Vietnamese State-Owned Enterprises Under International Economic Integration

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

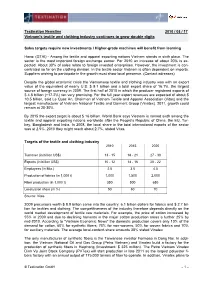

Vietnam's Textile and Clothing Industry Continues to Grow Double Digits

Textination Newsline 2010 / 08 / 17 Vietnam's textile and clothing industry continues to grow double digits Sales targets require new investments / Higher-grade machines will benefit from learning Hanoi (GTAI) - Among the textile and apparel exporting nations Vietnam stands in sixth place. The sector is the most important foreign exchange earner. For 2010 an increase of about 20% is ex- pected. About 30% of sales relate to foreign invested enterprises. However, the investment is con- centrated so far on the clothing division. In the textile sector Vietnam is often dependent on imports. Suppliers wishing to participate in the growth must show local presence. (Contact adresses) Despite the global economic crisis the Vietnamese textile and clothing industry was with an export value of the equivalent of nearly U.S. $ 9.1 billion and a total export share of 16.1%, the largest source of foreign currency in 2009. The first half of 2010 in which the producer registered exports of $ 4.8 billion (+17.2%) ran very promising. For the full year export revenues are expected of about $ 10.5 billion, said Le Quoc An, Chairman of Vietnam Textile and Apparel Association (Vitas) and the largest manufacturer of Vietnam National Textile and Garment Group (Vinatex). 2011, growth could remain at 20-30%. By 2015 the export target is about $ 16 billion. World Bank says Vietnam is ranked sixth among the textile and apparel exporting nations worldwide after the People's Republic of China, the EU, Tur- key, Bangladesh and India. In 2008, the local share in the total international exports of the sector was at 2.5%. -

Revolution, Reform and Regionalism in Southeast Asia

Revolution, Reform and Regionalism in Southeast Asia Geographically, Cambodia, Laos and Vietnam are situated in the fastest growing region in the world, positioned alongside the dynamic economies of neighboring China and Thailand. Revolution, Reform and Regionalism in Southeast Asia compares the postwar political economies of these three countries in the context of their individual and collective impact on recent efforts at regional integration. Based on research carried out over three decades, Ronald Bruce St John highlights the different paths to reform taken by these countries and the effect this has had on regional plans for economic development. Through its comparative analysis of the reforms implemented by Cam- bodia, Laos and Vietnam over the last 30 years, the book draws attention to parallel themes of continuity and change. St John discusses how these countries have demonstrated related characteristics whilst at the same time making different modifications in order to exploit the strengths of their individual cultures. The book contributes to the contemporary debate over the role of democratic reform in promoting economic devel- opment and provides academics with a unique insight into the political economies of three countries at the heart of Southeast Asia. Ronald Bruce St John earned a Ph.D. in International Relations at the University of Denver before serving as a military intelligence officer in Vietnam. He is now an independent scholar and has published more than 300 books, articles and reviews with a focus on Southeast Asia, -

Energy, Mining and Infrastructure Vietnam

Energy, Mining and Infrastructure Vietnam Client Alert Draft Model PSC and Partnership with PetroVietnam November 2012 This Alert notes two new developments. The first relates to a new draft on Model Petroleum Product Sharing Contracts and the second relates to a recent call from PetroVietnam for investment partnership in a number of projects. Draft Decree Amending Model PSC The Ministry of Industry and Trade in Vietnam (“MOIT”) recently posted on their website1 a draft decree replacing Decree No. 139/2005/ND-CP on the Should you wish to obtain further Issuance of a Model Contract for Petroleum Product Sharing Contracts information or want to discuss any (“PSCs”). A new model PSC will be issued once this draft decree is issues raised in this alert with us, please contact: officially enacted by the Government. Currently, the MOIT is in the process of collecting comments from the public on the draft decree before they Frederick Burke finalize it and submit to the Government for final approval. +84 8 3520 2628 [email protected] The new model PSC contains various amendments to the current model PSC issued under Decree No. 139/2005/ND-CP. A number of amendments Simon Taylor are made to update the model PSC with new regulations in petroleum +84 4 3936 9404 [email protected] industry, including the changes in tax and fee regime and the transfer of the role of the petroleum management body to the MOIT. A number of Dang Chi Lieu other changes have been made to the clauses on, among others, term +84 4 3 936 9341 [email protected] extension, work programs and budgets, the participation of PetroVietnam, assignment, abandonment, termination, stabilization, operator, confidentiality, and bonuses and payments to PetroVietnam. -

The Vietnam War 47

The Vietnam War 47 Chapter Three The Vietnam War POSTWAR DEMOBILIZATION By the end of 1945, the Army and Navy had demobilized about half their strength, and most of the rest was demobilized in 1946. Millions of men went home, got jobs, took advantage of the new Servicemen’s Readjustment Act (commonly known as the “GI Bill,” passed in 1944), got married, and started the “baby boom.” Just as in the period following victory in World War I, few Americans paid much attention to national defense. The newly created Department of Defense (formed in the 1947 merger of the War Department and the Navy Department) faced several concurrent tasks: demobilizing the troops; selling off surplus equipment, land, and buildings; and calculating what defense forces the United States actually needed. The govern- ment adopted a postwar defense policy of containing communism, centered on supporting the governments of foreign countries struggling against internal communists. In its early stages, containment called for foreign aid (both military and economic) and limited numbers of military advisers. The Army drew down to only a few divisions, mostly serving occupation duty in Germany and Japan, and most at two-thirds strength. So few men were volunteering for the military that, in 1948, Congress restored a peacetime draft. The world began looking like a more dangerous place when the Soviets cut off land access to Berlin and backed a coup in Czechoslovakia that replaced a coalition government with a communist one. Such events, in addition to the campaign led by Senator Joe Mc- Carthy to expose any possible American communists, stoked fears of a world- wide communist movement. -

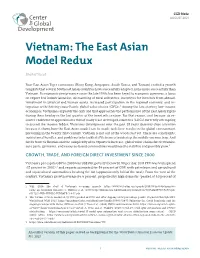

Vietnam: the East Asian Model Redux

CGD Note AUGUST 2021 Vietnam: The East Asian Model Redux Shahid Yusuf Four East Asian Tiger economies (Hong Kong, Singapore, South Korea, and Taiwan) crafted a growth template that several Southeast Asian countries have successfully adapted, none more successfully than Vietnam. Its economic performance since the late 1990s has been keyed to economic openness, a focus on export-led industrialization, dismantling of rural collectives, incentives for investors from abroad, investment in physical and human assets, increased participation in the regional economy, and in- tegration with thriving cross-Pacific global value chains (GVCs).1 Among the late starting low-income economies, Vietnam is arguably the only one that approaches the performance of the East Asian Tigers during their heyday in the last quarter of the twentieth century. For that reason, and because its re- source endowment approximates that of many least-developed countries (LDCs) currently attempting to ascend the income ladder, Vietnam’s development over the past 25 years deserves close attention because it shows how the East Asian model can be made to deliver results in the global environment prevailing in the twenty-first century. Vietnam is not out of the woods just yet. There are constraints, institutional hurdles, and problems to be tackled if Vietnam is to sidestep the middle-income trap. And for its trade to flourish and the complexity of its exports to increase, global value chains for electronics, auto parts, garments, and resource-based commodities would need to stabilize and possibly grow.2 GROWTH, TRADE, AND FOREIGN DIRECT INVESTMENT SINCE 2000 Vietnam’s per capita GDP in 2000 was US$390; poverty (below $1.90 per day, 2011 PPP) was widespread (37 percent in 2002);3 and exports accounted for 54 percent of GDP, with petroleum and agricultural and aquacultural commodities heading the list (approximately half of the total). -

J Emmer Thesis

COMPARISON OF NARRATIVES: AMERICAN VETERANS OF THE VIETNAM WAR AND OPERATION IRAQI FREEDOM By Janal J. Emmer At the heart of every person is a story, an account of a significant life event that is often hidden within the memory. When memories are written down, the past becomes a story, a style, a piece of literature. In this form, the personal narrative has two functions: a memory is information storage, communicating events across time and space; and second, memory recorded in a visual format allows people to examine it in a different way (Goff 59). The personal narrative itself floats somewhere between nonfiction and fiction, and finds a home amid the short story, novel, and autobiography. However, it resists these genres because memoirs generally lack a plot, climax, and ending. According to Don Ringnalda, in Fighting and Writing the Vietnam War, it is sometimes difficult to distinguish between a memoir and a first-person novel because the lines separating fact, fiction, memory, and autobiography become blurred (Ringnalda 74). The personal narrative also negotiates with the historical document. Memoirs have sometimes been considered neighbors of history, and historians and memoirists have also been grouped together from a literary perspective. The testimony provided in personal narratives enters the historical domain when it provides information about specific historical events, but poses problems for historians because the elements cannot meet the test of historical accuracy (Hynes 15; Goff 186). According to Samuel Hynes in The Soldiers’ Tale: Bearing Witness to Modern War, “Personal narratives are not history; they speak each with its own voice, as history does not, and they find their own shape, which are not the shapes of history. -

Wool Sourcing Guide Vietnam Vietnam

WOOL SOURCING GUIDE VIETNAM VIETNAM The Vietnam textile industry is the third largest apparel exporter in the world accounting for 6.3 per cent of world apparel exports in 2019. Once mainly a cut and sew supplier, Vietnam now boasts a robust wool supply chain including spinning, weaving, knitting and whole garment manufacturing. HANOI This vertical integration means designers, brands and HAI PHONG buyers can source all their garment requirements from the one country, cutting out logistical times and dealing with many suppliers. CAPITAL CITY: Hanoi AREA: 329,560 Sqkm POPULATION: 96.46 million (2019) DA NANG LANGUAGE: Vietnamese (official), Chinese, English, and French HOI AN RELIGION: Buddhism, Taoism, and Catholic CLIMATE: North Vietnam has a Southern Mediterranean QUY NHON climate and South Vietnam has a tropical monsoon climate type. MAJOR PORTS: Cam Pha, Da Nang, Haiphong, Ho Chi Minh, NHA TRANG Phu My, Quy Nhon DA LAT ECONOMY: Since early 2000, Vietnam has been progressively moving away from a centrally planned economy to a socialist- HO CHI MINH CITY oriented market economy. CURRENCY: The Vietnamese Dong (JUN 2015: 1USD = 21,673VND) THE WOOLMARK COMPANY AND VIETNAM The Woolmark Company (TWC) first identified Vietnam as an emerging manufacturing hub for wool textiles in 2012 when the Vietnam textile industry begun to focus on moving toward high quality products and production. Since then, we have been working closely with partners throughout the supply chain and currently collaborate with more than 90 partners including flatbed knitters, circular knitters and garment making companies. We have transferred technical knowhow about the manufacturing of wool products, disseminated information about sources of raw materials, chemicals and machines, and organised international trade missions to connect our project partners with buyers. -

Minnesota Remembers Vietnam

MINNESOTA REMEMBERS VIETNAM A COLLABORATION OF THE KSMQ-TV LAKELAND PBS PIONEER PUBLIC TV PRAIRIE PUBLIC TWIN CITIES PBS WDSE-WRPT To our COMMUNITIES Our year-long, statewide initiative called Minnesota Remembers Vietnam was conceived well over two years ago when we learned that filmmakers Ken Burns and Lynn Novick were going to present to America their comprehensive and definitive work on Vietnam. We took pause at Twin Cities PBS (TPT) and asked: “What could we do to bring this story home? What might we do to honor and give voice to those in Minnesota whose lives were touched by this confusing, divisive, and tumultuous period in American history? And what might we do to create understanding and healing?” We set our sights very high, and the collective $2 million raised in public support from the State of Minnesota’s Legacy Fund, generous foundations and organizations, and our community, allowed us to dream big and create what has been the largest and one of the most important projects in TPT’s 60-year history. In partnership with the five other PBS stations in the state, we explored the war from all sides. It has been a deeply moving experience for all of us at TPT and the stations of the MPTA, and we feel much richer for having been a part of this. I can tell you very sincerely that in my four decades of working with PBS, I've never been involved in a project that was so universally embraced. The unifying message that I heard time and time again from those who supported the war, those who demonstrated against it, and those who only learned about it through the history books was that the time was now to seize the moment to honor those who served their country during this tumultuous and confusing time… people who were shunned and endured hardships upon returning home, and who, until very recently, did not feel welcome to tell their stories, both the joyful memories of friendships and camaraderie and the haunting memories of battle. -

1. Oil and Gas Exploration & Production

1. Oil and gas exploration & production This is the core business of PVN, the current metres per year. By 2012, we are planning to achieve reserves are approximated of 1.4 billion cubic metres 20 million tons of oil and 15 billion cubic metres of of oil equivalent. In which, oil reserve is about 700 gas annually. million cubic metres and gas reserve is about 700 In this area, we are calling for foreign investment in million cubic metres of oil equivalent. PVN has both of our domestic blocks as well as oversea explored more than 300 million cubic metres of oil projects including: Blocks in Song Hong Basin, Phu and about 94 billion cubic metres of gas. Khanh Basin, Nam Con Son Basin, Malay Tho Chu, Until 2020, we are planning to increase oil and gas Phu Quoc Basin, Mekong Delta and overseas blocks reserves to 40-50 million cubic metres of oil in Malaysia, Uzbekistan, Laos, and Cambodia. equivalent per year; in which the domestic reserves The opportunities are described in detail on the increase to 30-35 million cubic metres per year and following pages. oversea reserves increase to 10-15 million cubic Overseas Oil and Gas Exploration and Production Projects RUSSIAN FEDERATION Rusvietpetro: A Joint Venture with Zarubezhneft Gazpromviet: A Joint Venture with Gazprom UZBEKISTAN ALGERIA Petroleum Contracts, Blocks Kossor, Molabaur Petroleum Contract, Study Agreement in Bukharakhiva Block 433a & 416b MONGOLIA Petroleum Contract, Block Tamtsaq CUBA Petroleum Contract, Blocks 31, 32, 42, 43 1. Oil and gas exploration & production e) LAO PDR Petroleum Contract, Block Champasak CAMBODIA 2. -

Textile & Apparel Industry Report

TEXTILE & APPAREL INDUSTRY REPORT OPPORTUNITIES FOR BREAKTHROUGH “...With internal advantages and expectations from Free Trade Agreements, Vietnam textile and apparel industry is now having opportunities for overall changes of deep development and expansion ” Bui Van Tot Senior Analyst E: [email protected] P: (08) -6290 8686 - Ext: 7593 04/2014 APPAREL INDUSTRY CONTENT Highlights 1 I. World textile and apparel industry 2 WORLD 1. Overview of the global textile and apparel industry 2 2. Global textile and apparel value chain 4 3. Main modes of production 8 3. Apparel machinery industry 9 II. Vietnam textile and apparel industry 11 1. Overview of Vietnam's textile and apparel industry 11 2. Export and import 13 VIETNAM 3. Value Chain of Vietnam's textile and apparel industry 18 3. Michael Porter Model Analysis 20 4. SWOT Analysis 22 5. Free Trade Agreements 23 7. Legality, related policies 25 III. Textile and apparel businesses 27 BUSINESSES 1. Business performance 27 2. Financial situation 31 3. Recommendations for listed companies 35 4. Typical unlisted companies 38 Appendix 40 Abbreviations Thanh Cong Textile Garment - Investment - Trading Joint TCM Stock Company GMC Saigon Garment Manufacturing Trading JSC EVE Everpia Vietnam JSC Binh Thanh Import - Export - Production and Trade Joint Stock GIL Company TNG TNG Investment and Trading JSC KMR Mirae Joint Stock Company NPS Phu Thinh - Nha Be Textile Joint Stock Company VITAS Vietnam Textile and Apparel Association VCOSA Viet Nam Cotton & Spinning Association MARD Ministry of Agriculture & Rural Development FDI Foreign Direct Investment TPP Trans-Pacific Strategic Economic Partnership Agreement FTA Free Trade Agreement MUTRAP European Trade Policy and Investment Support Project APPAREL INDUSTRY HIGHLIGHTS The current global apparel market is estimated at With an average growth rate of 14.5% per year for the US$1,100bn with trade value of US$700bn. -

Found, Featured, Then Forgotten: U.S. Network TV News and the Vietnam Veterans Against the War © 2011 by Mark D

Found, Featured, then Forgotten Image created by Jack Miller. Courtesy of Vietnam Veterans Against the War. Found, Featured, then Forgotten U.S. Network TV News and the Vietnam Veterans Against the War Mark D. Harmon Newfound Press THE UNIVERSITY OF TENNESSEE LIBRARIES, KNOXVILLE Found, Featured, then Forgotten: U.S. Network TV News and the Vietnam Veterans Against the War © 2011 by Mark D. Harmon Digital version at www.newfoundpress.utk.edu/pubs/harmon Newfound Press is a digital imprint of the University of Tennessee Libraries. Its publications are available for non-commercial and educational uses, such as research, teaching and private study. The author has licensed the work under the Creative Commons Attribution-Noncommercial 3.0 United States License. To view a copy of this license, visit http://creativecommons.org/licenses/by-nc/3.0/us/. For all other uses, contact: Newfound Press University of Tennessee Libraries 1015 Volunteer Boulevard Knoxville, TN 37996-1000 www.newfoundpress.utk.edu ISBN-13: 978-0-9797292-8-7 ISBN-10: 0-9797292-8-9 Harmon, Mark D., (Mark Desmond), 1957- Found, featured, then forgotten : U.S. network tv news and the Vietnam Veterans Against the War / Mark D. Harmon. Knoxville, Tenn. : Newfound Press, University of Tennessee Libraries, c2011. 191 p. : digital, PDF file. Includes bibliographical references (p. [159]-191). 1. Vietnam Veterans Against the War—Press coverage—United States. 2. Vietnam War, 1961-1975—Protest movements—United States—Press coverage. 3. Television broadcasting of news—United States—History—20th century. I. Title. HE8700.76.V54 H37 2011 Book design by Jayne White Rogers Cover design by Meagan Louise Maxwell Contents Preface ..................................................................... -

PRIVATE SECTOR DISCUSSIONS Number 7 VIETNAM's GARMENT

PRIVATE SECTOR DISCUSSIONS Number 7 VIETNAM’S GARMENT INDUSTRY: Public Disclosure Authorized Moving Up the Value Chain Prepared by: Hassan Oteifa - Former Manager of the International Finance Corporation's Textile Department Dietmar Stiel - SECO Consulting, Germany Public Disclosure Authorized Roger Fielding - Geoffrey Willis & Associates, UK Peter Davies - Fielden-Cegos, UK Hanoi University of Technology - Vietnam (HUT) Vietnam Chamber of Commerce and Industry (VCCI) And by: Public Disclosure Authorized MPDF Staff Public Disclosure Authorized January 1999 (Revised in March 2000) i TABLE OF CONTENTS ABBREVIATIONS AND ACRONYMS.....................................................................................v PREFACE .................................................................................................................................vi INTRODUCTION ....................................................................................................................vii I. AN OVERVIEW: Past Success and Future Challenges...........................................................1 A. Introduction........................................................................................................................ 1 B. Mission Objectives and Field Work ...................................................................................... 3 C. Mission’s Findings .............................................................................................................. 3 D. Review of the Vietnamese Garment Market.........................................................................