Press Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Senior Resource Guide

SENIOR RESOURCE GUIDE Non-Profit and Public Agencies Serving NORTH ALAMEDA COUNTY Alameda ● Albany ● Berkeley ● Emeryville ● Oakland ● Piedmont Senior Information & Assistance Program – Alameda County Area Agency on Aging 6955 Foothill Blvd, Suite 143 (1st Floor), Oakland, CA 94605; 1-800-510-2020 / 510-577-3530; http://seniorinfo.acgov.org Office Hours : 8:30am – 4pm Monday – Friday ADULT DAY CARE/RESPITE (useful website: www.daybreakcenters.org): Alzheimer's Services of the East Bay - ASEB, Berkeley, www.aseb.org .................................................................................................................................... 510-644-8292 Bay Area Community Services - BACS, Oakland, http://bayareacs.org ................................................................................................................................... 510-601-1074 Centers for Elders Independence - CEI, (PACE - Program of All-inclusive Care for the Elderly); www.cei.elders.org ..................................................... 844-319-1150 DayBreak Adult Care Centers, (personalized referrals & community education); http://daybreakcenters.org ................................................................ 510-834-8314 Hong Fook Adult Day Health Care, Oakland, (14th Street site); www.fambridges.org ........................................................................................................ 510-839-9673 Hong Fook Adult Day Health Care, Oakland, (Harrison Street site); www.fambridges.org ................................................................................................ -

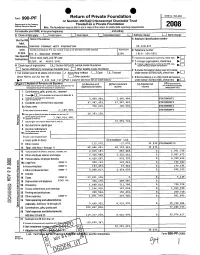

Form 990-PF Return of Private Foundation

0 0 Return of Private Foundation OMB No 1545-0052 Form 990-PF or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service 2008 Note. The foundation may be able to use a copy of this return to satisfy state reporting requirements. For calendar year 2008 , or tax year beginning , and ending G Check all that apply Initial return Final return Amended return L_J Address change Name change A Employer identification number Use the IRS Name of foundation label. Otherwise, HARLES STEWART MOTT FOUNDATION 38-1211227 print Number and street (or P 0 box number if mail is not delivered to street address ) Room/su to B Telephone number or type . 03 S. SAGINAW STREET 200 (810) 238-5651 See Specific City or town, state, and ZIP code C If exemption application is pending, check here Instructions . ► LINT MI 48502-1851 D 11.Foreign organizations, check here • 2. Foreign organizations meeting the 85% test. H Check typea of organization: XSection 501 (c)(3) exempt private foundation check here and attach computation = Section 4947(a)( 1 ) nonexemp t charitable trus t 0 Other taxable private foundation E If private foundation status was terminated I Fair market value of all assets at end of year J Accounting method: L_J Cash X Accrua l under section 507(b)(1)(A), check here (from Part ll, col (c), line 16) 0 Other (specify) F If the foundation is in a 60-month termination 1 933 , 369 747. (Part 1, column (d) must be on cash basis) under section 507(b)(1)(B), check here Part I Analysis of Revenue and Expenses (a) Revenue and (b) Net investment (c) Adjusted net (d) Disbursements (The total of amounts in columns ( b), (c), and (d) may not for charitable purposes necessarily equal the amounts in column (a) ex p enses p er books income income (cash basis only) 1 Contributions, gifts, grants, etc., received 2 Check it the foundation is not required to attach Sch B on savings and temporary 3 , 460 , 484. -

CDPH/OA/ADAP) Pharmacy Network Listing June 24, 2016

California Department of Public Health Office of AIDS, AIDS Drug Assistance Program (CDPH/OA/ADAP) Pharmacy Network Listing June 24, 2016 DIRECTORY OF CITIES Directory of cities .......................................................................................................................................................1 ACTON, CA ........................................................................................................................................................... 20 ADELANTO, CA ..................................................................................................................................................... 21 ALAMEDA, CA ...................................................................................................................................................... 22 ALBANY, CA .......................................................................................................................................................... 23 ALHAMBRA, CA .................................................................................................................................................... 24 ALISO VIEJO, CA ................................................................................................................................................... 25 ALTADENA, CA ..................................................................................................................................................... 26 AMERICAN CANYON, CA ..................................................................................................................................... -

Uniquely Oakland San Francisco Business Times

SPECIAL ADVERTISING SUPPLEMENT SEPTEMBER 6, 2019 Uniquely OaklandOpportunities shine in California’s most inclusive and innovative city 2 ADVERTISING SUPPLEMENT UNIQUELY OAKLAND SAN FRANCISCO BUSINESS TIMES Welcome to Mandela Station MANDELA STATION @WEST OAKLAND BART A Culture-Rich Transit Oriented Development 7TH ST T2 T1 Located at the 5.5-acre West Oakland Bart Station Site T3 T4 5TH ST A Centrally Located 750 Residential Units Opportunity Zone Project (approx. 240 units below market-rate) 500,000 sq.ft. of Class A oce space Only 7 minutes from Downtown San Francisco (via BART) 75,000 sq.ft. of quality retail Over 400 parking stalls Only 4 minutes to Downtown PROJ. # 168-153 WO BART Oakland (via BART) DATE: April 30, 2019 SHEET: A Regional Community...Connected JRDV ARCHITECTS INC. COPYRIGHT C 2015. ALL RIGHTS RESERVED. We’re on the Edge - and taking transit oriented living to the next level. www.westoaklandstation.com #WOSTATION [email protected] 中国港湾工程有限 公司 Strategic Urban Development Alliance, LLC China Harbour Engineering Company Ltd. suda SEPTEMBER 6, 2019 UNIQUELY OAKLAND ADVERTISING SUPPLEMENT 3 ‹ A LETTER FROM THE MAYOR OF OAKLAND › Uniquely Oakland Everyone belongs in the world’s best city for smart businesses, large or small elcome to Oakland, Calif., the best place ment dollars are pouring in, driving construction on the planet to pursue prosperity. on 240,000 square feet of new retail space and W If that seems like exaggeration, 945,000 square feet of new office space with consider this: Oakland is ideally located at the openings slated for 2019, 2020 and 2021. -

Civic Sideshows: Communities and Publics in East Oakland by Cristina Cielo

ISSC WORKING PAPER SERIES 2004-2005.01 Civic Sideshows: Communities and Publics in East Oakland by Cristina Cielo Sociology University of California, Berkeley November 16, 2005 Cristina Cielo Department of Sociology University of California, Berkeley [email protected] How do urban spatial practices contribute to the formation of collective identities and action and to the hierarchical structures of a city’s varied communities? This paper examines this question by presenting a comparative case study of two East Oakland public spaces – the streets and parks of a residential neighborhood and the hybrid public spaces of the Eastmont Town Center. A comparative analysis of the implicit property relations and “publics” produced at each site shows that, despite their differences, these spaces and their attendant collectivities share the same fundamental logic and limits. i 1 Introduction East Oakland’s city spaces do not bustle. In part, the silence of Oakland’s streets is rooted in its 1920s physical design in the idyllic suburban image of the ‘industrial garden.’ But we must follow its history into the present – through industrial and then commercial disinvestment in the area, changing demographics, rising unemployment and crime, and the forging of its contemporary identity – to understand what does go on in the area and why it looks so different from other parts of Oakland. In this paper, I examine two very different public spaces in East Oakland, the streets and parks of a residential neighborhood and the hybrid public spaces of the Eastmont Town Center. In these places, as elsewhere, both the state and the market’s inability to address local concerns has led residents to seek alternative means to meet their needs. -

Pari Passu Loans in Cmbs 2.0 Last Updated: January 5, 2018

PARI PASSU LOANS IN CMBS 2.0 LAST UPDATED: JANUARY 5, 2018 % of % of Has Issuance Issuance Cut-Off Pari Master Special Master Special B DBRS Property State or Origination Trust Whole-Loan Balance at Passu Pari Passu Servicer Servicer Servicer Servicer Number note Rated Property Name Deal Name Type Country City Province Year Balance Balance Issuance in Deal Piece (Loan) (Loan) (Transaction) (Transaction) 1 no 111 Livingston Street CD 2017-CD3 Office US Brooklyn NY 2017 67,000,000 120,000,000 5.05% 55.83% A-1, A-3 Midland Midland Midland Midland 1 no 111 Livingston Street CGCMT 2017-P7 Office US Brooklyn NY 2017 29,000,000 120,000,000 2.83% 24.17% A-2 Midland Midland Wells Fargo Rialto 1 yes 111 Livingston Street CD 2017-CD4 Office US Brooklyn NY 2017 24,000,000 120,000,000 2.67% 20.00% A-4 Midland Midland Midland Rialto 2 yes 1155 Northern Boulevard PFP 2017-4 Office US Manhasset NY 2017 9,523,109 11,630,063 1.46% 81.88% N/A Wells Fargo Wells Fargo Wells Fargo Wells Fargo 1166 Avenue of the 3 yes yes BBCMS 2017-C1 Office US New York NY 2017 56,250,000 110,000,000 6.57% 66.18% A-1 Wells Fargo Rialto Wells Fargo Rialto Americas 1166 Avenue of the 3 yes yes WFCM 2017-RB1 Office US New York NY 2017 28,750,000 110,000,000 4.51% 33.82% A-2 Wells Fargo Rialto Wells Fargo C-III Americas 4 yes 123 William Street WFCM 2017-RB1 Office US New York NY 2017 62,500,000 140,000,000 9.80% 44.64% A-1 Wells Fargo C-III Wells Fargo C-III 4 yes 123 William Street MSC 2017-H1 Office US New York NY 2017 50,000,000 140,000,000 4.59% 35.71% A-2 Wells Fargo C-III -

2 Revisions to the Draft EIR

2 Revisions to the Draft EIR This section includes the revisions to the Draft EIR. These revisions have been made in response to comments or based on review by the EIR preparers. The Final EIR includes responses to all comments received during the public comment period as well as late comments received through June 13. MTC and ABAG have refined the Draft Plan Bay Area (“Draft Plan”) based upon agency and public comments. The changes to the Draft Plan as described below do not alter the conclusions presented in the Draft EIR regarding significant environmental impacts or mitigation measures and therefore do not trigger recirculation. However, this section includes revisions to the Draft EIR so that it continues to correspond to the Draft Plan. 2.1 Description of Modifications Minor modifications have been made to the housing and employment distributions in the Draft Plan. These modifications take into account the considerable local input received on the land use plan to date. Specifically, the modifications reflect: (1) corrections to datasets that were used to develop the jobs and housing distributions in the Draft Plan; (2) adjustments to ensure consistency with Regional Housing Needs Allocation (RHNA); and (3) adjustments to local jurisdictions growth based on corrections to how the distribution methodology was applied. These modifications are described in more detail below. These minor modifications do not affect the conclusions of significance in the Draft EIR, nor do they impact the regional modeling results in a significant way. CORRECTIONS TO DATA SETS Several minor errors in the data used to develop the employment and housing distributions were identified both by ABAG staff and local jurisdictions. -

Oakland Oversight Board

OAKLAND OVERSIGHT BOARD R ESOLUTION N O . 2014- A RESOLUTION APPROVING A REVISED LONG-RANGE PROPERTY MANAGEMENT PLAN ADDRESSING THE DISPOSITION AND USE OF FORMER REDEVELOPMENT AGENCY PROPERTIES, AND AUTHORIZING THE DISPOSITION OF PROPERTY PURSUANT TO THE PLAN WHEREAS, Health and Safety Code Section 34191.5(b) requires a successor agency to prepare and submit for approval to the oversight board and the California Department of Finance a long-range property management plan within six months of receiving a finding of completion; and WHEREAS, Health and Safety Code Section 34191.5(c) requires that the long- range property management plan include certain information and address the disposition and use of real property that was owned by the former redevelopment agency; and WHEREAS, the Oakland Redevelopment Successor Agency (“ORSA”) received its Finding of Completion under Health and Safety Code Section 34179.7 from the California Department of Finance on May 29, 2013; and WHEREAS, ORSA prepared and approved the original Long-Range Property Management Plan that addressed the disposition and use of real property formerly owned by the Redevelopment Agency of the City of Oakland on July 2, 2013, ORSA Resolution No. 2013-022; and WHEREAS, the original Oakland Oversight Board approved this Long-Range Property Management Plan on July 15, 2013, Oversight Board Resolution No. 2013-14; and WHEREAS, the Long-Range Property Management Plan was rejected by the California Department of Finance on February 28, 2014; and WHEREAS, ORSA has prepared and approved -

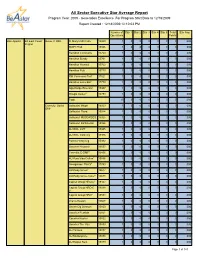

All Sector Executive Star Average Report Program Year: 2009 - Generation Excellence for Program Start Date to 12/18/2009 Report Created : 12/18/2009 12:10:03 PM

All Sector Executive Star Average Report Program Year: 2009 - Generation Excellence For Program Start Date to 12/18/2009 Report Created : 12/18/2009 12:10:03 PM Number of Star 1 Star 2 Star 3 Star 4 Star 5 Total Star Avg Operations Points Bon Appetit BA East Coast Bulau, P DMF St Mary's MD Cafe 15800 1 0 0 0 0 0 0 .000 Region MWPI Pratt 15806 1 0 0 0 0 0 0 .000 Hamilton Commons 15760 1 0 0 0 0 0 0 .000 Hamilton Bundy 15761 1 0 0 0 0 0 0 .000 Hamilton Howard 15762 1 0 0 0 0 0 0 .000 Hamilton Pub 15770 1 0 0 0 0 0 0 .000 RW Commons-Res* 17521 1 0 0 0 0 0 0 .000 Hamilton Juice Bar* 17779 1 0 0 0 0 0 0 .000 Oglethorpe Emerson 15947 1 0 0 0 0 0 0 .000 Google Austell* 18793 1 0 0 0 0 0 0 .000 Total 10 0 0 0 0 0 0 .000 Connolly, David Gallaudet Mktplc 15923 1 0 0 0 0 0 0 .000 DMF Gallaudet Plaza 15924 1 0 0 0 0 0 0 .000 Gallaudet MSSD/KDES 15925 1 0 0 0 0 0 0 .000 Gallaudet Rathskellar 15926 1 0 0 0 0 0 0 .000 AU WCL CafT 15945 1 0 0 0 0 0 0 .000 AU WCL Catering 15946 1 0 0 0 0 0 0 .000 Patrick Henry Clg 15982 1 0 0 0 0 0 0 .000 Goucher Heubeck 16557 1 0 0 0 0 0 0 .000 Connolly, D DMF* 16456 1 0 0 0 0 0 0 .000 AU Pura Vida Coffee* 16886 1 0 0 0 0 0 0 .000 Georgetown Peet's* 17740 1 0 0 0 0 0 0 .000 UoShady Grove* 18617 1 0 0 0 0 0 0 .000 UoShady Grove Cater* 18678 1 0 0 0 0 0 0 .000 Capital Group HRO-C* 19337 1 0 0 0 0 0 0 .000 Capital Group HRO-C 19338 1 0 0 0 0 0 0 .000 2* Capital Group HRO* 19558 1 0 0 0 0 0 0 .000 Oracle Reston 15608 1 0 0 0 0 0 0 .000 Gouch Clg Stimson 15850 1 0 0 0 0 0 0 .000 Goucher Pearlstn 15851 1 0 0 0 0 0 0 .000 Goucher -

Appendix B: Supplemental Technical Information

Appendix B: Supplemental Technical Information Draft Plan Bay Area Land Use Revision Requests and Final Modifications by Jurisdiction Table 1: Employment and Housing Modifications by Jurisdiction Housing Unit Modification Job Modification County City PDA or sub-area 2010 2040 2010 2040 Shifted to/from Rationale to Clayton and Los Altos Adjustment to ensure that Clayton and Los Altos Hills RHNA growth from Alameda Oakland Downtown -72 Hills 2014-2022 does not exceed total 30- year growth swap jobs to Dublin from Response to comment from City of Dublin. Expect greater job growth in City of Hayward and certain sectors than jobs distribution model predicts (model based largely on Livermore Lab in existing concentrations of jobs which are currently small in this city in Alameda Dublin 2300 unincorporated area comparison to other job centers swap jobs to Livermore Response to comment from City of Dublin. Expect greater job growth in from City of Hayward and certain sectors than the jobs distribution model predicts (model based largely Livermore Lab in on existing concentrations of jobs which are currently small in this city in Alameda Livermore 1500 unincorporated area comparison to other job centers) Correction to NETS. Response to comment form City of Hayward that employment growth is too high. Already fairly densely-built and areas of Alameda Hayward Downtown -961 -1000 growth are limited. swap jobs to Dublin and Livermore from Lab in Response to comment from County of Alameda. Expect lower job growth in Alameda Alameda County Unicorporated -2800 unincorporated area certain sectors than the jobs distribution model predicts. Response to comment from City of Brentwood. -

2012 Annual Report

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE 2012 Annual Report Bill Lockyer Treasurer State of California CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE 2012 Annual Report Report on the Allocation of Federal and State Low Income Housing Tax Credits in California April 2013 The State Treasurer’s Office and the California Tax Credit Allocation Committee comply with the Americans With Disabilities Act (ADA). If you need additional information or assistance, please contact the California Tax Credit Allocation Committee at (916) 654-6340 or TDD (916) 654-9922. CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE Voting Committee Members: Bill Lockyer, Chair State Treasurer Ana J. Matosantos, Director of Finance John Chiang, State Controller Advisory Committee Members: Claudia Cappio, Executive Director California Housing Finance Agency Laura Whittall-Scherfee, Deputy Director of the Division of Financial Assistance Department of Housing and Community Development Lois Starr County Representative Vacant City Representative Committee Staff: William J. Pavão, Executive Director Lisa Vergolini, Deputy Executive Director Rose Guerrero, Chief Compliance Section Ammer Singh, Compliance Program Manager Shannon Nardinelli, Compliance Program Manager Elizabeth Gutierrez, Compliance Program Manager Anthony Zeto, Development Program Manager Gina Ferguson, Development Program Manager (Specialist) Tiffani Armstrong Mayra Lozano Angel Barragan Kelly Luu Stephen Bellotti Tina Miller Phyllis Blanton David Navarrette Bruce Cager Connie Osorio Richard Chinakwe Georgene Palmerin Emilio Contreras Marisol Parks Generoso Deguzman Adam Sartain Carol Douglas Benjamin Schwartz Frank Harper Kole Tefft Diana Hester Toby Threlfall Nicola Hil Nicole Valenzuela Noemy Iniguez Jack Waegell Elaine Johnson Biu Wong Quang Le Carl Yeager TABLE OF CONTENTS EXECUTIVE SUMMARY – 2012 Program Highlights 1 I. RESULTS OF THE 2012 PROGRAM 5 II. -

Senior Resource Guide

SENIOR RESOURCE GUIDE Non-Profit and Public Agencies Serving NORTH ALAMEDA COUNTY Alameda ● Albany ● Berkeley ● Emeryville ● Oakland ● Piedmont Alameda County Area Agency on Aging 6955 Foothill Blvd, 3rd Floor, Oakland, CA 94605; 1-800-510-2020 / 510-577-3530; http://alamedasocialservices.org ADULT DAY CARE/RESPITE (useful website: www.daybreakcenters.org) Alzheimer's Services of the East Bay, Berkeley; http://aseb.org ................................................................................................................................................. 510-644-8292 Bay Area Community Services – BACS, Adult Day Care, Oakland; www.bayareacs.org .................................................................................................... 510-601-1074 Berkeley Adult Day Health Care; www.wohc.org ............................................................................................................................................................................. 510-601-0167 Centers for Elders Independence (PACE - Program of All-inclusive Care for the Elderly); www.cei.elders.org ...................................................................... 510-433-1150 DayBreak Adult Care Centers, formerly Adult Day Services Network (personalized referrals & community education); http://daybreakcenters.org ............................................................................................................................................................................................................................................................................