Report of the Results of the 2014 Survey of Office Needs in Tokyo's

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outdoor Club Japan (OCJ) 国際 アウトドア・クラブ・ジャパン Events

Outdoor Club Japan (OCJ) 国際 アウトドア・クラブ・ジャパン Events Norikuradake Super Downhill 10 March Friday to 12 March Monday If you are not satisfied ski & snowboard in ski area. You can skiing from summit. Norikuradake(3026m)is one of hundred best mountain in Japan. This time is good condition of backcountry ski season. Go up to the summit of Norikuradake by walk from the top of last lift(2000m). Climb about 5 hours and down to bottom lift(1500m) about 50 min. (Deta of last time) Transport: Train from Shinjuku to Matsumoto and Taxi from Matsumoto to Norikura-kogen. Return : Bus from Norikura-kogen to Sinshimashima and train to Shinjuku. Meeting Time & Place : 19:30 Shijuku st. platform 5 car no.1 for super Azusa15 Cost : About Yen30000 Train Shinjuku to matsumoto Yen6200(ow) but should buy 4coupon ticket each coupon Yen4190 or You can buy discount ticket shop in town price is similar. (price is non-reserve seat) Taxi about Yen13000 we will share. Return bus Yen1300 and local train Yen680. Inn Yen14000+tax 2 overnight 2 breakfast 1 dinner (no dinner Friday) Japanese room and hot spring! Necessary equipment : Skiers & Telemarkers need a nylon mohair skin. Snowboarders need snowshoes. Crampons(over 8point!) Clothes: Gore-tex jacket and pants, fleece, hut, musk, gloves, sunglasses, headlamp, thermos, lunch, sunscreen If you do not go up to the summit, you can enjoy the ski area and hot springs. 1 day lift pass Yen4000 Limit : 12persons (priority is downhill from summit) In Japanese : 026m)の頂上からの滑降です。 ゲレンデスキーに物足りないスキーヤー、スノーボーダー向き。 山スキーにいいシーズンですが、天気次第なので一応土、日と2日間の時間をとりました。 -

Symbol of Peace and Restoration Statue of “Kanaderu Otome” (A Girl Playing Guitar)

Community Information Paper Vol.33 December 2015 Issued by Azabu Regional City Office Edited by The Azabu Editing Office 5-16-45 Roppongi, Minato City, Tokyo 106-8515 Tel: 03-5114-8812 Fax: 03-3583-3782 Please contact Minato Call (City Information Service) for inquiries regarding Residents’ Life Support. Tel: 03-5472-3710 A community information paper created and edited by Azabu residents Fascinated by Artistic Azabu ⑦ Symbol of Peace and Restoration Statue of “Kanaderu Otome” (A Girl Playing Guitar) Shin Hongo (1905 – 1980) He was a leading sculptor of representational sculptures in Japan after the war, and a pio- neer of monumental statues and field sculp- tures. He was born and grew up in Sapporo. After graduating from the Craftworks and Sculpture Division, the Craft and Design De- partment of Koto Kogei Gakkou (tertiary insti- tution for crafts, presently the Department of Technology in Chiba University) in 1928, he studied under the great sculptor Kotaro Taka- mura. His representative works include a sculpture of a group of students who died in the war called “Kike Wadatsumi no Koe” (1950), the sculpture “Arashi no naka no Boshizo” (Mother and Child in a Storm) (1953), and more. (Pictures provided by Hongo Shin Memorial Museum of Sculpture, Sapporo) The coffee shop “Almond”, a famous都営地下鉄大江戸線 meeting 麻布十番駅 spot on a corner of the Roppongi Cross- ing, opened in 1964. Since 1954, 10 years before Almond was established, a statue of a 麻布十番大通り girl playing guitar has stood at the side of the crossing.東 京 メ トImmediately ロ 南 北 線 after the war, this Bronze Statue “Kanaderu Otome” by Shin Hongo statue, called “Kanaderu Otome,”きみちゃん像 was sculpted by Shin Hongo as a symbol of peace パ テ ィ オ 通 り パティオ and restoration. -

Meguro Walking Map

Meguro Walking Map Meguro Walking Map Primary print number No. 31-30 Published February 2, 2020 December 6, 2019 Published by Meguro City Edited by Health Promotion Section, Health Promotion Department; Sports Promotion Section, Culture and Sports Department, Meguro City 2-19-15 Kamimeguro, Meguro City, Tokyo Phone 03-3715-1111 Cooperation provided by Meguro Walking Association Produced by Chuo Geomatics Co., Ltd. Meguro City Total Area Course Map Contents Walking Course 7 Meguro Walking Courses Meguro Walking Course Higashi-Kitazawa Sta. Total Area Course Map C2 Walking 7 Meguro Walking Courses P2 Course 1: Meguro-dori Ave. Ikenoue Sta. Ke Walk dazzling Meguro-dori Ave. P3 io Inok Map ashira Line Komaba-todaimae Sta. Course 2: Komaba/Aobadai area Shinsen Sta. Walk the ties between Meguro and Fuji P7 0 100 500 1,000m Awas hima-dori St. 3 Course 3: Kakinokizaka/Higashigaoka area Kyuyamate-dori Ave. Walk the 1964 Tokyo Olympics P11 2 Komaba/Aobadai area Walk the ties between Meguro and Fuji Shibuya City Tamagawa-dori Ave. Course 4: Himon-ya/Meguro-honcho area Ikejiri-ohashi Sta. Meguro/Shimomeguro area Walk among the history and greenery of Himon-ya P15 5 Walk among Edo period townscape Daikan-yama Sta. Course 5: Meguro/Shimomeguro area Tokyu Den-en-toshi Line Walk among Edo period townscape P19 Ebisu Sta. kyo Me e To tro Hibiya Lin Course 6: Yakumo/Midorigaoka area Naka-meguro Sta. J R Walk a green road born from a culvert P23 Y Yutenji/Chuo-cho area a m 7 Yamate-dori Ave. a Walk Yutenji and the vestiges of the old horse track n o Course 7: Yutenji/Chuo-cho area t e L Meguro City Office i Walk Yutenji and the vestiges of the old horse track n P27 e / S 2 a i k Minato e y Kakinokizaka/Higashigaoka area o in City Small efforts, L Yutenji Sta. -

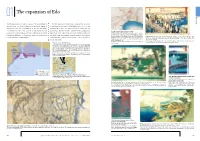

01 the Expansion Of

The expansion of Edo I ntroduction With Tokugawa Ieyasu’s entry to Edo in 1590, development of In 1601, construction of the roads connecting Edo to regions the castle town was advanced. Among city construction projects around Japan began, and in 1604, Nihombashi was set as the undertaken since the establishment of the Edo Shogunate starting point of the roads. This was how the traffic network government in 1603 is the creation of urban land through between Edo and other regions, centering on the Gokaido (five The five major roads and post towns reclamation of the Toshimasusaki swale (currently the area from major roads of the Edo period), were built. Daimyo feudal lords Post towns were born along the five major roads of the Edo period, with post stations which provided lodgings and ex- Nihombashi Hamacho to Shimbashi) using soil generated by and middle- and lower-ranking samurai, hatamoto and gokenin, press messengers who transported goods. Naito-Shinjuku, Nihombashi Shinsen Edo meisho Nihon-bashi yukibare no zu (Famous Places in Edo, leveling the hillside of Kandayama. gathered in Edo, which grew as Japan’s center of politics, Shinagawa-shuku, Senju-shuku, and Itabashi-shuku were Newly Selected: Clear Weather after Snow at Nihombashi Bridge) From the collection of the the closest post towns to Edo, forming the general periphery National Diet Library. society, and culture. of Edo’s built-up area. Nihombashi, which was set as the origin of the five major roads (Tokaido, Koshu-kaido, Os- Prepared from Ino daizu saishikizu (Large Colored Map by hu-kaido, Nikko-kaido, Nakasendo), was bustling with people. -

The 1960 US-Japan Security Treaty Uprising and the Origins of Contemporary Japan

Volume 18 | Issue 11 | Number 3 | Article ID 5403 | May 25, 2020 The Asia-Pacific Journal | Japan Focus Japan’s Streets of Rage: The 1960 US-Japan Security Treaty Uprising and the Origins of Contemporary Japan 現代日本の原点:60年安保闘争の街頭の怒り Nick Kapur Keywords: Anpo, US-Japan Security Treaty, Kishi Nobusuke, Hagerty Incident, Kanba Abstract Michiko This excerpt from the author’s recent book Japan at the Crossroads: Conflict and Compromise after Anpo (Harvard University Press, 2018) describes the dramatic climax of Sixty years ago this month, in June 1960, the the massive 1960 protests in Japan against the largest and longest popular protests in Japan’s US-Japan Security Treaty (abbreviated Anpo in modern history reached a stunning climax. At Japanese), which is the treaty that continues to issue was an attempt by Japan’s US-backed allow the United States to station troops on conservative government to pass a revised Japanese soil to this day. Events described version of the US-Japan Security Treaty – the include the May 19th incident, in which pact, abbreviated as Anpo in Japanese, which Japanese prime minister Kishi Nobusuke continues to allow the United States to shocked the nation by ramming the treaty maintain military bases and troops on Japanese through the National Diet after havingsoil to this day. The 1960 treaty was a opposition lawmakers physically removed by significant improvement over the original police; the Hagerty Incident of June 10, in treaty, which had been imposed on Japan by which a car carrying US envoys was mobbed by the United States as a condition for ending the protesters, necessitating a dramatic rescue by US military occupation of Japan in 1952. -

Ginza Opens As Building, a Trend-Setting Retail Harvest Club

CONTENTS MESSAGE FROM THE PRESIDENT 02 MESSAGE FROM THE PRESIDENT As a core company of the Tokyu Fudosan Holdings Group, 03 HISTORY OF TOKYU LAND CORPORATION We are creating a town to solve social issues through 05 ABOUT TOKYU FUDOSAN HOLDINGS GROUP value creation by cooperation. 06 GROUP’S MEDIUM- AND LONG-TERM MANAGEMENT PLAN 07 URBAN DEVELOPMENT THAT PROPOSES NEW LIFESTYLES 07 THE GREATER SHIBUYA AREA CONCEPT 09 LIFE STORY TOWN 11 URBAN DEVELOPMENT 25 RESIDENTIAL 33 WELLNESS 43 OVERSEAS BUSINESSES 47 REAL ESTATE SOLUTIONS Tokyu Land Corporation is a comprehensive real estate company the aging population and childcare through the joint development of with operations in urban development, residential property, wellness, condominiums and senior housing. In September 2017, we celebrated overseas businesses and more. We are a core company of Tokyu the opening of the town developed in the Setagaya Nakamachi Fudosan Holdings Group. Since our founding in 1953, we have Project, our first project for creating a town which fosters interactions 48 MAJOR AFFILIATES consistently worked to create value by launching new real estate between generations. 49 HOLDINGS STRUCTURE businesses. We have expanded our business domains in response to For the expansion of the scope of cyclical reinvestment business, changing times and societal changes, growing from development to we are expanding the applicable areas of the cyclical reinvestment 50 TOKYU GROUP PHILOSOPHY property management, real estate agency and, in particular, a retail business to infrastructure, hotels, resorts and residences for business encouraging work done by hand. These operations now run students, in our efforts to ensure the expansion of associated assets independently as Tokyu Community Corporation, Tokyu Livable, Inc. -

SMOKING AREA MAP Akihabara

Ginza Line Iidabashi Station Area Akihabara Station Area Suehirocho Sta. Ueno Public Smoking Area Private Smoking Area Iidabashi Oedo Line Both cigarette and Only heating type Government Offices Bldg. Iidabashi Sta. 2 00 00 heating type are possible 00 is possible Taito 3 Akihabara Tsukudo Elem. Sch. 4 Iidabashi Station Area Akihabara Station Area paspa Iidabashi West Exit Café Veloce Akihabara Station East Exit store Namboku Line/ 36 B-3 52 B-5 Kanda Fire Station Legal Affairs Bureau Onabuta Building 1F 1-7-7 Fujimi Ohgaku Building 1F 2-19 Kanda-Sakumacho Yurakucho Line 70 Taito Branch Office Iidabashi Sta. paspa Iidabashi East Exit Café Veloce Akihabara Station Ekimae-Square store B-5 37 Create Building 1F 1-8-10 Iidabashi B-3 53 Tsk building 1F 104 Kanda-Matsunagacho Agebacho 34 Shohei Elem. Sch. 22 Tabacco Sale Free Smoking Area Toshida Tully's Coffee Akihabara UDX store 29 38 B-3 80 B-5 80 1-7-8 Iidabashi Akihabara UDX 1 4-14-1 Soto-Kanda 69 Tokyo Kusei Kaikan 4 Iidabashi Sta. Soto-Kanda Doutor Coffee Shop Iidabashi Tokyo Kusei-Kaikan store Tully's Coffee Sumitomo Fudosan Akihabara First Building Terrace store 102 Tozai Line 34 B-3 81 B-4 Akihabara Tokyo Kusei Kaikan 3-5-1 Iidabashi Sumitomo Fudosan Akihabara First Building Terrace 1F 1-9-1 Soto-Kanda Kaguragashi Iidabashi Sta. 44 90 Chuo-dori Ave. 87 Sta. 12 Doutor Coffee Shop Iidabashi-Fujimi store 8 35 2-3-10 Fujimi B-2 Kanda- 53 Café de Crie Iidabashi East Exit store Kanda Station Area B-3 Aioicho 69 Rock Belay Building 1F 4-7-1 Iidabashi KISUKE SMOKING SPACE 81 C-4 13 Café de Crie Iidabashi Ramla store 16 3-3-9 Kanda-Kajicho B-2 37 11 70 Iidabashi Central Plaza Ramla 1F 4-25 Iidabashi 35 Iidabashi Kaneko Tobacco Shop Smoking Area 7 10 17 C-4 Akihabara Sta. -

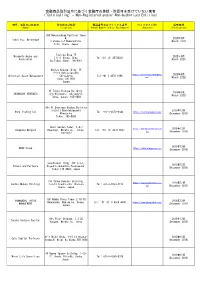

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. 16F Namba Parks Tower 2-10-70 YAMANASHI KYOTO 2019年12月 Nanbanaka, Naniwa-ku, Osaka, Tel: +81 (0) 6-4560-4440 https://www.ykmglobal.com/ MANAGEMENT (December 2019) Japan 8th Floor Shidome, 1.2.20 2019年12月 Tenshi Venture Capital Kaigan, Minatu-ku, Tokyo (December 2019) 6flr Nishi Bldg. -

Tokyo – Ebisu Meguro

92 ©Lonely Planet Publications Pty Ltd E b i s u , M e g u r o & A r o u n d EBISU | DAIKANYAMA | NAKA-MEGURO | MEGURO Neighbourhood Top Five 1 Strolling along the 2 Seeing Japan’s con- 4 Visiting Meguro Meguro-gawa in Naka- tribution to the world of Fudōson (p 95 ), a spiritual Meguro (p 94 ). It’s not so photography at the Tokyo centre since the days of much the river – it’s a canal, Metropolitan Museum of Edo. really – but the unhurried Photography (p 94 ). 5 Browsing the design village vibe and artsy shops 3 Squeezing into a space shops on Meguro-dōri, on either side that make at one of Ebisu’s popular home of MISC (Meguro this one of Tokyo’s most standing bars, like Buri Interior Shops Community; cherished spots. (p100 ). p 95 ). SARUGAKUCHŌ Arisugawa Memorial 01km K e# y Park 00.5miles ū - HIRO-O i Y DAIKANYAMA r am a dō MINAMI- t - e- i AZABU dō EBISU- Meiji-dōri h r # ibuya- s 3 i h ga i i NISHI r S wa ō n Kom -d SHIBUYA- EBISU - azaw a n e KU i a G i r MITA EBISU-MINAMI ō # d 1 i - r a ō 2 d o d a MINATO-KU NAKA- ) r Ya e - N p 2# s y u a k MEGURO mate lo u w MEGURO- s an p a ( at x S a a Pl E -dōr KU k a o t SHIROKANE -z a u i i Shizen r y h a ō h S Kyōiku-en C d ō- SHIROKANEDAI ū h C MEGURO a Gon ak TAKANAWA nosuke-z KAMI- 5# SHIMO- ri ŌSAKI dō MEGURO o- gur Me HIGASHI- 4# ri GOTANDA ō -d a d ra ku Rinshi- a NISHI- Meg S Yatsuya no-mori ur ma-d GOTANDA o- g ōri Kōen awa SHINAGAWA-KU For more detail of this area, see Map p 291 A 93 Lonely Planet’s Explore Ebisu, Meguro & Around Top Tip Ebisu and Meguro are Tokyo on a more human scale, You don’t have to spend with low-rise buildings, shopping arcades and a smatter- much time walking around ing of down-to-earth eateries and bars. -

Fabuleux Tokyo

Index 21_21 Design Sight 32 Dentsu 31 Diète nationale 33 A Drum Museum 26 Ad Museum 31 E Aida, Mitsuo 29 Akagi-jinja 44 Ebisu 41 Akasaka 31 Édifice Sompo Japan 8 Akihabara 46 Edo, ancien château d’ 27 Armani 30 Edo-Tôkyô Museum 45 Asahi 26 Étang de Shinobazu 24 Asakusa 25 Expo Nitten 32 Avenue Jizo dori 47 Avenue Kappabashi-dori 26 F Avenue Omotesandô 18 Fleuve Meguro 41 Avenue Takeshita 17 Fleuve Sumida 26, 35 Ayoama 17 Fuji TV 36 B Fukagawa Edo Museum 46 Brasserie française Paul Bocuse 32 G Bunkamura 16 Gare de Shinjuku 10 Bunkyô Civic Center 45 Gare de Tôkyô 29 C Ginza 30 Ginza Place 30 Café 1894 29 Golden-Gai 12 Capsule hotels 16 Caretta Shiodome 31 H Cathédrale Sainte-Marie de Tôkyô 39 Hanami 27 Cat Street 19 Harajuku 17 Center Gai 15 Hara Museum of Contemporary Art 41 Chien Hachikô 14 Heiseikan 20 Cimetière d’Aoyama 18 Hermès 30 Cimetière de Yanaka 24 Higashi Gyoen 27 Croisière 35 Hikarie 15 D Honkan 20 Horyuji 20 Daikanransha 37 Hôtel Park Hyatt 8 Daikanyama T-Site 41 Hôzô-mon 25 Daykanyama 41 Humax Pavilion 15 http://www.guidesulysse.com/catalogue/FicheProduit.aspx?isbn=9782765872658 I Miraikan 36 Mitsubishi Ichigokan Museum 29 Idemitsu Museum of Arts 28 Mitsui Memorial Museum 29 Ikebukuro 38 Mitsukoshi 30 Institute for Nature Study 42 Mode Gakuen Cocoon Tower 8 Intermediatheque 29 Mori Art Museum 31 Isetan 10 MOT 46 Ito Yokado 12 Musée Artizon 29 J Musée de sculptures Asakura Chôsokan 24 Jardin botanique Koishikawa Shokubut- Musée de Shitamachi 24 suen 45 Musée des sabres japonais 45 Jardin des pivoines 23 Musée Nezu 18 Jardin -

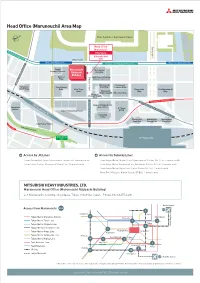

Marunouchi.Pdf

Head Office (Marunouchi) Area Map N Outer Gardens of the Imperial Palace Head Office Gyoko-dori Marunouchi Chiyoda Line Hibiya Sta. Entrance Babasaki-dori Hibiya-dori Side Mita Line Hibiya Sta. Chiyoda Line Nijubashimae Sta. Mita Line Otemachi Sta. Teigeki Marunouchi Meiji Seimei (Imperial Theatre) Nijubashi Kan Bldg. Building Babasaki-dori Yurakucho Line Sta. Kokusai Meiji Yasuda Life Bldg. Bldg. (Marunouchi MY PLAZA) Hibiya Line Hibiya Sta. Marunouchi Marunouchi Yurakucho Shin-Kokusai Park Bldg. 2-chome Bldg. Denki Bldg. Bldg. Shin-Tokyo Marunouchi Shin-Marunouchi Bldg. Marunouchi Bldg. Bldg. BRICK SQUARE Mitsubishi Bldg. Mitsubishi IchigokanMuseum, Tokyo JR Keiyo Line Tokyo Sta. JR YokosukaMarunouchi Line, Sobu LineLine Tokyo Sta. JR Yurakucho Sta. Bank of Mitsubishi UFJ Head Office Yurakucho JP Tower Mullion Tokyo International Forum KITTE Tokyo Bldg. TOKIA Marunouchi Marunouchi Marunouchi South Exit Central Exit North Exit G Tokyo Kotsu-Kaikan i nz a S Tokyo E ta. xpressway Nishi-Ginza JCT JR Tokyo Sta. Access by JR Lines Access by Subway Lines · From Yurakucho Station, International Forum Exit: 5-minute walk · From Tokyo Metro Chiyoda Line, Nijubashimae Station, No. 1 Exit: 2-minute walk · From Tokyo Station, Marunouchi South Exit: 10-minute walk · From Tokyo Metro Yurakucho Line, Yurakucho Station, D1 Exit: 3-minute walk · From Tokyo Metro Hibiya Line, Hibiya Station, B4 Exit: 2-minute walk · From Toei Mita Line, Hibiya Station, B5 Exit: 1-minute walk MITSUBISHI HEAVY INDUSTRIES, LTD. Marunouchi Head Office (Marunouchi Nijubashi -

DAIKYO Completes Construction of Its Lions Forsia Akihabara East And

DAIKYO Completes Construction of Its Lions Forsia Akihabara East and Lions Forsia Tsukiji Station Rental Condominiums—Tenancy Begins Towards End of January ~Catering to teleworking needs through the installation of wall‐mounted work spaces~ TOKYO, Japan ‐ January 22, 2021 ‐ DAIKYO INCORPORATED (“DAIKYO”) announced that tenants can begin moving in to its Lions Forsia Akihabara East and Lions Forsia Tsukiji Station rental condominiums towards end of January. These newly constructed condominiums feature unit plans tailored to teleworking, such as wall‐ mounted storage rails and wall‐mounted desks. Lions Forsia Akihabara East Lions Forsia Tsukiji Station Wall‐mounted storage rails Wall‐mounted desk As work styles such as teleworking diversify, there is a growing need for homes to offer comfortable work spaces. For this reason, DAIKYO is offering unit plans tailored to teleworking in some of its one‐bedroom units at these rental condominiums. Lions Forsia Akihabara East is located six minutes on foot from Akihabara Station on the Tokyo Metro Hibiya Line; it offers a wide variety of unit plans, including one‐bedroom units with a kitchen; one‐bedroom units with a kitchen and dining area; one‐bedroom units with a kitchen, dining, and living area; and two‐bedroom units with a kitchen, dining, and living area. Wall‐mounted storage rails have been installed in five of the condominium’s 38 units. These unique wall‐mounted rails enable tenants to create their own work spaces by attaching and removing shelves and desks. Lions Forsia Tsukiji Station is situated two minutes on foot from Tsukiji Station on the Tokyo Metro Hibiya Line; it occupies an extremely convenient location, with tenants able to access multiple train lines.