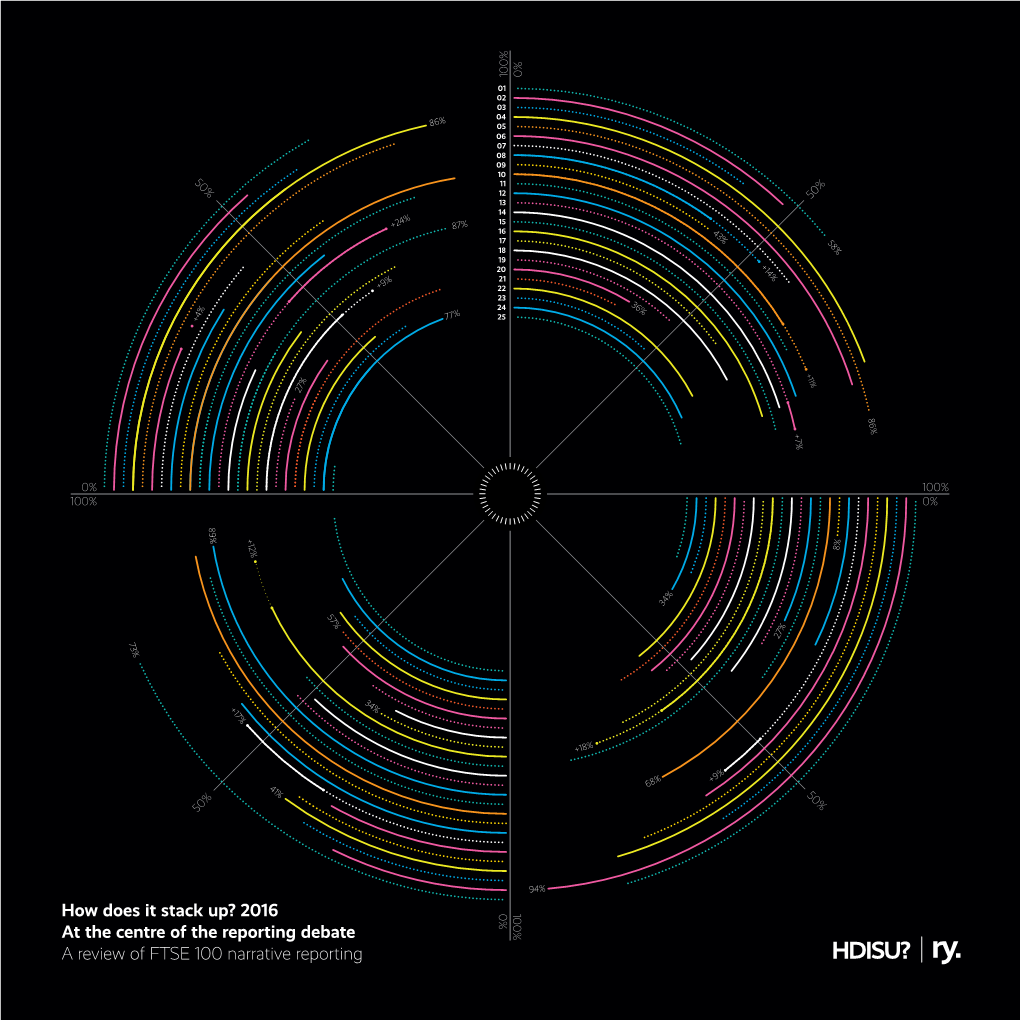

How Does It Stack Up? 2016 at the Centre of the Reporting Debate A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Letter from Dame Melanie Dawes to Rt Hon Damian Green MP on The

Dame Melanie Dawes Chief Executive [email protected] Rt Hon Damian Green MP House of Commons London SW1A OAA 30 July 2021 Dear Damian, Thank you for your email about BBC coverage of the Olympics, the deal with Discovery, and how these arrangements fit with our code on listed events. There has been significant press coverage of the issues, and the BBC have commented on them too, so I thought it would be helpful to outline the current arrangements, how the code applies in this case and some of the implications for the future. As you may know, the broadcasting arrangements applying to the Tokyo Games are the result of deals done some years ago. In 2012 the BBC acquired the exclusive UK broadcast rights for live coverage of both summer and winter Olympics up to and including the current Games. However, in 2015 Discovery reached an agreement with the IOC for a multimedia rights package encompassing fifty countries in Europe. That deal included the UK broadcast and on-demand rights for live coverage of the 2022 and 2024 Games. Subsequently, in 2016, the BBC agreed to sub-licence pay-TV rights to the current Games, in return for free-to-air rights to the 2022 and 2024 Games. As part of this sub-licencing deal, during the current Games the BBC is allowed to show two live streams at any one time from whichever events it chooses. The reason for concentrating on the rights is that they, rather than the actual coverage provided by a broadcaster of a listed event, are the focus of the current legislative regime. -

Scotland's Digital Media Company

Annual Report and Accounts 2010 Annual Report and Accounts Scotland’s digital media company 2010 STV Group plc STV Group plc In producing this report we have chosen production Pacific Quay methods which aim to minimise the impact on our Glasgow G51 1PQ environment. The papers chosen – Revive 50:50 Gloss and Revive 100 Uncoated contain 50% and 100% recycled Tel: 0141 300 3000 fibre respectively and are certified in accordance with the www.stv.tv FSC (Forest stewardship Council). Both the paper mill and printer involved in this production are environmentally Company Registration Number SC203873 accredited with ISO 14001. Directors’ Report Business Review 02 Highlights of 2010 04 Chairman’s Statement 06 A conversation with Rob Woodward by journalist and media commentator Ray Snoddy 09 Chief Executive’s Review – Scotland’s Digital Media Company 10 – Broadcasting 14 – Content 18 – Ventures 22 KPIs 2010-2012 24 Performance Review 27 Principal Risks and Uncertainties 29 Corporate Social Responsibility Corporate Governance 34 Board of Directors 36 Corporate Governance Report 44 Remuneration Committee Report Accounts 56 STV Group plc Consolidated Financial Statements – Independent Auditors’ Report 58 Consolidated Income Statement 58 Consolidated Statement of Comprehensive Income 59 Consolidated Balance Sheet 60 Consolidated Statement of Changes in Equity 61 Consolidated Statement of Cash Flows 62 Notes to the Financial Statements 90 STV Group plc Company Financial Statements – Independent Auditors’ Report 92 Company Balance Sheet 93 Statement -

TV News Channels in Europe: Offer, Establishment and Ownership European Audiovisual Observatory (Council of Europe), Strasbourg, 2018

TV news channels in Europe: Offer, establishment and ownership TV news channels in Europe: Offer, establishment and ownership European Audiovisual Observatory (Council of Europe), Strasbourg, 2018 Director of publication Susanne Nikoltchev, Executive Director Editorial supervision Gilles Fontaine, Head of Department for Market Information Author Laura Ene, Analyst European Television and On-demand Audiovisual Market European Audiovisual Observatory Proofreading Anthony A. Mills Translations Sonja Schmidt, Marco Polo Sarl Press and Public Relations – Alison Hindhaugh, [email protected] European Audiovisual Observatory Publisher European Audiovisual Observatory 76 Allée de la Robertsau, 67000 Strasbourg, France Tel.: +33 (0)3 90 21 60 00 Fax. : +33 (0)3 90 21 60 19 [email protected] http://www.obs.coe.int Cover layout – ALTRAN, Neuilly-sur-Seine, France Please quote this publication as Ene L., TV news channels in Europe: Offer, establishment and ownership, European Audiovisual Observatory, Strasbourg, 2018 © European Audiovisual Observatory (Council of Europe), Strasbourg, July 2018 If you wish to reproduce tables or graphs contained in this publication please contact the European Audiovisual Observatory for prior approval. Opinions expressed in this publication are personal and do not necessarily represent the view of the European Audiovisual Observatory, its members or the Council of Europe. TV news channels in Europe: Offer, establishment and ownership Laura Ene Table of contents 1. Key findings ...................................................................................................................... -

Savour Three Brand New, Lifestyle Channels This Month!

OCTOBER 2018 Your monthly TV guide Giada On The Beach Property Brothers At Home: Drew’s Honeymoon House Luke Nguyen’s Food Trail Savour three brand new, lifestyle channels this month! OCTOBER 2018 Need home renovation and decoration ideas? Perhaps you need an inspiration for a food party? Then you'll definitely not want to miss these 3 brand new channels! From now till 30 November, enjoy free preview of Food Network (CH 252), HGTV (CH 250) and Asian Food Channel (CH 256)! Plus, catch all new season premieres for the biggest TV shows such as The Walking Dead Season 9 and Blindspot Season 4. SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY 1 2 3 4 5 6 BAD PAPA THE PICKERS S13 BECAUSE THIS IS CULINARY OUR FIRST TIME GENIUS USA THE INTERN HISTORY HD tvN CH 518/619 ITV Choice (HD) Oh!K (HD) CH 209 Thursdays & Fridays, FX (HD) CH 310 Warner TV (HD) CH 337 8.35pm CH 525 7.50pm Wednesdays, 9pm 9.45pm Fridays, 10pm CH 306 6pm 7 8 9 10 11 12 13 SUPERGIRL S3 SEXPEDIA Celestial Classic FOX Life (HD) Warner TV (HD) Fox Action Movies cHK (HD) CH 510 FOX Family Movies SCM HD CH 571 Movies CH 580 9pm CH 301 9pm CH 306 9pm (HD) CH 408 10pm Weekdays, 10pm (HD) CH406 8pm 9.30pm 14 15 16 17 18 19 20 MY SO-CALLED INFERNAL SIMPLE LIFE SAY YES TO THE AFFAIRS III VEGAS DRESS FX (HD) CH 310 Fox Action Movies FYI HD CH 260 KIX (HD) CH 309 Celestial Classic cHK (HD) CH 510 10pm (HD) CH 408 8.05pm Tuesdays, 8pm Wednesdays, 9.30pm Movies CH 580 9pm TLC CH 254 9pm 9pm 21 22 23 24 25 26 27 DC LEGENDS OF 1 AM FRANKIE TOMORROW S4 BIG HALLOWEEN Warner TV (HD) ITV Choice (HD) PARTY Nickelodean (HD) FOX Movie (HD) CH 306 FOX Action Movies CH 337 cHK (HD) CH 510 Disney Junior CH 240 11.30am CH 414 9pm Tuesdays, 9pm (HD) CH 408 10pm Thursdays, 9pm 8pm CH 236 12pm © 2018 Sony Pictures Animation Inc. -

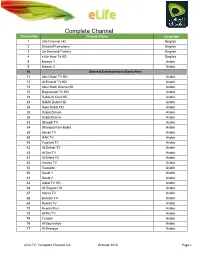

Complete Channel List October 2015 Page 1

Complete Channel Channel No. List Channel Name Language 1 Info Channel HD English 2 Etisalat Promotions English 3 On Demand Trailers English 4 eLife How-To HD English 8 Mosaic 1 Arabic 9 Mosaic 2 Arabic 10 General Entertainment Starts Here 11 Abu Dhabi TV HD Arabic 12 Al Emarat TV HD Arabic 13 Abu Dhabi Drama HD Arabic 15 Baynounah TV HD Arabic 22 Dubai Al Oula HD Arabic 23 SAMA Dubai HD Arabic 24 Noor Dubai HD Arabic 25 Dubai Zaman Arabic 26 Dubai Drama Arabic 33 Sharjah TV Arabic 34 Sharqiya from Kalba Arabic 38 Ajman TV Arabic 39 RAK TV Arabic 40 Fujairah TV Arabic 42 Al Dafrah TV Arabic 43 Al Dar TV Arabic 51 Al Waha TV Arabic 52 Hawas TV Arabic 53 Tawazon Arabic 60 Saudi 1 Arabic 61 Saudi 2 Arabic 63 Qatar TV HD Arabic 64 Al Rayyan HD Arabic 67 Oman TV Arabic 68 Bahrain TV Arabic 69 Kuwait TV Arabic 70 Kuwait Plus Arabic 73 Al Rai TV Arabic 74 Funoon Arabic 76 Al Soumariya Arabic 77 Al Sharqiya Arabic eLife TV : Complete Channel List October 2015 Page 1 Complete Channel 79 LBC Sat List Arabic 80 OTV Arabic 81 LDC Arabic 82 Future TV Arabic 83 Tele Liban Arabic 84 MTV Lebanon Arabic 85 NBN Arabic 86 Al Jadeed Arabic 89 Jordan TV Arabic 91 Palestine Arabic 92 Syria TV Arabic 94 Al Masriya Arabic 95 Al Kahera Wal Nass Arabic 96 Al Kahera Wal Nass +2 Arabic 97 ON TV Arabic 98 ON TV Live Arabic 101 CBC Arabic 102 CBC Extra Arabic 103 CBC Drama Arabic 104 Al Hayat Arabic 105 Al Hayat 2 Arabic 106 Al Hayat Musalsalat Arabic 108 Al Nahar TV Arabic 109 Al Nahar TV +2 Arabic 110 Al Nahar Drama Arabic 112 Sada Al Balad Arabic 113 Sada Al Balad -

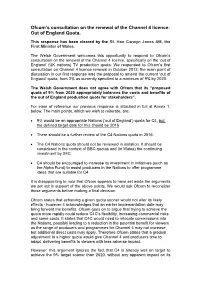

Ofcom's Consultation on the Renewal of the Channel 4 Licence

Ofcom’s consultation on the renewal of the Channel 4 licence: Out of England Quota. This response has been cleared by the Rt. Hon Carwyn Jones AM, the First Minister of Wales. The Welsh Government welcomes this opportunity to respond to Ofcom’s consultation on the renewal of the Channel 4 licence, specifically on the ‘out of England’ (UK nations) TV production quota. We responded to Ofcom’s first consultation on Channel 4 licence renewal in October 2013; the main point of discussion in our first response was the proposal to amend the current ‘out of England’ quota, from 3% as currently specified to a minimum of 9% by 2020. The Welsh Government does not agree with Ofcom that its “proposed quota of 9% from 2020 appropriately balances the costs and benefits of the out of England production quota for stakeholders”. For ease of reference our previous response is attached in full at Annex 1, below. The main points, which we wish to reiterate, are: • 9% would be an appropriate Nations (‘out of England’) quota for C4, but the defined target date for this should be 2016. • There should be a further review of the C4 Nations quota in 2016. • The C4 Nations quota should not be reviewed in isolation. It should be considered in the context of BBC quotas and (in Wales) the continuing investment by S4C. • C4 should be encouraged to increase its investment in initiatives (such as the Alpha Fund) to assist producers in the Nations to offer programme ideas that are suitable for C4. It is disappointing to note that Ofcom appears to have set aside the arguments we set out in support of the above points. -

C Ntent Page 4 L

#GreatJobs C NTENT page 4 www.contentasia.tv l www.contentasiasummit.com Kids Online platforms’ TIFFCOM opens plans in Asia to record highs @TIFFCOM Booth #A1-C8 50 buyers, record 371 TIFFCOM 2017 SPECIAL ISSUE exhibitors in Tokyo, organisers say C NTENT This year’s sixth annual Japan Con- tent Showcase (JCS/TIFFCOM) market バランス オブ パワー フ ォ ー マ ッ ト アジアで 最 も人 気 が 子供 オ ン ラ イ ン プ ラ ッ opened in Tokyo Tuesday morning (24 ハ リ ウ ッ ド 対 ア ジ ア あるフォーマット、ジャンル トフォームのアジア戦略 Oct) with record exhibitors, an uptick in buyers, a focus on the state of Japanese animation and a look at entertainment innovation and marketing. Key animation trends included the rise in short easy-to-produce/broadcast anime and fantasy animation, Hiromichi Masuda, vice chairman of The Associa- tion of Japanese Animations business committee, told delegates at the open- ing seminar on the current state of Japa- nese animation. Anime-based musicals and live con- certs were also on the rise, said Naofumi アカデミー賞受賞者 J・K・シモンズ Ito, Asatsu-DK Inc’s department director, ACADEMY AWARD® WINNER J.K. SIMMONS The rest of the story is on page five Asia outreach A NEW ONE-HOUR DRAMA SERIES peaks at MIPCOM Visit the Sony Pictures Entertainment booth (C12) Local co’s bump up partnership efforts This year’s MIPCOM market closed in Cannes on 19 October with unprece- dented interest from Asian companies in global relationships and outreach. This is not just because Korean compa- nies continue their frantic search to fill the ©2018 MRC II Distribution Company, LP. -

Tailwind® 500/550 with RDU TV Programming for Europe

Tailwind® 500/550 with RDU TV programming for Europe European Programming 23 CNBC Europe E 57 WDR Köln G 91 N24 Austria G 125 EinsPlus G ® for Tailwind 500/550 with RDU 24 Sonlife Broadcasting Network E 58 WDR Bielefeld G 92 rbb Berlin G 126 PHOENIX G A Arabic G German P Portuguese 25 Russia Today E 59 WDR Dortmund G 93 rbb Brandenburg G 127 SIXX G D Deutch K Korean S Spanish 26 GOD Channel E 60 WDR Düsseldorf G 94 NDR FS MV G 128 sixx Austria G E English M Multi T Turkish F French Po Polish 27 BVN TV D 61 WDR Essen G 95 NDR FS HH G 129 TELE 5 G 28 TV Record SD P 62 WDR Münster G 96 NDR FS NDS G 130 DMAX G Standard Definition Free-to-Air channel 29 TELESUR S 63 WDR Siegen G 97 NDR FS SH G 131 DMAX Austria G 30 TVGA S 64 Das Erste G 98 MDR Sachsen G 132 SPORT1 G The following channel list is effective April 21, 2016. Channels listed are subject to change 31 TBN Espana S 65 hr-fernsehen G 99 MDR S-Anhalt G 133 Eurosport 1 Deutschland G without notice. 32 TVE INTERNACIONAL EUROPA S 66 Bayerisches FS Nord G 100 MDR Thüringen G 134 Schau TV G Astra 33 CANAL 24 HORAS S 67 Bayerisches FS Süd G 101 SWR Fernsehen RP G 135 Folx TV G 34 Cubavision Internacional S 68 ARD-alpha G 102 SWR Fernsehen BW G 136 SOPHIA TV G 1 France 24 (in English) E 35 RT Esp S 69 ZDF G 103 DELUXE MUSIC G 137 Die Neue Zeit TV G 2 France 24 (en Français) F 36 Canal Algerie F 70 ZDFinfo G 104 n-tv G 138 K-TV G 3 Al Jazeera English E 37 Algerie 3 A 71 zdf_neo G 105 RTL Television G 139 a.tv G 4 NHK World TV E 38 Al Jazeera Channel A 72 zdf.kultur G 106 RTL FS G 140 TVA-OTV -

DPP Technical Delivery Standards

TECHNICAL STANDARDS FOR DELIVERY OF TELEVISION PROGRAMMES TO This document is a complete guide to the common technical standards agreed by the BBC, BTSport, Channel 4, Channel 5, ITV, Sky, S4C and TG4. The first three pages of this document outline parts of the specification that are unique to TG4. The main body of the document outlines the main DPP specification as adopted by all members. The Standards include: Technical Specifications, i.e. the technical production methods which must be used, and the parameters which all material must meet to be acceptable by the broadcasters. Picture and Sound Quality requirements, which also form a binding obligation on producers of material. Assessment of quality is by nature subjective, and is highly dependent on the nature of the programme. Some of the Quality Requirements are expressed in relative terms (“reasonable”, “not excessive” etc), and it will be necessary to make a judgement as to whether the quality expectations of the intended audience will be fulfilled, and whether the broadcaster will feel that value for money has been achieved. Delivery Requirements, which specify the form and layout of the programme material. Every programme submitted for transmission must satisfy a Quality Control process specified by the Broadcaster. Any programme failing the QC process on tape or file may be rejected and returned to the supplier for repair. Please ensure you are using the current version of this document, available at: http://www.tg4.ie/en/production/guidelines.html Technical Responsibility and Contacts TG4 is required to ensure that for all broadcast programmes technical quality is maintained to a satisfactory standard. -

Dstv Business - Stay Ultra R519 Per TV Point

DStv Business - Stay Ultra R519 Per TV Point General Entertainment Sport Religion 101 - M-Net (HD) 200 - SuperSport Blitz (HD) 331 - One Gospel 103 - 1Magic (HD) 201 - SuperSport 1 (HD) 340 - Dumisa 108 - Sundance TV (HD) 202 - SuperSport 2 (HD) 341 - Faith (prev TBN) 115 - M-Net City (HD) 203 - SuperSport 3 (HD) 342 - DayStar 119 - BBC First (HD) 204 - SuperSport 4 (HD) 343 - TBN Africa (prev Rhema) 120 - BBC Brit (HD) 205 - SuperSport 5 (HD) 347 - iTV 121 - Discovery Channel (HD) 206 - SuperSport 6 (HD) 390 - Emmanuel TV 122 - Comedy Central 207 - SuperSport 7 (HD) 123 - iTV Choice (HD) 208 - SuperSport 8 (HD) News & Commerce 124 - E! Entertainment (HD) 209 - SuperSport 9 (HD) 400 - BBC World News 125 - FOX (HD) 210 - SuperSport 10 (HD) 401 - CNN International (HD) 131 - Lifetime 211 - SuperSport 11 (HD) 402 - Sky News 132 - CBS Reality 212 - SuperSport 12 (HD) 403 - eNews Channel Africa 135 - TLC Entertainment (HD) 235 - SuperSport Maximo (HD) 404 - SABC News 136 - Discovery Family (HD) 240 - Ginx (HD) 406 - Al Jazeera 144 - kykNET (HD) 407 - Russia Today 161 - Mzansi Magic (HD) Free-To-Air Channels 409 - CGTN News 166 - Zee World 191 - SABC 1 (HD) 410 - CNBC Africa 901 - M-Net Plus 1 (HD) 192 - SABC 2 (HD) 411 - Bloomberg 193 - SABC 3 (HD) Movies 194 - eTV (HD) Specialist Channels 104 - M-Net Movies Premiere (HD) 431 - BVN (Dutch) 105 - M-Net Movies Smile (HD) Community Channels 435 - RTPi (Portuguese) 106 - M-Net Movies Action+ (HD) 251 - Soweto TV 437 - TV5 Monde Afrique 109 - M-Net Movies Pop Up (HD) 260 - Bay TV (French) 111 - -

Vietnam to Air Two-Hour Special

#GreatJobs C NTENT page 4 www.contentasia.tv l www.contentasiasummit.com Creevey’s Omni Channels Asia signs Oona/ Telkomsel deal Alliance delivers 30 channels in 2018/9 Gregg Creevey’s new joint venture, Omni Channels Asia (OCA), has partnered with Indonesia’s mobile-centric OTT aggrega- tor Oona to launch up to 30 new genre- focused channels in Indonesia in 2018/9. The Oona deal gives the linear/VOD channels access to Telkomsel’s 135 million mobile customers across the country. The first eight channels went up this month, two months after Multi Channels Asia announced its OCA joint venture with U.S.-based streaming channels provider TV4 Entertainment. The Indonesian channels include Inside- Outside, a global channel rolling out through TV4 Entertainment’s strategic partnership with U.K. indie all3media. Asia’s Got Talent returns to AXN Sony Networks Asia kicks off talent hunt season three Sony Pictures Television Networks Asia kicks off the third edition of big-budget talent search, Asia’s Got Talent, this week. Production is led by Derek Wong, who returned to the Singapore-based regional network earlier this year as vice president of production. Online auditions open on 16 May and run until 9 July on the AXN site. Open auditions will be held from June in major cities around the region. Locations have not yet been announced. Entries are open to performers in 15 countries. 14-27 MAY 2018 page 1. C NTENTASIA 14-27 May 2018 Page 2. Hong Kong’s CA backs Big issues top BCM talking points relaxed media regulations N.Korea, China, IP ownership top Busan agenda Hong Kong’s Communications Author- ity (CA) is backing a relaxation of TV and radio regulations proposed by the territory’s Commerce and Economic Development Bureau. -

Annual Repo Rt 2010

TUARASCÁIL BHLIANTÚIL 2010 TUARASCÁIL BHLIANTÚIL TG4 2010 03/06/2011 11:52 TG4 ANNUAL REPORT 2010 REPORT ANNUAL TG4 2010 ANNUAL REPORT ANNUAL Cludach 2010 FINAL.indd 1 SÚIL EILE ContEntS Mission, Vision & Core Values 3 TG4’s CoMMiTMenTs for 2010 5 Key TG4 PerforManCe HiGHliGHTs of 2010 8 THe Board of Teilifís na GaeilGe and oTHer inforMaTion 15 CHairMan’s rePorT 18 direCTor General’s rePorT 21 CorPoraTe GoVernanCe 26 finanCe reView 2010 28 finanCial sTaTeMenTs 30 TG4 ANNUAL REPORT 2010 1 Tuarascáil Béarla 2010 FINAL Singles.indd 1 03/06/2011 11:41 1916 Seachtar na CásCa 2 TG4 ANNUAL REPORT 2010 Tuarascáil Béarla 2010 FINAL Singles.indd 2 03/06/2011 11:41 SÚIL EILE “I thoroughly enjoyed the documentary series on the 1916 leaders from tG4, the best of the home based channels” Tuam Herald MISSIon, VISIon & CorE VaLuES 1916 SeaCHtar na CÁSCa Winner of 9 awards including: IFta Best Language Celtic Media: Best Documentary Series TG4’s mission is to provide an it works with its key stakeholders and Quality and Value-for-Money: attractive and innovative television overall reflect the principles which are and content service in Irish, that the founding characteristics of the To provide a high quality programme celebrates Irish creativity and identity organisation. The culture of the TG4 schedule. – language, culture, music and sport, organisation is built on these values. packaged and presented to be It is expected that each TG4 employee To operate a cost effective and accessible and appealing in order to lives these values day-to-day and uses efficient structure.