2020: Nine Entertainment Co. (ASX: NEC) has released its H1 FY20 results for the 6 months to December 2019. On a Statutory basis, pre Specific Items, on Revenue of $1.2b, Nine reported Group EBITDA of $251m, and a Net Profit After Tax of $114m. Post Specific Items, the Statutory Net Profit was $102m. These numbers are stated excluding Discontinued Businesses. On a pre AASB16 and Specific Item basis, Nine reported Group EBITDA of $231m, down 8% on the Pro Forma results in H1 FY19 for its Continuing Businesses. On the same basis, Net Profit After Tax and Minority Interests was $115m, down 9%. Key takeaways include: • Strong growth from digital video businesses o $35m EBITDA improvement at Stan1, with subscribers exceeding 1.8m o 65% growth in EBITDA at 9Now1, with market leading BVOD share of ~50% o Further investment in 9Now to accelerate growth into the broader digital video market • Result was heavily impacted by challenging cycles o Broad based ad market weakness including a 7% decline in Metro FTA revenues o Housing market softness impacting Domain’s residential listing volumes • Stability in Metro Media earnings1 • Synergies of $9m identified following completion of the Macquarie Media acquisition • Nine expects FY20 EBITDA at a similar level to FY191 1 like-basis, pre AASB16 Hugh Marks, Chief Executive Officer of Nine Entertainment Co. -

Chapter 3 Section 5

SECTION 5: CHINA’S DOMESTIC INFORMATION CONTROLS, GLOBAL MEDIA INFLUENCE, AND CYBER DIPLOMACY Key Findings • China’s current information controls, including the govern- ment’s new social credit initiative, represent a significant es- calation in censorship, surveillance, and invasion of privacy by the authorities. • The Chinese state’s repression of journalists has expanded to target foreign reporters and their local Chinese staff. It is now much more difficult for all journalists to investigate politically sensitive stories. • The investment activities of large, Chinese Communist Par- ty-linked corporations in the U.S. media industry risk under- mining the independence of film studios by forcing them to consider self-censorship in order to gain access to the Chinese market. • China’s overseas influence operations to pressure foreign media have become much more assertive. In some cases, even without direct pressure by Chinese entities, Western media companies now self-censor out of deference to Chinese sensitivity. • Beijing is promoting its concept of “Internet sovereignty” to jus- tify restrictions on freedom of expression in China. These poli- cies act as trade barriers to U.S. companies through both cen- sorship and restrictions on cross-border data transfers, and they are fundamental points of disagreement between Washington and Beijing. • In its participation in international negotiations on global Inter- net governance, norms in cyberspace, and cybersecurity, Beijing seeks to ensure continued control of networks and information in China and to reduce the risk of actions by other countries that are not in its interest. Fearing that international law will be used by other countries against China, Beijing is unwilling to agree on specific applications of international law to cyberspace. -

NEWSLETTER ISSN 1443-4962 No

ABOVE: The Great Southern Herald building, Katanning, Western Australia, 2003. The paper began publication on 5 October 1901. Issues from 1901-54 have been digitised and are available through Trove. BELOW: The Narrogin Observer, also WA, was in a shopping complex, with some distractions, 2003. It began publication on 26 August 1905. Both newspapers are still published. AUSTRALIAN NEWSPAPER HISTORY GROUP NEWSLETTER ISSN 1443-4962 No. 89 September 2016 Publication details Compiled for the Australian Newspaper History Group by Rod Kirkpatrick, 337/55 Linkwood Drive, Ferny Hills, Qld, 4055. Ph. +61-7-400 031 614. Email: [email protected] Contributing editor and founder: Victor Isaacs, of Canberra, is at [email protected] Back copies of the Newsletter and some ANHG publications can be viewed online at: http://www.amhd.info/anhg/index.php Deadline for the next Newsletter: 9 December 2016. Subscription details appear at end of Newsletter. [Number 1 appeared October 1999.] Ten issues had appeared by December 2000 and the Newsletter has since appeared five times a year. 1—Current Developments: National & Metropolitan Editor’s note: This issue appears about a week early because my wife and I will move on 29 September into our new home in Brisbane after five months in “no fixed abode”—in various holiday apartments in one block at Redcliffe. My new address is in the details box on Page 1. 89.1.1 Sunday Times and PerthNow go to Seven West The competition watchdog has delivered its approval to a proposed shake-up of the Western Australian media landscape. After two false starts, Kerry Stokes’ Seven West Media will soon have control of the state’s two mainstream metropolitan mastheads (Australian, 15 September 2016).