Switzerland, Liechtenstein; Business Study Touche Ross International

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Liechtenstein

G:\UNO\BERICHTE\Frauen\Vierter Länderbericht\4. Länderbericht-en.doc LIECHTENSTEIN Fourth PERIODIC REPORT submitted under article 18 of the Convention on the Elimination of All Forms of Discrimination against Women of 18 December 1979 Vaduz, 11 August 2009 RA 2009/1874 2 Table of contents FOREWORD .................................................................................................................................................. 3 I. OVERVIEW OF LIECHTENSTEIN........................................................................................................... 4 1. Political and social structures.................................................................................................4 2. Legal and institutional framework .........................................................................................5 II. INTRODUCTION .................................................................................................................................. 8 The situation of women in Liechtenstein and implementation of the Beijing Platform for Action ...............8 III. REMARKS ON THE INDIVIDUAL ARTICLES OF THE CONVENTION ..................................................... 9 Article 2 Policy measures to eliminate discrimination against women ................................................9 Article 3 Ensuring the full development and advancement of women...............................................18 Article 4 Positive measures to accelerate de facto equality ...............................................................19 -

LIECHTENSTEIN the 341 © Lonely Planet Publications Planet Lonely © Malbun Triesenberg Schloss Vaduz Trail LANGUAGE: GERMAN LANGUAGE: Fürstensteig

© Lonely Planet Publications 341 Liechtenstein If Liechtenstein didn’t exist, someone would have invented it. A tiny mountain principality governed by an iron-willed monarch in the heart of 21st-century Europe, it certainly has novelty value. Only 25km long by 12km wide (at its broadest point) – just larger than Man- hattan – Liechtenstein doesn’t have an international airport, and access from Switzerland is by local bus. However, the country is a rich banking state and, we are told, the world’s largest exporter of false teeth. Liechtensteiners sing German lyrics to the tune of God Save the Queen in their national anthem and they sure hope the Lord preserves their royals. Head of state Prince Hans Adam II and his son, Crown Prince Alois, have constitutional powers unmatched in modern Europe but most locals accept this situation gladly, as their monarchs’ business nous and, perhaps also, tourist appeal, help keep this landlocked sliver of a micro-nation extremely prosperous. Most come to Liechtenstein just to say they’ve been, and tour buses disgorge day- trippers in search of souvenir passport stamps. If you’re going to make the effort to come this way, however, it’s pointless not to venture further, even briefly. With friendly locals and magnificent views, the place comes into its own away from soulless Vaduz. In fact, the more you read about Fürstentum Liechtenstein (FL) the easier it is to see it as the model for Ruritania – the mythical kingdom conjured up in fiction as diverse as The Prisoner of Zenda and Evelyn Waugh’s Vile Bodies. -

Liechtenstein Financial Market

Financial Market, Entrepreneurial Economy and Studying Finance Prof. Dr. Marco J. Menichetti Chair in Business Administration, Banking and Financial Management Institute for Finance [email protected] October 2017 Outline What is a Financial Market? Liechtenstein: Entrepreneurial Economy and Financial Market Studying Finance in Connection with an Asset Management Hub Menichetti, October 2017 2 Outline What is a Financial Market? Liechtenstein: Entrepreneurial Economy and Financial Market Studying Finance connected to an important Asset Management Hub Menichetti, October 2017 3 What is a Financial Market? Financial Financial Intermediaries/ Centers Institutions Financial Markets Regulation and Market Supervision Menichetti, October 2017 4 Financial Markets Financial Markets • Bond Markets • Stock Markets • Foreign Exchange Markets • Markets for Alternative Investments • International Financial Markets Structure of Financial Markets • Primary and Secondary Markets • Exchanges and Over-the Counter Markets • Money and Capital Markets • Spot and Forward Markets Source: Mishkin & Eakins (2016). Menichetti, October 2017 5 Financial Center Geographical location (1) that has a heavy concentration of financial institutions, (2) that offers a highly developed commercial and communications infrastructure, and (3) where a great number of domestic and international trading transactions are conducted. London, New York, and Tokyo are the world's premier financial centers. • Regional, national, international financial center • Global financial center: direct access from all over the world • Niche financial centers: Corporate Finance, Asset Management, FX, Derivatives, Trade Finance, Project Finance etc. • Onshore vs. offshore financial centers Source: Zomoré (2007); Mishkin & Eakins (2016). Menichetti, October 2017 6 Leading Wealth Management Centers (2015) - International Private Client Market Volume MARKET VOLUME (IN USD TRILLION AND AS PERCENTAGE OF MARKET SHARE) Source: Deloitte (2015). -

Graubünden for Mountain Enthusiasts

Graubünden for mountain enthusiasts The Alpine Summer Switzerland’s No. 1 holiday destination. Welcome, Allegra, Benvenuti to Graubünden © Andrea Badrutt “Lake Flix”, above Savognin 2 Welcome, Allegra, Benvenuti to Graubünden 1000 peaks, 150 valleys and 615 lakes. Graubünden is a place where anyone can enjoy a summer holiday in pure and undisturbed harmony – “padschiifik” is the Romansh word we Bündner locals use – it means “peaceful”. Hiking access is made easy with a free cable car. Long distance bikers can take advantage of luggage transport facilities. Language lovers can enjoy the beautiful Romansh heard in the announcements on the Rhaetian Railway. With a total of 7,106 square kilometres, Graubünden is the biggest alpine playground in the world. Welcome, Allegra, Benvenuti to Graubünden. CCNR· 261110 3 With hiking and walking for all grades Hikers near the SAC lodge Tuoi © Andrea Badrutt 4 With hiking and walking for all grades www.graubunden.com/hiking 5 Heidi and Peter in Maienfeld, © Gaudenz Danuser Bündner Herrschaft 6 Heidi’s home www.graubunden.com 7 Bikers nears Brigels 8 Exhilarating mountain bike trails www.graubunden.com/biking 9 Host to the whole world © peterdonatsch.ch Cattle in the Prättigau. 10 Host to the whole world More about tradition in Graubünden www.graubunden.com/tradition 11 Rhaetian Railway on the Bernina Pass © Andrea Badrutt 12 Nature showcase www.graubunden.com/train-travel 13 Recommended for all ages © Engadin Scuol Tourismus www.graubunden.com/family 14 Scuol – a typical village of the Engadin 15 Graubünden Tourism Alexanderstrasse 24 CH-7001 Chur Tel. +41 (0)81 254 24 24 [email protected] www.graubunden.com Gross Furgga Discover Graubünden by train and bus. -

Switzerland 4Th Periodical Report

Strasbourg, 15 December 2009 MIN-LANG/PR (2010) 1 EUROPEAN CHARTER FOR REGIONAL OR MINORITY LANGUAGES Fourth Periodical Report presented to the Secretary General of the Council of Europe in accordance with Article 15 of the Charter SWITZERLAND Periodical report relating to the European Charter for Regional or Minority Languages Fourth report by Switzerland 4 December 2009 SUMMARY OF THE REPORT Switzerland ratified the European Charter for Regional or Minority Languages (Charter) in 1997. The Charter came into force on 1 April 1998. Article 15 of the Charter requires states to present a report to the Secretary General of the Council of Europe on the policy and measures adopted by them to implement its provisions. Switzerland‘s first report was submitted to the Secretary General of the Council of Europe in September 1999. Since then, Switzerland has submitted reports at three-yearly intervals (December 2002 and May 2006) on developments in the implementation of the Charter, with explanations relating to changes in the language situation in the country, new legal instruments and implementation of the recommendations of the Committee of Ministers and the Council of Europe committee of experts. This document is the fourth periodical report by Switzerland. The report is divided into a preliminary section and three main parts. The preliminary section presents the historical, economic, legal, political and demographic context as it affects the language situation in Switzerland. The main changes since the third report include the enactment of the federal law on national languages and understanding between linguistic communities (Languages Law) (FF 2007 6557) and the new model for teaching the national languages at school (—HarmoS“ intercantonal agreement). -

©Copyright 2017 Yu Sasaki Precocious Enough to Rationalize Culture? Explaining the Success and Failure of Nation-Building in Europe, 1400–2000

©Copyright 2017 Yu Sasaki Precocious Enough to Rationalize Culture? Explaining the Success and Failure of Nation-building in Europe, 1400–2000 Yu Sasaki A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy University of Washington 2017 Reading Committee: Anthony Gill, Chair Edgar Kiser Victor Menaldo Steven Pfaff Program Authorized to Offer Degree: Department of Political Science University of Washington Abstract Precocious Enough to Rationalize Culture? Explaining the Success and Failure of Nation-building in Europe, 1400–2000 Yu Sasaki Chair of the Supervisory Committee: Professor Anthony Gill Political Science Why do some ethnic groups consolidate their cultural practices earlier than others? Extant schol- arship in ethnicity, nations, and state-building hypothesizes that the state is the most important determinant. In my dissertation, I argue that it is not the only channel and there are other fac- tors that matter. In three standalone essays, I investigate the role of (1) geography, (2) technology, and (3) public goods provision at the ethnic-group level. I provide a simple conceptual frame- work of how each of these determinants affects cultural consolidation for ethnic groups. I argue that geographical conditions and technology adoption can have a positive impact on ethnic groups’ ability to develop unique cultural attributes without an independent state. Although they may be politically incorporated by stronger groups in the modern period, they still demand self-rule or standardize their vernacular. I also argue that, in contrast with the expectation from the political economy research on ethnicity, cultural consolidation does not always yield public goods provision at the ethnic-group level. -

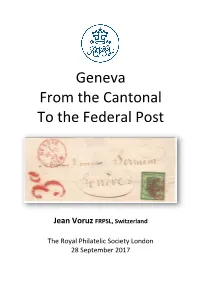

Geneva from the Cantonal to the Federal Post

Geneva From the Cantonal To the Federal Post Jean Voruz FRPSL, Switzerland The Royal Philatelic Society London 28 September 2017 Front cover illustration On 1 st October 1849, the cantonal posts are reorganized and the federal post is created. The Geneva cantonal stamps are still valid, but the rate for local letters is increased from 5 to 7 cents. As the "Large Eagle" with a face value of 5c is sold at the promotional price of 4c, additional 3c is required, materialized here by the old newspapers stamp. One of the two covers being known dated on the First Day of the establishment of the Federal Service. 2 Contents Frames 1 - 2 Cantonal Post Local Mail Frame 2 Cantonal Post Distant Mail Frame 3 Cantonal Post Sardinian & French Mail Frame 4 Transition Period Nearest Cent Frames 4 - 6 Transition Period Other Phases Frame 7 Federal Post Local Mail Frame 8 Federal Post Distant Mail Frames 9 - 10 Federal Post Sardinian & French Mail Background Although I started collecting stamps in 1967 like most of my classmates, I really entered the structured philately in 2005. That year I decided to display a few sheets of Genevan covers at the local philatelic society I joined one year before. Supported by my new friends - especially Henri Grand FRPSL who was one of the very best specialists of Geneva - I went further and got my first FIP Large Gold medal at London 2010 for the postal history collection "Geneva Postal Services". Since then the collection received the FIP Grand Prix International at Philakorea 2014 and the FEPA Grand Prix Finlandia 2017. -

A New Challenge for Spatial Planning: Light Pollution in Switzerland

A New Challenge for Spatial Planning: Light Pollution in Switzerland Dr. Liliana Schönberger Contents Abstract .............................................................................................................................. 3 1 Introduction ............................................................................................................. 4 1.1 Light pollution ............................................................................................................. 4 1.1.1 The origins of artificial light ................................................................................ 4 1.1.2 Can light be “pollution”? ...................................................................................... 4 1.1.3 Impacts of light pollution on nature and human health .................................... 6 1.1.4 The efforts to minimize light pollution ............................................................... 7 1.2 Hypotheses .................................................................................................................. 8 2 Methods ................................................................................................................... 9 2.1 Literature review ......................................................................................................... 9 2.2 Spatial analyses ........................................................................................................ 10 3 Results ....................................................................................................................11 -

Langwies Abfahrt Partenza Departure Départ Live-Anzeige 13

Langwies Abfahrt Partenza Departure Départ Live-Anzeige 13. Dezember 2020 - 11. Dezember 2021 05:00 12:00 19:00 01:00 Zeit Linie Zielort Zeit Linie Zielort Zeit Linie Zielort Zeit Linie Zielort R 05:06 B a Chur, Bahnhofplatz 12:05 R , Chur 19:05 R Chur 01:17 B / 0 Chur, Bahnhofplatz Peist,Schulhaus 05:12 - St. Peter,Caflies 05:15 - Peist 12:13 - St. Peter-M. 12:17 - Lüen-C. 12:26 - Peist 19:13 - St. Peter-M. 19:17 - Lüen-C. 19:26 - a Peist,Schulhaus 01:25 - St. Peter, Gufa 01:26 - Pagig, Abzw. 05:18 - Castiel, Dorf 05:24 - Altstadt 12:44 - Chur 12:53 Altstadt 19:44 - Chur 19:53 £ n St. Peter,Caflies 01:30 - St. Peter,Rath. 01:30 - Maladers, alte Post 05:34 - Chur, Malteser 05:43 - 12:50 Arosa 19:50 Arosa Pagig, Abzw. 01:32 - Pagig, Pudanal 01:32 - Chur, Bahnhofpl. 05:48 R R Tura 01:33 - Castiel, Galgenbühl 01:37 - Litzirüti 12:56 - Arosa 13:09 Litzirüti 19:56 - Arosa 20:09 U 05:50 Arosa Castiel, Dorf 01:37 - Calfreisen, Abzw. 01:37 - R Calfreisen, Dorf 01:38 - Sax (Maladers) 01:42 - Litzirüti 05:56 - Arosa 06:09 13:00 20:00 Maladers, Dorf 01:46 - Maladers, Schule 01:46 - 06:00 Zeit Linie Zielort Zeit Linie Zielort Maladers, alte Post 01:48 - Maladers, Chisgruob 01:48 - Zeit Linie Zielort 13:05 R Chur 20:04 R Chur Maladers, Tumma 01:48 - Peist 13:13 - St. Peter-M. 13:17 - Lüen-C. 13:26 - Peist 20:11 - St. -

Mediendokumentation Skigebietsverbindung Arosa Lenzerheide

Mediendokumentation Skigebietsverbindung Arosa Lenzerheide Inhalt Baubericht Arosa Lenzerheide................................................................................................................... 2 Projektbeschrieb: Verbindungsbahn Hörnli-Urdenfürggli .......................................................................... 4 Projektbeschrieb: Erschliessungsbahnen Lenzerheide ................................................................................ 5 Wintermarke Arosa Lenzerheide (Marketingkonzept)............................................................................... 7 Wirtschaftliche Bedeutung der Skigebietsverbindung................................................................................ 8 Geschichte der Skigebietsverbindung........................................................................................................ 9 Tschiertschen............................................................................................................................................ 9 Baubericht Arosa Lenzerheide Die Idee einer Verbindung der beiden Skigebiete Arosa und Lenzerheide besteht seit den frühen 70er Jahren. Die geografisch eng beieinander liegenden Schneesportgebiete sind nur durch das Urdental von- einander getrennt. Die Distanz beträgt lediglich 2 km Luftlinie. Bereits am 1. Juni 2008 haben die Stimm- berechtigten der Gemeinde Arosa an der Urnenabstimmung mit 613 Ja zu 114 Nein der Skigebietsver- bindung Arosa Lenzerheide mit einem Ja-Anteil von 84.3% zugestimmt. Am 27. November 2011 ist -

Evidence from the Cantons of Switzerland

University of Zurich Department of Economics Working Paper Series ISSN 1664-7041 (print) ISSN 1664-705X (online) Working Paper No. 85 Improving Efficiency Through Consolidation of Jurisdictions? Evidence from the Cantons of Switzerland Philippe K. Widmer, George Elias and Peter Zweifel July 2012 Improving Efficiency Through Consolidation of Jurisdictions? Evidence from the Cantons of Switzerland Philippe K. Widmera,∗, George Eliasb, Peter Zweifela aUniversity of Zurich, Department of Economics, Switzerland bUniversity of Bern, Department of Economics, Switzerland Abstract The purpose of this paper is to analyze the optimal scale of local jurisdictions (cantons) in Switzerland applying Data Envelopment Analysis (DEA) to the years 2000 to 2004. Aggregate output performance indicators for four local government activities (administration, education, health, and transportation) are used to measure technical and scale efficiency and to derive DEA scores. Results show that these public services fail to exhibit economies of scale, undermining quests for centralization of public good provision while suggesting the possibility of Tiebout competition. Keywords: DEA, efficiency measurement, economies of scale, public good provision, Switzerland, JEL: C14, C67, H11, H72, H83 ∗ Corresponding author: Philippe Widmer, Department of Economics, University of Zurich, Hottingerstrasse 10, CH-8032 Zurich, Switzerland. Phone: +41 (0)79 732 50 42, Fax: +41 (0)62 205 15 80 87, E-mail: [email protected] July 5, 2012 1. Introduction The assignment of responsibilities to levels of government is an ongoing issue among fed- eral states worldwide. Some countries have a tradition of transferring additional responsibilities to their member states while others have pursued centralization or even have been delegating authority to supra-national institutions, as in the case of the European Union [see e.g. -

Switzerland in the 19Th Century

Switzerland in the 19th century The founding of the Swiss federal state ushered in a period of greater stability as regards both domestic and foreign affairs. The revised Constitution of 1874 extended the powers of the federal government and introduced the optional legislative referendum. Switzerland developed its system of direct democracy further and in 1891 granted the people the right of initiative on the partial revision of the Federal Constitution. That same year the Catholic conservatives – the losers of the Sonderbund war – celebrated, for the first time, the election of one of its representatives to the federal government. The federal state used its new powers to create favourable conditions for the development of a number of industries and service sectors (railways, machine construction and metalworking, chemicals, food industry and banking). These would become the mainstays of the Swiss economy. Not everyone in Switzerland reaped the benefits of the economic upturn. In the 19th century poverty, hunger and a lack of job prospects drove many Swiss people to seek their fortunes elsewhere, particularly in North and South America. At home, industrial towns and cities saw an influx of rural and, increasingly, foreign migrants. Living conditions for many members of this new urban working class were often precarious. Foreign policy During the wave of revolution that engulfed Europe in the early 1850s, relations between Switzerland and Austria, which also ruled northern Italy, were extremely tense. Many Italians, who wanted to see a united and independent Italy (Risorgimento), sought refuge in liberal- run Ticino. The local community sympathised with their cause, some even fighting alongside their Italian comrades or smuggling weapons for them.