PRIVATE SECTOR DISCUSSIONS Number 7 VIETNAM's GARMENT

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vietnam's Textile and Clothing Industry Continues to Grow Double Digits

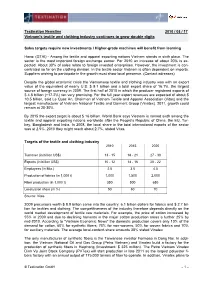

Textination Newsline 2010 / 08 / 17 Vietnam's textile and clothing industry continues to grow double digits Sales targets require new investments / Higher-grade machines will benefit from learning Hanoi (GTAI) - Among the textile and apparel exporting nations Vietnam stands in sixth place. The sector is the most important foreign exchange earner. For 2010 an increase of about 20% is ex- pected. About 30% of sales relate to foreign invested enterprises. However, the investment is con- centrated so far on the clothing division. In the textile sector Vietnam is often dependent on imports. Suppliers wishing to participate in the growth must show local presence. (Contact adresses) Despite the global economic crisis the Vietnamese textile and clothing industry was with an export value of the equivalent of nearly U.S. $ 9.1 billion and a total export share of 16.1%, the largest source of foreign currency in 2009. The first half of 2010 in which the producer registered exports of $ 4.8 billion (+17.2%) ran very promising. For the full year export revenues are expected of about $ 10.5 billion, said Le Quoc An, Chairman of Vietnam Textile and Apparel Association (Vitas) and the largest manufacturer of Vietnam National Textile and Garment Group (Vinatex). 2011, growth could remain at 20-30%. By 2015 the export target is about $ 16 billion. World Bank says Vietnam is ranked sixth among the textile and apparel exporting nations worldwide after the People's Republic of China, the EU, Tur- key, Bangladesh and India. In 2008, the local share in the total international exports of the sector was at 2.5%. -

Energy, Mining and Infrastructure Vietnam

Energy, Mining and Infrastructure Vietnam Client Alert Draft Model PSC and Partnership with PetroVietnam November 2012 This Alert notes two new developments. The first relates to a new draft on Model Petroleum Product Sharing Contracts and the second relates to a recent call from PetroVietnam for investment partnership in a number of projects. Draft Decree Amending Model PSC The Ministry of Industry and Trade in Vietnam (“MOIT”) recently posted on their website1 a draft decree replacing Decree No. 139/2005/ND-CP on the Should you wish to obtain further Issuance of a Model Contract for Petroleum Product Sharing Contracts information or want to discuss any (“PSCs”). A new model PSC will be issued once this draft decree is issues raised in this alert with us, please contact: officially enacted by the Government. Currently, the MOIT is in the process of collecting comments from the public on the draft decree before they Frederick Burke finalize it and submit to the Government for final approval. +84 8 3520 2628 [email protected] The new model PSC contains various amendments to the current model PSC issued under Decree No. 139/2005/ND-CP. A number of amendments Simon Taylor are made to update the model PSC with new regulations in petroleum +84 4 3936 9404 [email protected] industry, including the changes in tax and fee regime and the transfer of the role of the petroleum management body to the MOIT. A number of Dang Chi Lieu other changes have been made to the clauses on, among others, term +84 4 3 936 9341 [email protected] extension, work programs and budgets, the participation of PetroVietnam, assignment, abandonment, termination, stabilization, operator, confidentiality, and bonuses and payments to PetroVietnam. -

Vietnam: the East Asian Model Redux

CGD Note AUGUST 2021 Vietnam: The East Asian Model Redux Shahid Yusuf Four East Asian Tiger economies (Hong Kong, Singapore, South Korea, and Taiwan) crafted a growth template that several Southeast Asian countries have successfully adapted, none more successfully than Vietnam. Its economic performance since the late 1990s has been keyed to economic openness, a focus on export-led industrialization, dismantling of rural collectives, incentives for investors from abroad, investment in physical and human assets, increased participation in the regional economy, and in- tegration with thriving cross-Pacific global value chains (GVCs).1 Among the late starting low-income economies, Vietnam is arguably the only one that approaches the performance of the East Asian Tigers during their heyday in the last quarter of the twentieth century. For that reason, and because its re- source endowment approximates that of many least-developed countries (LDCs) currently attempting to ascend the income ladder, Vietnam’s development over the past 25 years deserves close attention because it shows how the East Asian model can be made to deliver results in the global environment prevailing in the twenty-first century. Vietnam is not out of the woods just yet. There are constraints, institutional hurdles, and problems to be tackled if Vietnam is to sidestep the middle-income trap. And for its trade to flourish and the complexity of its exports to increase, global value chains for electronics, auto parts, garments, and resource-based commodities would need to stabilize and possibly grow.2 GROWTH, TRADE, AND FOREIGN DIRECT INVESTMENT SINCE 2000 Vietnam’s per capita GDP in 2000 was US$390; poverty (below $1.90 per day, 2011 PPP) was widespread (37 percent in 2002);3 and exports accounted for 54 percent of GDP, with petroleum and agricultural and aquacultural commodities heading the list (approximately half of the total). -

Wool Sourcing Guide Vietnam Vietnam

WOOL SOURCING GUIDE VIETNAM VIETNAM The Vietnam textile industry is the third largest apparel exporter in the world accounting for 6.3 per cent of world apparel exports in 2019. Once mainly a cut and sew supplier, Vietnam now boasts a robust wool supply chain including spinning, weaving, knitting and whole garment manufacturing. HANOI This vertical integration means designers, brands and HAI PHONG buyers can source all their garment requirements from the one country, cutting out logistical times and dealing with many suppliers. CAPITAL CITY: Hanoi AREA: 329,560 Sqkm POPULATION: 96.46 million (2019) DA NANG LANGUAGE: Vietnamese (official), Chinese, English, and French HOI AN RELIGION: Buddhism, Taoism, and Catholic CLIMATE: North Vietnam has a Southern Mediterranean QUY NHON climate and South Vietnam has a tropical monsoon climate type. MAJOR PORTS: Cam Pha, Da Nang, Haiphong, Ho Chi Minh, NHA TRANG Phu My, Quy Nhon DA LAT ECONOMY: Since early 2000, Vietnam has been progressively moving away from a centrally planned economy to a socialist- HO CHI MINH CITY oriented market economy. CURRENCY: The Vietnamese Dong (JUN 2015: 1USD = 21,673VND) THE WOOLMARK COMPANY AND VIETNAM The Woolmark Company (TWC) first identified Vietnam as an emerging manufacturing hub for wool textiles in 2012 when the Vietnam textile industry begun to focus on moving toward high quality products and production. Since then, we have been working closely with partners throughout the supply chain and currently collaborate with more than 90 partners including flatbed knitters, circular knitters and garment making companies. We have transferred technical knowhow about the manufacturing of wool products, disseminated information about sources of raw materials, chemicals and machines, and organised international trade missions to connect our project partners with buyers. -

1. Oil and Gas Exploration & Production

1. Oil and gas exploration & production This is the core business of PVN, the current metres per year. By 2012, we are planning to achieve reserves are approximated of 1.4 billion cubic metres 20 million tons of oil and 15 billion cubic metres of of oil equivalent. In which, oil reserve is about 700 gas annually. million cubic metres and gas reserve is about 700 In this area, we are calling for foreign investment in million cubic metres of oil equivalent. PVN has both of our domestic blocks as well as oversea explored more than 300 million cubic metres of oil projects including: Blocks in Song Hong Basin, Phu and about 94 billion cubic metres of gas. Khanh Basin, Nam Con Son Basin, Malay Tho Chu, Until 2020, we are planning to increase oil and gas Phu Quoc Basin, Mekong Delta and overseas blocks reserves to 40-50 million cubic metres of oil in Malaysia, Uzbekistan, Laos, and Cambodia. equivalent per year; in which the domestic reserves The opportunities are described in detail on the increase to 30-35 million cubic metres per year and following pages. oversea reserves increase to 10-15 million cubic Overseas Oil and Gas Exploration and Production Projects RUSSIAN FEDERATION Rusvietpetro: A Joint Venture with Zarubezhneft Gazpromviet: A Joint Venture with Gazprom UZBEKISTAN ALGERIA Petroleum Contracts, Blocks Kossor, Molabaur Petroleum Contract, Study Agreement in Bukharakhiva Block 433a & 416b MONGOLIA Petroleum Contract, Block Tamtsaq CUBA Petroleum Contract, Blocks 31, 32, 42, 43 1. Oil and gas exploration & production e) LAO PDR Petroleum Contract, Block Champasak CAMBODIA 2. -

Textile & Apparel Industry Report

TEXTILE & APPAREL INDUSTRY REPORT OPPORTUNITIES FOR BREAKTHROUGH “...With internal advantages and expectations from Free Trade Agreements, Vietnam textile and apparel industry is now having opportunities for overall changes of deep development and expansion ” Bui Van Tot Senior Analyst E: [email protected] P: (08) -6290 8686 - Ext: 7593 04/2014 APPAREL INDUSTRY CONTENT Highlights 1 I. World textile and apparel industry 2 WORLD 1. Overview of the global textile and apparel industry 2 2. Global textile and apparel value chain 4 3. Main modes of production 8 3. Apparel machinery industry 9 II. Vietnam textile and apparel industry 11 1. Overview of Vietnam's textile and apparel industry 11 2. Export and import 13 VIETNAM 3. Value Chain of Vietnam's textile and apparel industry 18 3. Michael Porter Model Analysis 20 4. SWOT Analysis 22 5. Free Trade Agreements 23 7. Legality, related policies 25 III. Textile and apparel businesses 27 BUSINESSES 1. Business performance 27 2. Financial situation 31 3. Recommendations for listed companies 35 4. Typical unlisted companies 38 Appendix 40 Abbreviations Thanh Cong Textile Garment - Investment - Trading Joint TCM Stock Company GMC Saigon Garment Manufacturing Trading JSC EVE Everpia Vietnam JSC Binh Thanh Import - Export - Production and Trade Joint Stock GIL Company TNG TNG Investment and Trading JSC KMR Mirae Joint Stock Company NPS Phu Thinh - Nha Be Textile Joint Stock Company VITAS Vietnam Textile and Apparel Association VCOSA Viet Nam Cotton & Spinning Association MARD Ministry of Agriculture & Rural Development FDI Foreign Direct Investment TPP Trans-Pacific Strategic Economic Partnership Agreement FTA Free Trade Agreement MUTRAP European Trade Policy and Investment Support Project APPAREL INDUSTRY HIGHLIGHTS The current global apparel market is estimated at With an average growth rate of 14.5% per year for the US$1,100bn with trade value of US$700bn. -

An Analysis of Consumer's Need and Behavior in Purchasing Garment In

Journal of Economics, Business and Management, Vol. 5, No. 2, February 2017 An Analysis of Consumer’s Need and Behavior in Purchasing Garment in Vietnam Thao Thi Phuong Vu Chinese rival. Abstract—The paper focuses on the facts that what customers truly desire about garment products and the reason why they, in majority, tend to choose Chinese garment to purchase. Detailed II. CONTENT analyses on Vietnamese garment industry’s weaknesses as well as strengths depending on the result of the survey are also A. The Development of Vietnamese Garment Industry written down so that right actions will be decided in order to help local garment in this rivalry. Since the aim of the topic is to help Vietnamese garment Some solutions are suggested by analyzing the opportunities recover its domination before its mainly current rival Chinese and challenges with which Vietnamese garment meet hence in its local market, to understand deeply Vietnamese garment there will be great chance for local garment products in industry’s history is definitely necessary. From this satisfying its resident customers. The real target of Vietnamese knowledge, the research partly figures out which are its strong garment industry is to affirm its position not only within local and weak points at the first place as well as is aware of what market but also in the world’s market with the general brand name “made in Vietnam”. have led to these strengths and weaknesses. There are quite a number of issues which Vietnam’s After the peaceful revolution in October 1954, communist industries generally and garment industry privately need to party and government of Vietnam decided to restore fiber, alter; however, the three main things to garment enterprises are textile, dye factories, especially those in Nam Dinh province considered as “material, design and prices”. -

Annual Report 2019 an Industry and Compliance Review Vietnam

Annual Report 2019 An Industry And Compliance Review Vietnam REPORTING PERIOD January 2017 – June 2018 ILO CATALOGUING IN PUBLICATION DATA Better Work Vietnam: garment industry 10th compliance synthesis report / International Labour Office; International Finance Corporation. - Geneva: ILO, 2019 1 v. ISSN 2227-958X (web pdf) International Labour Office; International Finance Corporation clothing industry / textile industry / working conditions / workers’ rights / labour legislation / ILO Con- vention / international labour standards / comment / application / Vietnam 08.09.3 Copyright © International Labour Organization (ILO) and Inter- The designations employed in this, which are in conformity national Finance Corporation (IFC) (2019) with United Nations practice, and the presentation of material therein do not imply the expression of any opinion whatsoever First published (2019) on the part of the IFC or ILO concerning the legal status of any Publications of the ILO enjoy copyright under Protocol 2 of the country, area or territory or of its authorities, or concerning the Universal Copyright Convention. Nevertheless, short excerpts delimitation of its frontiers. from them may be reproduced without authorization, on The responsibility for opinions expressed in signed articles, condition that the source is indicated. For rights of reproduction studies and other contributions rests solely with their authors, or translation, application should be made to the ILO, acting and publication does not constitute an endorsement by the IFC on behalf of both organisations: ILO Publications (Rights and or ILO of the opinions expressed in them. Permissions), International Labour Office, CH-1211 Geneva 22, Switzerland, or by email: [email protected]. The IFC and ILO Reference to names of firms and commercial products and welcome such applications. -

A Comparative Study on Distribution Channels of Textile

1 FacultyofEconomicSciences,CommunicationandIT MuhammadUsmanKhan Acomparativestudyondistribution channelsoftextileandgarment industryinPakistanandVietnam: TherolesofIntermediaries Marketing Datum/Termin: 2010/05/20 Handledare: LarsHaglund Karlstads universitet 651 88 Karlstad Tfn 054-700 10 00 Fax 054-700 14 60 [email protected] www.kau.se 2 Table of Contents 1. Introduction ......................................................................................................................................... 5 2. Background .......................................................................................................................................... 5 2.1 Why Pakistan ................................................................................................................................. 5 2.2 Why textile industry in Pakistan .................................................................................................... 6 2.3 Pakistan Competitive Advantages ................................................................................................. 6 2.3 Why Vietnam ................................................................................................................................. 6 2.4 Why middle man ............................................................................................................................ 6 2.5 International Distribution channel in Connection with Pakistani and Vietnamese distribution channel ............................................................................................................................................... -

The Central Region of Vietnam

GOING FOR GOLD The Central Region of Vietnam 2017 Investment Guide to the Central Region of Vietnam In association with Da Nang Welcomes APEC VIET NAM 2017 Nguyen Tien Quang Director of VCCI Da Nang Foreword The publication “Going for Gold - The Central Region of Vietnam” was developed as a guidebook to introduce the economic potential and investment opportunities of localities and enterprises in the Central Region - Highlands of Vietnam, to businesspeople and investors from the 21 Asia-Pacific economies taking part in the APEC Vietnam 2017 events. In the publication process, the local authorities in the region have effectively cooperated with VCCI Da Nang. The process has also attracted the response of regional entrepreneurs. We would like to express our sincere thanks to partners and sponsors for your valuable cooperation. VCCI Da Nang would like to thank KPMG Vietnam for their professional consultancy. They have made great contributions to the publication. In particular, we would like to thank Dr. Vu Tien Loc - Chairman of VCCI - for his encouragement and support in the publication process. Despite our efforts, there are still inevitable shortcomings in this guidebook. We look forward to readers’ understanding and feedback. Best Regards! On behalf of Editorial Board Nguyen Tien Quang Director of VCCI Da Nang Creating New Dynamism, Fostering a Shared Future Editorial Board: • Investment and Trade Promotion Center of Quang Ngai Province Editor-in-Chief: Nguyen Tien Quang • Investment and Trade Promotion Center of Binh Dinh Province Editors: -

South East Asia Stepping Into the Textile Future Oerlikon Neumag

issue 23 – january 2016 South East Asia stepping into the textile future A portrait of Indonesia, Malaysia, Thailand and Vietnam With the ASEAN states, the Southeast Asia textile region comprises an economic area of around 10% of the world’s population. Oerlikon Neumag focusses on polyester nonwovens Technical nonwovens on the rise Polyester is becoming increasingly significant in the spunbond sector. "In conjunction with the WinTape take-up unit, the EvoTape system increases profitability of tape yarn production by up to 50% compared to conventional, standard systems. “ Steffen Husfeldt Head of Chemnitz Site Oerlikon Barmag Faster, higher, smarter Tape yarn production with EvoTape and WinTape Faster production Boost operations with extreme productivity and minimum space requirements. Higher than ever before Achieve superlative efficiency with the lowest energy consumption, raw materials usage and staff requirements.The EvoTape concept fulfills the requirements of the e-save label. Smarter investments Ensure your production is sustainable, efficient and future-oriented. The concept is currently available for the production of tape yarns for Carpet backing Geotextiles Baler twine Sacks and big bags For further information visit us at Follow us on Facebook! www.evotape.barmag.com www.facebook.com/OerlikonBarmag OMF Anzeige BSZ 210x297mm fb EN 160119.indd 1 19.01.16 11:30 In focus Editorial Southeast Asia stepping into the textile future With the ASEAN states, the South- east Asia textile region comprises an economic area of around 10% of the world’s population. 8 Innovation and technology Dear Customers, dear Readers, Oerlikon Neumag focusses on The manmade fiber industry is also a growth engine outside polyester nonwovens of China and India. -

Vietnam Country Study Labour Standards in the Garment Supply Chain

Vietnam country study Labour Standards in the Garment Supply Chain Strategic Partnership for Garment Supply Chain Transformation Vietnam country study Labour Standards in the Garment Supply Chain by Do Quynh Chi, Research Center for Employment Relations (ERC) Vietnam country study - Labour standards in the garment supply chain 3 Table of Contents Introduction 1. Executive Summary p. 7 2. General country information p. 9 2.1. Economic indicators p. 11 2.2. Social, political & governance indicators p. 12 2.3. Income and poverty p. 12 2.4. General human rights situation p. 13 3. The Garment Industry p. 14 4. Industrial Relations p. 17 4.1 Industrial Relations p. 18 4.2 Living Wage p. 19 4.3. Gender-based Violence p. 21 5. Local and international stakeholders p. 23 5.1 Governmental institutions p. 24 5.2 Employers organizations p. 24 5.3 Trade unions, p. 25 5.4 Labour NGO’s p. 26 5.5 Brands and factories p. 27 5.6 Other initiatives p. 28 6. Implementation of the Core Labour Standards p. 29 6.1 Employment is freely chosen p. 30 6.2 There is no discrimination in employment p. 31 6.3 No exploitation of child labour p. 31 6.4 Freedom of association and the right to collective bargaining p. 32 6.5 Payment of a living wage p. 33 6.6 No excessive working hours p. 36 6.7 Safe and healthy working conditions p. 36 6.8 Legally-binding employment relationship p. 37 7. Good and / or innovative practices p. 38 7.1 Living wage p.