Portfolio Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Greater London Authority

Consumer Expenditure and Comparison Goods Retail Floorspace Need in London March 2009 Consumer Expenditure and Comparison Goods Retail Floorspace Need in London A report by Experian for the Greater London Authority March 2009 copyright Greater London Authority March 2009 Published by Greater London Authority City Hall The Queen’s Walk London SE1 2AA www.london.gov.uk enquiries 020 7983 4100 minicom 020 7983 4458 ISBN 978 1 84781 227 8 This publication is printed on recycled paper Experian - Business Strategies Cardinal Place 6th Floor 80 Victoria Street London SW1E 5JL T: +44 (0) 207 746 8255 F: +44 (0) 207 746 8277 This project was funded by the Greater London Authority and the London Development Agency. The views expressed in this report are those of Experian Business Strategies and do not necessarily represent those of the Greater London Authority or the London Development Agency. 1 EXECUTIVE SUMMARY.................................................................................................... 5 BACKGROUND ........................................................................................................................... 5 CONSUMER EXPENDITURE PROJECTIONS .................................................................................... 6 CURRENT COMPARISON FLOORSPACE PROVISION ....................................................................... 9 RETAIL CENTRE TURNOVER........................................................................................................ 9 COMPARISON GOODS FLOORSPACE REQUIREMENTS -

Download Our Operating and Portfolio Review

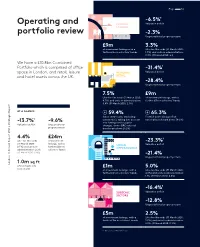

Page 36 -6.5%1 Operating and CENTRAL Valuation deficit LONDON portfolio review -2.3% Ungeared total property return £9m 3.3% of investment lettings with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 1.3%) and units in administration: 0.3% (31 March 2020: nil) We have a £10.8bn Combined Portfolio which is comprised of office -31.4%1 space in London, and retail, leisure REGIONAL Valuation deficit and hotel assets across the UK. RETAIL -28.4% Ungeared total property return 7.5% £9m Like-for-like voids (31 March 2020: of investment lettings, with a 4.7%) and units in administration: further £7m in solicitors’ hands 5.8% (31 March 2020: 2.1%) AT A GLANCE 59.4% 65.3% Same centre sales (excluding Footfall down (ShopperTrak ¹ automotive), taking into account national benchmark down 58.2%) -13.7% -9.6% new lettings and occupier Valuation deficit Ungeared total changes, down (BRC national » Strategic Report property return benchmark down 29.2%) 4.4% £24m Like-for-like voids of investment -23.3%1 (31 March 2020: lettings, with a URBAN Valuation deficit 2.5%) and units in further £12m in OPPORTUNITIES administration: 2.2% solicitors’ hands (31 March 2020: 0.8%) -21.4% Ungeared total property return 1.0m sq ft Landsec // AnnualLandsec Report // 2021 of developments £1m 5.0% now on site of investment lettings, with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 4.8%) and units in administration: 1.1% (31 March 2020: 0.4%) -16.4%1 SUBSCALE Valuation deficit SECTORS -12.8% Ungeared total property return £5m 2.5% of investment lettings, with a Like-for-like voids (31 March 2020: further £3m in solicitors’ hands 2.0%) and units in administration: 2.9% (31 March 2020: 0.9%) 1. -

Half-Yearly Results 2017 Appendices

Appendices Contents Page Page Performance A2 Central London office market A19 Top 10 assets by value A3 London office market – take-up A20 Combined Portfolio valuation movements A4 Landsec’s London developments – construction contracts A21 Like-for-like portfolio valuation analysis A5 Voids and units in administration A22 Yield changes A6 Retail Portfolio vacancy – 30 September 2017 A23 Property – gilt yield spread A7 Reversionary potential A24 Rental value performance – LFL properties vs IPD Quarterly Universe A8 Lease maturities – Combined Portfolio A25 Rental and capital value trends – LFL portfolio A9 Rent reviews, lease expiries and breaks – Retail Portfolio A26 Rental and capital value trends – Retail LFL portfolio A10 Rent reviews, lease expiries and breaks – London Portfolio A27 Rental and capital value trends – London LFL portfolio A11 Reconciliation of cash rents and P&L rents to ERV A28 Portfolio performance relative to IPD Quarterly Universe A12 Net rental income analysis A29 Analysis of performance relative to IPD A13 Cash flow and adjusted net debt A30 Development programme returns A14 Expected debt maturities A31 Development expenditure A15 Financing A32 Future development opportunities A16 Financial history A33 Retailer affordability – shopping centres A17 The Security Group A34 Central London supply – September 2017 A18 The Security Group – Portfolio concentration limits A35 1 Landsec – Appendices Page A 2 Performance Creating shareholder value while strengthening the balance sheet 250 50% 240 230 45% 220 210 200 40% 190 -

Limited and Guild Realisations Limited (Formerly Republic (Retail) Limited) - Both in Administration (Together ‘The Companies’)

Ernst & Young LLP 1 Bridgewater Place, Water Lane Leeds LS11 5QR T el: 0113 298 2200 Fax: 0113 298 2201 www.ey.com/uk TO ALL KNOWN CREDITORS 8 April 2013 Ref: RHK/JPS/TRJ/AE/PCF11.1 Direct line: 0113 298 2496 Direct fax: 0113 298 2206 Email: [email protected] Dear Sirs Republic (UK) Limited and Guild Realisations Limited (formerly Republic (Retail) Limited) - both in Administration (together ‘the Companies’) Further to my appointment as Joint Administrator of the Companies, I attach a copy of my statement of proposals in accordance with paragraph 49 of Schedule B1 to the Insolvency Act 1986. As you will note from the proposals, there is no prospect of any funds becoming available to unsecured creditors of either of the Companies other than by virtue of the prescribed part. As a consequence, I do not propose to summon meetings of creditors. If, however, creditors whose debts amount to at least 10% of total debts of either of the Companies make a request in the prescribed form within 8 business days of these proposals being sent out, a meeting will be held in that company. Copies of the prescribed form (Form 2.21B) are enclosed in case you wish to request a meeting. I would draw your attention to the provisions of Rule 2.37 of the Insolvency Rules 1986 which provide that if a meeting is requested, it will only be held if the expenses of summoning and holding such a meeting are paid by the creditor or creditors making the request and if security is first deposited with me for payment. -

Taylor Wimpey Has a Policy of Continuous Improvement and Reserves the Right to Change Specifications, Designs, Floorplans and Siteplans at Any Time

CITY LIVING AT ITS BEST AT NORWICH RIVERSIDE CONTENTS 04 - City living at its best 06 - Contemporary styling designed to impress 08 - Well-connected 12 - Luxury touches that make a home even more special 13 - Specification 14 - The Sewell – 1 bedroom apartment 16 - The Nelson – 2 bedroom apartment 18 - The Car Club Please note: Information correct at time of going to print, in February 2012. Taylor Wimpey has a policy of continuous improvement and reserves the right to change specifications, designs, floorplans and siteplans at any time. Room dimensions are subject to change and should not be used when ordering floorcoverings or furnishings. Please ask the Sales Executive for up-to-date information when reserving your new home. 03 CITY LIVING AT ITS BEST NR1 is a new collection of stylish one and two bedroom apartments offering a contemporary design complemented by luxury fittings. Located approximately half a mile from Norwich railway station and one mile from the centre of Norwich, the apartments are perfectly situated for modern city living. 05 CONTEMPORARY STYLING DESIGNED TO IMPRESS The ever-growing historic city of Norwich is renowned for being When it comes to sports, health and Norwich is home to the new NR1 diverse and lively, with something country clubs you will be spoilt for development. NR1 is situated in an to suit all tastes. From traditional choice. Whether it is your weekly ideal location close to a wealth of pubs, trendy bars and all night Zumba or aerobics class, you will amenities, including the Riverside clubs, to chic cafés, award-winning not miss out on your exercise fix. -

Sustainability Report 2017

Sustainability Report 2017 Making our experience count Progress Commitments Sustainability Complete Existing commitment (retained) On track Existing commitment (extended) performance Incomplete New commitment at a glance Our commitments and progress to date Creating jobs and opportunities Community employment Fairness Diversity Health, safety and security Commitment Commitment Commitment Commitment Help a total of 1,200 Ensure the working environments Make measurable improvements Maintain an exceptional standard disadvantaged people we control are fair and ensure that to the profile – in terms of gender, of health, safety and security secure jobs by 2020 everyone who is working on our ethnicity and disability – of our in all the working environments behalf – within an environment we employee mix we control Progress control – is paid at least the Living Wage by 2020 Progress Progress Employment secured for 962 people from Progress Participant in the National Chaired the Health in disadvantaged backgrounds Equality Standard assessment Construction Leadership Group Accreditation received from the process. Set specific diversity and launched Mates in Mind Living Wage Foundation metrics to be achieved by 2020 mental health programme Efficient use of natural resources Carbon Renewable energy Energy Waste Commitment Commitment Commitment Commitment Reduce carbon intensity (kgCO2/ Continue to procure 100% Reduce energy intensity (kWh/ Send zero waste to landfill with m2) by 40% by 2030 compared to renewable electricity across m2) by 40% by 2030 -

REGISTER of MEMBERS' FINANCIAL INTERESTS As at 6

REGISTER OF MEMBERS’ FINANCIAL INTERESTS as at 6 June 2016 _________________ Abbott, Ms Diane (Hackney North and Stoke Newington) 1. Employment and earnings Fees received for co-presenting BBC’s ‘This Week’ TV programme. Address: BBC Broadcasting House, Portland Place, London W1A 1AA. (Registered 04 November 2013) 14 May 2015, received £700. Hours: 3 hrs. (Registered 03 June 2015) 4 June 2015, received £700. Hours: 3 hrs. (Registered 01 July 2015) 18 June 2015, received £700. Hours: 3 hrs. (Registered 01 July 2015) 16 July 2015, received £700. Hours: 3 hrs. (Registered 07 August 2015) 8 January 2016, received £700 for an appearance on 17 December 2015. Hours: 3 hrs. (Registered 14 January 2016) 28 July 2015, received £4,000 for taking part in Grant Thornton’s panel at the JLA/FD Intelligence Post-election event. Address: JLA, 14 Berners Street, London W1T 3LJ. Hours: 5 hrs. (Registered 07 August 2015) 23rd October 2015, received £1,500 for co-presenting BBC’s “Have I Got News for You” TV programme. Address: Hat Trick Productions, 33 Oval Road Camden, London NW1 7EA. Hours: 5 hrs. (Registered 26 October 2015) 10 October 2015, received £1,400 for taking part in a talk at the New Wolsey Theatre in Ipswich. Address: Clive Conway Productions, 32 Grove St, Oxford OX2 7JT. Hours: 5 hrs. (Registered 26 October 2015) 21 March 2016, received £4,000 via Speakers Corner (London) Ltd, Unit 31, Highbury Studios, 10 Hornsey Street, London N7 8EL, from Thompson Reuters, Canary Wharf, London E14 5EP, for speaking and consulting on a panel. -

Annual Report 2020 Welcome to Landsec 2020 in Numbers Here Are Some of the Our Portfolio Important Financial and Non-Financial Performance Figures for Our Year

Annual Annual Report 2020 Landsec Annual Report 2020 Welcome to Landsec 2020 in numbers Here are some of the Our portfolio important financial and non-financial performance figures for our year. Some of these measures are impacted by Covid-19. 23.2p Dividend, down 49.1% 55.9p Adjusted diluted earnings per share (2019: 59.7p) Office Retail Specialist Our Office segment consists of Our Retail segment includes outlets, Our Specialist segment comprises high-quality, modern offices in great retail parks, large regionally dominant 17 standalone leisure parks, 23 hotels 1,192p locations in central London. Our offer shopping centres outside London and the iconic Piccadilly Lights in EPRA net tangible assets ranges from traditional long-term and shopping centres within London. central London. per share, down 11.6% leases through to shorter-term, flexible We also have great retail space within Pages 24-29 space. We also have significant our office buildings. development opportunities. Pages 24-29 Pages 24-29 -8.2% Total business return (2019: -1.1%) A £12.8bn portfolio Chart 1 10 1. West End office 26% 9 £11.7bn 2. City office 13% 8 1 Total contribution to 3. Mid-town office 11% the UK economy each 4. Southwark and other office 4% 7 year from people based 5. London retail 11% Combined at our assets 6. Regional retail 13% 7. Outlets 7% Portfolio 6 8. Retail parks 3% 2 9. Leisure and hotels 9% £(837)m 10. Other 3% 5 Loss before tax 3 4 (2019: £(123)m) Read more on pages 174-177 Comprising 24 million sq ft Chart 2 -4.5% Ungeared total property of space return (2019: 0.4%) 1 1. -

Hampshire Bus, Train and Ferry Guide 2014-2015

I I I I NDEX F LACES ERVED I I O P S To Newbury To Newbury To Tilehurst To Reading To Reading, To Reading To Wokingham I To Windsor I I Oxford and I and Reading I Bracknell 103 I Abbotts Ann. D3 Fyfield . D2 ABC D E F G H JI K Portsmouth & Southsea a . G8 the NorthI Three Mile I X2 I Adanac Park . D6 Wash Comon The Link I 194 Portsmouth Harbour a. G8 I Cross I Alderbury. B4 Glendene Caravan Park, Bashley . C8 104 2A I I Poulner . B7 Burghfield 2 I 72 I Alderholt . .A . A6 Godshill . B6 I I Pound Green . G1 Common I Aldermaston . G1 Godwinscroft . B8 u I 7 BERKSHIRE I 82 I Privett, Gosport . F8 103 Greenham I Aldershot a . K3 Golden Pot Inn . H3 I Inkpen 7 21 22 The Link Brimpton I Purbrook . G7 Ball Hill Aldermaston I I Allbrook . E5 Golf Course, Nr Alton . H3 Common I Beacon Crookham I PUBLIC TRANSPORT MAP OF I I h Allington . C3 Goodworth Clatford . D3 Wash 2 I t I I 194 a Alton a . H4 Gosport . G8 Quarley . D3 104 I 22 I P Water I 103 Spencers Wood I s Queen Alexander Hospital,Cosham. G7 2A I Great Hollands e Alton Hospital and Sports Centre . H4 Grange Park. F6 24 I I tl 21 The Link Bishopswood I a I s Amesbury . B3 Grateley . D3 Quetta Park . J3 7u Bishop’s Green I G X2 I a 21 22A I Broadlaying 23 Road Shops X2 I 194 C Ampfield . -

Shopping and Sightseeing

Itineraries Shopping and Sightseeing Shopaholics will love Hampshire’s retail offerings, which include well known high street brands, designer boutiques and independent outlets. The historic naval city of Portsmouth Spend the afternoon browsing the is home to one of the south coast’s bustling city of Winchester. Famed for Scotland most popular outlet shopping centres, its links with King Alfred the Great, Gunwharf Quays. With top quality the city has a host of boutique shops, brands such as Next, Ralph Lauren and cosy cafés and fine dining restaurants. Gap, spend a morning browsing the Follow its medieval cobbled streets Hall © Great shops which offer heavily discounted and uncover a new surprise around Newcastle prices. There is plenty to do other than every corner. As well as shopping, shopping, as Gunwharf Quays is located the city boasts a stunning Cathedral, in Portsmouth Harbour. Next door sits fascinating Military Museums and it England the famous Historic Dockyard, and is also home to King Arthur’s Round there are harbour tours, restaurants and Table at the Great Hall. cafés available along the waterfront. Manchester Similar attractions nearby: End your stay in Portsmouth with a Visitors may also want to consider Wales Birmingham visit up the 170 metre tall Spinnaker stops at: West Quay Shopping Centre, Tower which sits next to Gunwharf Southampton and Festival Place, Bristol London Quays. Soak up the panoramic views Basingstoke of Portsmouth Harbour and beyond before enjoying a light lunch at the Nearby hotel options: Café in the Clouds. Marriott Hotel Portsmouth, Holiday Inn Hampshire Winchester, Chilworth Best Western. -

Bolshoi Ballet Screenings: 2-For-1 Participating Cinema List

Bolshoi Ballet screenings: 2-for-1 participating cinema list City Cinema Street Zipcode ABERDEEN Cineworld, Aberdeen Union 26, Union Square Shopping Centre, First Level Mall, Union AB11 5RG ALTRINCHAM Vue Altrincham DenmarkSt StreetAltrincham WA14 2WG ASHFORD Cineworld, Ashford Unit 1, Eureka Leisure Pk TN25 4BN ASHFORD Ashford Picturehouse Elwick Rd TN23 1AE BATH Tivoli Bath 6-8 Dorchester St, Southgate Shopping Centre BA1 1SS BATH The Little Theatre Cinema St Michael's Place BA1 1SG BEDFORD Cineworld, Bedford Newnham Ave MK41 9LW BLUEWATER Showcase, Bluewater Showcase Cinema de Lux Bluewater Plaza DA9 9SG BOLTON Cineworld, Bolton The Valley, 15 Eagley Brook Way BL1 8TS BOLTON Vue Bolton Middlebrook Retail & Leisure Park, Level 1 BL6 6HJ BRAINTREE Cineworld, Braintree Freeport Leisure, Charter Way CM77 8YH BRIGHTON Dukes at Komedia 44–47 Gardner Street, Brighton BN1 1UN BRISTOL Showcase, Bristol CDL Glass House, Cabot Circus BS1 3BX BRISTOL Vue Bristol Cribbs Causeway The Venue Cribbs Causeway, Merlin Road BS10 7SR BROMLEY Vue Bromley 6 St Mark's Square BR2 9UY BROUGHTON Cineworld, Broughton Clippers Quay, Salford M50 3XP CAMBERLEY Vue Camberley The Atrium, Park St GU15 3PL CAMBRIDGE Arts Picturehouse 38–39 St Andrew’s Street CB2 3AR CARDIFF Showcase, Cardiff Treforest Ind Estate CF10 1PX CARLISLE Vue Carlisle 50 Botchergate, Carlisle CA1 1QS CHELTENHAM Cineworld, Cheltenham The Brewery, St Margaret's Road GL50 4EF CHELTENHAM Cineworld, Cheltenham Screening Rooms The Brewery, Oxford Passage, St Margaret's Road, GL50 4EF CHESIRE OAKS Vue -

Liberty International PLC Annual Report 2006

Liberty International 2006 PLC Annual report The company’s website, which contains further information, is available at www.liberty-international.co.uk Liberty International PLC Annual report 2006 Front cover Covent Garden Estate, Central London Management structure and advisers Back cover Chapelfield, Norwich Liberty International PLC Property Companies Capital & Counties Sir Donald Gordon, President for Life Capital Shopping Centres Ian Hawksworth, Managing Director Chairman and Executive Directors Kay Chaldecott, Managing Director Bill Black, Executive Director Sir Robert Finch, Chairman Peter Badcock, Director Gary Marcuccilli, Executive Director David Fischel, Chief Executive Richard Cable, Development Director 40 Broadway, London SW1H 0BU Aidan Smith, Finance Director Martin Ellis, Executive Director Telephone 020 7887 7000 01 Introduction* Richard Cable Caroline Kirby, Executive Director Facsimile 020 7887 0000 02 Performance* Kay Chaldecott 40 Broadway, London SW1H 0BU www.capitalandcounties.com 04 Summary of investment and Ian Hawksworth Telephone 020 7887 4220 Business Units development properties* Non-executive Directors Facsimile 020 7887 4225 Andrew Hicks, Capco Covent Garden 07 Chairman’s statement John Abel www.capital-shopping-centres.co.uk Mark Imms, Capco Urban * Robin Buchanan Group Managers Gary Marcuccilli, Capco Central London 12 Operational review Patrick Burgess * Property Management Bill Black, Capco Opportunities 13 Long-term financial record Graeme Gordon (Alternate - Richard Gordon) Jonathan Ainsley, Martin