Best Bank M&A Deals

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

JP Morgan Chase Sofya Frantslikh Pace University

Pace University DigitalCommons@Pace Honors College Theses Pforzheimer Honors College 3-14-2005 Mergers and Acquisitions, Featured Case Study: JP Morgan Chase Sofya Frantslikh Pace University Follow this and additional works at: http://digitalcommons.pace.edu/honorscollege_theses Part of the Corporate Finance Commons Recommended Citation Frantslikh, Sofya, "Mergers and Acquisitions, Featured Case Study: JP Morgan Chase" (2005). Honors College Theses. Paper 7. http://digitalcommons.pace.edu/honorscollege_theses/7 This Article is brought to you for free and open access by the Pforzheimer Honors College at DigitalCommons@Pace. It has been accepted for inclusion in Honors College Theses by an authorized administrator of DigitalCommons@Pace. For more information, please contact [email protected]. Thesis Mergers and Acquisitions Featured Case Study: JP Morgan Chase By: Sofya Frantslikh 1 Dedicated to: My grandmother, who made it her life time calling to educate people and in this way, make their world better, and especially mine. 2 Table of Contents 1) Abstract . .p.4 2) Introduction . .p.5 3) Mergers and Acquisitions Overview . p.6 4) Case In Point: JP Morgan Chase . .p.24 5) Conclusion . .p.40 6) Appendix (graphs, stats, etc.) . .p.43 7) References . .p.71 8) Annual Reports for 2002, 2003 of JP Morgan Chase* *The annual reports can be found at http://www.shareholder.com/jpmorganchase/annual.cfm) 3 Abstract Mergers and acquisitions have become the most frequently used methods of growth for companies in the twenty first century. They present a company with a potentially larger market share and open it u p to a more diversified market. A merger is considered to be successful, if it increases the acquiring firm’s value; m ost mergers have actually been known to benefit both competition and consumers by allowing firms to operate more efficiently. -

Largest Community Banks in the Southeast

Largest Community Banks in the Southeast Rank Institution Name Ticker State Total Assets ($mm) Total Deposits ($mm) 1 BankUnited, Inc. BKU FL $17,681 $12,834 2 United Bankshares, Inc. UBSI WV $12,085 $8,753 3 WesBanco, Inc.* WSBC WV $8,224 $6,438 4 South State Corporation SSB SC $7,880 $6,518 5 United Community Banks, Inc. UCBI GA $7,526 $6,241 6 Union Bankshares Corporation UBSH VA $7,194 $5,634 7 Capital Bank Financial Corp. CBF FL $6,690 $5,175 8 TowneBank* TOWN VA $6,083 $4,534 9 FCB Financial Holdings, Inc. FCB FL $6,055 $3,991 10 Pinnacle Financial Partners, Inc. PNFP TN $5,866 $4,662 11 BNC Bancorp* BNCN NC $4,919 $4,033 12 Carter Bank & Trust CARE VA $4,679 $4,272 13 Yadkin Financial Corporation YDKN NC $4,179 $3,185 14 ServisFirst Bancshares, Inc.* SFBS AL $4,176 $3,549 15 Ameris Bancorp ABCB GA $3,999 $3,373 16 Community Trust Bancorp, Inc. CTBI KY $3,670 $2,902 17 CenterState Banks, Inc. CSFL FL $3,639 $3,066 18 Republic Bancorp, Inc. RBCAA KY $3,626 $2,060 19 City Holding Company CHCO WV $3,385 $2,793 20 State Bank Financial Corporation* STBZ GA $3,353 $2,730 Community banks^ headquartered in AL, FL, GA, KY, NC, SC, TN, VA or WV ranked by Total Assets (including pending and recently completed acquisitions) as of 9/30/14 * Pro forma for pending acquisitions and/or acquisitions completed since 9/30/14 ^ Community banks defined as banks with less than $20B in total assets Sources: SNL Financial & Banks Street Partners 1 Largest Community Banks in Virginia & the Carolinas Rank Institution Name Ticker State Total Assets ($mm) Total Deposits ($mm) 1 South State Corporation SSB SC $7,896 $6,518 2 Union Bankshares Corporation UBSH VA $7,194 $5,634 3 TowneBank# TOWN VA $6,083 $4,534 4 BNC Bancorp* BNCN NC $4,919 $4,033 5 Carter Bank & Trust CARE VA $4,679 $4,272 6 Yadkin Financial Corporation YDKN NC $4,179 $3,185 7 Cardinal Financial Corporation CFNL VA $3,315 $2,425 8 First Bancorp FBNC NC $3,196 $2,679 9 Square 1 Financial, Inc. -

Fhlbiamendcomplrescissiond

ALLY FINANCIAL INC. f/k/a GMAC, INC.; ) GS MORTGAGE SECURITIES CORP.; ) GOLDMAN, SACHS & CO.; GOLDMAN ) SACHS MORTGAGE COMPANY; THE ) GOLDMAN SACHS GROUP, INC.; ) RBS SECURITIES INC. f/k/a GREENWICH ) CAPITAL MARKETS, INC.; INDYMAC ) MBS, INC.; J.P. MORGAN ACCEPTANCE ) CORPORATION I; J.P. MORGAN ) SECURITIES INC.; JPMORGAN ) SECURITIES HOLDINGS LLC; ) JPMORGAN CHASE & CO.; CHASE ) MORTGAGE FINANCE CORPORATION; ) UBS SECURITIES LLC; WAMU ASSET ) ACCEPTANCE CORP.; WAMU CAPITAL ) CORP.; WELLS FARGO ASSET ) SECURITIES CORPORATION; WELLS ) FARGO BANK, NATIONAL ) ASSOCIATION; WELLS FARGO & ) COMPANY, and JOHN DOE ) DEFENDANTS, 1-50, ) ) Defendants. ) Table of Contents I. NATURE OF THE ACTION ........................................................................................... 1 II. EXECUTIVE SUMMARY .............................................................................................. 2 A. PMLBS Defined.................................................................................................... 2 B. The Bank Purchased Only the Highest Rated (Triple-A-Rated) PLMBS ................................................................................................................. 3 C. The Mortgage Originators Who Issued Loans Backing the Certificates Abandoned Underwriting Guidelines and Issued Loans Without Ensuring the Borrowers’ Ability to Pay and Without Sufficient Collateral.............................................................................................. 4 D. The Defendants Provided Misleading Information About -

First Horizon's Supplement to Their Application to the Federal Reserve

SUPPLEMENT TO THE APPLICATION TO THE BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM RELATING TO THE PROPOSED ACQUISITION OF CAPITAL BANK FINANCIAL CORP. BY FIRST HORIZON NATIONAL CORPORATION AND FIRESTONE SUB, INC. PURSUANT TO SECTIONS 3(a)(2), 3(a)(3) AND 3(a)(5) OF THE BANK HOLDING COMPANY ACT OF 1956, AS AMENDED, AND REGULATION Y PROMULGATED THEREUNDER August 2, 2017 RESPONSES OF FIRST HORIZON NATIONAL CORPORATION TO THE REQUEST FOR ADDITIONAL INFORMATION Set forth below are the responses of First Horizon National Corporation (“First Horizon”) to the Board of Governors of the Federal Reserve System staff’s request for additional information, dated July 14, 2017, relating to First Horizon’s application (the “Application”) pursuant to Section 3 of the Bank Holding Company Act of 1956, as amended (the “BHC Act”), for prior approval to merge with Capital Bank Financial Corp. (“CBFC”), and thereby indirectly acquire Capital Bank Corp. (“Capital Bank”). Preceding each response, the related question is restated in bold. Capitalized terms not otherwise defined herein shall have the meanings set forth in the Application. 1. Provide current and pro forma shareholders lists for First Horizon that specifically identify any shareholder or group of shareholders that would own or control, directly or indirectly, 5 percent or more of any class of voting securities, or 10 percent or more of the total equity, of First Horizon both before and after consummation of the proposed transaction. In calculating the voting ownership, include any warrants, options, and other convertible instruments, and show all levels of voting ownership on both a fully diluted and an individually diluted basis. -

First Horizon Corporation Annual Report 2021

First Horizon Corporation Annual Report 2021 Form 10-K (NYSE:FHN) Published: February 25th, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 - or - ☐ TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 SECURITIES EXCHANGE ACT OF 1934 For the Transition period from __________ to__________ Commission File Number: 001-15185 fhn-20201231_g1.jpg FIRST HORIZON CORPORATION (Exact name of registrant as specified in its charter) TN 62-0803242 (State or other jurisdiction (IRS Employer incorporation of organization) Identification No.) 165 Madison Avenue Memphis, Tennessee 38103 (Address of principal executive office) (Zip Code) Registrant’s telephone number, including area code: 901-523-4444 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol(s) Name of Exchange on which Registered $.625 Par Value Common Capital Stock FHN New York Stock Exchange LLC Depositary Shares, each representing a 1/4,000th interest in a share of Non-Cumulative Perpetual Preferred Stock, Series A FHN PR A New York Stock Exchange LLC Depositary Shares, each representing a 1/400th interest in FHN PR B New York Stock Exchange LLC a share of Non-Cumulative Perpetual Preferred Stock, Series B Depositary Shares, each representing a 1/400th interest in FHN PR C New York -

Global Payments, Inc. (GPN) J.P

Corrected Transcript 14-Nov-2017 Global Payments, Inc. (GPN) J.P. Morgan Ultimate Services Investor Conference Total Pages: 18 1-877-FACTSET www.callstreet.com Copyright © 2001-2017 FactSet CallStreet, LLC Global Payments, Inc. (GPN) Corrected Transcript J.P. Morgan Ultimate Services Investor Conference 14-Nov-2017 CORPORATE PARTICIPANTS Tien-Tsin Huang Analyst, JPMorgan Securities LLC Jeffrey Steven Sloan Chief Executive Officer & Director, Global Payments, Inc. ...................................................................................................................................................................................................................................................... MANAGEMENT DISCUSSION SECTION Tien-Tsin Huang Analyst, JPMorgan Securities LLC Thanks, everybody for joining. My name is Tien-Tsin Huang; cover the Payments and IT Services Group at JPMorgan and super-excited and delighted to have Jeff Sloan back with us, CEO of Global Payments, [indiscernible] (00:14) always busy – we respect having him here again. So thank you. So what we'll do is, we'll have Q&A, I'll field it as I always do. I took a lot of questions from you guys and pieced it together. We'll go through some of these and then we'll open it up for Q&A. ...................................................................................................................................................................................................................................................... QUESTION AND ANSWER SECTION Tien-Tsin -

Capital Bank Financial Corp. Stockholder

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF NORTH CAROLINA STEPHEN BUSHANSKY, On Behalf of Himself and All Others Similarly Situated, Case No. Plaintiff, v. CLASS ACTION COMPLAINT CAPITAL BANK FINANCIAL CORP., R. EUGENE TAYLOR, MARTHA M. BACHMAN, JURY TRIAL DEMANDED RICHARD M. DEMARTINI, PETER N. FOSS, WILLIAM A. HODGES, SCOTT B. KAUFFMAN, OSCAR A. KELLER III, MARC D. OKEN, ROBERT L. REID, and WILLIAM G. WARD SR., Defendants, Plaintiff Stephen Bushansky ("Plaintiff'), by and through his undersigned counsel, for his complaint against defendants, alleges upon personal knowledge with respect to himself, and as to all other upon information and belief based upon, inter alia, the investigation of counsel allegations herein, as follows: NATURE OF THE ACTION 1. Plaintiff brings this class action on behalf of the public stockholders of Capital Bank Financial Corp. ("Capital Bank" or the "Company") against Capital Bank and the members of Capital Bank's Board of Directors (the "Board" or the "Individual Defendants") for their violations of Section 14(a) and 20(a) of the Securities Exchange Act of 1934 (the "Exchange Act"), 15.U.S.C. 78n(a), 78t(a), and U.S. Securities and Exchange Commission ("SEC") Rule 14a-9, 17 C.F.R. 240.14a-9, arising out of their attempt to sell the Company to First Horizon National Corporation ("First Horizon") (the "Proposed Transaction"). 2. On May 4, 2017, Capital Bank issued a press release announcing it had entered 1 Case 3:17-cv-00422 Document 1 Filed 07/17/17 Page 1 of 26 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF NORTH CAROLINA STEPHEN BUSHANSKY, On Behalf of Himself and All Others Similarly Situated, Case No. -

IN the UNITED STATES DISTRICT COURT for the SOUTHERN DISTRICT of TEXAS HOUSTON DIVISION MARGARITA VILLAGRAN, § § Plaintiff, §

Case 4:05-cv-02685 Document 75 Filed in TXSD on 10/23/07 Page 1 of 43 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION MARGARITA VILLAGRAN, § § Plaintiff, § v. § CIVIL ACTION NO. H-05-2685 § CENTRAL FORD, INC., § § Defendant. § MEMORANDUM AND OPINION Margarita Villagran sues on her own behalf and on behalf of a class of people sent mailings by Central Ford, Inc., an automobile dealership. Villagran alleges that the mailings violated the Fair Credit Reporting Act (FCRA), 15 U.S.C. § 1681 et seq., because they used information obtained without authorization from the addressees’ credit reports, for a purpose not permitted under the Act. The FCRA allows companies such as Central Ford to use information obtained from consumers’ credit reports for communications that extend “firm offers of credit.” The FCRA prohibits the use of such information to advertise rather than extend “firm offers of credit.” Villagran alleges that the mailing she and others received did not extend a “firm offer of credit.” She seeks damages under 15 U.S.C. § 1681n(a), which provides that for each violation, the consumer may recover “any actual damages sustained by the consumer as a result of [a violation] or damages of not less than $100 and not more than $1,000,” punitive damages, attorney’s fees, and costs. Villagran has amended her motion to certify a class action, (Docket Entry No. 55); Case 4:05-cv-02685 Document 75 Filed in TXSD on 10/23/07 Page 2 of 43 Central Ford has responded, (Docket Entry No. -

Powerline Plans

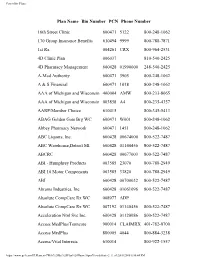

Powerline Plans Plan Name Bin Number PCN Phone Number 16th Street Clinic 600471 5122 800-248-1062 170 Group Insurance Benefits 610494 9999 800-788-7871 1st Rx 004261 CRX 800-964-2531 4D Clinic Plan 006037 810-540-2425 4D Pharmacy Management 600428 01990000 248-540-2425 A-Med Authority 600471 3905 800-248-1062 A & S Financial 600471 1018 800-248-1062 AAA of Michigan and Wisconsin 400004 AMW 800-233-8065 AAA of Michigan and Wisconsin 003858 A4 800-235-4357 AARP/Member Choice 610415 800-345-5413 ABAG Golden Gate Brg WC 600471 W001 800-248-1062 Abbey Pharmacy Network 600471 1451 800-248-1062 ABC Liquors, Inc. 600428 00674000 800-522-7487 ABC Warehouse,Detroit MI 600428 01140456 800-522-7487 ABCRC 600428 00677003 800-522-7487 ABI - Humphrey Products 003585 23070 800-788-2949 ABI 10 Motor Components 003585 33820 800-788-2949 ABI 600428 00700032 800-522-7487 Abrams Industries, Inc. 600428 01061096 800-522-7487 Absolute CompCare Rx WC 008977 ADP Absolute CompCare Rx WC 007192 01140456 800-522-7487 Acceleration Ntnl Svc Inc. 600428 01120086 800-522-7487 Access MedPlus/Tenncare 900014 CLAIMRX 401-782-0700 Access MedPlus 880005 4044 800-884-3238 Access/Vital Interests 610014 800-922-1557 https://www.qs1.com/PLPlans.nsf/Web%20By%20Plan%20Name!OpenView&Start=2 (1 of 2)8/8/2006 6:50:44 PM Powerline Plans Accident Fund of Michigan 600428 00700054 800-522-7487 Accubank Mortgage Inc 600428 00672018 800-522-7487 Aclaim 005848 800-422-5246 ACMG Employers Health Plan 400004 ACM 800-233-8065 Acordia Sr Benefits Horizons 600428 00790015 800-522-7487 https://www.qs1.com/PLPlans.nsf/Web%20By%20Plan%20Name!OpenView&Start=2 (2 of 2)8/8/2006 6:50:44 PM Powerline Plans Plan Name Bin Number PCN Phone Number Acordia Sr Benefits Horizons 600428 00790015 800-522-7487 ACT Industries, Inc. -

List of Participating Merchants Mastercard Automatic Billing Updater

List of Participating Merchants MasterCard Automatic Billing Updater 3801 Agoura Fitness 1835-180 MAIN STREET SUIT 247 Sports 5378 FAMILY FITNESS FREE 1870 AF Gilroy 2570 AF MAPLEWOOD SIMARD LIMITED 1881 AF Morgan Hill 2576 FITNESS PREMIER Mant (BISL) AUTO & GEN REC 190-Sovereign Society 2596 Fitness Premier Beec 794 FAMILY FITNESS N M 1931 AF Little Canada 2597 FITNESS PREMIER BOUR 5623 AF Purcellville 1935 POWERHOUSE FITNESS 2621 AF INDIANAPOLIS 1 BLOC LLC 195-Boom & Bust 2635 FAST FITNESS BOOTCAM 1&1 INTERNET INC 197-Strategic Investment 2697 Family Fitness Holla 1&1 Internet limited 1981 AF Stillwater 2700 Phoenix Performance 100K Portfolio 2 Buck TV 2706 AF POOLER GEORGIA 1106 NSFit Chico 2 Buck TV Internet 2707 AF WHITEMARSH ISLAND 121 LIMITED 2 Min Miracle 2709 AF 50 BERWICK BLVD 123 MONEY LIMITED 2009 Family Fitness Spart 2711 FAST FIT BOOTCAMP ED 123HJEMMESIDE APS 2010 Family Fitness Plain 2834 FITNESS PREMIER LOWE 125-Bonner & Partners Fam 2-10 HBW WARRANTY OF CALI 2864 ECLIPSE FITNESS 1288 SlimSpa Diet 2-10 HOLDCO, INC. 2865 Family Fitness Stand 141 The Open Gym 2-10 HOME BUYERS WARRRANT 2CHECKOUT.COM 142B kit merchant 21ST CENTURY INS&FINANCE 300-Oxford Club 147 AF Mendota 2348 AF Alexandria 3012 AF NICHOLASVILLE 1486 Push 2 Crossfit 2369 Olympus 365 3026 Family Fitness Alpin 1496 CKO KICKBOXING 2382 Sequence Fitness PCB 303-Wall Street Daily 1535 KFIT BOOTCAMP 2389730 ONTARIO INC 3045 AF GALLATIN 1539 Family Fitness Norto 2390 Family Fitness Apple 304-Money Map Press 1540 Family Fitness Plain 24 Assistance CAN/US 3171 AF -

Actions of the Board, Its Staff, and the Federal Reserve Banks; Applications and Reports Received

Federal Reserve Release H.2 Actions of the Board, Its Staff, and the Federal Reserve Banks; Applications and Reports Received No. 45 Week Ending November 7, 1998 Board of Governors of the Federal Reserve System, Washington, DC 20551 H.2 Board Actions November 1, 1998 to November 7, 1998 Bank Holding Companies Banc One Corporation, Columbus, Ohio -- requests by certain commenters for reconsideration of the Board's approval of the application to merge with First Chicago NBD Corporation, Chicago, Illinois. - Denied, November 2, 1998 Peoples Heritage Financial Group, Inc., Portland, Maine, and Peoples Heritage Merger Corp. -- to merge with SIS Bancorp, Inc., Springfield, Massachusetts, and acquire Springfield Institution for Savings and Glastonbury Bank & Trust Company, Glastonbury, Connecticut. - Approved, November 4, 1998 Banks, State Member Marine Midland Bank, Buffalo, New York -- request for an exemption from section 23A of the Federal Reserve Act to acquire the commercial loan portfolio of the New York City and Chicago branches and related Cayman Island branch and International Banking facility of Hongkong and Shanghai Banking Corporation, Ltd., Victoria, Hong Kong. - Granted, November 3, 1998 Currency Federal Reserve notes -- 1999 new currency budget. - Approved, November 4, 1998 Regulations And Policies To Their Credit: Women-Owned Businesses -- availability of a videotape designed to heighten awareness among lenders about the business opportunities available in lending to businesses owned by women. - Announced, November 2, 1998 Reserve -

Capital Bank Financial Corp. Announces Pricing of Its Initial Public Offering

September 19, 2012 Capital Bank Financial Corp. Announces Pricing of Its Initial Public Offering CORAL GABLES, FL–(Marketwire – Sep 20, 2012) – Capital Bank Financial Corp. ( NASDAQ : CBF) (“Capital Bank Financial”), before well known as North American Financial Holdings, Inc., a North Carolina-based inhabitant bank land company, currently voiced the pricing of the primary open charity of 10,000,000 shares of Class A usual batch at $18.00 per share. Capital Bank Financial is offered 5,681,818 shares and sure of the stockholders have been offered 4,318,182 shares. The shares of Class A usual batch have been approaching to proceed trade on The NASDAQ Global Select Market on Sep 20, 2012 underneath the pitch “CBF.”The underwriters have a 30-day choice to squeeze from the offered stockholders up to an one more 1,500,000 shares of Class A usual stock, on the same conditions and conditions, to cover over-allotments, if any. The charity is approaching to tighten on Sep 25, 2012. Capital Bank Financial will not embrace any deduction from the sale of shares by the offered stockholders. Capital Bank Financial intends to make use of the net deduction from the charity for ubiquitous corporate purposes. Credit Suisse Securities (USA) LLC, BofA Merrill Lynch, Goldman, Sachs & Co., Barclays and FBR have been behaving as corner book-running managers of the offering. Keefe, Bruyette & Woods and Sandler, O’Neill + Partners, L.P. have been behaving as co-managers of the offering. The charity will be done usually by equates to of a prospectus. When available, copies of the last handbill relating to the charity might be performed by contacting Credit Suisse Securities (USA) LLC, One Madison Avenue, New York, NY 10010, Attention: Prospectus Department, emailing [email protected] or job 1-800-221-1037, or BofA Merrill Lynch, 4 World Financial Center, New York, NY 10080, Attention: Prospectus Department or emailing [email protected].