2020 Half Year Results Announcement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

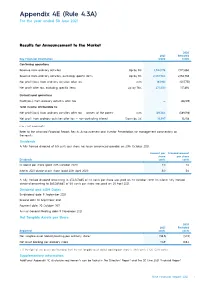

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Presentation to Macquarie Conference

4 May 2021 ASX Markets Announcements Office ASX Limited 20 Bridge Street Sydney NSW 2000 PRESENTATION TO MACQUARIE CONFERENCE 4 May 2021: Attached is a copy of Nine’s presentation to the Macquarie Australia Conference 2021. Authorised for lodgment by Mike Sneesby, Chief Executive Officer. Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2060 ABN 60 122 203 892 MIKE SNEESBY | CHIEF EXECUTIVE OFFICER Important Notice and Disclaimer as a result of reliance on this document. as a general guide only, and should not be relied on This document is a presentation of general as an indication or guarantee of future performance. background information about the activities of Nine Forward Looking Statements Forward looking statements involve known and unknown risks, uncertainty and other factors which Entertainment Co. Holdings Limited (“NEC”) current This document contains certain forward looking can cause NEC’s actual results to differ materially at the date of the presentation, (4 May 2021). The statements and comments about future events, from the plans, objectives, expectations, estimates information contained in this presentation is of including NEC’s expectations about the performance and intentions expressed in such forward looking general background and does not purport to be of its businesses. Forward looking statements can statements and many of these factors are outside complete. It is not intended to be relied upon as generally be identified by the use of forward looking the control of NEC. -

Timber Lines

TIMBER LINES S VOL. VIII JUNE 19 THIRTY-YEAR CLUB R-6 FOREST SERVICE V TIMBER LINES NO. VIII - PUBLISHED NOW MD THEN 13Y R-6 THIRTY-YEAR CLUB - JUNEl9SL When things go wrong, as they sometimes will, When the road you're trudging seenis all up hill, Whe funds are low and the debts are high And you want to smile, but you have to sigh When care is pressing you doun a bit, Rest, if you must - but don't you quit. Success Is failure turned inside out, The silver tint on the clouds of doubt, And you never can tell how cl6se you are, It may be near when it seems afar; 'So stick to the fight when you're hardest hit - It'swhenthings seem worst that you niust'nt. quit.. Anonymous S .. :.:THE PURPOSE OF TIER LINES To provide a means of keeping the clib informed on matters of common interest, to provide a nidiuzn of communication between members, to assist in making real the objectives of our constitution arid to' provide a bridge to span the gap between membersinretirement arid those stillin active service. To these things we dedicate Timber Lines. Editor Ny greetings to the 30-Year Club with some notes of major happenings in F.Y. 1951i. The past year has been a busy one for Region Six. That's not new. There has never been a year since the Region was formed that has not been a busy one..This year our timber cut is up slightly. It is close to 2billionfeet, although prices are down and our receipts will be less than last year. -

AUSTRALIAN PODCAST RANKER TOP 100 PODCASTS Reporting Period: 25 November - 22 December

AUSTRALIAN PODCAST RANKER TOP 100 PODCASTS Reporting Period: 25 November - 22 December RANK PODCAST PUBLISHER SALES REPRESENTATION RANK CHANGE 1 Hamish & Andy SCA-PodcastOne Australia PodcastOne Australia 0 2 The Lighthouse News Corp Australia News Corp / Nova Ent h5 3 Kate, Tim & Marty Nova Nova Entertainment 0 4 7am Schwartz Media Schwartz Media New 5 The Kyle & Jackie O Show Australian Radio Network Australian Radio Network i3 6 Life and Crimes with Andrew Rule News Corp Australia News Corp / Nova Ent h2 7 SEN Breakfast SEN / Crocmedia SEN / Crocmedia i2 8 Whateley SEN / Crocmedia SEN / Crocmedia i4 9 Sky News - News Bulletin News Corp Australia News Corp / Nova Ent h5 10 WILOSOPHY with Wil Anderson TOFOP Productions Whooshkaa New 11 Money News with Ross Greenwood Nine Radio1 Nine Radio i5 12 The Alan Jones Breakfast Show Nine Radio Nine Radio i2 13 Bedtime Explorers The Parent Brand The Parent Brand New 14 Kennedy Molloy SCA-Triple M SCA i5 15 The Howie Games SCA-PodcastOne Australia PodcastOne Australia i4 16 Hughesy and Kate SCA-Hit SCA i1 17 Moonman In The Morning - 104.9 SCA-Triple M SCA i5 Triple M Sydney 18 The Hot Breakfast SCA-Triple M SCA h1 19 Who the Hell is Hamish? News Corp Australia News Corp / Nova Ent i6 20 Chrissie, Sam & Browny Nova Nova Entertainment i4 21 Jase & PJ Australian Radio Network Australian Radio Network i1 22 Tech News News Corp Australia News Corp / Nova Ent h3 23 Police Tape News Corp Australia News Corp / Nova Ent h24 24 The Ray Hadley Morning Show Nine Radio Nine Radio i3 25 Motley Fool Money Australia -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

2015 SWM Annual Report

ABN 91 053 480 845 Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Seven West Media cares about the environment. By printing 2000 copies of this Annual Report on ecoStar Silk and ecoStar Offset the environmental impact was reduced by*: 1,185kg 171kg 1,707km of landfill of CO2 and travel in the average greenhouse gases European car 26,982 2,486kWh 1,926kg litres of water of energy of wood Source: European BREF data (virgin fibre paper). Carbon footprint data evaluated by Labelia Conseil in accordance with the Bilan Carbone® methodology. Results are obtained according to technical information and are subject to modification. *compared to a non-recycled paper. Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Contents What We Do 4 The Future of Us 44 Our Brands 6 Board of Directors 46 Our Strategy 8 Corporate Governance Statement 49 Our Strategic Framework 10 Directors’ Report 60 Letter from the Chairman 12 Remuneration Report 64 Letter from the Managing Director & CEO 14 Auditor’s Independence Declaration 83 Performance Dashboard 16 Financial Statements 84 Performance of the Business 18 Directors’ Declaration 134 Group Performance 20 Independent Auditor’s Report 135 Television 26 Company Information 137 Newspapers 32 Investor Information 138 Magazines 36 Shareholder Information 139 Other Business and New Ventures 40 Risk, Environment and Social Responsibility 42 2 Seven West Media Annual Report 2015 ABN 91 053 480 845 Contents The right people creating great content across television, digital, mobile and newspaper and magazine publishing. Delivering the future of content 3 What We Do We are achieving growth in the delivery of our content across our portfolio of integrated media platforms. -

Appendix 4E (Rule 4.3A) for the Year Ended 30 June 2020

FINANCIAL REPORT– 30 JUNE 2020 Appendix 4E (Rule 4.3A) for the year ended 30 June 2020 Results for Announcement to the Market 2020 2019 Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities, excluding specific items Up by 17% 2,172,021 1,854,676 (Loss)/Profit from ordinary activities after tax n/m (508,778) 216,566 Net profit after tax, excluding specific items Down by 17% 155,937 187,064 Discontinued operations (Loss)/Profit from ordinary activities after tax n/m (66,189) 17,314 Total income attributable to: Net (loss)/profit from ordinary activities after tax — owners of the parent n/m (590,033) 221,229 Net profit from ordinary activities after tax — non-controlling interest Up by 19% 15,066 12,651 n/m: not meaningful. Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends An interim fully franked dividend of 5 cents per share was paid on 20 April 2020. Since the end of the financial year, the directors have determined that a fully franked dividend of 2 cents per share will be payable in October 2020 in respect of the year ended 30 June 2020. Dividend and AGM Dates Ex-dividend date: 9 September 2020 Record date: 10 September 2020 Payment date: 20 October 2020 Annual General Meeting date: 12 November 2020 Net Tangible Assets per Share 2020 2019 Reported cents cents Net tangible asset (deficit)/backing per ordinary share1 (39.0) (10.9) Net asset backing per ordinary share 110.6 162.6 1 If right-of-use assets are included then the net tangible assets backing per share is (25.8) cents (2019: N/A). -

April 2009 Bulletinfeature Articles | Interviews | News | Book Reviews | Calendar L 2009 Meteorological Services E 58 (2) - APRI

Vol. 58 (2) - April 2009 BulletinFeature articles | Interviews | News | Book reviews | Calendar www.wmo.int 2009 L Meteorological services 58 (2) - APRI E VOLUM for transportation Meteorology and marine transportation 111 Weather monitoring and etin forecasting services for BULL provincial highways and MO railways in China W 118 World Meteorological Organization 7bis, avenue de la Paix - Case postale 2300 - CH-1211 Geneva 2 - Switzerland Tel.: +41 (0) 22 730 81 11 - Fax: +41 (0) 22 730 81 81 E-mail: [email protected] - Website: www.wmo.int Weather and climate change ISSN 0042-9767 implications for surface transportation in the USA 84 Meteorological services to aviation 94 Meteorology for travellers 104 Weather affects the operation of the transportation systems that we all rely on ... Climate, on the other hand, affects transportation infrastructure. M. McGuirk et al. Bulletin The journal of the Contents World Meteorological Organization In this issue .......................................................................................... 80 Volume 58 (2) - Avril 2009 World Climate Conference-3 .............................................................. 82 Secretary-General M. Jarraud Weather and climate change implications for surface Deputy Secretary-General Hong Yan transportation in the USA by Marjorie McGuirk, Scott Shuford, Assistant Secretary-General J. Lengoasa Thomas C. Peterson and Paul Pisano ............................................................... 84 The WMO Bulletin is published quarterly (January, April, July, October) in English, French, Meteorological services to aviation by Chi Ming Shun, Ian Lisk, Russian and Spanish editions. Carr McLeod and Kevin L. Johnston ............................................................ 94 Editor Hong Yan Associate Editor Judith C.C. Torres Meteorology for travellers by S.T. Christopher ........................................ 104 Editorial board Hong Yan (Chair) Meteorology and marine transportation by Peter Dexter and J. -

Engineers Australia Sydney Division Water Engineering Panel

Engineers Australia Sydney Division Water Engineering Panel REAL-TIME QUANTITATIVE RAINFALL FORECASTING WHERE ARE WE AND WHERE ARE WE HEADING Abstract: Weather prediction and specifically forecasting rainfall in the near term has made significant strides in the last decade. This has largely been due to advances in science and computer power, with several agencies commanding supercomputers in the top 50 in the world. However, rainfall still remains one of the most difficult parameters to forecast even out to 12 hours. The intrinsic problems with forecasting rainfall over other such parameters such as temperature and winds, is its often very chaotic nature both temporally and geographically. Even with global supercomputers modelling at greater resolutions, few are capable of providing the pinpoint accuracy often required by rainfall sensitive industries and projects. The aim of this talk is to provide an industry-wide overview on current science and forecasting techniques with regard to rainfall, with a special focus on the very latest techniques for trying to improve and correct forecast data provided by the global computer models. The example of the Chatswood Integrated Flood Control and Stormwater Reuse Scheme shall be used as a case study of how such techniques may be applied to vastly enhance rainfall forecasting accuracy. In addition, the talk will touch on how these forecast techniques can be used across the industry as a whole, as well as a quick look into expected future developments. Speaker Bio: Martin Palmer spent nine years in the British Royal Navy as a Warfare Officer, specialising as a Meteorologist, Oceanographer and Hydrographic Surveyor. -

Social Media Thought Leaders Updated for the 45Th Parliament 31 August 2016 This Barton Deakin Brief Lists

Barton Deakin Brief: Social Media Thought Leaders Updated for the 45th Parliament 31 August 2016 This Barton Deakin Brief lists individuals and institutions on Twitter relevant to policy and political developments in the federal government domain. These institutions and individuals either break policy-political news or contribute in some form to “the conversation” at national level. Being on this list does not, of course, imply endorsement from Barton Deakin. This Brief is organised by categories that correspond generally to portfolio areas, followed by categories such as media, industry groups and political/policy commentators. This is a “living” document, and will be amended online to ensure ongoing relevance. We recognise that we will have missed relevant entities, so suggestions for inclusions are welcome, and will be assessed for suitability. How to use: If you are a Twitter user, you can either click on the link to take you to the author’s Twitter page (where you can choose to Follow), or if you would like to follow multiple people in a category you can click on the category “List”, and then click “Subscribe” to import that list as a whole. If you are not a Twitter user, you can still observe an author’s Tweets by simply clicking the link on this page. To jump a particular List, click the link in the Table of Contents. Barton Deakin Pty. Ltd. Suite 17, Level 2, 16 National Cct, Barton, ACT, 2600. T: +61 2 6108 4535 www.bartondeakin.com ACN 140 067 287. An STW Group Company. SYDNEY/MELBOURNE/CANBERRA/BRISBANE/PERTH/WELLINGTON/HOBART/DARWIN -

Scheme Booklet Registered with Asic

QMS Media Limited 214 Park Street South Melbourne, VIC 3205 T +61 3 9268 7000 www.qmsmedia.com ASX Release 13 December 2019 SCHEME BOOKLET REGISTERED WITH ASIC QMS Media Limited (ASX:QMS) refers to its announcement dated 12 December 2019 in which it advised that the Federal Court had made orders approving: • the dispatch of a Scheme Booklet to QMS shareholders in relation to the previously announced Scheme of Arrangement with Shelley BidCo Pty Ltd, an entity controlled by Quadrant Private Entity and its institutional partners (Scheme); and • the convening of meetings of QMS shareholders to consider and vote on the Scheme. The Scheme Booklet has been registered today by the Australian Securities and Investments Commission. A copy of the Scheme Booklet, including the Independent Expert's Report and the notices of the Scheme Meetings, is attached to this announcement and will be dispatched to QMS' shareholders before Thursday 19 December 2019. Key events and indicative dates The key events (and expected timing of these) in relation to the approval and implementation of the Scheme are as follows: Event Date Scheme Booklet dispatched to QMS shareholders Before Thursday 19 December 2019 General Scheme Meeting 10.00am on Thursday 6 February 2020 Rollover Shareholders Scheme Meeting Thursday 6 February (immediately following the General Scheme Meeting) Second Court Hearing Monday 10 February 2020 Effective Date Tuesday 11 February 2020 Scheme Record Date 5.00pm on Friday 14 February 2020 Implementation Date Friday 21 February 2020 Note: All dates following the date of the General Scheme Meeting and the Rollover Shareholders Scheme Meeting are indicative only and, among other things, are subject to all necessary approvals from the Court and any other regulatory authority and satisfaction or (if permitted) waiver of all conditions precedent in the Scheme Implementation Deed. -

Australian Share Exemption List

Business Ngā Ūmanga IR871 | June 2016 Australian share exemption list This factsheet provides the names of companies (excluding listed investment companies) that are considered to meet the exemption from the FIF (foreign investment fund) rules for the year ending 31 March 2016. Companies are listed alphabetically by company name. Where a company has been added to, or removed from, one of the qualifying indices of the Australian stock exchange (ASX) in the year to 31 March 2016, a date is shown in the appropriate column. Qualifying listed investment companies (LICs) are part of the FTSE AFSA Australia Listed Investment Companies (LIC) Index which is owned and operated by FTSE (Financial Times Stock Exchange). Because the LIC index is no longer in the public domain, we’ve removed LICs from this factsheet. You’ll need to contact the investment company or the FTSE to confirm whether your investment is part of the LIC Index. 0–9 ASX Company name Date Date ticker added removed ASX Company name Date Date code ticker added removed APD APN Property Group Ltd 21/03/16 code ARB ARB Corp Ltd ONT 1300 Smiles Ltd ALL Aristocrat Leisure Ltd 3PL 3P Learning Ltd AWN Arowana International Ltd 21/03/16 A ARI Arrium Ltd ACX Aconex Ltd AHY Asaleo Care Ltd ACR Acrux Ltd AIO Asciano Ltd ADA Adacel Technologies Ltd 21/03/16 AFA ASF Group Ltd ADH Adairs Ltd 21/09/15 ASZ ASG Group Ltd ABC Adelaide Brighton Ltd ASH Ashley Services Group Ltd 21/03/16 AHZ Admedus Ltd ASX ASX Ltd ADJ Adslot Ltd 21/03/16 AGO Atlas Iron Ltd 21/03/16 AFJ Affinity Education Group 2/12/15