044000494.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Décision N° 16-DCC-210 Du 9 Décembre 2016 Relative À La Prise

RÉPUBLIQUE FRANÇAISE Décision n° 16-DCC-210 du 9 décembre 2016 relative à la prise de contrôle conjoint d’un fonds de commerce exploité par la société ATAC par la société Worksea et ITM Entreprises L’Autorité de la concurrence, Vu le dossier de notification adressé complet au service des concentrations le 9 novembre 2016, relatif à la prise de contrôle conjoint d’un fonds de commerce exploité par la société ATAC par la société Worksea et ITM Entreprises, formalisée par une lettre d’intention en date du 22 juillet 2016 ; Vu le livre IV du code de commerce relatif à la liberté des prix et de la concurrence, et notamment ses articles L. 430-1 à L. 430-7 ; Adopte la décision suivante : I. Les entreprises concernées et l’opération 1. ITM Entreprises, société contrôlée à 100 % par la société civile des Mousquetaires, elle-même détenue par 1 330 personnes physiques dits « adhérents associés », conduit et anime le réseau de commerçants indépendants connu sous le nom de « Groupement des Mousquetaires ». En sa qualité de franchiseur, la société ITM Entreprises a comme activité principale l’animation d’un réseau de points de vente, alimentaires et non alimentaires, exploités par des commerçants indépendants sous les enseignes suivantes : Intermarché, Ecomarché, Netto, Restaumarché, Bricomarché, Roady et Vêti. Cette gestion s’effectue notamment au travers de la signature et du suivi de contrats d’enseigne avec les sociétés exploitant ces points de vente. ITM Entreprises met également à la disposition de ses franchisés divers services de prospection, de conseil, de formation, etc. Enfin, ITM Entreprises offre aux franchisés la possibilité de bénéficier de conditions d’approvisionnement avantageuses auprès de ses filiales nationales et régionales mais également de fournisseurs référencés extérieurs au « Groupement des Mousquetaires ». -

Why Food Waste Is Becoming a Revolution? Putting the Bin out of Business Could Be Good for Business November 2017

Why food waste is becoming a revolution? Putting the bin out of business could be good for business November 2017 This article was written by Léonore Perrin from “We are Phenix” a successful French social company born in 2014 who helps businesses to turn waste into wealth by unleashing the potential of surplus products. L’Institut du Commerce asked “We are Phenix” to explain to the ECR Community the current waste initiatives’ landscape in France. Since 2017, l’Institut du Commerce embodies the Efficient Consumer Response in France. The association supports its members (manufacturers, retailers and service providers) to work together to better fulfill the consumers’ needs. More precisely, it provides them with the perfect framework to build collectively tomorrow’s businesses thanks to a better understanding of the deep changes occurring for the shopper, the supply chain and the retail (data, environment, technology…). There is an urge to eradicate waste in our societies. The circular economy is a basic yet revolutionary approach that could transform tomorrow’s production and consumption. L’Institut du Commerce is proud to announce the launch in December 2017 of a new working group entitled « Circular Economy: How can retail have a positive impact »? Each year, an estimated 1.3 billion tons of food is lost or wasted globally. That’s over a third of the world’s food production which is thrown away, somewhere between farm to fork. In the European Union it is estimated that 11% of food losses and waste occurs at the production level, while 17% at the distribution level. From food banks to food aid organizations, food redistribution is not a new thing. -

Questions Autour D'une Alliance!^

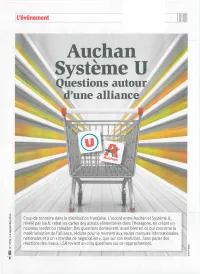

L'événement 11 Auçhan SystèmQuestions autoue Ur d'une alliance!^ Coup de tonnerre dans la distribution française. L'accord entre Auchan et Système U, révélé par lsa.fr, rebat les cartes des achats alimentaires dans l'Hexagone, en créant un nouveau leader ou coleader. Des questions demeurent, aussi bien en ce qui concerne la matérialisation de l'alliance, réduite pour le moment aux seules marques internationales, nationales et à un «mandat de négociation», que sur son évolution. Sans parler des réactions des rivaux. LSA revient en cinq questions sur ce rapprochement. n L'événement Est-cela naissanced'un nouveau leader ? Par la grâce d'un accord mettant leurs achats en commun via un mandat de négociation confié à la centrale Eurauchan, Serge Papin, patron de Système U, et Vianney Mulliez, président du conseil de ' 1« *' | surveillance d'Auchan, passent en France du statut de challenger à jJ <r> H, H 0 celui de poids lourds de la distribution alimentaire. LES CHIFFRES VENTES CUMULÉES 44,5 Mrds€ (CA TTC avec carburants) 210 hypers, ur le papier, l'addition des chiffres d'affaires comme une concentration, et ne sera pas notifié 1039 supers, d'Auchan et de Système U place le nouvel à l'Autorité de la concurrence. Il n'empêche, leurs 715 proxi Sensemble en position de leader virtuel de la parts de marché cumulées constitueront bien le AUCHAN distribution alimentaire en France. «Système A», véritable poids économique à l'achat des nouveaux 16,8 Mrds€ (-2,6%) comme certains nomment déjà la nouvelle alliance, alliés. Ils détiennent ensemble 21,5 % de part de 139 magasins «pèse» 44,5 Mrds € de chiffre d'affaires TTC avec marché depuis le début de l'année (selon Kantar), SIMPLYMARKET carburants, selon le dernier top 100 de LSA. -

“Continuing to Innovate for the Future of Retail” Contents Contents

2018 ANNUAL REPORT “CONTINUING TO INNOVATE FOR THE FUTURE OF RETAIL” CONTENTS CONTENTS INTERVIEW WITH “WHAT’S THE PURPOSE JEAN-CHARLES HIGHLIGHTS KEY FIGURES NAOURI PAGE 6 PAGE 12 OF AN ANNUAL REPORT?” PAGE 2 POWERFUL STRATEGIC A RESPONSIBLE GOVERNANCE BRANDS ALLIANCES APPROACH t’s a question that comes up often, in them an enticing shopping experience, PAGE 14 PAGE 20 PAGE 30 PAGE 38 all large companies. and making their lives easier with I With 12,000 stores that open their helpful services and innovative digital doors every morning – under such solutions. banners as Vival, Franprix, Naturalia, To infuse some of that energy into our Éxito, Assaí and Devoto – and hundreds annual report, we interviewed around of transformation projects to be sixty men and women who work in a very INTERNATIONAL INNOVATION AUGMENTED A MORE PRESENCE CULTURE STORES AGILE MODEL implemented in an ever shorter time to wide range of positions within the market, the Casino Group views the company, from store greeter to Executive PAGE 48 PAGE 58 PAGE 68 PAGE 78 annual report as an invaluable Committee member. “What does Casino opportunity to take a step back from the represent for you?”, “How is your job frenetic race against the clock that evolving?” and “What are today’s trends represents the daily routine in the retail in terms of customer expectations?”. sector. The result is this annual report, which BANNERS AND SOCIETAL FINANCIAL Casino has more than 220,000 service- provides an overview of the Casino SUBSIDIARIES PERFORMANCE PERFORMANCE oriented employees who are fully Group and shares the beliefs and committed to providing our customers enthusiasm of a small sample of the PAGE 86 PAGE 108 PAGE 122 with safe, high-quality products, offering people behind its success. -

VIANNEY MULLIEZ : C’Est Un Beau Cadeau D’Anniversaire, Pour Les 50 Ans De Notre Entreprise, Que De Constater Combien L’Histoire Nous a Donné Raison

VIANNEY MULLIEZ : C’est un beau cadeau d’anniversaire, pour les 50 ans de notre entreprise, que de constater combien l’Histoire nous a donné raison. Chez Auchan, nous n’en tirons aucune vanité, mais comment ne pas nous réjouir du choix judicieux qu’a fait, en 1961, notre fondateur Gérard Mulliez. D’emblée, il nous a doté d’une vision et d’une identité forte en misant résolument sur les valeurs humaines et en décidant que, chez Auchan, jamais on ne transigerait avec celles-ci. ARNAUD MULLIEZ : Des valeurs si ancrées dans notre culture d’entreprise qu’elles font notre réputation et notre fierté. Pour nous, et dans tous nos métiers, il importe que le « process » soit au service de l’Homme et cela ne doit jamais être l’inverse. Cette approche prend tout son L’EÉDITO DE VIANNEY MULLIEZ ET D’ARNAUD MULLIEZ ème Edito sens, au début de ce XXI siècle, dans un monde économique globalisé que la récente crise a ébranlé dans ses certitudes. Les experts, les observateurs expliquent cette crise, qui est d’abord une crise de confiance, par le fait que nombre de managers auraient trop misé sur le profit et le court terme. VIANNEY MULLIEZ : « Il faut absolument remettre l’homme au cœur de l’entreprise » insiste-t-on aujourd’hui. 19612011 Mais, chez Auchan, l’Homme est depuis toujours « la » priorité pour les dirigeants, dans tous nos différents métiers basés sur notre expertise de la consommation et fédérés au sein de notre groupe. Qu’il s’agisse de la grande distribution, de la banque, de l’immobilier commercial ou d’Internet. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases. -

Décision N° 14-DCC-11 Du 28 Janvier 2014 Relative À La Prise De Contrôle Par La Société Franprix Leader Price Holding De 4

RÉPUBLIQUE FRANÇAISE Décision n° 14-DCC-11 du 28 janvier 2014 relative à la prise de contrôle par la société Franprix Leader Price Holding de 47 magasins de commerce de détail à dominante alimentaire Le Mutant et de 22 fonds de commerce de boucherie L’Autorité de la concurrence, Vu le dossier de notification adressé complet au service des concentrations le 11 décembre 2013, relatif à la prise de contrôle de 47 magasins de commerce de détail à dominante alimentaire et de 22 fonds de commerce de boucherie par la société Franprix Leader Price Holding (« FLPH »), formalisée par un protocole d’accord conclu le 25 octobre 2013 ; Vu le livre IV du code de commerce relatif à la liberté des prix et de la concurrence, et notamment ses articles L. 430-1 à L. 430-7 ; Vu les engagements présentés le 14 janvier 2014 par la partie notifiante ; Vu les éléments complémentaires transmis par les parties au cours de l’instruction ; Adopte la décision suivante : I. Les entreprises concernées et l’opération 1. La société Franprix Leader Price Holding (ci-après « FPLPH ») est une filiale du groupe Casino Guichard Perrachon (ci-après « Casino »), dont le principal objet est la prise de participation dans des sociétés exploitant des magasins sous les enseignes Franprix et Leader Price. Le groupe Casino, troisième acteur français du secteur de la distribution à dominante alimentaire, gère un parc de plus de 12 000 magasins dans le monde (hypermarchés, supermarchés, magasins de proximité, magasins discompteurs) sous les enseignes notamment Géant Casino, Franprix, Casino Supermarché, Petit Casino, Casino Shop, Casino Shopping, Spar, Vival, Monoprix et Leader Price. -

Overseas Packaging Study Tour VAMP.006 1996

Overseas packaging study tour VAMP.006 1996 Prepared by: B. Lee ISBN: 1 74036 973 4 Published: June 1996 © 1998 This publication is published by Meat & Livestock Australia Limited ABN 39 081 678 364 (MLA). Where possible, care is taken to ensure the accuracy of information in the publication. Reproduction in whole or in part of this publication is prohibited without the prior written consent of MLA. MEAT & LIVESTOCK AUSTRALIA CONTENTS 1.0 EXECUTIVE SUMMARY ............................................ 1 2.0 BACKGROUND .................................................... 4 3.0 THE INTERNATIONAL STUDY TOUR .............. .................. 6 3.1 Objectives of the International Study Tour ................................. 6 3.2 Study Tour Itinerary and Dates .......................................... 6 3.3 The Study Team ...................................................... 6 4.0 SUMMARY OF SITE VISITS ......................................... 7 4.1 Taiwan ............................................................. 7 4.2 Hong Kong .......................................................... 8 4.3 France .............................................................. 9 4.4 Holland ............................................................ l 0 4.5 United Kingdom ..................................................... 13 4.6 Canada ............................................................ 15 4.7 Summary Comments of Site Visits by Study Group ......................... 17 5.0 KEY FINDINGS FROM THE STUDY TOUR ....... .................... 18 5.1 -

Company Presentationpresentation

April 2020 CompanyCompany PresentationPresentation 1 Who we are Family Business based in Provence created in 2000 by Franck Bonfils, current CEO. The first peanuts come out of Setting up in the first warehouse Construction of the first plant in Launch of the first ORGANIC the family kitchen. Carpentras! range. New plant of 10 000 M² Launch of the « Bulk full service » Launch of the brand Launch of the first bag operational in 2020 to support the concept in French supermarkets « JUSTE BIO ». biodegradable and compostable development of the activity Who we are A fast and continuous growth since A constantly reinforced workforce 2014… on strategic positions 73 48 30 80 100 32 13,5 19 7,5 4,5 2014 2015 2016 2017 2018 2019 2016 2017 2018 2019 Turnover in M€ Staff Our mission: Simplify access to organic high quality products 4000 Supermarkets equipped with our distributors in France and abroad A wide and differentiating range: 141 references certified organic ALL segments covered PLASTIC FREE ORGANIC CHOICE All are products are controlled and packaged in France. Our Quality Policy: 7 500 T of organic products packaged in 2019 • A precise knowledge of the ORGANIC sector • An ECOCERT certified production site 60% of the investments devoted to Quality and production tools An enhanced analysis plan: • 100% of the “raw material / supplier” pair controlled by independent laboratories, • Products manufactured and / or packaged in our premises, • A systematic control of the batches during production. New supplier : Analysis of the 6 first receptions -

L'alliance Ratée Auchan-Système U

Dany Vyt Maître de Conférences, Centre de Recherche en Economie et Management (CREM UMR CNRS 6211), IGR-IAE Rennes, [email protected] Magali Jara Maître de Conférences, Laboratoire d'Economie et de Management (LEMNA), IUT de Saint Nazaire-Université de Nantes, [email protected] Gérard Cliquet Maître de Conférences, Centre de Recherche en Economie et Management (CREM UMR CNRS 6211), IGR-IAE Rennes, [email protected] 1 L’alliance ratée Auchan-Système U Résumé: Ce travail consiste à mesurer les enjeux des fusions-acquisitions au sein des réseaux de distribution. L’évolution des rapprochements dans ce secteur qui passe d’une compétition à une coopétition est détaillée avant d’évoquer les enjeux territoriaux des politiques de rapprochement des réseaux. Nous étudions en détail le cas de la fusion avortée entre les groupes Auchan et Système U . A partir de l’entropie relative, indice qui permet de mesurer la dispersion spatiale d’un réseau, nous quantifions l’apport en matière de couverture territoriale d’un tel transfert d’enseignes. Alors que la mise en commun des moyens, notamment en ce qui concerne la mutualisation des centrales d’achat dans une logique de sourcing transcende la forme organisationnelle des parties prenantes, l’échange de magasins au sein de ce type d’organisation hybride était voué à l’échec. Mots-clés : Auchan, Acquisitions, Fusions, Entropie, Système U. Auchan and Systeme U: a failed merger Abstract: The objective of this paper is to measure the challenges of mergers and acquisitions within the retailing networks. We measure the evolution of the mergers in the retail field which moves from a competition to a coopetition. -

FRENCH MARKET PRESENTATION for : FEVIA from : Sophie Delcroix – Elise Deroo – Green Seed France Date : 19Th June, 2014

FRENCH MARKET PRESENTATION For : FEVIA From : Sophie Delcroix – Elise Deroo – Green Seed France Date : 19th June, 2014 FEVIA 1 I. GREEN SEED GROUP : WHO WE ARE II. MARKET BACKGROUND AND CONSUMER TRENDS III. THE FRENCH RETAIL SECTOR IV. KEY RETAILERS PROFILES V. FOODSERVICE VI. KEY LEARNINGS VII. CASE STUDIES FEVIA 2 Green Seed Group Having 25 years of experience, the Green Seed Group is a unique international network of 11 offices in Europe, North America and Australia, specializing in the food & beverage sector OUR MISSION Advise both French and foreign food and beverage companies or marketing boards, on how to develop a sustainable and profitable position abroad Green Seed France help you to develop your activity in France using our in-depth knowledge of the local food and beverage market and our established contacts within the trade FEVIA 3 A growing and unique international network Germany (+ A, CH) The Netherlands Scandinavia U.S.A./Canada Great Britain Belgium France Portugal Spain Italy 11 offices covering 18 countries Australasia FEVIA 4 The Green Seed model Over the last decade, one of the most important trends in the French food & drink trade has been for retailers to deal with their suppliers on a direct line. Green Seed France has developed its business model around this trend. We act as business facilitators ensuring that every step of the process is managed with maximum efficiency. From first market visit, to launch as well as the ongoing relationship that follows. We offer a highly cost-effective solution of “flexible local sales and marketing management support” aimed at adding value. -

Direction Des Statistiques D'entreprises E2015/01

Direction des Statistiques d'Entreprises E2015/01 La concurrence du hard discount : quels effets sur les prix et l’emploi ? Pierre BISCOURP Document de travail Institut National de la Statistique et des Études Économiques 1 Institut National de la Statistique et des Études Économiques Série des documents de travail de la Direction des Statistiques d'Entreprises E 2015/01 La concurrence du hard discount : quels effets sur les prix et l’emploi ? Pierre BISCOURP 1 Mars 2015 Ces documents de travail ne reflètent pas la position de l'INSEE et n'engagent que leurs auteurs. Working papers de not reflect the position of INSEE but only their author's views. 1 Division Commerce, Insee. 2 La concurrence du hard discount : quels effets sur les prix et l’emploi ? Pierre Biscourp, Insee Mars 2015 Résumé L’arrivée sur le marché français des chaînes allemandes de hard discount à la fin des années 1980 a constitué un choc majeur. Les réseaux allemands de hard discount, en premier lieu Aldi et Lidl, ont pénétré le territoire français à partir de ses frontières Nord et Est, avant de s’étendre progressivement vers le Sud. Entre le début des années 1990 et la fin des années 2000, ils ont investi la quasi-totalité du marché français. On interprète le schéma d’expansion géographique « en tâche d’huile » à partir du concept d’économies de densité proposé par Holmes (2011) pour expliquer le développement de Wal- Mart aux Etats-Unis. Un réseau réalise des économies de densité lorsque l’implantation des magasins et des plateformes logistiques minimise le coût de distribution.