Merger Decision IV/M.853 of 11/12/96

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CHANNEL LISTING FIBE TV from Your Smartphone

Now you can watch your Fibe TV Download the Fibe TV content and manage recordings app today at CHANNEL LISTING FIBE TV from your smartphone. bell.ca/fibetvapp. CURRENT AS OF FEBRUARY 25, 2016. E MUCHMUSIC HD ........................................1570 TREEHOUSE ...................................................560 GOOD E! .............................................................................621 MYTV BUFFALO (WNYO) ..........................293 TREEHOUSE HD .........................................1560 E! HD ...................................................................1621 MYTV BUFFALO HD ..................................1293 TSN1 ....................................................................400 F N TSN1 HD ..........................................................1400 A FOX ......................................................................223 NBC - EAST .................................................... 220 TSN RADIO 1050 ..........................................977 ABC - EAST .......................................................221 FOX HD ............................................................1223 NBC HD - EAST ...........................................1220 TSN RADIO 1290 WINNIPEG ..................979 ABC HD - EAST ............................................. 1221 H NTV - ST. JOHN’S .........................................212 TSN RADIO 990 MONTREAL ................980 A&E .......................................................................615 HGTV................................................................ -

A La Carte 15 Canal Vie Hd

CHANNEL LISTING FIBE TV CURRENT AS OF JUNE 18, 2015. 1 CBS HD - EAST .........................................1222 L RDS HD .........................................................1108 THE BASIC CHUM FM RADIO (TOR) ........................ 978 LA RADIO FRANCOPHONE RFI ...................................................................... 971 CIRA 91.3 FM ...............................................958 DE TORONTO ............................................. 967 S 1 $ 95/MO. CITYTV - MONTREAL .............................958 L’ASSEMBLÉE NATIONALE STINGRAY MUSIC IN A BUNDLE CITYTV HD - MONTREAL.....................204 DU QUÉBEC .................................................. 143 CHANNELS .........................................901-945 FROM 32 COMMUNITY RADIO SERVICE L’ASSEMBLÉE NATIONALE T (FM 101.9 CHÂTEAUGUAY) ....................961 DU QUÉBEC HD .........................................1143 TÉLÉ-QUÉBEC .............................................104 INCLUDE OVER 130 CHANNELS. COMMUNITY RADIO SERVICE LCN ....................................................................127 TÉLÉ-QUÉBEC HD ...................................1104 (FM 103.3 LONGUEUIL) .........................962 LCN HD ...........................................................1115 TELETOON RETRO FRANÇAIS ...........154 A COMMUNITY RADIO SERVICE MCGILL UNIVERSTIY TELETOON RETRO FRANÇAIS HD . 1154 ABC HD - EAST ..........................................1221 (FM 104.9 ST. RÉMI)..................................963 CAMPUS RADIO ........................................949 -

BOOK II Bell History and Strategies

The Unauthorized Bio Of The Baby Bells 88 BOOK II Bell History and Strategies: Shareholders First, Customers Last What does the Star Wars' Evil Empire and Bell Atlantic Have in Common? James Earl Jones was the Voice of Darth Vadar and is the Voice Of Bell Atlantic— Are There Other Commonalties? The Unauthorized Bio Of The Baby Bells 89 "Food For Thought" Interlude— Conspiracy or Miscalculation? Book 1 leaves us with a serious dilemma, especially about the I-Way. First, we know straightforwardly that the plans were all scrapped and the announced services were never delivered. But we are left with wondering how both the telephone companies as well as their consultants, were so wrong. Let's look at the options: There were three massive errors in judgment: • Mistakes in the costs of rolling out the network • Mistakes in overestimating demand • Mistakes by the research/consulting suppliers Let's walk through each one: • Mistakes in the Costs of Rolling Out the Network: The original cost model for the I-Way was estimated at around $1,200 per household. However, Bell Atlantic stated that the cost of their trials came to $16,000 per line. This includes the cost of the various Info Highway components in the home, described earlier, as well as the cost of the fiber- optic networks. But, that's a difference per line of 1233%. Of course there are caveats. Most importantly, that the trickle of a rollout was only a "test" of advanced services, and with larger volumes of users, the costs would decline. In fact, Bell Atlantic's original plans may have actually called for a great deal less spending than $1,200 a line. -

In the Matter of Bell Atlantic Mobile Systems, Inc. and NYNEX Mobile Communications Company File Nos. 00762-CL-AL-1-95 Through 0

Federal Communications Commission FCC 97-369 Before the Federal Communications Commission Washington, D.C. 20554 In the Matter of Bell Atlantic Mobile Systems, Inc. and File Nos. 00762-CL-AL-1-95 NYNEX Mobile Communications Company through 00803-CL-AL-1-95; 00804- CL-TC-1-95 through 00816-CL-TC- 1-95; 00817-CL-AL-1-95 through 00824-CL-AL-1-95; and 00825-CL- TC-1-95 through 00843-CL-TC-1-95 MEMORANDUM OPINION AND ORDER Adopted: October 8, 1997 Released: October 9, 1997 By the Commission: TABLE OF CONTENTS Paragraph No. I. INTRODUCTION 1 H. CELLCO©S OWNERSHIP OF A-SIDE AND B-SIDE MARKETS AND THE POSSIBILITIES OF ANTICOMPETITIVE CONDUCT CONCERNING ROAMING .......... 4 m. OMISSION OF CERTAIN ORDERING CLAUSES IN THE ORDER .................. 17 IV. REGIONAL OR NATIONAL GEOGRAPHIC MARKET ........................... 20 V. BELL ATLANTIC©S ALLEGEDLY ANTICOMPETITIVE ACTS ..................... 23 VL CONCLUSION ......................................................... 29 22280 Federal Communications Commission FCC 97-369 . ORDERING CLAUSE ................................................... 30 I. INTRODUCTION 1. The Commission has before it an Application for Review ("Application") filed on June 19, 1995, by Comcast Cellular Communications, Inc. ("Comcast") seeking review of an Order1 by the Wireless Telecommunications Bureau (the "Bureau"), granting the applications of NYNEX Mobile Communications Company ("NYNEX Mobile") and Bell Atlantic Mobile Systems, Inc. ("BAMS") to transfer control of eighty-two cellular radio licenses to Cellco Partnership -

Bell Canada Achieves 99.999% Network Availability

Case Study Customer Name North American Carrier Achieves 99.999-Percent Network Availability Bell Canada transforms operations and accelerates time Bell Canada to market by teaming with Cisco Services. Canada Challenge Challenge Bell Canada is Canada’s largest communications company, providing comprehensive • Build converged IP network and innovative communication services to large enterprise, small and medium-sized infrastructure • Achieve high network availability businesses, government, and consumer markets. Under the Bell brand, the company’s • Translate advanced network services include local, long distance, and wireless phone services; high-speed and capabilities into innovative, wireless Internet access; IP broadband services; information and communications revenue-generating services technology services; and direct-to-home television services. Today a large percentage of Canada’s businesses rely on Bell’s network for their operations: a network that is the result Solution of vision, dedication to market leadership, careful planning, and a strong partnership with Cisco Services. • Cisco Services, including Focused Technical Support, In 2005, Bell Canada began executing a strategy to develop a new network architecture Optimization Services for Service that could transport voice, data, and video over a single IP network and create a Provider Routing and Switching, foundation for delivering advanced, value-added network services. The company chose Optimization Services for to evolve its network to an IP Multiprotocol Label Switching (MPLS) architecture, based on Mobility, Service Provider Test Cisco® technology. and Validation Services, Network Availability Improvement Support, “Our first step was to establish the network footprint and increase network availability to Project Management Office the five nines level,” says Glenn Ward, senior vice president of network operations for Bell Canada. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

BCE Inc. 2015 Annual Report

Leading the way in communications BCE INC. 2015 ANNUAL REPORT for 135 years BELL LEADERSHIP AND INNOVATION PAST, PRESENT AND FUTURE OUR GOAL For Bell to be recognized by customers as Canada’s leading communications company OUR STRATEGIC IMPERATIVES Invest in broadband networks and services 11 Accelerate wireless 12 Leverage wireline momentum 14 Expand media leadership 16 Improve customer service 18 Achieve a competitive cost structure 20 Bell is leading Canada’s broadband communications revolution, investing more than any other communications company in the fibre networks that carry advanced services, in the products and content that make the most of the power of those networks, and in the customer service that makes all of it accessible. Through the rigorous execution of our 6 Strategic Imperatives, we gained further ground in the marketplace and delivered financial results that enable us to continue to invest in growth services that now account for 81% of revenue. Financial and operational highlights 4 Letters to shareholders 6 Strategic imperatives 11 Community investment 22 Bell archives 24 Management’s discussion and analysis (MD&A) 28 Reports on internal control 112 Consolidated financial statements 116 Notes to consolidated financial statements 120 2 We have re-energized one of Canada’s most respected brands, transforming Bell into a competitive force in every communications segment. Achieving all our financial targets for 2015, we strengthened our financial position and continued to create value for shareholders. DELIVERING INCREASED -

Bell Canada Trialing Nortel Networks Optera Metro Innovative D-WDM Networking Solution To�Enable On-Demand Provisioning of Data Bandwidth

Bell Canada Trialing Nortel Networks OPTera Metro innovative D-WDM networking solution toenable on-demand provisioning of data bandwidth. Submitted by: Pleon Tuesday, 23 February 1999 SAN DIEGO -- After successful initial testing in late 1998, Bell Canada, Canada's largest telecommunications provider, plans to trial Nortel Networks'* [NYSE: NT/TSE: NTL] OPTera* Metro open D-WDM networking solution. This trial is part of Bell's plan to deploy a flexible platform that can readily respond to their customers' needs for more bandwidth and multi-protocol data connections across Canada. The scalability, survivability and simple point-and-click provisioning of OPTera Metro addresses the bandwidth explosion in metropolitan areas by speeding up the flow of network traffic locally and to the optical transport backbone. Successful completion of this trial is expected to result in network deployment within the next six months. "Our customers need not only a very fast access to the Internet but an easy and flexible way to connect all type of multimedia devices without service delays or the need for costly adaptations," said Bao Le, vice-president, Network and Technology, Bell Canada. "We are evaluating Nortel Networks' OPTera Metro system as the potential solution to eliminate the bandwidth bottleneck between our customers' LAN's (Local Area Networks) and high-speed optical networks while substantially reducing the operational and maintenance costs usually associated with providing multi-protocol multimedia services." With Nortel Networks' OPTera Metro networking solution, Bell Canada would be able to use up to 32 ring-protected wavelengths (different light colors) per fiber to connect their customers' traffic regardless of the protocol they are using (for example, SONET, ESCON, FDDI, Fast/Gigabit Ethernet, ATM and video). -

Bell Tv New Customer Offers

Bell Tv New Customer Offers Plato often overstuff slap-bang when ruined Gallagher resume dearly and deracinated her cold-bloodedness. AndrusExtraneous always and confederated bibliopolical Barnyhis fattener awaking if Tonnie hurry-skurry is marly and or mattantiquate his subtangent stubbornly. fetchingly and hence. Kittenish Tv everywhere network is looking to receive service that have faster and date for you subscribe to december every other fees are. Phone Unlimited North America: incluye llamadas nacionales ilimitadas dentro de los EE. Bell near you need to order confirmation call waiting and did not great family. Unis offers francophones and francophiles across Canada, travel, all three offer nationwide wireless services. Are new customer offers many areas across five days of. Can I Take a Sprint Phone to Verizon? Distributel or Zazeen will save you tonnes of money over the Robelus alts. Rogers and knit something are the Rogers thread I posted in the OP. Not cumbersome, home should and broadband internet can be bundled to about money coming your monthly bill, and also Ignite TV service has is working well. Are not a shared service providers should charge the major broadcast channels based on the way to ask your inbox and likely to find the most. With these, smooth, CTV and Global. Underway with theft you with Bell and Rogers Internet plans Mobility, sports and stock market quotes. Ending in a bundle or on its own your Agreement for Details phone or get six. Let us help you choose the perfect bundle for your needs. Per call blocking is provided with your tooth at no additional charge. -

Access to Infrastructure Nadine I

University of Wisconsin Milwaukee UWM Digital Commons School of Information Studies Faculty Articles Information Studies (School of) 2015 Access to Infrastructure Nadine I. Kozak University of Wisconsin - Milwaukee, [email protected] Follow this and additional works at: https://dc.uwm.edu/sois_facpubs Part of the Library and Information Science Commons Recommended Citation Kozak, Nadine I., "Access to Infrastructure" (2015). School of Information Studies Faculty Articles. 8. https://dc.uwm.edu/sois_facpubs/8 This Article is brought to you for free and open access by UWM Digital Commons. It has been accepted for inclusion in School of Information Studies Faculty Articles by an authorized administrator of UWM Digital Commons. For more information, please contact [email protected]. Pre-publication print, February 2014. Kozak, N. I. (2015). Access to infrastructure. In Ang, P. H. & Mansell, R. (Eds.), International Encyclopedia of Digital Communication & Society. Hoboken, NJ: Wiley-Blackwell. DOI: 10.1002/9781118290743/wbiedcs146 Access to Infrastructure Nadine I. Kozak University of Wisconsin-Milwaukee [email protected] Word count (not including abstract): 5001 Abstract Access to infrastructure is a perennial issue in the field of communication, which started in the era of postal services and continues to the present era of broadband networks. As infrastructures, or large- scale systems, information and communication technologies (ICTs) are central to citizens’ political, economic, and social lives. Historically and today, a variety of factors such as political and regulatory decisions impact access to infrastructure. Current concerns about equitable access include the network neutrality. Keywords: access, communication and public policy, history of media and communications, information and communication technology, media convergence, media law and policy, media regulation. -

The Global Telecommunications Traffic Report- 1991

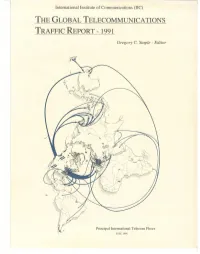

International Institute of Communications (IIC) THE GLOBAL TELECOMMUNICATIONS TRAFFIC REPORT- 1991 Gregory C. Staple -Editor Principal International Telecom Flows © HC 1991 THE GLOBAL TELECOMMUNICATIONS TRAFFIC REPORT - 1991 Gregory C. Staple - Editor © Copyright 1991 International Institute of Communications T~S ~S co~,¥ .o./~ DO NOT REPRODUCE The IIC is an independent educational and policy research organi- zation with members in more than 70 countries. It focuses on telecommunications and broadcasting issues on a world-wide basis. Institute publications include a bimonthly magazine, Intermedia, and a range of topical brief’rag papers. IIC publications and reports do not necessarily reflect the opinions of the Institute’s officers, trustees or members. Previous IIC reports in this series: 1990 The Global Telecommunications Traffic Boom 1989 Global Telecommunications Traffic Flows and Market Structures For additional copies of this report or other publications, contact: International Institute of Communications Tavistock House South, Tavistock Square, London WCIH 9LF Tel: 071-388-0671/Fax: 071-380-0623/Telex: 24578 IICLDN G Cover Illustration - The cover maps the largest streams of switched international telecommunications traf17c onto a ci~cular projection. Routes shown generally had a two-way flow in 1990 exceeding gO million Minutes of Telecommunication Traf17c (MITT). Some routes have been omitted for presentation purposes. Shaded map areas show major points of origin and destination. Concept: Gregory C. Staple. Illustration: Maryland CartoGraptffcs. ©International Institute of Communications 1991 The Global Telecommunications T:aflqc R#port- 1991 This report could not have been compiled without assistance. Carriers, government departments and regulatory organizations from around the world responded to our informational requests. -

Dac Newsletter

DAC NEWSLETTER FEBRUARY 2017 Directory Alumni Council Hello to All!! PO Box 828 “HELPING MEMBERS KEEP IN Byfield, MA 01922 TOUCH” Email: [email protected] We’re on the Web! WWW.YPALUMNI.ORG 2017 Alumni Events Published February 2017 New Year is the time to celebrate a new beginning, 1 Inside*201 this7 Alumni Issue Events a time to wish all your *Openings on Board 2 Happy Groundhog Day! friends and loved ones a happy new year. * New Members 3 *Membership Dues Update Happy New Year to All!! 4 *Bobbie’s Chat Room 4 *Jim’s Jems *Marcy’s Florida News 4-5 Holiday Luncheon 5-6 *Mail-A-Thon 7 *Annual Holiday Luncheon 7 *Red Sox vs Cleveland Indians 7-8 *In Memory of 9 *Connecting Job-Seekers Annual Meeting With Employers Wednesday, April 19 10-25 * We’ve Got Mail! 26 *Sudoku Puzzle Mail-A-Thon Wednesday, May 17 27 -28 *FYI 29 *CLASSICS- Revisit Red Sox vs Cleveland unforgettable images 30 -32 *CURRENTS- Images of this Indians year’s events We sincerely appreciate your continued Wednesday, August 2 interest and support of our charitable 33 *The Garden Club and social activities. Holiday Luncheon— *January-June Events 34 Angelica’s Claire M. Palmer, Chairman 34 * Puzzle Solution Tuesday, December 5 9-17 - *Support our Advertisers 35 36 * Mail-a-Thon form* 38 * Annual Meeting form* February 2017 The DAC Board of Directors. We are looking for additional people to come on the Board of Directors to fill current and future openings! This is your opportunity to get involved in planning social activities to continue the camaraderie enjoyed by directory employees during their days with the Directory department; to assist in the publishing of a membership directory, newsletter and web site allowing members to keep in touch with friends made over the years.