1. Oil and Gas Exploration & Production

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

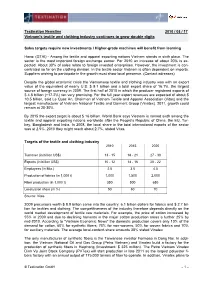

Vietnam's Textile and Clothing Industry Continues to Grow Double Digits

Textination Newsline 2010 / 08 / 17 Vietnam's textile and clothing industry continues to grow double digits Sales targets require new investments / Higher-grade machines will benefit from learning Hanoi (GTAI) - Among the textile and apparel exporting nations Vietnam stands in sixth place. The sector is the most important foreign exchange earner. For 2010 an increase of about 20% is ex- pected. About 30% of sales relate to foreign invested enterprises. However, the investment is con- centrated so far on the clothing division. In the textile sector Vietnam is often dependent on imports. Suppliers wishing to participate in the growth must show local presence. (Contact adresses) Despite the global economic crisis the Vietnamese textile and clothing industry was with an export value of the equivalent of nearly U.S. $ 9.1 billion and a total export share of 16.1%, the largest source of foreign currency in 2009. The first half of 2010 in which the producer registered exports of $ 4.8 billion (+17.2%) ran very promising. For the full year export revenues are expected of about $ 10.5 billion, said Le Quoc An, Chairman of Vietnam Textile and Apparel Association (Vitas) and the largest manufacturer of Vietnam National Textile and Garment Group (Vinatex). 2011, growth could remain at 20-30%. By 2015 the export target is about $ 16 billion. World Bank says Vietnam is ranked sixth among the textile and apparel exporting nations worldwide after the People's Republic of China, the EU, Tur- key, Bangladesh and India. In 2008, the local share in the total international exports of the sector was at 2.5%. -

2012 Confirmed Participants List Speaker Names in Bold

2012 Confirmed Participants List Speaker names in bold ALMENDRAS, Jose Rene –Department of DANG, Dinh Quy – Diplomatic Academy of Energy, Philippines Vietnam, Vietnam ANDITYA, Chrisnawan – Ministry of Energy and DAO, Minh Hien – Electricity Regulatory Mineral Resources, Indonesia Authority of Vietnam (ERAV), Vietnam ANDREOZZI, Marco – Pegaso Canton Ltd., China DAO, Trong Tu – Centre for Sustainable Water ANGELL, Ian – Talisman Energy, Malaysia Resources Development and Adaptation to AU, Tuan Minh – Asian Development Bank, Climate Change, Vietnam Vietnam DINH, Tien Hoa – Vietnam National Coal and BERKOBEN, Russell – ExxonMobil Exploration Mineral Industries Holding Corporation, Ltd. and Production, Vietnam (Vinacomin), Vietnam BICKEL, Dustin – Embassy of the United States, DO, Dinh Khang – Vietnam Academy of Science Laos and Technology (VAST); Company for BLAIR, Dennis – The National Bureau of Asian Improvement of Technology (IMTECH), Vietnam Research Board of Directors, United States DO, Tuan Manh – Sectoral Economic BLAND, Ben – Financial Times, Indonesia Department, Government Office of Vietnam, BOUNSOU, Xayphone – Ministry of Energy and Vietnam Mines, Laos DUONG, Ngoc Doan – Institute of Energy, BREBER, Pierre – Chevron, United States Vietnam BUENO, Edith – National Electrification EBINGER, Charles – Brookings Institution, Administration, Philippines United States BURKE, Fred – Baker & McKenzie, Vietnam FIELDS, Adam – Embassy of the United States, CHATSIS, Deborah – Embassy of Canada, Vietnam Vietnam FOOTE, -

Algeria Upstream OG Report.Pub

ALGERIA UPSTREAM OIL & GAS REPORT Completed by: M. Smith, Sr. Commercial Officer, K. Achab, Sr. Commercial Specialist, and B. Olinger, Research Assistant Introduction Regulatory Environment Current Market Trends Technical Barriers to Trade and More Competitive Landscape Upcoming Events Best Prospects for U.S. Exporters Industry Resources Introduction Oil and gas have long been the backbone of the Algerian economy thanks to its vast oil and gas reserves, favorable geology, and new opportunities for both conventional and unconventional discovery/production. Unfortunately, the collapse in oil prices beginning in 2014 and the transition to spot market pricing for natural gas over the last three years revealed the weaknesses of this economic model. Because Algeria has not meaningfully diversified its economy since 2014, oil and gas production is even more essential than ever before to the government’s revenue base and political stability. Today’s conjoined global health and economic crises, coupled with persistent declining production levels, have therefore placed Algeria’s oil and gas industry, and the country, at a critical juncture where it requires ample foreign investment and effective technology transfer. One path to the future includes undertaking new oil and gas projects in partnership with international companies (large and small) to revitalize production. The other path, marked by inertia and institutional resistance to change, leads to oil and gas production levels in ten years that will be half of today's production levels. After two decades of autocracy, Algeria’s recent passage of a New Hydrocarbons Law seems to indicate that the country may choose the path of partnership by profoundly changing its tax and investment laws in the hydrocarbons sector to re-attract international oil companies. -

Morphology of Water-Based Housing in Mekong Delta, Vietnam

MATEC Web of Conferences 193, 04005 (2018) https://doi.org/10.1051/matecconf/201819304005 ESCI 2018 Morphology of water-based housing in Mekong delta, Vietnam Thi Hong Hanh Vu1,* and Viet Duong1 1University of Architecture Ho Chi Minh City, 196 Pasteur, District 1, Ho Chi Minh City, Vietnam Abstract. A long time ago, houses along and on the water have been distinctive elements of the water-based Mekong Delta. Over a long history of development, these morphological settlements have been deteriorated due to environmental, economic, and cultural changes from water to mainland, resulted in the reductions of water-based communities and architectural deterioration. This research is aimed to analyze the distinguishing values of those housing types/communities in 5 chosen popular water-based settlements in Mekong Delta region to give positive recommendations for further changes. 1 Introduction Mekong Delta is located in the South of Vietnam, downstream of the Mekong River. This is a nutrious plain with dense water channels. People here have chosen their settlements to be near, in order of priority: markets – rivers – friends –roads/streets/routes - and farmlands (Nhất cận thị, nhị cận giang, tam cận lân, tứ cận lộ, ngũ cận điền). When the population increased, they started to move inward the land; as a result, their living culture have gradually changed, so have their houses [1-3]. Over long history of exploitation, the local inhabitants and migrants from other parts of Vietnam and nearby countries have turned this Mekong delta to a rich and distinctive society with diverse ethnic communities, cultures and beliefs, living harmoniously together. -

Form 20-F 2011 UNITED STATES SECURITIES and EXCHANGE COMMISSION WASHINGTON, D.C

Form 20-F 2011 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 20-F/A (Amendment No. 1) (Mark One) ‘ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR Í ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2011 OR ‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to OR ‘ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report Commission file number: 1-10888 TOTAL S.A. (Exact Name of Registrant as Specified in Its Charter) Republic of France (Jurisdiction of Incorporation or Organization) 2, place Jean Millier La Défense 6 92400 Courbevoie France (Address of Principal Executive Offices) Patrick de La Chevardière Chief Financial Officer TOTAL S.A. 2, place Jean Millier La Défense 6 92400 Courbevoie France Tel: +33 (0)1 47 44 45 46 Fax: +33 (0)1 47 44 49 44 (Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange on which registered Shares New York Stock Exchange* American Depositary Shares New York Stock Exchange * Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. -

Optimizing FCC Operations in a High Rare Earth

August 03, 2011 VOL: 2 ISS: 15 Optimizing FCC Operations in a High Rare Earth Cost Market: Part I Highlights of Recent Grace FCC Webinar Focusing on Unit Operation and Profitability when Re- formulating FCC Catalyst to Lower Rare Earth Higher feed volumes are processed metric ton on the Asian Metal Index, a acid site density and prevents dealumi- through FCC units than ever before, at 2700% increase in price over the course nation. A catalyst designed with a high the same time that more challenging of a year! This is why the industry has RE exchange for high gasoline selectiv- feedstocks have entered the market. demonstrated such a strong response to ity will have more Cont. page 2 The industry has responded with ef- finding solutions to RE inflation. fective catalyst chemistry that has in- Rare earth supplies are expected to In This Issue... cluded adding higher quantities of rare remain in critically short supply until at earth (RE) to the zeolite. However, least 2014, when mines in other parts of FEATURE with the unprecedented inflation in RE the world are fully developed. Lantha- costs, the onus is now on reformulat- Optimizing FCC Operations in a High num (atomic number: 57) is the lightest Rare Earth Cost Market: Part I ing FCC catalysts to lower RE, while of the rare earths as shown on a typical maintaining or exceeding the high lev- Periodic Table of the Elements. Lantha- els of performance achieved by the latest PROCESS OPERATIONS num has been the dominant RE metal ISOCRACKING Technology Update catalyst systems. -

Vietnam Maximizing Finance for Development in the Energy Sector

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized VIETNAM MAXIMIZING FINANCE FOR DEVELOPMENT IN THE ENERGY SECTOR DECEMBER 2018 Public Disclosure Authorized ACKNOWLEDGMENTS This report was prepared by a core team led by Franz Gerner (Lead Energy Specialist, Task Team Leader) and Mark Giblett (Senior Infrastructure Finance Specialist, Co-Task Team Leader). The team included Alwaleed Alatabani (Lead Financial Sector Specialist), Oliver Behrend (Principal Investment Officer, IFC), Sebastian Eckardt (Lead Country Economist), Vivien Foster (Lead Economist), and David Santley (Senior Petroleum Specialist). Valuable inputs were provided by Pedro Antmann (Lead Energy Specialist), Ludovic Delplanque (Program Officer), Nathan Engle (Senior Climate Change Specialist), Hang Thi Thu Tran (Investment Officer, IFC), Tim Histed (Senior Business Development Officer, MIGA), Hoa Nguyen Thi Quynh (Financial Management Consultant), Towfiqua Hoque (Senior Infrastructure Finance Specialist), Hung Tan Tran (Senior Energy Specialist), Hung Tien Van (Senior Energy Specialist), Kai Kaiser (Senior Economist), Ketut Kusuma (Senior Financial Sector Specialist, IFC), Ky Hong Tran (Senior Energy Specialist), Alice Laidlaw (Principal Investment Officer, IFC), Mai Thi Phuong Tran (Senior Financial Management Specialist), Peter Meier (Energy Economist, Consultant), Aris Panou (Counsel), Alejandro Perez (Senior Investment Officer, IFC), Razvan Purcaru (Senior Infrastructure Finance Specialist), Madhu Raghunath (Program Leader), Thi Ba -

Final Report

SOCIALIST REPUBLIC OF VIETNAM DATA COLLECTION SURVEY ON COOPERATION IN OVERSEAS BUSINESS EXPANSION STRATEGY OF SMALL AND MEDIUM-SIZED ENTERPRISES IN AGRICULTURE SECTOR AND FUTURE DIRECTION OF AGRICULTURAL COOPERATION FINAL REPORT Summary March 2020 Japan International Cooperation Agency (JICA) Nippon Koei Co., Ltd. Meros Consulting Co., Ltd. VT JR 20-002 North West North East Son La province Red river Delta (Son La city) Ha Noi capital Nghe An Province (Vinh City) North Central Coast Legend: : Target Area South Central Coast Central Highlands Ho Chi Minh city Lam Dong Province (Da Lat City) Ben Tre Province (Ben Tre City) Can Tho city Mekong River Delta 0 100 200km Source:Survey team Location Map of Target Area Site Photos (1) Nghe An Province Production materials for mushroom production Fermenting process of fish source using wooden barrel (ATC Investment and Production Joint Stock Company) (Van Phan Fisheries Joint Stock Company) (2) Lam Dong Province Hydroponic plant culture of lettuce Coffee bean roaster (specially ordered) (Phong Thuy Agricultural Product Trade Manufacturing Co., Ltd.) (La Viet Co., Ltd) (3) Can Tho City Drying machine for fruits Pre-processing of durian (Mekong Fruit Co., Ltd) (Dai Thuan Thien Co., Ltd.) (4) Ben Tre Province Coconut processing factory (large scale: 5 ha) Coconut fruit processing (Luong Quoi Coconut Co., Ltd.) (Mekong Impex Fresh Fruit Co., Ltd.) (5) Son La Province Production of lingzhi mushroom using raw timber Drying machine for fruits (Manh Thang Company Ltd.) (Quyet Thanh Agriculture Cooperative) -

The Politics of Oil Nationalizations

University of California Los Angeles The Politics of Oil Nationalizations A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in Political Science by Paasha Mahdavi 2015 c Copyright by Paasha Mahdavi 2015 Abstract of the Dissertation The Politics of Oil Nationalizations by Paasha Mahdavi Doctor of Philosophy in Political Science University of California, Los Angeles, 2015 Professor Michael L. Ross, Chair This dissertation is about the institutional choices governments make to man- age their petroleum wealth. It is about the determinants of these choices, but more importantly, their consequences for effective governance and how they ex- plain variations in political outcomes in oil-producing countries. I begin by de- scribing several different institutional pathways { involving national oil companies (NOCs) and their varying characteristics { that governments can take in extract- ing petroleum and regulating its production. My goal, then, is to show how these seemingly technical institutional choices can have profound impacts on gover- nance, ranging from effects on state revenue collection to incentives for corruption to ultimately the survival of the regime itself. To this aim, I collected original longitudinal data on the formation of NOCs in 62 countries since 1900; data from U.S. Department of Justice transcripts on the prosecution of corrupt practices in the energy sectors of 80 countries in the 2006-12 period; and existing cross-national data on government revenue capture from the sale of oil and natural resources. I analyze the determinants of NOC formation in the first empirical chapter, where I use Bayesian analysis informed with interview-based data from oil consultants to test and confirm leading theories of state revenue-maximization as the primary determinant of expropriation. -

Energy, Mining and Infrastructure Vietnam

Energy, Mining and Infrastructure Vietnam Client Alert Draft Model PSC and Partnership with PetroVietnam November 2012 This Alert notes two new developments. The first relates to a new draft on Model Petroleum Product Sharing Contracts and the second relates to a recent call from PetroVietnam for investment partnership in a number of projects. Draft Decree Amending Model PSC The Ministry of Industry and Trade in Vietnam (“MOIT”) recently posted on their website1 a draft decree replacing Decree No. 139/2005/ND-CP on the Should you wish to obtain further Issuance of a Model Contract for Petroleum Product Sharing Contracts information or want to discuss any (“PSCs”). A new model PSC will be issued once this draft decree is issues raised in this alert with us, please contact: officially enacted by the Government. Currently, the MOIT is in the process of collecting comments from the public on the draft decree before they Frederick Burke finalize it and submit to the Government for final approval. +84 8 3520 2628 [email protected] The new model PSC contains various amendments to the current model PSC issued under Decree No. 139/2005/ND-CP. A number of amendments Simon Taylor are made to update the model PSC with new regulations in petroleum +84 4 3936 9404 [email protected] industry, including the changes in tax and fee regime and the transfer of the role of the petroleum management body to the MOIT. A number of Dang Chi Lieu other changes have been made to the clauses on, among others, term +84 4 3 936 9341 [email protected] extension, work programs and budgets, the participation of PetroVietnam, assignment, abandonment, termination, stabilization, operator, confidentiality, and bonuses and payments to PetroVietnam. -

Occupation and Revolution

Occupation and Revolution . HINA AND THE VIETNAMESE ~-...uGUST REVOLUTION OF 1945 I o I o 1 I so lWoroeters -------uangTri ~ N I \\ Trrr1~ Sap Peter Worthing CHINA RESEARCH MONOGRAPH 54 CHINA RESEARCH MONOGRAPH 54 F M' INSTITUTE OF EAST ASIAN STUDIES ~ '-" UNIVERSITY OF CALIFORNIA • BERKELEY C(5 CENTER FOR CHINESE STUDIES Occupation and Revolution China and the Vietnamese August Revolution of 1945 Peter Worthing A publication of the Institute of East Asian Studies, University of Califor nia, Berkeley. Although the Institute of East Asian Studies is responsible for the selection and acceptance of manuscripts in this series, responsibil ity for the opinions expressed and for the accuracy of statements rests with their authors. Correspondence and manuscripts may be sent to: Ms. Joanne Sandstrom, Managing Editor Institute of East Asian Studies University of California Berkeley, California 94720-2318 E-mail: [email protected] The China Research Monograph series is one of several publications series sponsored by the Institute of East Asian Studies in conjunction with its constituent units. The others include the Japan Research Monograph series, the Korea Research Monograph series, and the Research Papers and Policy Studies series. A list of recent publications appears at the back of the book. Library of Congress Cataloging-in-Publication Data Worthing, Peter M. Occupation and revolution : China and the Vietnamese August revolu tion of 1945 I Peter M. Worthing. p. em. -(China research monograph; 54) Includes bibliographical references and index. ISBN 978-1-55729-072-4 1. Vietnam-Politics and government-1858-1945. 2. Vietnam Politics and government-1945-1975. 3. World War, 1939-1945- Vietnam. -

Spatiotemporal Dynamics of Dengue Epidemics, Southern Vietnam Hoang Quoc Cuong, Nguyen Thanh Vu, Bernard Cazelles, Maciej F

Spatiotemporal Dynamics of Dengue Epidemics, Southern Vietnam Hoang Quoc Cuong, Nguyen Thanh Vu, Bernard Cazelles, Maciej F. Boni, Khoa T.D. Thai, Maia A. Rabaa, Luong Chan Quang, Cameron P. Simmons, Tran Ngoc Huu, and Katherine L. Anders An improved understanding of heterogeneities in den- drive annual seasonality; intrinsic factors associated with gue virus transmission might provide insights into biological human host demographics, population immunity, and the and ecologic drivers and facilitate predictions of the mag- virus, drive the multiannual dynamics (5–7). Analyses from nitude, timing, and location of future dengue epidemics. To Southeast Asia have demonstrated multiannual oscillations investigate dengue dynamics in urban Ho Chi Minh City and in dengue incidence (8–10), which have been variably as- neighboring rural provinces in Vietnam, we analyzed a 10- sociated with macroclimatic weather cycles (exemplified year monthly time series of dengue surveillance data from southern Vietnam. The per capita incidence of dengue was by the El Niño Southern Oscillation) in different settings lower in Ho Chi Minh City than in most rural provinces; an- and with changes in population demographics in Thailand nual epidemics occurred 1–3 months later in Ho Chi Minh (11). In Thailand, a spatiotemporal analysis showed that the City than elsewhere. The timing and the magnitude of an- multiannual cycle emanated from Bangkok out to more dis- nual epidemics were significantly more correlated in nearby tant provinces (9). districts than in remote districts, suggesting that local bio- Knowledge of spatial and temporal patterns in dengue logical and ecologic drivers operate at a scale of 50–100 incidence at a subnational level is relevant for 2 main rea- km.