Support at 100 Day SMA; Regulatory Concerns Remained on Other Digital Platform Leaders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Contents the Year 2002 in Review Major Events of Hong Kong

List of Contents The year 2002 in review Major events of Hong Kong securities market 2002 Market highlights Cash market - Main board Cash market - Growth enterprise market (GEM) Derivatives market Clearing statistics Exchange participants The investing community Hong Kong stock market historical events Appendices The Year 2002 in Review The Year The Year 2002 in Review The Hong Kong economy remained weak in 2002 but trade figures began to turn around in the second half of the year. Benefiting from the weakening US dollar and strong demand in the Mainland of China, Hong Kong’s total exports regained double-digit growth over a year earlier in the third quarter of 2002. The seasonally adjusted unemployment rate also fell from its historical peak of 7.8% in July 2002 to 7.2% in December 2002. However, the domestic sector remained sluggish in both investment and consumer spending. The latest economic forecast suggests a 2% growth in real terms of GDP and a 3% decline in the Composite Consumer Price Index for 2002. The trading performance of the Hong Kong securities and futures markets further weakened during the year. Hang Seng Index fell 18.2% from the previous year to end at 9,321.29. The average daily turnover of the Main Board also declined to HK$6,474 million, 19.3% less than that in 2001. The GEM Index ended at 110.4 at end of December 2002, representing a decrease of 44.6% from the previous year. The average daily turnover of the GEM improved slightly to HK$178 million in 2002, an increase of 9.9% from 2001. -

Geely Auto Alert

Deutsche Bank Markets Research Rating Company Date 4 March 2015 Hold Geely Auto Alert Breaking News Asia China Reuters Bloomberg Exchange Ticker Price at 4 Mar 2015 (HKD) 3.31 Automobiles & 0175.HK 175 HK HKG 0175 Price target - 12mth (HKD) 2.95 Components ADR Ticker ISIN 52-week range (HKD) 3.61 - 2.44 GELYY US36847Q1031 HANG SENG INDEX 24,703 Disposal of manual transmission Vincent Ha, CFA Research Analyst business (+852) 2203 6247 To stay focused on core auto manufacturing operation [email protected] Geely announced after today’s market close that the company will sell its manual transmission manufacturing operation to Zhejiang Wanliyang Stock data Transmission (002434.SZ, RMB19.36, Not Rated), an auto part supplier for RMB300m, 1.13x December 2014 NAV. After the completion of the sale, Geely Market cap (HKDm) 29,133 expects to probably realize RMB35m disposal gain, and will procure manual Market cap (USDm) 3,757 transmissions from Wanliyang at least until December 2018. Shares outstanding (m) 8,801.4 Major shareholders Zhejiang Geely According to Geely, the manual transmission business disposal is in line with Hldg (45%) the company’s strategy of streamlining its business to be focused on Free float (%) 57 automobile manufacturing. To recap, Geely also sold its automatic Avg daily value traded 18.8 transmission business back to its parent Zhejiang Geely in FY14 for similar (USDm) reason. Source: Deutsche Bank We do not see a material long-term impact on Geely’s operations or financials Key data from the subject business sale other than for less inter-segmental revenue. -

Hsi Total Return Index Futures Hscei Total Return Index Futures

HSI TOTAL RETURN INDEX FUTURES HSCEI TOTAL RETURN INDEX FUTURES September 2018 INTRODUCTION In stock investing, the return and risk profile for investors has two components: stock price appreciation and dividend. The conventional stock Index futures such as the Hang Seng Index (HSI) futures and Hang Seng China Enterprises Index (HSCEI) futures are risk management tools based on an index calculated from prices of constituent stocks only. The introduction of total return index (TRI) futures by Hong Kong Exchanges and Clearing Limited (HKEX) aims to meet the trading and risk management needs of investors who adopt a total return strategy. TRI futures are based on an index calculated by assuming the cash dividends of constituent stocks are re-invested into the index’s portfolio according to their respective market capitalisation weightings. The Hong Kong Futures Exchange Limited (HKFE) is offering four TRI futures contracts: • Hang Seng Index (Gross Total Return Index) Futures (HSIGTRI Futures) • Hang Seng Index (Net Total Return Index) Futures (HSINTRI Futures) • Hang Seng China Enterprises Index (Gross Total Return Index) Futures (HSCEIGTRI Futures) • Hang Seng China Enterprises Index (Net Total Return Index) Futures (HSCEINTRI Futures) USAGES OF TRIS Due to the unique nature of indexing, TRIs are widely used by fund managers, actuaries and financial advisers to measure their index-based performances in equity funds and pension funds, as price indexes fail to capture the dividend income of the equity funds over time. TRIs are commonly used as the underlying index of equity total return index swaps traded in the over-the-counter (OTC) market among banks, insurance companies and investment funds, which enable users to realise the economic benefits of ownership of shares – price appreciation and dividend return – without the cost of capital outlay and expense of the consequences of ownership, such as custodian arrangements and regular reconciliations. -

Is There a January Effect in the Greater China Area?

Is There a January Effect in the Greater China Area? by Chung-Wen (Sally) Hsu M.Sc., Civil Engineering, National Central University, Taiwan PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration O Chung-Wen (Sally) Hsu 2005 SIMON FRASER UNIVERSITY Spring 2005 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author. APPROVAL Name: Chung-Wen (Sally) Hsu Degree: Master of Business Administration Title of Project: Is There a January Effect in the Greater China Area? Supervisory Committee: Robert Grauer Supervisor Peter Klein Senior Supervisor Date Approved: SIMON FRASER UNIVERSITY PARTIAL COPYRIGHT LICENCE The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection. The author has further agreed that permission for multiple copying of this work for scholarly purposes may be granted by either the author or the Dean of Graduate Studies. It is understood that copying or publication of this work for financial gain shall not be allowed without the author's written permission. -

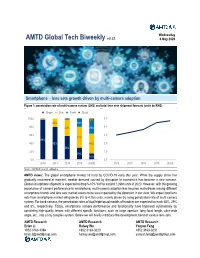

Global Tech Biweekly Vol.22 May 6, 2020 Smartphone – Lens Sets Growth Driven by Multi-Camera

Wednesday AMTD Global Tech Biweekly vol.22 6 May 2020 Smartphone – lens sets growth driven by multi-camera adoption Figure 1: penetration rate of multi-camera system (LHS) and total lens sets shipment forecast (units bn/RHS) - Single - Dual - Triple - Quad 100% 5.0 2% 2% 1% 8% 20% 19% 80% 40% 29% 4.0 60% 3.0 51% 98% 40% 80% 48% 2.0 58% 20% 1.0 29% 16% 0% 0.0 2016 2017 2018 2019 2020E 2016 2017 2018 2019 2020E Source: AMTD Research estimates AMTD views: The global smartphone market hit hard by COVID-19 early this year. While the supply chain has gradually recovered at moment, weaker demand caused by disruption to economics has become a new concern. Global smartphone shipment is expected to drop 5-10% YoY to around 1.26bn units in 2020. However, with the growing importance of camera performance to smartphone, multi-camera adoption has become mainstream among different smartphone brands and lens sets market seems to be less impacted by the downturn in our view. We expect total lens sets from smartphone market will grow by 5% to 4.7bn units, mainly driven by rising penetration rate of multi-camera system. For back camera, the penetration rates of dual/triple/quad models of handset are expected to reach 48%, 29% and 8%, respectively. Today, smartphone camera performance and functionality have improved substantially by combining high-quality lenses with different specific functions, such as large aperture, long focal length, ultra-wide angle, etc., into a tiny complex system. Below we will briefly introduce the development trend of various lens sets. -

Hang Seng Indexes Announces Index Review Results

10 November 2017 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 29 September 2017. All changes will be effective on 4 December 2017 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents is fixed at 50. Inclusion: Code Company 2007 Country Garden Holdings Co. Ltd. 2382 Sunny Optical Technology (Group) Co. Ltd. Removal: Code Company 135 Kunlun Energy Co. Ltd. 293 Cathay Pacific Airways Ltd. The list of constituents is provided in Appendix 1. 2. Hang Seng China Enterprises Index The following constituent changes will be made to the Hang Seng China Enterprises Index. The total number of constituents is fixed at 40. Inclusion: Code Company 2238 Guangzhou Automobile Group Co., Ltd. - H Shares Removal: Code Company 916 China Longyuan Power Group Corporation Ltd. - H Shares The list of constituents is provided in Appendix 2. Changes in constituent companies of the HSCEI will also be applied to the Hang Seng China Enterprises Smart Index. more… Hang Seng Indexes Announces Index Review Results/ 2 3. Hang Seng Composite LargeCap & MidCap Index The following constituent changes will be made to the Hang Seng Composite LargeCap & MidCap Index. The total number of constituents will increase from 289 to 291. Inclusion: Code Company Size Industry ZhongAn Online P & C Insurance 6060 MidCap Financials Co., Ltd. – H Shares 6088 FIT Hong Teng Ltd. MidCap Information Technology Following the constituent changes above, the number of constituents in the Hang Seng Composite Index will increase from 491 to 493. -

CSOP Hang Seng Index Daily (-1X) Inverse Product

Evaluation Only. Created with Aspose.PDF. Copyright 2002-2019 Aspose Pty Ltd. CSOP Hang Seng Index Daily (-1x) Inverse Product Stock Code : 7300 HK All Information as of 30 July 2021 IMPORTANT: Investments involve risks, including the total loss of your investment. Investors are advised to consider their own investment objectives and circumstances in determining the suitability of an investment in the CSOP Hang Seng Index Daily (-1x) Inverse Product (the “Product”). CSOP Hang Seng Index Daily (-1x) Inverse Product is a futures-based product which invests directly in futures contracts on the Hang Seng Index (“HSI Futures”) listed on the HKFE so as to give the Product the inverse (-1x) of the daily performance of the Hang Seng Index ("Index") This is an inverse product and is different from conventional ETF. Should the value of the underlying securities of the Index increase, it could have a negative effect on the performance of the Product. Unitholders could, in certain circumstances including a bull market, face minimal or no returns, or may even suffer a complete loss, on such investments. The Product is designed to be used for short term trading or hedging purposes, and is not intended for long term investment. The Product is not intended for holding longer than one day as the performance of this Product over a longer period may deviate from and be uncorrelated to the inverse performance of the Index over the period. Investment in futures contracts involves specific risks such as high volatility, leverage, rollover and margin risks. A relatively small price movement in HSI Futures may result in a proportionally high impact and substantial losses to the Product, having a material adverse effect on the NAV. -

Hang Seng Indexes Announces Index Review Results

14 August 2020 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 30 June 2020. All changes will take effect on 7 September 2020 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents remains unchanged at 50. Inclusion: Code Company 1810 Xiaomi Corporation - W 2269 WuXi Biologics (Cayman) Inc. 9988 Alibaba Group Holding Ltd. - SW Removal: Code Company 83 Sino Land Co. Ltd. 151 Want Want China Holdings Ltd. 1088 China Shenhua Energy Co. Ltd. - H Shares The list of constituents is provided in Appendix 1. The Hang Seng Index Advisory Committee today reviewed the fast expanding innovation and new economy sectors in the Hong Kong capital market and agreed with the proposal from Hang Seng Indexes to conduct a comprehensive study on the composition of the Hang Seng Index. This holistic review will encompass various aspects including, but not limited to, composition and selection of constituents, number of constituents, weightings, and industry and geographical representation, etc. The underlying aim of the study is to ensure the Hang Seng Index continues to serve as the most representative and important benchmark of the Hong Kong stock market. Hang Seng Indexes will report its findings and propose recommendations to the Advisory Committee within six months. The number of constituents of the Hang Seng Index may increase during this period. Hang Seng Indexes Announces Index Review Results /2 2. -

2016Semi-Annual Report

CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds SEMI-ANNUAL 2016 REPORT For the six months ended 30 June 2016 Value Partners Limited 9th Floor, Nexxus Building 41 Connaught Road Central, Hong Kong Tel: (852) 2880 9263 Fax: (852) 2565 7975 Email: [email protected] Website: www.valuepartners-group.com In the event of inconsistency, the English text of this Semi-Annual Report shall prevail over the Chinese text. This report shall not constitute an offer to sell or a solicitation of an offer to buy shares in any of the funds. Subscriptions are to be made only on the basis of the information contained in the explanatory memorandum, as supplemented by the latest semi-annual and annual reports. CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds (A Cayman Islands unit trust) CONTENTS Pages General information 2-3 Manager’s report 4-9 Statement of financial position (unaudited) 10 Investment portfolio (unaudited) 11-15 Investment portfolio movements (unaudited) 16 SEMI-ANNUAL REPORT 2016 For the six months ended 30 June 2016 1 CHINA CONVERGENCE FUND A Sub-fund of Value Partners Intelligent Funds (A Cayman Islands unit trust) GENERAL INFORMATION Manager Legal Advisors Value Partners Limited With respect to Cayman Islands law 9th Floor, Nexxus Building Maples and Calder 41 Connaught Road Central 53rd Floor, The Center Hong Kong 99 Queen’s Road Central Hong Kong Directors of the Manager Dato’ Seri Cheah Cheng Hye With respect to Hong Kong law Mr. Ho Man Kei, Norman King & Wood Mallesons Mr. So Chun Ki Louis 13th Floor, Gloucester Tower The Landmark Trustee, Registrar, Administrator and 15 Queen’s Road Central Principal Office Hong Kong Bank of Bermuda (Cayman) Limited P.O. -

SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED 舜宇光學科技(集團)有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 2382.HK)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED 舜宇光學科技(集團)有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 2382.HK) INTERIM RESULTS ANNOUNCEMENT FOR THE SIX MONTHS ENDED 30 JUNE 2019 RESULT HIGHLIGHTS The Group’s unaudited consolidated revenue for the six months ended 30 June 2019 was approximately RMB15,574.9 million, representing an increase of approximately 30.0% as compared with the corresponding period of last year. The increase in revenue was mainly benefited from the Group’s further development in smartphone related businesses and rapid growth in the vehicle imaging and sensing fields. The gross profit for the six months ended 30 June 2019 was approximately RMB2,864.0 million, representing an increase of approximately 23.4% as compared with the corresponding period of last year. The gross profit margin was approximately 18.4%. The net profit for the six months ended 30 June 2019 increased by approximately 20.4% to approximately RMB1,432.4 million as compared with the corresponding period of last year. The net profit margin was approximately 9.2%. FINANCIAL RESULTS The board (the “Board”) of directors (the “Directors”, each a “Director”) -

All Web Holdings 092018.Xlsx

Percent of Total Holdings VanEck – Emerging Markets Equity UCITS 30/9/2018 U.S. Dollar Security Name Port. Weight Total 100.00 Alibaba Group Holding Ltd. 6.75 Tencent Holdings Ltd. 6.48 Ping An Insurance (Group) Company of China, Ltd. 5.08 Samsung Electronics Co., Ltd. 4.72 HDFC Bank Limited 4.40 Naspers Limited 3.80 CIE Automotive, S.A. 2.57 Galaxy Entertainment Group Limited 2.04 Kweichow Moutai Co., Ltd. 1.85 Huazhu Group Ltd. 1.68 Malaysia Airports Holdings Bhd. 1.65 CP All Public Co. Ltd. 1.63 Ayala Land Inc. 1.56 Sberbank Russia OJSC 1.51 Focus Media Information Technology Co., Ltd. 1.45 Samsung SDI Co., Ltd 1.44 PT Bank Rakyat Indonesia (Persero) Tbk 1.44 Beijing Enterprises Water Group Limited 1.42 Fleury SA 1.28 Unifin Financiera SAB de CV SOFOM ENR 1.27 Transaction Capital Ltd. 1.27 Srisawad Corporation Public Company Limited 1.25 Baozun, Inc. 1.24 A-Living Services Co., Ltd. 1.24 China Maple Leaf Educational Systems Ltd. 1.22 Chroma Ate Inc. 1.20 Itau Unibanco Holding S.A. 1.19 International Container Terminal Services, Inc. 1.15 Cholamandalam Investment & Finance Co. Ltd. 1.15 Sunny Optical Technology (Group) Co., Ltd. 1.12 Fu Shou Yuan International Group Ltd. 1.11 Regional, S.A.B. de C.V. 1.11 China Zhengtong Auto Services Holdings Limited 1.09 Bloomberry Resorts Corporation 1.06 Beijing Capital International Airport Co., Ltd. 1.04 Yandex NV 1.00 Bank of Georgia Group Plc 0.99 POYA International Co., Ltd. -

Fund Information

Fund Information HANG SENG INDEX FUND CLASS A (HKD) (MIP) (U42281) Fund Price Type of Morningstar Fund Size Risk Level Investment Tenor Divdend Policy Change vs Previous Investment Return Overall Rating NAV Last Update Trading Day (%) HKD28.94000 0.07% 27-09-2021 (PM) HKD 2,501,252,407.00 4 ≥1 Year(s) Inc (Unit) 3 ★★ 0 Month(s) Product Features - Investment Objective and Strategy The investment objective of the Fund is to match as closely as practicable, before fees and expenses, the total return performance (net of withholding tax) of the Hang Seng Index (the “Index”) through investing primarily in the constituent stocks of the Index. The Manager primarily adopts the full replication strategy by which the assets of the Fund comprise the constituent stocks with reference to their respective weightings in the Index or futures contracts on the Index. Exposure to the Index may also be obtained through other index-tracking strategies or financial derivative instruments (such as futures contracts) from which the return to the Fund will substantially reflect the performance of the Index. The Fund's net derivative exposure may be up to 50% of its Net Asset Value. Fund Portfolio as of 30-06-2021 Asset Allocation Equity Holdings Geographical Allocation Equity Holdings Sector Allocation Stock Bond Cash Other 99.07 0.00 0.93 0.00 Total Number of Equity Holdings 58 Total Number of Bond Holdings 0 Fee Information Performance History Subscription Fee 3.00% Switching Handling Fee 1% *Not applicable to Guaranteed Funds* Management Fee 1.000% p.a. Redemption Fee - Performance Fee - Incentive Fee - Other Fund Information Launch Date 13-07-1998 Fund Type Index Fund and Index Leveraged Fund Fund Category Greater China Equity Investment Market Sector Hong Kong Equity Dealing Freqeuncy/ Dealing Cut-off Time Two Dealing Sessions per Dealing Day / Fund indexed performance (initial value =100%).