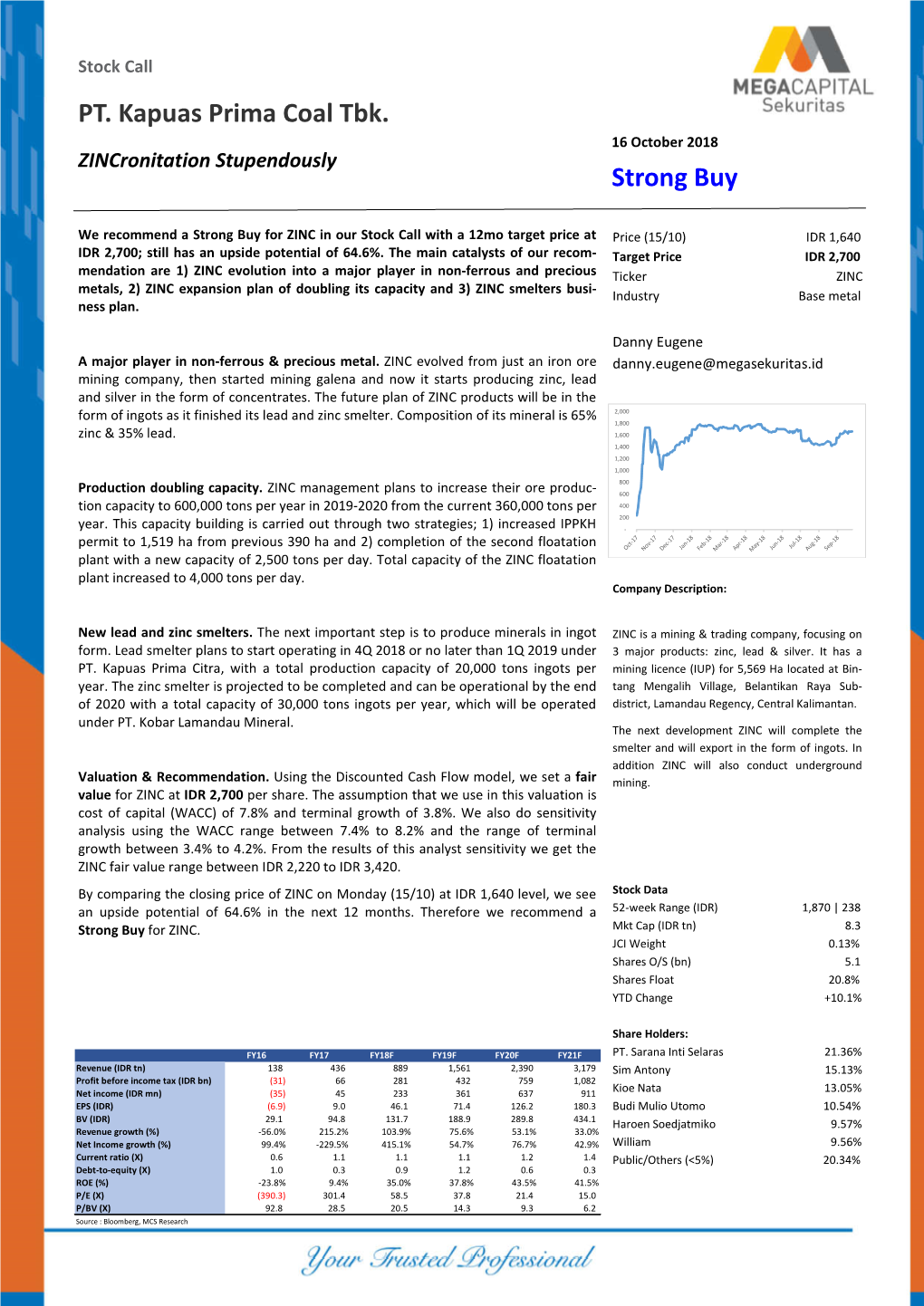

PT. Kapuas Prima Coal Tbk. Strong

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

33 CHAPTER II GENERAL DESCRIPTION of SERUYAN REGENCY 2.1. Geographical Areas Seruyan Regency Is One of the Thirteen Regencies W

CHAPTER II GENERAL DESCRIPTION OF SERUYAN REGENCY 2.1. Geographical Areas Seruyan Regency is one of the thirteen regencies which comprise the Central Kalimantan Province on the island of Kalimantan. The town of Kuala Pembuang is the capital of Seruyan Regency. Seruyan Regency is one of the Regencies in Central Kalimantan Province covering an area around ± 16,404 Km² or ± 1,670,040.76 Ha, which is 11.6% of the total area of Central Kalimantan. Figure 2.1 Wide precentage of Seruyan regency according to Sub-District Source: Kabupaten Seruyan Website 2019 Based on Law Number 5 Year 2002 there are some regencies in Central Kalimantan Province namely Katingan regency, Seruyan regency, Sukamara regency, Lamandau regency, Pulang Pisau regency, Gunung Mas regency, Murung Raya regency, and Barito Timur regency 33 (State Gazette of the Republic of Indonesia Year 2002 Number 18, additional State Gazette Number 4180), Seruyan regency area around ± 16.404 km² (11.6% of the total area of Central Kalimantan). Administratively, to bring local government closer to all levels of society, afterwards in 2010 through Seruyan Distric Regulation Number 6 year 2010 it has been unfoldment from 5 sub-districts to 10 sub-districts consisting of 97 villages and 3 wards. The list of sub-districts referred to is presented in the table below. Figure 2.2 Area of Seruyan Regency based on District, Village, & Ward 34 Source: Kabupaten Seruyan Website 2019 The astronomical position of Seruyan Regency is located between 0077'- 3056' South Latitude and 111049 '- 112084' East Longitude, with the following regional boundaries: 1. North border: Melawai regency of West Kalimantan Province 2. -

DECISION Number 45/PUU-IX/2011 for the SAKE OF

DECISION Number 45/PUU-IX/2011 FOR THE SAKE OF JUSTICE UNDER THE ONE ALMIGHTY GOD THE CONSTITUTIONAL COURT OF THE REPUBLIC OF INDONESIA [1.1] Hearing constitutional cases at the first and final levels has passed a decision in the case of petition for Judicial Review of Law Number 41 Year 1999 concerning Forestry as amended by Law Number 19 Year 2004 concerning the Stipulation of Government Regulation in Lieu of Law Number 1 Year 2004 concerning Amendment to Law Number 41 Year 1999 concerning Forestry to become a Law under the 1945 Constitution of the Republic of Indonesia, filed by: [1.2] 1. Regional Government of Kapuas Regency represented by: Name : Ir. H. Muhammad Mawardi, MM. Place/date of birth : Amuntai, June 5, 1962 Occupancy : Regent of Kapuas, Central Kalimantan Province Address : Jalan Pemuda KM. 55 Kuala Kapuas referred to as --------------------------------------------------- Petitioner I; 2. Name : Drs. Hambit Bintih, MM. Place/date of birth : Kapuas, February 12, 1958 Occupation : Regent of Gunung Mas, Central Kalimantan Province 2 Address : Jalan Cilik Riwut KM 3, Neighborhood Ward 011, Neighborhood Block 003, Kuala Kurun Village, Kuala Kurun District, Gunung Mas Regency referred to as -------------------------------------------------- Petitioner II; 3. Name : Drs. Duwel Rawing Place/date of birth : Tumbang Tarusan, July 25, 1950 Occupation : Regent of Katingan, Central Kalimantan Province Address : Jalan Katunen, Neighborhood Ward 008, Neighborhood Block 002, Kasongan Baru Village, Katingan Hilir District, Katingan Regency referred to as -------------------------------------------------- Petitioner III; 4. Name : Drs. H. Zain Alkim Place/date of birth : Tampa, July 11, 1947 Occupation : Regent of Barito Timur, Central Kalimantan Province Address : Jalan Ahmad Yani, Number 97, Neighborhood Ward 006, Neighborhood Block 001, Mayabu Village, Dusun Timur District, Barito Timur Regency 3 referred to as ------------------------------------------------- Petitioner IV; 5. -

Strategi Pemerintah Kabupaten Sukamara Dalam Pemberdayaan

WACANA Vol. 13 No. 1 Januari 2010 ISSN. 1411-0199 STRATEGI PEMERINTAH KABUPATEN SUKAMARA DALAM PEMBERDAYAAN EKONOMI MASYARAKAT (Studi Tentang Pemberdayaan Usaha Kecil Pembuatan Kerupuk Ikan Di Kecamatan Sukamara Kabupaten Sukamara Propinsi Kalimantan Tengah) Strategies of the Sukamara Regency Government in Empowering Community Economic (Study about Empowerment of Fish Chips Small Businesses at the Sukamara Sub District, Central Kalimantan). ISWAN GEMAYANA Mahasiswa Program Magister Ilmu Administrasi Publik, PPSUB Sukanto dan Ismani HP Dosen Jurusan Ilmu Administrasi Publik, FIAUB ABSTRAK Penelitian berawal dari latar belakang masalah tentang upaya oleh pemerintah kabupaten Sukamara dalam memberdayakan usaha kecil pembuatan kerupuk ikan di Kecamatan Sukamara kabupaten Sukamara mengingat sampai saat ini, masih belum mampu menjadikan usaha kecil pembuat kerupuk ikan sebagai produk unggulan. Tujuan dari penelitian ini ialah untuk mendiskripsikan dan menganalisis: (1) Potensi usaha kecil pembuatan kerupuk ikan di Kecamatan Sukamara Kabupaten Sukamara, (2) Strategi pemberdayaan usaha kecil pembuatan kerupuk ikan di Kecamatan Sukamara Kabupaten Sukamara dan (3) Faktor-faktor penghambat dan pendukung dalam pemberdayaan usaha kecil pembuatan kerupuk ikan di Kecamatan Sukamara Kabupaten Sukamara. Jenis penelitian yang dilakukan dalam penelitian ini adalah penelitian kwalitatif dengan lokasi penelitian pada pengusaha kecil pembuatan kerupuk di Kecamatan Sukamara Kabupaten Sukamara Propinsi Kalimantan Tengah. Analisis yang dilakukan dengan mengikuti model Miles Huberman yaitu analisis interaktif. Hasil penelitian menunjukkan bahwa upaya yang dilakukan oleh Pemerintah Kabupaten Sukamara dalam memberdayakan pengusaha kecil pembuat kerupuk ikan telah dilakukan, namun belum bisa dilakukan secara maksimal mengingat Pemerintah Kabupaten Sukamara sebagai pemerintahan baru hasil pemekaran mengalami beberapa kendala diantaranya keterbatasan personil, alokasi anggaran masih terserap untuk pembuatan infrastruktur gedung-gedung perkantoran pemerintah dan penataan organisasi kedalam. -

Identification of Factors Affecting Food Productivity Improvement in Kalimantan Using Nonparametric Spatial Regression Method

Modern Applied Science; Vol. 13, No. 11; 2019 ISSN 1913-1844 E-ISSN 1913-1852 Published by Canadian Center of Science and Education Identification of Factors Affecting Food Productivity Improvement in Kalimantan Using Nonparametric Spatial Regression Method Sifriyani1, Suyitno1 & Rizki. N. A.2 1Statistics Study Programme, Department of Mathematics, Faculty of Mathematics and Natural Sciences, Mulawarman University, Samarinda, Indonesia. 2Mathematics Education Study Programme, Faculty of Teacher Training and Education, Mulawarman University, Samarinda, Indonesia. Correspondence: Sifriyani, Statistics Study Programme, Department of Mathematics, Faculty of Mathematics and Natural Sciences, Mulawarman University, Samarinda, Indonesia. E-mail: [email protected] Received: August 8, 2019 Accepted: October 23, 2019 Online Published: October 24, 2019 doi:10.5539/mas.v13n11p103 URL: https://doi.org/10.5539/mas.v13n11p103 Abstract Problems of Food Productivity in Kalimantan is experiencing instability. Every year, various problems and inhibiting factors that cause the independence of food production in Kalimantan are suffering a setback. The food problems in Kalimantan requires a solution, therefore this study aims to analyze the factors that influence the increase of productivity and production of food crops in Kalimantan using Spatial Statistics Analysis. The method used is Nonparametric Spatial Regression with Geographic Weighting. Sources of research data used are secondary data and primary data obtained from the Ministry of Agriculture -

Usaid Lestari

USAID LESTARI LESSONS LEARNED TECHNICAL BRIEF OPTIMIZATION OF REFORESTATION FUND IN CENTRAL KALIMANTAN MARCH 2020 This publication was produced for review by the United States Agency for International Development. It was prepared by Tetra Tech ARD. This publication was prepared for review by the United States Agency for International Development under Contract # AID-497-TO-15-00005. The period of this contract is from July 2015 to July 2020. Implemented by: Tetra Tech P.O. Box 1397 Burlington, VT 05402 Tetra Tech Contacts: Reed Merrill, Chief of Party [email protected] Rod Snider, Project Manager [email protected] USAID LESTARI – Optimization of Reforestation Fund in Central Kalimantan Page | i LESSONS LEARNED TECHNICAL BRIEF OPTIMIZATION OF REFORESTATION FUND IN CENTRAL KALIMANTAN MARCH 2020 DISCLAIMER This publication is made possible by the support of the American People through the United States Agency for International Development (USAID). The contents of this publication are the sole responsibility of Tetra Tech ARD and do not necessarily reflect the views of USAID or the United States Government. USAID LESTARI – Optimization of Reforestation Fund in Central Kalimantan Page | ii TABLE OF CONTENTS Acronyms and Abbreviations iv Executive Summary 1 Introduction: Reforestation Fund, from Forest to Forest 3 Reforestation Fund in Central Kalimantan Province: Answering the Uncertainty 9 LESTARI Facilitation: Optimization of Reforestation Fund through Improving FMU Role 15 Results of Reforestation Fund Optimization -

Download Article

Advances in Social Science, Education and Humanities Research, volume 84 International Conference on Ethics in Governance (ICONEG 2016) Local Knowledge of Dayak Tomun Lamandau About the Honey Harvest Brian L. Djumaty Antakusuma University Pangkalan Bun, Indonesia [email protected] Abstract--Culture is the result of a set of experiences provided by observations and documents [5]. This type of research is nature. like the local knowledge to harvest honey by society descriptive. Descriptive Aiming to describe accurately the Tomun Lamandau, Central Borneo. This research uses characteristics and focus on the fundamental question of descriptive qualitative method and data collection techniques "How" for trying to acquire and convey the facts clearly and including observation, interviews, and documentation. The accurately [6]. The goal is to describe accurately the results showed that society already have knowledge about protecting nature in a way as not to damage the honeycomb and characteristics of a phenomenon or problem studied so as to tree. Some of the equipment used to harvest the honey has been convey the facts clearly and accurately [7]. modified. B. Research Field Keywords: Local Knowledge, Dayaknese, Protecting Nature This research was carried out starting from a survey of Introduction student placement Field Work Experience (KKN) Antakusuma I. INTRODUCTION University in Kabupatan Lamandau. Writer fascinated by the Based on data from the Central Statistics Agency (BPS) in culture of the local community. One of them is the knowledge 2010, there are more than 300 ethnic groups or tribes 1.340 or of local communities to harvest the honey. more than 300 ethnic groups. The diversity of the culture of This research was conducted in June-August 2016. -

Attacks on Forest-Dependent Communities in Indonesia and Resistance Stories

ATTACKS ON FOREST-DEPENDENT COMMUNITIES IN INDONESIA AND RESISTANCE STORIES Photo: Sahabat Hutan Harapan A Compilation of WRM Bulletin Articles March 2021 WORLD RAINFOREST MOVEMENT Attacks on Forest-Dependent Communities in Indonesia and Resistance Stories A Compilation of WRM Bulletin Articles March 2021 INDEX INTRODUCTION ................................................................................................................................................... 4 ATTACKS ON FOREST-DEPENDENT COMMUNITIES .............................................. 7 “Paper Dragons”: Timber Plantation Corporations and Creditors in Indonesia ............... 7 Large-scale investments and climate conservation initiatives destroy forests and people’s territories ................................................................................................................................................................... 10 Indonesia: Proposed laws threaten to reinstate corporate control over agrodiversity ................................................................................................................................................................................... 13 Indonesia: Exploitation of women and violation of their rights in oil palm plantations ................................................................................................................................................................. 16 Indonesia: Oil palm plantations and their trace of violence against women ............................ 20 Indonesia: -

Optimization of Reforestation Fund in Central Kalimantan

USAID LESTARI LESSONS LEARNED TECHNICAL BRIEF OPTIMIZATION OF REFORESTATION FUND IN CENTRAL KALIMANTAN MARCH 2020 This publication was produced for review by the United States Agency for International Development. It was prepared by Tetra Tech ARD. This publication was prepared for review by the United States Agency for International Development under Contract # AID-497-TO-15-00005. The period of this contract is from July 2015 to July 2020. Implemented by: Tetra Tech P.O. Box 1397 Burlington, VT 05402 Tetra Tech Contacts: Reed Merrill, Chief of Party [email protected] Rod Snider, Project Manager [email protected] USAID LESTARI – Optimization of Reforestation Fund in Central Kalimantan Page | i LESSONS LEARNED TECHNICAL BRIEF OPTIMIZATION OF REFORESTATION FUND IN CENTRAL KALIMANTAN MARCH 2020 DISCLAIMER This publication is made possible by the support of the American People through the United States Agency for International Development (USAID). The contents of this publication are the sole responsibility of Tetra Tech ARD and do not necessarily reflect the views of USAID or the United States Government. USAID LESTARI – Optimization of Reforestation Fund in Central Kalimantan Page | ii TABLE OF CONTENTS Acronyms and Abbreviations iv Executive Summary 1 Introduction: Reforestation Fund, from Forest to Forest 3 Reforestation Fund in Central Kalimantan Province: Answering the Uncertainty 9 LESTARI Facilitation: Optimization of Reforestation Fund through Improving FMU Role 15 Results of Reforestation Fund Optimization -

Government Expenditure and Poverty Reduction in the Proliferation Areas of Central Kalimantan, Indonesia

Journal of Socioeconomics and Development. 2020. 3(2): 47–56 Journal of Socioeconomics and Development https://publishing-widyagama.ac.id/ejournal-v2/index.php/jsed Government expenditure and poverty reduction in the proliferation areas of Central Kalimantan, Indonesia Andrie Elia, Yulianto, Harin Tiawon, Sustiyah*, and Kusnida Indrajaya University of Palangka Raya, Palangka Raya, Indonesia *Correspondence email: [email protected] ARTICLE INFO ABSTRACT ►Research Article The purpose of this study was to analyze the relationship between government expenditure and poverty, and also linked to the regional economic activity and Article History labor absorption. The study used a quantitative research by means of time series Received 13 June 2020 data collected from the new proliferation area in Central Kalimantan, including Accepted 28 July 2020 Pulang Pisau, Katingan, East Barito, Seruyan, Gunung Mas, Murung Raya, Published October 2020 Sukamara, and Lamandau. Analysis method used the path analysis to estimate Keywords statistical parameters indicating relationship between variables. The research government expenditure; result shows that poverty significantly effects on government expenditure in the grdp; labor absorption; new eight regency in Central Kalimantan province. Poverty has also had an Kalimantan; poverty impact on government expenditure through the provision of employment and Gross Regional Domestic Product (GRDP). The local government is expected to JEL Classification manage more effectively regional finances that focus on community economic H72; I38; J21 activities. The policy also opens investment opportunity to increase economic activity and create jobs based on the prominent regional product, such as agriculture, plantation and mining sectors. Investment can increase employment and indirectly reduce poverty. Citation: Elia, A., Yulianto, Tiawon, H., Sustiyah, and Indrajaya, K. -

Sapaan Dalam Bahasa Dayak Tomun Di Desa Sekoban

PLAGIAT MERUPAKAN TINDAKAN TIDAK TERPUJI SAPAAN DALAM BAHASA DAYAK TOMUN DI DESA SEKOBAN, KECAMATAN LAMANDAU, KABUPATEN LAMANDAU, PROVINSI KALIMANTAN TENGAH Skripsi Diajukan untuk Memenuhi Salah Satu Syarat Memperoleh Gelar Sarjana Sastra Indonesia Program Studi Sastra Indonesia Oleh Nicki Pratama NIM : 144114005 PROGRAM STUDI SASTRA INDONESIA FAKULTAS SASTRA UNIVERSITAS SANATA DHARMA YOGYAKARTA MEI 2018 - PLAGIAT MERUPAKAN TINDAKAN TIDAK TERPUJI I l Skripsi SAPAATI DALAM BAHASA DAYAK TOMUN DI DESA SEKOBAI\, KECAMATAI\I LAMANDAU KABT]PATf,,N LAMANDA,U, PROYINSI KALIMANTAIY TENGAH v . I. kaptomo Baryadi, M.Hum. tanggal30 April2018 PLAGIAT MERUPAKAN TINDAKAN TIDAK TERPUJI PLAGIAT MERUPAKAN TINDAKAN TIDAK TERPUJI PERNYATAAN KEASLIAN KARYA Saya menyatakan dengan sesungguhnya bahwa skripsi yang saya tulis ini tidak memuat karya atau bagian karya orang lain, kecuali yang telah disebutkan dalam kutipan dan daftar pustaka sebagaimana layaknya karya ilmiah. Yogyakarta, Nicki Pratama IV PLAGIAT MERUPAKAN TINDAKAN TIDAK TERPUJI Pernyataan Persetujuan Publikasi Karya Ilmiah untuk Kepentingan Akademis Yang bertanda tangan di bawah ini, saya mahasiswa Universitas Sanata Dharma: Nama : Nicki Pratama NIM :144114005 Demi pengembangan ilmu pengetahuan, saya memberikan kepada Perpustakaan Universitas Sanata Dharma karya ilmiah saya yang berjudul Sapaan Dalam Bahasa Dayak Tomun <ii Desa Sekoban, Kecamatan Lamanciau, Kabupaten Lamandau, Provinsi Kalimantan Tengah beserta perangkat yang diperlukan (bila ada). Dengan demikian, saya memberikan kepada Perpustakaan Universitas Sanata Dharma hak menyimpan, mengalihkan'dalam bentuk lain, mengelolanya dalam bentuk pangkalan data, mendistribusikan secara terbatas dan mempublikasikannya di internet atau media yang lain untuk kepentingan akademis tanpa perlu meminta izin dari saya maupun memberikan loyality kepada saya selama tetap mencantumkan nama saya sebagai penulis. Demikian pernyataan saya buat dengan sebenarnya. -

Effects of Education Funding in Increasing Human Development Index

Jejak Vol 12 (2) (2019): 482-497 DOI: https://doi.org/10.15294/jejak.v12i2.23391 JEJAK Journal of Economics and Policy http://journal.unnes.ac.id/nju/index.php/jejak Effects of Education Funding in Increasing Human Development Index Mukhammad Yogiantoro1 , 2Diah Komariah, 3Irawan Irawan 1,2,3Post-Graduate Program, Masters in Economics, Palangka Raya University Permalink/DOI: https://doi.org/10.15294/jejak.v12i2.23391 Received: May 2019; Accepted: July 2019; Published: September 2019 Abstract Every citizen has the right to get education with the aim of educating the nation's life as mandated in the opening of the 1945 Constitution. This study aims to determine the efficiency of education funding both from the APBN and the APBD purely in relation to increasing HDI and educational performance. The study uses influence analysis with multiple regression and descriptive quantitative research, with 3 variables, namely the large variable education funding from APBD and APBN, Education Performance and Human Development Index. The sample selection method used was purposive sampling, namely in Regencys / Cities in Central Kalimantan in the Period of 2015 - 2017. Research resulted in a relationship between education funding and HDI, Education and Performance Funds for Education and HDI and Educational Performance. Educational performance in this case is measured by teacher qualifications, teacher certification, educational ratios (Teachers: Students and Classes: Students), facilities and infrastructures physical condition, Gross Participation Rate (APK), Pure Participation Rate (APM), and Dropout Numbers. In the multiple regression, the effect of education funding both from the APBD and the APBN does not affect more dominantly in increasing Human Development Index. -

Indonesia: Rollback in the Time of COVID-19

Indonesia: Rollback in the Time of COVID-19 Non-Transparent Policy Changes, Continued Neglect and Criminalisation of Indigenous Peoples during the COVID-19 pandemic in Indonesia DISCUSSION PAPER FEBRUARY 2021 Mia Siscawati, Ph.D. | Senior Lecturer, School of Strategic and Global Studies, Universitas Indonesia Cover images Left: Samuel and his son check their fishing net for a catch. Dayak Bahau Busaang indigenous community of Long Isun, East Kalimantan, Indonesia. Credit: Angus MacInnes / FPP Right: People of the village, sprayers in hand, lining up to fill their tanks with disinfectant - Dayak Iban from Sungai Utik, Borneo, Indonesia Credit: Kynan Tegar / If Not Us Then Who ROLLBACK IN THE TIME OF COVID-19 1 Foreword The Covid-19 pandemic became a ghost terrifying everybody throughout 2020 and has yet to end. Indonesia is one of the most affected countries in South East Asia. Thousands have lost their lives, and hundreds of thousands, or even millions, of people have lost their job, which will in turn affect those dependent on them. This is not to mention the impacts on those whose lives are completely dependent on land and forests. The report assessing the impacts of the pandemic on indigenous peoples has opened our eyes that when the world is increasingly centered on industrial and urban-centric lives, there are millions of people out there who have been struggling hard to survive on land and forests, even long before the pandemic. They are indigenous peoples living in and around tropical forests – forests that have been sustaining earth’s life. These peoples are the true land and forest defenders.