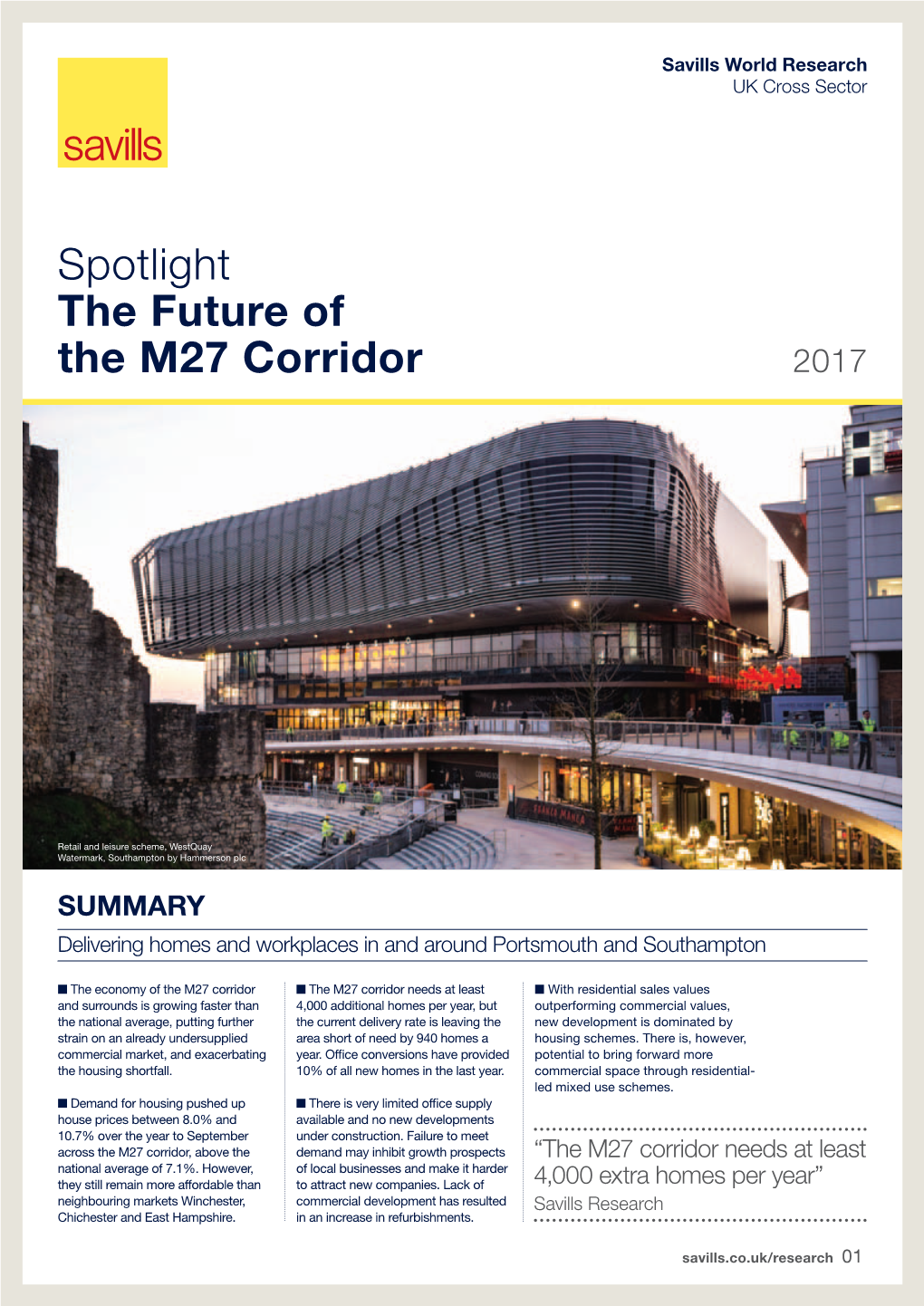

Spotlight the Future of the M27 Corridor 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hampshire Bus, Train and Ferry Guide 2014-2015

I I I I NDEX F LACES ERVED I I O P S To Newbury To Newbury To Tilehurst To Reading To Reading, To Reading To Wokingham I To Windsor I I Oxford and I and Reading I Bracknell 103 I Abbotts Ann. D3 Fyfield . D2 ABC D E F G H JI K Portsmouth & Southsea a . G8 the NorthI Three Mile I X2 I Adanac Park . D6 Wash Comon The Link I 194 Portsmouth Harbour a. G8 I Cross I Alderbury. B4 Glendene Caravan Park, Bashley . C8 104 2A I I Poulner . B7 Burghfield 2 I 72 I Alderholt . .A . A6 Godshill . B6 I I Pound Green . G1 Common I Aldermaston . G1 Godwinscroft . B8 u I 7 BERKSHIRE I 82 I Privett, Gosport . F8 103 Greenham I Aldershot a . K3 Golden Pot Inn . H3 I Inkpen 7 21 22 The Link Brimpton I Purbrook . G7 Ball Hill Aldermaston I I Allbrook . E5 Golf Course, Nr Alton . H3 Common I Beacon Crookham I PUBLIC TRANSPORT MAP OF I I h Allington . C3 Goodworth Clatford . D3 Wash 2 I t I I 194 a Alton a . H4 Gosport . G8 Quarley . D3 104 I 22 I P Water I 103 Spencers Wood I s Queen Alexander Hospital,Cosham. G7 2A I Great Hollands e Alton Hospital and Sports Centre . H4 Grange Park. F6 24 I I tl 21 The Link Bishopswood I a I s Amesbury . B3 Grateley . D3 Quetta Park . J3 7u Bishop’s Green I G X2 I a 21 22A I Broadlaying 23 Road Shops X2 I 194 C Ampfield . -

Shopping and Sightseeing

Itineraries Shopping and Sightseeing Shopaholics will love Hampshire’s retail offerings, which include well known high street brands, designer boutiques and independent outlets. The historic naval city of Portsmouth Spend the afternoon browsing the is home to one of the south coast’s bustling city of Winchester. Famed for Scotland most popular outlet shopping centres, its links with King Alfred the Great, Gunwharf Quays. With top quality the city has a host of boutique shops, brands such as Next, Ralph Lauren and cosy cafés and fine dining restaurants. Gap, spend a morning browsing the Follow its medieval cobbled streets Hall © Great shops which offer heavily discounted and uncover a new surprise around Newcastle prices. There is plenty to do other than every corner. As well as shopping, shopping, as Gunwharf Quays is located the city boasts a stunning Cathedral, in Portsmouth Harbour. Next door sits fascinating Military Museums and it England the famous Historic Dockyard, and is also home to King Arthur’s Round there are harbour tours, restaurants and Table at the Great Hall. cafés available along the waterfront. Manchester Similar attractions nearby: End your stay in Portsmouth with a Visitors may also want to consider Wales Birmingham visit up the 170 metre tall Spinnaker stops at: West Quay Shopping Centre, Tower which sits next to Gunwharf Southampton and Festival Place, Bristol London Quays. Soak up the panoramic views Basingstoke of Portsmouth Harbour and beyond before enjoying a light lunch at the Nearby hotel options: Café in the Clouds. Marriott Hotel Portsmouth, Holiday Inn Hampshire Winchester, Chilworth Best Western. -

Bolshoi Ballet Screenings: 2-For-1 Participating Cinema List

Bolshoi Ballet screenings: 2-for-1 participating cinema list City Cinema Street Zipcode ABERDEEN Cineworld, Aberdeen Union 26, Union Square Shopping Centre, First Level Mall, Union AB11 5RG ALTRINCHAM Vue Altrincham DenmarkSt StreetAltrincham WA14 2WG ASHFORD Cineworld, Ashford Unit 1, Eureka Leisure Pk TN25 4BN ASHFORD Ashford Picturehouse Elwick Rd TN23 1AE BATH Tivoli Bath 6-8 Dorchester St, Southgate Shopping Centre BA1 1SS BATH The Little Theatre Cinema St Michael's Place BA1 1SG BEDFORD Cineworld, Bedford Newnham Ave MK41 9LW BLUEWATER Showcase, Bluewater Showcase Cinema de Lux Bluewater Plaza DA9 9SG BOLTON Cineworld, Bolton The Valley, 15 Eagley Brook Way BL1 8TS BOLTON Vue Bolton Middlebrook Retail & Leisure Park, Level 1 BL6 6HJ BRAINTREE Cineworld, Braintree Freeport Leisure, Charter Way CM77 8YH BRIGHTON Dukes at Komedia 44–47 Gardner Street, Brighton BN1 1UN BRISTOL Showcase, Bristol CDL Glass House, Cabot Circus BS1 3BX BRISTOL Vue Bristol Cribbs Causeway The Venue Cribbs Causeway, Merlin Road BS10 7SR BROMLEY Vue Bromley 6 St Mark's Square BR2 9UY BROUGHTON Cineworld, Broughton Clippers Quay, Salford M50 3XP CAMBERLEY Vue Camberley The Atrium, Park St GU15 3PL CAMBRIDGE Arts Picturehouse 38–39 St Andrew’s Street CB2 3AR CARDIFF Showcase, Cardiff Treforest Ind Estate CF10 1PX CARLISLE Vue Carlisle 50 Botchergate, Carlisle CA1 1QS CHELTENHAM Cineworld, Cheltenham The Brewery, St Margaret's Road GL50 4EF CHELTENHAM Cineworld, Cheltenham Screening Rooms The Brewery, Oxford Passage, St Margaret's Road, GL50 4EF CHESIRE OAKS Vue -

South Coast the Spectacular South Coast

The Spectacular South Coast The Spectacular South Coast The Spectacular South Coast From the Port of Southampton, a whole world of unique and memorable attractions encompassing history and heritage dating back 1000 years awaits. There’s so much for cruise passengers to discover – all within an hour of the Port. This guide will offer great scope for putting together memorable and unique half day, full day excursions and new experiences – in fact, you’re spoilt for choice. The Spectacular South Coast Welcome to Hampshire Southampton is known as the cruise From our research, you have told us that capital of Europe and for good reason, flexibility is the key to making a unique the city welcomes over 2 million cruise excursion, so look out for ( ) on the passengers a year. entries. This indicates the attraction is willing to help you customise your tour Most passengers will arrive at to the needs of your clients and create Southampton unaware of the wealth a tailor-made experience. of fascinating heritage or special experiences that are available to them Please enjoy exploring the many within a relatively small radius. different reasons to visit Hampshire. We have put together a vast array of For further information on the Leisure interesting and memorable experiences Excursions for Cruise & Conference to help you create innovative and unique project please contact Laura Campbell: excursions for the most discerning cruise [email protected] passenger. History and heritage are found within minutes of the port and all destinations in our guide within 40 miles or one hour’s driving distance. -

Press Release Westgate Oxford Alliance Acquires Castle Quarter

Press Release Westgate Oxford Alliance acquires Castle Quarter 02 February 2016 The Westgate Oxford Alliance, a joint venture between Land Securities and The Crown Estate, has acquired the Castle Quarter, Oxford for £47.2m from The Trevor Osborne Property Group. The city centre site is made up of a Malmaison hotel in the former Oxford Prison, an exciting hub of restaurants and bars, and 40 modern apartments. It is in close proximity to the Westgate Oxford development, which is also owned by the Westgate Alliance and currently undergoing a £440m development to become a brand new shopping and leisure destination, due for completion in autumn 2017. Jack Busby, Portfolio Director at Land Securities, said: “We are delighted to have purchased this attractive and historic site so close to our Westgate Oxford development. We believe Oxford is an exciting and unique location and this latest acquisition is testament to our confidence in the city as an international hub for retail and heritage “Westgate Oxford Alliance is investing heavily in Oxford and is working closely with Oxford City Council and Oxfordshire County Council to unlock the regeneration potential of the city centre.” Hannah Milne, Head of Regional Portfolio at The Crown Estate, said: “The acquisition of Castle Quarter is a fantastic opportunity to deepen our strategic partnership with Land Securities and at the same time reaffirm our commitment to ensuring Oxford is established as one of the south-east’s most regionally dominant shopping and leisure destinations.” CBRE, Davis Coffer Lyons and Eversheds advised the Westgate Oxford Alliance. JLL and Charles Russell Speechlys advised The Trevor Osborne Property Group. -

View Annual Report

Land Securities Group PLC 2010 Report Annual 5 Strand, London WC2N 5AF T +44 (0)20 7413 9000 E [email protected] W www.landsecurities.com Creating strong foundations One New Change This world-class development will bring new vitality and variety to a truly remarkable site in the City of London, next to St Paul’s Cathedral. The shops are on schedule to open for Christmas 2010, and the offices will open in June 2011. Annual Report 2010 Forward-looking statements This brochure has been printed on Naturalis Design & illustration by sasdesign.co.uk This Annual Report and the Land Securities’ website may contain certain Absolute White paper. This paper is made up of Words by Tim Rich ‘forward-looking statements’ with respect to Land Securities Group PLC 100% fibre ECF virgin wood fibre, independently Portraits by Philip Gatward and Andy Lane and the Group’s financial condition, results of operations and business, certified in accordance with the FSC (Forest Photography by Lonelyleap, Matt Mawson Annual Report 2010 — Online content and certain of Land Securities Group PLC and the Group’s plans and Stewardship Council). The paper is manufactured and Michael Christopher Brown objectives with respect to these items. at a mill that is certified to ISO14001 environmental Printed at St Ives Westerham Press Ltd, management standards. All of the pulp is bleached ISO14001, FSC certified and CarbonNeutral® Go to our online report for additional features and supporting content: Forward-looking statements are sometimes, but not always, identified using an elemental chlorine free (ECF) process and by their use of a date in the future or such words as ‘anticipates’, ‘aims’, the inks used are all vegetable oil based. -

Download Brochure

EASTLEIGH FAIR OAK TRAVEL TIMES NURSLING 9 5 1 DURLEY SWANMORE FROM OAKELEY VALE HAMBLEDON WEST END BOORLEY GREEN 21 BURSLEDON RAILWAY M271 STATION HEDGE END 0.9 miles / 3 mins WELCOME TO OAKELEY VALE 4 SOUTHAMPTON 17 20 NETLEY RAILWAY M27 CURBRIDGE 19 26 STATION WICKHAM 13 MARCHWOOD 23 3 miles / 9 mins Nestled in a prime, family friendly location just 15 LOCAL ADVENTURES ON YOUR DOORSTEP BURSLEDON minutes from Southampton, Oakeley Vale is perfectly 24 SOUTHAMPTON 10 6 miles / 26 mins positioned to enjoy the spoils of the Hampshire Looking for a day out? Bursledon and the surrounding 22 WHITELEY coastline and countryside whilst offering easy access 14 NETLEY 8 SOUTHWICK local area have all your needs catered for. SOUTHAMPTON AIRPORT to the motorway and local commuter routes. HYTHE 3 11 7 miles / 16 mins Families are spoilt for choice with Manor Farm, part SOUTHAMPTON WATER PARK GATE Thoughtfully arranged around large areas of open ROMSEY of the River Hamble Country Park, just minutes from FAREHAM green space, the homes at Oakeley Vale benefit from a home, or explore the 35 hectares of Holly Hill Woodland 15 miles / 36 mins TITCHFIELD close relationship with nature. A raised boardwalk over Park with shaded winding paths, lakes and sunken a small natural stream provides an enchanting nature COSHAM PORTSMOUTH grottos, perfect for building dens and letting the 7 walk, whilst outdoor fun is close at hand with a specially imagination run wild. The excitement of Marwell Zoo 12 2 15 miles / 25 mins designed play area and play trail. and Paulton’s Park are also a short drive away. -

Portfolio Review

Portfolio Our diverse asset mix Chart 14 11 1 review 1. City of London 11% 10 2. Mid-town 10% 3. West End 24% 9 4. Inner London 3% 2 5. Central London retail 10% 6. London shopping centres 4% 8 7. Regional shopping centres 17% 8. Retail parks 5% 9. Outlets 7% Combined 10. Leisure 6% Portfolio We have a diverse 11. Hotels 3% portfolio of assets 7 located in vibrant 65% 3 locations across of our assets by value are located in London London and the UK. 6 Here’s an update on Our opportunity, approach 5 4 and capital allocation varies how we bought, by sub-sector managed, developed and sold this year. Our top ten assets by value New Street Square, EC4 Cardinal Place, SW1 One New Change, EC4 Bluewater, Kent Gunwharf Quays, Contemporary offices, retail Landmark site, part of our Office and leisure destination The dominant shopping Portsmouth and restaurant campus. Victoria cluster, home to blue- in an iconic building. and leisure destination in Outlet shopping, leisure and Annualised net rent £37.7m chip businesses and retailers. Annualised net rent £29.9m the south east of England. entertainment destination Annualised net rent £29.1m Annualised net rent £28.6m on a waterfront location. (Landsec share) Annualised net rent £29.0m 1&2 New Ludgate, EC4 Queen Anne’s Gate,SW1 Trinity Leeds Nova, SW1 62 Buckingham Gate, SW1 Contemporary office, Landmark office building Retail and leisure destination A stunning new mixed use Office and retail space with restaurant and retail space. comprehensively refurbished forming the heart of Leeds destination within our Victoria a cinema in the basement. -

Outlet Centres in Europe

MARKET SURVEY March 2015 Outlet Centres in Europe Market Survey covering all operating and planned Outlet Centres in the European Countries Study within the Scope of ecostra’s Basic Research understanding markets | evaluating risks | discovering chances Preliminary remarks Beginning in the USA and, over the past 25 years, subsequently spreading in Europe as well, a new retail format has been established: the Factory Outlet Centre (FOC) or Designer Outlet Centre (DOC). In the meantime, such a high density of Outlet Centres already exists in some European countries (e.g. Great Britain), that one can certainly speak of market saturation here. Thus, in Great Britain, as in the USA also, a market shakeout is observable among locations of Outlet Centres, whereby the most professional operators, and accordingly suitable locations, win out over less productive concepts or locations with weaknesses. The situation in continental Europe is somehow different. Due what are, to date, extremely restrictive building permission procedures compared to those in the rest of Europe, Germany has only a very few Outlet Centres in relation to the size of this national market. However, there is little doubt that this will change in the medium-term perspective, at least. The kind of emotional argument that often used to take place until just a few years ago has now given way to a much more factual discussion on the advantages and disadvantages of establishing an Outlet Centre. Whereas Germany still shows a lot of potential for new Outlet Centres, Italy has seen a rapid development in the last years, and it’s difficult to discover any “white spots” on the map there. -

Fit out Guide

Fit Out Guide HCJ/LJ/B100841/JR Issue M November 2017 CONTENTS 1.0 INTRODUCTION / OVERVIEW ........................................................................................ 2 2.0 PROJECT DIRECTORY.................................................................................................... 4 3.0 LANDLORD APRPOVAL PROCESS ............................................................................... 7 STEP 1 RETAILER BRIEFING .......................................................................................... 8 STEP 2(A) CONCEPT DESIGN REVIEW ......................................................................... 9 STEP 2(B) DETAILED DESIGN REVIEW ....................................................................... 10 STEP 3 PRE-START, HANDOVER AND FIT OUT ....................................................... 111 STEP 4 COMPLETION AND CONSENT TO TRADE ................................................... 122 4.0 STORE DESIGN ............................................................................................................ 133 4.1 Introduction .................................................................................................................... 133 4.2 Sustainability .................................................................................................................. 133 5.0 RETAIL SHELL SPECIFICATION ................................................................................ 144 5.1 Drawing Information from Landlord................................................................................. -

Time Will Tell STORES with + BASELWORLD STAR POWER

SUMMER 2019 The Company of Master Jewellers Magazine #55 + Time will tell STORES WITH + BASELWORLD STAR POWER + ELLIOT BROWN THE FUTURE IS AI + WATCHO RESURRECTING + NEW FOR SS19 WINE MAXIMISE YOUR MARKETING Welcome Contents CMJ NEWS 5 Say Hello Introducing new Members and new Approved Suppliers WELCOME 12 Grand Tour Behind the scenes at CMJ Growth & Learning ...to a new issue of Facets magazine, one that I Network events across the UK hope you will find inspiring and informative as we 16 Savvy Style step into summer. We are incredibly proud of the Find out more about the shortlisted retailers in changes that have taken place behind-the-scenes the ‘Store Design of the Year’ category at the at the Company of Master Jewellers in recent UK Jewellery Awards 2019, sponsored by CMJ months, and there is now even more reason to 20 Meet ‘Pete’ A new CMJ tool that allows you to find what spend through the group and benefit from working together as a team. you’re looking for, fast Speaking of team members, on behalf of myself and the entire CMJ Board, BUSINESS & PLANNING I would like to wish Lucy Reece-Raybould our very best as she moves on to a 22 Baselworld Review new role in the footwear sector. We are grateful for all her hard work and The show might be in transition, but what’s commitment over the past nine years. We would also like to say thank you to new and what did CMJ Members and Approved Terry Boot, who leaves us after 20-months to return to a career in financial Suppliers think? Now’s the time to find out operations. -

RETAIL Investor Conference Oxford 2018 RETAIL PORTFOLIO Scott Parsons Managing Director Landsec – Investor Conference 2018 3 Agenda

RETAIL Investor Conference Oxford 2018 RETAIL PORTFOLIO Scott Parsons Managing Director Landsec – Investor Conference 2018 3 Agenda MARKET AND PORTFOLIO UPDATE Scott Parsons Managing Director, Retail Portfolio OUTLETS Ailish Christian-West Head of Property WESTGATE OXFORD Andrew Dudley Head of Development FILM Q&A TOUR OF WESTGATE OXFORD LUNCH Landsec – Investor Conference 2018 4 Repositioned Retail Portfolio Retail Portfolio proportion of capital value – March 2007 vs September 2017 38% 33% 27% 23% 15% 14% 12% 12% 11% 9% 6% 2007 2017 2007 2017 2007 2017 2007 2017 2007 2017 2007 2017 2007 2017 Regional Suburban London Hotels Retail parks Leisure parks Outlets Secondary shopping centres shopping centres centres Landsec – Investor Conference 2018 5 Retail Portfolio strategy Landsec – Investor Conference 2018 6 Retail space UK vs US Shopping centre GLA (sq m) per capita Department store % of total GLA USA 2.19 USA 46% Canada 1.56 UK 27% Australia 1.03 Austria 0.45 Australia 23% UK 0.43 European Union 0.31 Asia 17% China 0.26 Middle East 15% Germany 0.22 Source: ICSC Source: JLL Landsec – Investor Conference 2018 7 Internet penetration Despite fast growth in online retail, physical store is and will continue to be the dominant sales channel. Today, 85.5% of the total £223bn of comparison goods spend in the UK touches a store. Source: CACI Landsec – Investor Conference 2018 8 Department store rents are relatively low Rental comparison between shopping centre “anchors” and other uses Rent / sq ft £5.82 £5.82 £6.75 £22.43 £21.00 £22.10 £21.50