MIS Case Study Notes

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Marginable OTC Stocks

List of Marginable OTC Stocks @ENTERTAINMENT, INC. ABACAN RESOURCE CORPORATION ACE CASH EXPRESS, INC. $.01 par common No par common $.01 par common 1ST BANCORP (Indiana) ABACUS DIRECT CORPORATION ACE*COMM CORPORATION $1.00 par common $.001 par common $.01 par common 1ST BERGEN BANCORP ABAXIS, INC. ACETO CORPORATION No par common No par common $.01 par common 1ST SOURCE CORPORATION ABC BANCORP (Georgia) ACMAT CORPORATION $1.00 par common $1.00 par common Class A, no par common Fixed rate cumulative trust preferred securities of 1st Source Capital ABC DISPENSING TECHNOLOGIES, INC. ACORN PRODUCTS, INC. Floating rate cumulative trust preferred $.01 par common $.001 par common securities of 1st Source ABC RAIL PRODUCTS CORPORATION ACRES GAMING INCORPORATED 3-D GEOPHYSICAL, INC. $.01 par common $.01 par common $.01 par common ABER RESOURCES LTD. ACRODYNE COMMUNICATIONS, INC. 3-D SYSTEMS CORPORATION No par common $.01 par common $.001 par common ABIGAIL ADAMS NATIONAL BANCORP, INC. †ACSYS, INC. 3COM CORPORATION $.01 par common No par common No par common ABINGTON BANCORP, INC. (Massachusetts) ACT MANUFACTURING, INC. 3D LABS INC. LIMITED $.10 par common $.01 par common $.01 par common ABIOMED, INC. ACT NETWORKS, INC. 3DFX INTERACTIVE, INC. $.01 par common $.01 par common No par common ABLE TELCOM HOLDING CORPORATION ACT TELECONFERENCING, INC. 3DO COMPANY, THE $.001 par common No par common $.01 par common ABR INFORMATION SERVICES INC. ACTEL CORPORATION 3DX TECHNOLOGIES, INC. $.01 par common $.001 par common $.01 par common ABRAMS INDUSTRIES, INC. ACTION PERFORMANCE COMPANIES, INC. 4 KIDS ENTERTAINMENT, INC. $1.00 par common $.01 par common $.01 par common 4FRONT TECHNOLOGIES, INC. -

Issue 23 November 2005 1 Submarine Telecoms Forum Is Published Bi-Monthly by WFN Strategies, L.L.C

DDefenseefense & Non-traditionaNon-traditional CableCable SystemsSystems – 4th4th AnnAnniiversaryversary IssueIssue November 2005 Issue 23 1 Submarine Telecoms Forum is published bi-monthly by WFN Strategies, L.L.C. The publication may not be reproduced or transmitted in any form, in whole or in part, without the Exordium permission of the publishers. NNovember’sovember’s iissuessue mmarksarks ourour ffourthourth aanniversarynniversary inin publishingpublishing SubmarineSubmarine TelecomsTelecoms Forum,Forum, andand thoughthough tthngshngs sstilltill aaren’tren’t aass rrosyosy aass theythey werewere inin thethe “build“build itit andand theythey willwill come”come” era,era, nornor willwill theythey probablyprobably everever Submarine Telecoms Forum is an independent com- bbee – tthingshings aarere stillstill ccertainlyertainly mmuchuch improved.improved. mercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical TThehe ffewew pprinciplesrinciples wwee establishedestablished inin thethe beginning,beginning, wewe continuecontinue toto holdhold dear.dear. WeWe promisedpromised then,then, andand fi bre technologies and techniques. ccontinueontinue ttoo ppromiseromise yyou,ou, oourur rreaders:eaders: Liability: while every care is taken in preparation of this 11.. TThathat wwee wwillill pproviderovide a wwideide rrangeange ooff iideasdeas aandnd iissues;ssues; publication, the publishers cannot be held responsible for the 22.That.That wwee wwillill sseekeek ttoo iincite,ncite, eentertainntertain -

Telecom in the Time of Crash

INCIDENTAL PAPER Telecom in the Time of Crash Kas Kalba November 2002 Program on Information Resources Policy Center for Information Policy Research Harvard University The Program on Information Resources Policy is jointly sponsored by Harvard University and the Center for Information Policy Research. Chairman Managing Director Anthony G. Oettinger John C. B. LeGates Kas Kalba is President of Kalba International, Inc., a management consulting and research firm. He is writing a book on the telecom crash, from which this paper is derived, and has been a longstanding participant in PIRP activities. Copyright © 2002 by Kas Kalba. Not to be reproduced in any form without written consent from Kas Kalba, Kalba International. Inc., 23 Sandy Pond Road, Lincoln, 01773, USA. +1 (781) 259-9589. E-mail: [email protected] URL: http://www.kalbainternational.com ISBN 1-879716-85-2 I-02-2 November 2002 PROGRAM ON INFORMATION RESOURCES POLICY Harvard University Center for Information Policy Research Affiliates AT&T Corp. Nippon Telegraph & Telephone Corp Australian Telecommunications Users (Japan) Group PDS Consulting BellSouth Corp. PetaData Holdings, Inc. The Boeing Company Samara Associates Booz Allen Hamilton Skadden, Arps, Slate, Meagher & Flom Center for Excellence in Education LLP Commission of the European Sonexis Communities Strategy Assistance Services Critical Path TOR LLC CyraCom International United States Government: Ellacoya Networks, Inc. Department of Commerce Hanaro Telecom Corp. (Korea) National Telecommunications and Hearst Newspapers Information Administration Hitachi Research Institute (Japan) Department of Defense IBM Corp. National Defense University Korea Telecom Department of Health and Human Lee Enterprises, Inc. Services Lexis–Nexis National Library of Medicine John and Mary R. -

Download Date 30/09/2021 09:11:11

Index revisions, market quality and the cost of equity capital. Item Type Thesis Authors Aldaya, Wael H. Rights <a rel="license" href="http://creativecommons.org/licenses/ by-nc-nd/3.0/"><img alt="Creative Commons License" style="border-width:0" src="http://i.creativecommons.org/l/by- nc-nd/3.0/88x31.png" /></a><br />The University of Bradford theses are licenced under a <a rel="license" href="http:// creativecommons.org/licenses/by-nc-nd/3.0/">Creative Commons Licence</a>. Download date 30/09/2021 09:11:11 Link to Item http://hdl.handle.net/10454/5687 University of Bradford eThesis This thesis is hosted in Bradford Scholars – The University of Bradford Open Access repository. Visit the repository for full metadata or to contact the repository team © University of Bradford. This work is licenced for reuse under a Creative Commons Licence. Index revisions, market quality and the cost of equity capital Wael Hamdi Aldaya Submitted for the degree of Doctor of Philosophy School of Management University of Bradford 2012 i ABSTRACT Wael Hamdi AlDAYA Index revisions, market quality and the cost of equity capital Keywords: Index revisions, stock liquidity, cost of capital, market quality, price efficiency. This thesis examines the impact of FTSE 100 index revisions on the various aspects of stock market quality and the cost of equity capital. Our study spans over the period 1986–2009. Our analyses indicate that the index membership enhances all aspects of liquidity, including trading continuity, trading cost and price impact. We also show that the liquidity premium and the cost of equity capital decrease significantly after additions, but do not exhibit any significant change following deletions. -

Admission Document Prepared in Accordance with the AIM Rules

233582 Gold Cover Spread 8mm Spine 07/10/2014 14:06 Page 1 Placing and Admission to AIM Gamma Communications plc Nominated AdviserAdviser,, Broker & Sole Bookrunner Perivan Financial Print 233582 233582 Gold pp001-pp004 07/10/2014 14:06 Page 1 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to the contents of this document or as to what action you should take you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser authorised under the Financial Services and Markets Act 2000 (“FSMA”) who specialises in advising on the acquisition of shares and other securities. This document comprises an admission document prepared in accordance with the AIM Rules. Application will be made for the Ordinary Shares to be admitted to trading on AIM. It is expected that Admission will become effective and that trading in the Ordinary Shares on AIM will commence at 8.00 a.m. on 10 October 2014. The Ordinary Shares are not dealt on any other recognised investment exchange and it is emphasised that no application has been, or is being, made for the Ordinary Shares to be admitted to any such exchange. This document is not an approved prospectus for the purposes of section 85 of FSMA, has not been prepared in accordance with the Prospectus Rules published by the Financial Conduct Authority (“FCA”) and a copy of it has not been, and will not be, delivered to the UK Listing Authority in accordance with the Prospectus Rules or delivered to or approved by any other authority which could be a competent authority for the purposes of the Prospectus Directive. -

Access to Infrastructure Nadine I

University of Wisconsin Milwaukee UWM Digital Commons School of Information Studies Faculty Articles Information Studies (School of) 2015 Access to Infrastructure Nadine I. Kozak University of Wisconsin - Milwaukee, [email protected] Follow this and additional works at: https://dc.uwm.edu/sois_facpubs Part of the Library and Information Science Commons Recommended Citation Kozak, Nadine I., "Access to Infrastructure" (2015). School of Information Studies Faculty Articles. 8. https://dc.uwm.edu/sois_facpubs/8 This Article is brought to you for free and open access by UWM Digital Commons. It has been accepted for inclusion in School of Information Studies Faculty Articles by an authorized administrator of UWM Digital Commons. For more information, please contact [email protected]. Pre-publication print, February 2014. Kozak, N. I. (2015). Access to infrastructure. In Ang, P. H. & Mansell, R. (Eds.), International Encyclopedia of Digital Communication & Society. Hoboken, NJ: Wiley-Blackwell. DOI: 10.1002/9781118290743/wbiedcs146 Access to Infrastructure Nadine I. Kozak University of Wisconsin-Milwaukee [email protected] Word count (not including abstract): 5001 Abstract Access to infrastructure is a perennial issue in the field of communication, which started in the era of postal services and continues to the present era of broadband networks. As infrastructures, or large- scale systems, information and communication technologies (ICTs) are central to citizens’ political, economic, and social lives. Historically and today, a variety of factors such as political and regulatory decisions impact access to infrastructure. Current concerns about equitable access include the network neutrality. Keywords: access, communication and public policy, history of media and communications, information and communication technology, media convergence, media law and policy, media regulation. -

The Global Telecommunications Traffic Report- 1991

International Institute of Communications (IIC) THE GLOBAL TELECOMMUNICATIONS TRAFFIC REPORT- 1991 Gregory C. Staple -Editor Principal International Telecom Flows © HC 1991 THE GLOBAL TELECOMMUNICATIONS TRAFFIC REPORT - 1991 Gregory C. Staple - Editor © Copyright 1991 International Institute of Communications T~S ~S co~,¥ .o./~ DO NOT REPRODUCE The IIC is an independent educational and policy research organi- zation with members in more than 70 countries. It focuses on telecommunications and broadcasting issues on a world-wide basis. Institute publications include a bimonthly magazine, Intermedia, and a range of topical brief’rag papers. IIC publications and reports do not necessarily reflect the opinions of the Institute’s officers, trustees or members. Previous IIC reports in this series: 1990 The Global Telecommunications Traffic Boom 1989 Global Telecommunications Traffic Flows and Market Structures For additional copies of this report or other publications, contact: International Institute of Communications Tavistock House South, Tavistock Square, London WCIH 9LF Tel: 071-388-0671/Fax: 071-380-0623/Telex: 24578 IICLDN G Cover Illustration - The cover maps the largest streams of switched international telecommunications traf17c onto a ci~cular projection. Routes shown generally had a two-way flow in 1990 exceeding gO million Minutes of Telecommunication Traf17c (MITT). Some routes have been omitted for presentation purposes. Shaded map areas show major points of origin and destination. Concept: Gregory C. Staple. Illustration: Maryland CartoGraptffcs. ©International Institute of Communications 1991 The Global Telecommunications T:aflqc R#port- 1991 This report could not have been compiled without assistance. Carriers, government departments and regulatory organizations from around the world responded to our informational requests. -

Expmlanatory Memorandum for the Quarterly Report

Irish Communications Market Quarterly Key Data Explanatory Memorandum Document No: 05/92a Date: 20th December 2005 An Coimisiún um Rialáil Cumarsáide Commission for Communications Regulation Abbey Court Irish Life Centre Lower Abbey Street Dublin 1 Ireland Telephone +353 1 804 9600 Fax +353 1 804 9680 Email [email protected] Web www.comreg.ie Contents Contents ..............................................................................................1 1 Executive Summary..........................................................................2 2 Questionnaire Issue ..........................................................................3 3 Primary Data ...................................................................................1 4 Secondary data ................................................................................5 4.1 PRICING DATA..........................................................................................5 4.2 COMPARATIVE DATA ...................................................................................6 5 Glossary..........................................................................................7 6 PPP Conversion Rates data ................................................................0 1 ComReg 05/92a 1 Executive Summary Following the publication of an annual market review in November 1999, ComReg’s predecessor- the ODTR- published its first Quarterly Review on 22nd March 2000. Since that date, ComReg has continued to collect primary statistical data from authorised operators on a quarterly -

Matched Giving Company List

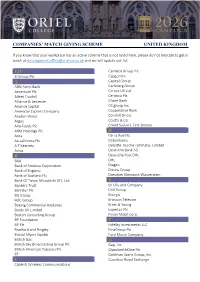

COMPANIES’ MATCH GIVING SCHEME UNITED KINGDOM If you know that your workplace has an active scheme that is not listed here, please do not hesitate to get in touch at [email protected] and we will update our list. 123 Camelot Group Plc 3i Group Plc Capgemini A Capital Group ABN Amro Bank Carlsberg Group Accenture Plc Cemex UK Ltd Alfred Dunhill Centrica Plc Alliance & Leicester Chase Bank Alliance Capital Citigroup Inc. American Express Company Cooperative Bank Anglian Water Cornhill Direct Argos Coutts & Co. Arla Foods Plc Credit Suisse | First Boston ARM Holdings Plc D Asda De La Rue Plc AstraZeneca Plc Debenhams A.T Kearney Deloitte Touche Tohmatsu Limited Aviva Deutsche Bank AG B Deutsche Post DHL BAA DHL Bank of America Corporation Diageo Bank of England Dixons Group Bank of Scotland Plc Dresdner Kleinwort Wasserstein Bank Of Tokyo-Mitsubishi UFJ, Ltd E Bankers Trust Eli Lilly and Company Barclays Plc EMI Group BG Group Energis BOC Group Ericsson Telecom Boeing Commercial Airplanes Ernst & Young Boots UK Limited Experian Plc Boston Consulting Group Exxon Mobil Corp. BP Foundation F BP Plc Fidelity Investments LLC Bradford and Bingley FirstGroup Plc Bristol-Myers Squibb Ford Motor Company British Gas G British Sky Broadcasting Group Plc Gap, Inc. British American Tobacco Plc GlaxoSmithKline Plc BT Goldman Sachs Group, Inc. C Guardian Royal Exchange Cable & Wireless Communications H Philips Halifax Phoenix Group Home Retail Group PPG Industries HSBC Bank Plc PricewaterhouseCoopers HSBC Holdings Plc Proctor & Gamble Co. I R IBM Reuters IDEO Robert Fleming & Co. Industrial Bank of Japan Rolls Royce J Royal Bank of Scotland Group Plc J P Morgan & Co Royal Dutch Shell Plc J Sainsbury Plc Royal London Mutual Insurance Society Limited Johnson & Johnson RSA Insurance Group Plc JPMorgan Chase Bank RWE npower Plc K S Kellogg’s Santander Group Kingfisher Plc Santander UK Plc KPMG LLP Schneider Electric L Schroders Plc Legal & General Group Plc Seaboard Corp. -

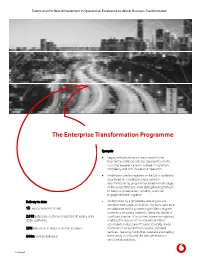

The Enterprise Transformation Programme

Submission for Best Achievement in Operational Excellence to deliver Business Transformation The Enterprise Transformation Programme Synopsis Legacy infrastructure is a major issue for the telecommunications industry. It presents a risk to customer experience and is a driver of significant complexity and cost for network operators. Vodafone is the first operator in the UK to tackle this issue head on; creating a unique network decommissioning programme tasked with all stages of the project lifecycle, from data gathering through to network power-down, including customer engagement and migration. Delivery to date: Underpinned by a proprietary data engine and workflow tool known as Kosmos, the team have built 15 Legacy networks closed an adaptable, evolving operating model to migrate customers off legacy networks. Using this model, a 2,018 Enterprise customers migrated off legacy onto significant number of customers have now migrated, stable platforms. enabling the closure of 15 networks and their associated products and IT stacks. Critically, these 29% Reduction in major customer incidents customers now benefit from reliable, standard services - reducing risk to their business and making £44m Savings delivered them ready to consume the next generation of connectivity solutions. C2 General “If we could walk away from the contract, we would. I don’t think Vodafone truly understands how precarious the relationship is” – Large utility customer, 2015. In 2012 Vodafone, traditionally a leader in mobile telecommunications, acquired Cable & Wireless Worldwide (CWW). The rationale behind the acquisition was to build a global fixed line communications powerhouse to meet the demands of an Enterprise market seeking fixed and mobile services, as well as IT, from a trusted communications partner. -

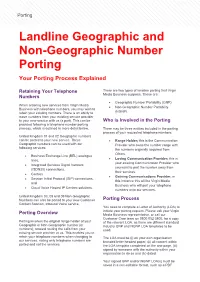

Your Porting Process Explained

Porting Landline Geographic and Non-Geographic Number Porting Your Porting Process Explained Retaining Your Telephone There are two types of landline porting that Virgin Media Business supports. These are: Numbers • Geographic Number Portability (GNP). When ordering new services from Virgin Media • Non-Geographic Number Portability Business with telephone numbers, you may wish to retain your existing numbers. There is an ability to (NGNP). move numbers from your existing service provider to your new service with us (a port). This can be Who is Involved in the Porting provided following a telephone number porting process, which is outlined in more detail below. There may be three entities included in the porting process of your requested telephone numbers: United Kingdom 01 and 02 Geographic numbers can be ported to your new service. These • Range Holder; this is the Communication Geographic numbers can be used with our Provider who owns the number range with following services: the numbers originally acquired from Ofcom. • Business Exchange Line (BEL) analogue • Losing Communication Provider; this is lines, your existing Communication Provider who • Integrated Services Digital Network you want to port the number away from (ISDN30) connections, their services. • Centrex • Gaining Communications Provider; in • Session Initial Protocol (SIP) connections, this instance this will be Virgin Media and Business who will port your telephone • Cloud Voice Hosted IP Centrex solutions. numbers onto our services. United Kingdom 03, 08 and 09 Non-Geographic Numbers can also be ported to your new Customer Porting Process Contact Solution, Inbound Voice service. You need to complete a Letter of Authority (LOA) to initiate your porting request. -

Call to Action on Tough GDPR Laws

Evans opens up on Steve Soper: A man hSo’s big expansion with the courage of plans p26 his convictions p32 VOL 22 ISSUE 1 JUNE 2017 www.comms-dealer.com Call recording for PCI, FCA and MiFID ll compliance. oak.co.uk ADVERTISEMENT ADVERTISEMENT THE HEARTBEAT OF THE UK COMMS INDUSTRY created by Cloud Billing made easy. Multiple online billing 01256 799812 solutions designed for every business requirement. www.quickstart-billing.co.uk 3-24 Industry News Catch up with events in comms 28 Business Profile A model that creates true value CD_commcloud.pdf 1 24/04/2017 12:24 34 Experience the Company Profile Call to action onC Why Liquid Voice M is in full flow Y CM Communications Cloud tough GDPR lawsMY 36 CY We get your Interview WITH less than one year to go until tough new EU data laws come into forceCMY employees, the level of preparedness among those affected appears to be woeful. Intercity Technology K customers and set to go global apps talking SPECIAL REPORT Bruce Potter, Chairman of month had ‘some’ understand- Blake Morgan, commented: ing of GDPR. “We have a long 50 When the European General “We are just a year away from way to go and only a year to do Data Protection Regulation a major shake-up of European it,” stated Dr. Dierk Schindler Market Review (GDPR) comes into effect on information governance laws (pictured above), Head of EMEA Schools: Playground May 25th next year all organisa- and it’s fair to say that many and Global Legal at NetApp.