Portugal Marketbeat Autumn 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In Lisbon, Portugal

São Nicolau Chiado €1,225,000 Baixa-Chiado Ref: PW1148 Unique development in the heart of Lisbon, Chiado. Telephone: +351 213 471 603 Email: [email protected] Avenida da Liberdade 67B, 5th Floor, 1250-140 Lisboa, Portugal Licence AMI - 14414 | APEMIP 5940 Property Description Unique development in the heart of Lisbon, Chiado. São Nicolau Chiado is a pombaline building, fully renovated where the class and the original traits were kept, making this development timeless. Elegance and efficiency have been combined with original materials, modern design and constructive solutions. The condominium comprises of 18 apartments ranging from 1 to 3 bedroom duplexes and with areas between 55 and 176 sq. m. Chiado is Lisbon's most elegant and trendiest neighborhood is where everyone meets for coffee, shopping, or before dinner and a night out in neighboring Bairro Alto. Situated between the neighborhoods of Bairro Alto and Baixa Pombalina, Chiado is a traditional shopping area that features a mix of old and modern commercial establishments. Many of the buildings in this elegant and trendy location were first built in the 1700s, although many were restored in the 1990s, after their destruction by a devastating fire in 1988. It's a neighborhood that flashes back to the late 19th and early 20th centuries, the "Belle Epoque "when writers such as Fernando Pessoa and Eça de Queiroz used to write at the now- historic cafes. It's also the neighborhood of theaters, of charming old bookshops and major international brands, giving it a lively cosmopolitan ambiance at any time of the day. Despite being just a small part of Lisbon, Chiado truly is a place that’s easy for those who visit to fall in love with. -

Annual Report and Accounts 2018

ANNUAL REPORT AND ACCOUNTS 2018 1 TABLE OF CONTENTS Message from the Chairman .................................................................................................... 4 Nature of the Report ................................................................................................................ 7 i. Metropolitano de Lisboa Group ........................................................................................ 8 1. Organization’s profile ...................................................................................................................... 8 2. Mission, Vision and Values ............................................................................................................ 10 3. Corporate Bodies ........................................................................................................................... 12 4. Management Policies and Mechanisms ........................................................................................ 14 ii. The Metropolitano de Lisboa’s Activity ........................................................................... 17 1. Macroeconomic Framework ......................................................................................................... 17 2. Passenger Transport Service ......................................................................................................... 27 3. Other activities .............................................................................................................................. 33 4. ML’s -

Returning to Portugal This Document Provides Information and Details of Organisations Which May Be Useful If You Are Facing Removal Or Deportation to Portugal

Praxis NOMS Electronic Toolkit A resource for the resettlement of Foreign National Prisoners (FNPs) www.tracks.uk.net Passport I want to leave CLICK HERE the UK I do not want to CLICK HERE leave the UK I am unsure about CLICK HERE Returningleaving the to UK Portugal I will be released CLICK HERE into the UK Copyright © Free Vector Maps.com Returning to Portugal This document provides information and details of organisations which may be useful if you are facing removal or deportation to Portugal. While every care is taken to ensure that the information is correct this does not constitute a guarantee that the organisations will provide the services listed. Your Embassy in the UK Embassy of Portugal 11 Belgrave Square, London SW1X 8PP Tel: 020 7235 5331 Fax: 020 7245 1287 Consular Section 3 Portland Place W1B 1HR Tel: 020 7291 3770 Fax: 020 7291 3799 Email: [email protected] www.portuguese-embassy.co.uk Consulate General in Manchester 1 Portland Street, Manchester M1 3BE Tel: 0161 236 0990 Fax: 0161 236 2064 Email: [email protected] Travel documents A valid Portuguese passport or national identity card or a passport or id card which has expired in the last 5 years can be used to remove you from the UK to Portugal. If you do not have those documents then you will need to be interviewed by the Portuguese officials in order to obtain an Emergency Travel Document (ETD); if you are in prison or detention this will be facilitated by the Home Office. Any supporting evidence of identity or nationality such as birth certificates etc. -

Recomposições E Representações Sociais Das Avenidas Novas Numa

X Congresso Português de Sociologia Na era da “pós-verdade”? Esfera pública, cidadania e qualidade da democracia no Portugal contemporâneo Covilhã, 10 a 12 de julho de 2018 Secção/Área temática / Thematic Section/Area: Territórios: Cidades e Campos Recomposições e representações sociais das Avenidas Novas numa cidade em transformação Recompositions and social representations of Avenidas Novas in a transforming city PINTO, Fernando; ISCTE-IUL; CIES, CP; Lisboa; Portugal; [email protected] Resumo As Avenidas Novas assinalaram uma viragem decisiva no tempo e no modo da expansão urbana de Lisboa, no começo do século XX, sustentando um movimento de ampliação para norte, a partir das coordenadas do plano urbanístico liderado por Ressano Garcia. Associadas desde cedo a uma forte especulação imobiliária, patente na dissonância de tipologias construtivas e na ausência de um plano arquitetónico de conjunto, ficaram também marcadas pelo facto de se terem constituído num dos eixos estruturantes de dilatação do centro funcional da cidade, sofrendo os impactos da terciarização e do uso generalizado do automóvel sobre as suas acessibilidades fáceis. Apresentam-se aqui os primeiros resultados de uma investigação, relativos à história das Avenidas Novas e suas recomposições espaciais. A pesquisa contempla ainda uma contextualização sociodemográfica e socioeconómica e tem o seu foco nas representações sociais sobre esta área da cidade. Palavras-chave:Avenidas Novas; expansão urbana; reconfiguração espacial; mobilidade espacial. Abstract Avenidas Novas marked a turning point in the time and mode of urban expansion in Lisbon at the beginning of the twentieth century, sustaining a movement of expansion from de coordinates of the urban plan led by Ressano Garcia to the north. -

Bairro Altoin Lisbon, Portugal

Rosa 121 / 350 GV POA Bairro Alto Ref: PW1338 The Bairro Alto district is known for its bohemian ambiance, restaurants, bars and its traditional commerce. Telephone: +351 213 471 603 Email: [email protected] Avenida da Liberdade 67B, 5th Floor, 1250-140 Lisboa, Portugal Licence AMI - 14414 | APEMIP 5940 Property Description The Bairro Alto district is known for its bohemian ambiance, restaurants, bars and its traditional commerce. Full of character, only two steps away from the elegant Chiado, this neighbourhood keeps most of its original traits, being one of the oldest and typical areas in Lisbon. Also near to Principe Real and a few metres from one of the best-known sights, Miradouro de São Pedro de Alcântara, a new venture will be born in the Bairro Alto, with an architecture of excellence coupled with the charm and diversity of a single district. Rua da Rosa begins at the Calçada do Combro in Chiado, and steeps to the Rua Dom Pedro V in the mellow Principe Real. A lively cobblestoned street populated with small traditional and inventive restaurants, fado houses and trendy entrepreneur pop-up studios. Rosa 121 offers 10 unique units – 2 shops and 8 studio apartments and areas between 35 m2 and 71 m2. The units, signed by the architectural atelier KLIK Architects, are designed with modern and elegant characteristics, with a special attention to the quality of the finishing materials and construction. 350k GV eligible Furnished Guaranteed yield Enquire for more information. <iframe src="https://www.portugalhomes.com/3d/rosa121/index.html" -

Lisbon-Nouveau Brochure WEB EN

WELCOME Tailor made corporate accommodation solutions in the center of Lisbon. Located in the Saldanha - Marquês de Pombal business district, the Lisbon Nouveau apartments are the ideal solution for the accommodation for your short, medium or long term travelling employees. Fully renovated and equipped with great versatility, the Lisbon Nouveau apartments will make your collaborators feel at home. The generous areas and superior equipment allow the guest to host family and friends comfortably. Mobility and comfort are factors in which we invest in order to contribute to the well-being and productivity of those who travel in business. We hope to earn your trust. Located at the entrance of the Picoas metro station, the Lisbon Nouveau apartments are the ideal mobility solution for your employees. They provide an easy connection to the University of Lisbon by tube, and quick access to the road which links Lisbon to the business centers of Lagoas Park and Tagus Park, allowing direct metro access to Lisbon Airport and the most important points of the city. Within walking distance from the Lisbon Nouveau apartments, the guests can find a wide variety of supermarkets, shopping centers, shops and restaurants, some with extended hours, convenient for long and tiring work days. AIRPORT / PARQUE DAS NAÇÕES PICOAS METRO STATION 15 MIN BY CAR IN FRONT DOWNTOWN / BAIXA-CHIADO 15 MIN BY TUBE MARQUÊS DE POMBAL / AV. LIBERDADE airport 5 MIN WALK oriente red line yellow line alameda blue line saldanha arroios green line picoas PARQUE parque EDUARDO VII MARQUÊS DE POMBAL marquês de pombal AV. LIBERDADE rato avenida ALFAMA PRÍNCIPE REAL martim moniz CASTELO restauradores DE S.JORGE rossio DOWNTOWN baixa-chiado CAIS DO SODRÉ terreiro do paço BELÉM SANTOS CASCAIS cais do sodré TAGUS RIVER APARTMENTS 1A & 2A APARTMENTS 1B & 2B 1 2 5 2 3 1 6 3 4 5 4 6 1 hall NOUVEAU T1 2 kitchnette 3 living room 1A Barbacena Palace 4 suite This apartment accommodates two 5 bathroom people, has a suite with a double bed 6 balcony and a bathroom. -

O Parque Das Nações Em Lisboa Uma Montra Da Metrópole À Beira Tejo

Tese apresentada para cumprimento dos requisitos necessários à obtenção do grau de Doutor em Sociologia, especialidade de Sociologia Urbana, do Território e do Ambiente, realizada sob a orientação científica de Luís Vicente Baptista e R. Timothy Sieber. Investigação apoiada pela Fundação para a Ciência e Tecnologia com a bolsa com a referência SFRH/BD/37598/2007, financiada por fundos nacionais do MEC. Aos meus pais e ao Helder. Agradecimentos A todos aqueles que, a título pessoal ou institucional, aceitaram ser entrevistados, conversar ou passear, aqui em Lisboa, mas também em Boston. Sem eles este trabalho não existiria. Ao Luís Baptista por me ter contagiado com o seu entusiasmo pela cidade, pela liberdade que, enquanto orientador, me proporcionou no trabalho, mas também por me incluir em tantos outros projectos, com os quais muito aprendi. Ao Tim Sieber por me ter apresentado Boston e o seu porto e por, mesmo à distância, estar atento e ter sempre uma palavra de incentivo. À Catharina Thörn e ao Heitor Frúgoli Jr. pelo interesse que demonstraram no meu trabalho. Ao Gonçalo Gonçalves, à Graça Cordeiro, à Inês Pereira, ao João Pedro Nunes, à Lígia Ferro e à Rita Cachado pelos projectos partilhados, mas também pelo círculo de simpatia e amizade. Aos amigos Carolina Rojas, Cristina Pinto, Edalina Sanches, Grete Viddal, Hélène Bettembourg, Jim Bettembourg Mendes, Pedro Gomes, Rahul Kumar, Rita António, Rita Santos, Sérgio Paes, Sofia Ferreira e Tiago Mendes, pelos momentos partilhados ao longo dos anos. Ainda aos colegas e amigos Ana Fernandes, Inês Vieira, Joana Lucas, João Martins, Jordi Nofre, Paula Gil, Patrícia Paquete, Rachel Almeida e Rita Burnay, pelas conversas e sugestões. -

Hygiea Internationalis

Regional Dynamics and Social Diversity – Portugal in the 21st Century Teresa Ferreira Rodrigues Introduction hrough its history Portugal always presented regional differences concerning population distribution, as well as fertility and mortality trends. Local T specificities related to life and death levels reflect diverse socioeconomic conditions and also different health coverage. We will try to diagnose the main concerns and future challenges related to those regional differences, using quantitative and qualitative data on demographic trends, well-being average levels and health services offer. We want to demonstrate that this kind of academic researches can be useful to policy makers, helping them: (1) to implement regional directed policies; (2) to reduce internal diversity; and (3) to improve quality of life in the most excluded areas. Our first issue consists in measuring the link between Portuguese modernization and asymmetries on social well-being levels1. Today Portugal faces some modera- tion on population growth rates, a total dependency on migration rates, both exter- nal and internal, as well as aged structures. But national average numbers are totally different from those at a regional level, mainly if using non demographic indicators, such as average living patterns or purchase power2. The paper begins with a short diagnosis on the huge demographic and socioeco- nomic changes of the last decades. In the second part we analyze the extent of the link between those changes and regional convergence on well-being levels. Finally, we try to determine the extent of regional contrasts, their main causes and the rela- tionship between social change and local average wealth standards, as well as the main problems and challenges that will be under discussion in the years to come, in what concerns to health policies. -

Lista De 28 De Fevereiro a 06 De Março De 2020

Lista de 28 de Fevereiro a 06 de Março de 2020 Nome Tipo Data de Início Data de Fim Processo Morada Freguesia UIT Novo Programa Ricardo Araújo Pereira Filmagem 01-03-2020 07-06-2020 214/POEP/2020 Avenida Fontes Pereira de Melo Arroios Centro Calçada do Monte, Rua da Senhora do Monte, Rua de São Gens, Amar Demais Filmagem 02-03-2020 06-03-2020 250/POEP/2020 São Vicente Centro Histórico Travessa do Monte, Rua Damasceno Monteiro Misericórdia, Santa Maria Distribuição de Flyers Publicitário 05-02-2020 29-04-2020 46/POEP/2020 Praça de Luís de Camões, Rua Garrett Centro Histórico Maior Praça do Comércio, Rua Gomes Freire, Calçada do Monte, Campo dos Santa Maria Maior, Arroios, O Atentado Filmagem 29-02-2020 29-02-2020 255/POEP/2020 Mártires da Pátria, Rua Júlio de Andrade, Paço da Rainha, Travessa da Centro Histórico, Centro São Vicente, Santo António Cruz do Torel Terramotto Vs Moda Lisboa vs CML - 54ª edição Moda Estrela, Misericórdia, Avenidas Divertimento/Espetáculo 26-02-2020 05-03-2020 150/POEP/2020 Largo Vitorino Damásio, Cais do Sodré, Campo Pequeno Centro Histórico, Centro Lisboa Novas Largo Trindade Coelho, Rua Delfim de Brito Guimarães, Rua de São Misericórdia, Campolide, Lázaro, Terreiro do Trancão, Antigas Oficinas Metropolitano Calvanas, Centro Histórico, Centro, Lançamento Mundial Novo Mini Eléctrico Publicitário 01-02-2020 23-03-2020 57/POEP/2020 Santa Maria Maior, Parque das Avenida da Ribeira das Naus, Rua do Arsenal, Rua do Alecrim, Praça do Oriental, Norte Nações, Lumiar Comércio Praça do Duque de Saldanha, Praça dos Restauradores, -

Discover Lisbon with Our Guide!

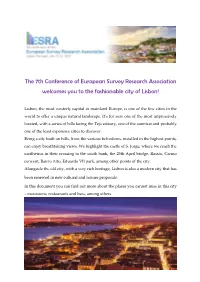

The 7th Conference of European Survey Research Association welcomes you to the fashionable city of Lisbon! Lisbon, the most westerly capital in mainland Europe, is one of the few cities in the world to offer a unique natural landscape. It’s for sure one of the most impressively located, with a series of hills facing the Tejo estuary, one of the sunniest and probably one of the least expensive cities to discover. Being a city built on hills, from the various belvederes, installed in the highest points, can enjoy breathtaking views. We highlight the castle of S. Jorge, where we reach the cacilheiros in their crossing to the south bank, the 25th April bridge, Rossio, Carmo convent, Bairro Alto, Eduardo VII park, among other points of the city. Alongside the old city, with a very rich heritage, Lisbon is also a modern city that has been renewed in new cultural and leisure proposals. In this document you can find out more about the places you cannot miss in this city – excursions, restaurants and bars, among others. Index What to see & Where to walk............................................................................................... 4 Tram 28E route – the best way to know Lisbon ......................................................4 Prazeres cemetery ..........................................................................................................6 Santo Condestável Church ..............................................................................................6 Basílica da Estrela and garden .......................................................................................6 -

The Working-Class Houses and Its Insertion in Urban Areas

THE WORKING-CLASS HOUSES AND ITS INSERTION IN URBAN AREAS THE 33 MUNICIPAL CASE STUDIES OF THE CITY OF LISBON _________________________________________________________________________________ José Miguel Moreira Correia ABSTRACT The purpose of this study is to analyze the insertion of 33 municipality working-class houses of in the urban fabric of the city of Lisbon. The methodology adopted was based on the Spatial Syntax theory by using the measurements of choice and integration in a Geographic Information Systems environment. The first step was the analysis of 33 cases studies with normalized angular measures of integration and choice, from the global scale to the local scale with radii of 400 m, 800 m, 1200 m and 2000 m respectively. The second step was a detailed analysis based on the adjacency of the spaces from the public street to the dwellings for a subset of 4 working-class houses, selected due to their type-morphological diversity. From the first analysis (the 33 study cases), it was possible to conclude that the patios and the workers' villages have high insertion values in the neighborhood, highlighting the idea that this type of construction intended to promote the proximity of the dwellings to the factories. At the global level the insertion value is weaker, however with a positive growth trend in the period analyzed (1871 - 2005). For all study cases it was verified that the courtyard acts as an aggregating element of the collective space, although it can be accessed in very different ways, which in translates into a proper identity for each patio/village worker. Keywords: Workforce housing Space Syntax analysis Urban morphology Housing GIS November 2018 INTRODUCTION This work is part of a protocol established between the Instituto Superior Técnico (IST) – CERIS research center and the Municipality of Lisbon to study the 33 municipal working-class houses. -

International Literary Program

PROGRAM & GUIDE International Literary Program LISBON June 29 July 11 2014 ORGANIZATION SPONSORS SUPPORT GRÉMIO LITERÁRIO Bem-Vindo and Welcome to the fourth annual DISQUIET International Literary Program! We’re thrilled you’re joining us this summer and eagerly await meeting you in the inimitable city of Lisbon – known locally as Lisboa. As you’ll soon see, Lisboa is a city of tremendous vitality and energy, full of stunning, surprising vistas and labyrinthine cobblestone streets. You wander the city much like you wander the unexpected narrative pathways in Fernando Pessoa’s The Book of Disquiet, the program’s namesake. In other words, the city itself is not unlike its greatest writer’s most beguiling text. Thanks to our many partners and sponsors, traveling to Lisbon as part of the DISQUIET program gives participants unique access to Lisboa’s cultural life: from private talks on the history of Fado (aka The Portuguese Blues) in the Fado museum to numerous opportunities to meet with both the leading and up-and- coming Portuguese authors. The year’s program is shaping up to be one of our best yet. Among many other offerings we’ll host a Playwriting workshop for the first time; we have a special panel dedicated to the Three Marias, the celebrated trio of women who collaborated on one of the most subversive books in Portuguese history; and we welcome National Book Award-winner Denis Johnson as this year’s guest writer. Our hope is it all adds up to a singular experience that elevates your writing and affects you in profound and meaningful ways.