Overseas Packaging Study Tour VAMP.006 1996

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pipanniversarybrochure.Pdf

www.jardines.com “ Pride in Performance has enabled us to share and celebrate successes across the Group. Anthony Nightingale ” CONTENTS 2 A Decade of Pride in Performance 3 How it Works 5 5 elements to Success 6 Striving 12 Innovating 20 Collaborating 26 Solving 34 Connecting 45 The Entries A DECADE OF PRIDE IN PERFORMANCE HOW IT WORKs A myriad of achievements have contributed to Jardine Matheson’s success since its From inception, the chief executive officers of each business gave their support and founding in 1832. The content of this booklet, however, considers the Group’s more recent encouragement to the new award programme, getting PIP off to an excellent start. history, and a formalized approach that was launched in 2002 to identify and reward outstanding performances across the Group. In the first three years of PIP, entrants sought recognition as the Grand Prize Winner or one of two runners up. From 2005, five categories were introduced so as to recognize specific Through the Pride in Performance (‘PIP’) annual award programme, Jardines recognizes areas of achievement, from which the Grand Prize Winner is then chosen. individual business units within the Group that embody its core values and translate them into sustained commercial success. In addition to recognition, PIP is designed to share Of the categories, some remained consistent, such as Customer Focus, Marketing those operating company success stories with the larger Group. Excellence and Successful New Venture, while others evolved. Business Turnaround became Business Outperformance as the Group’s operations progressed, and Productivity Using the Group’s core values as criteria for submission – The Right People, Energy, Enhancement evolved into Innovation and Creativity. -

16. Redmart Singapore

REDMART SINGAPORE DELIVERING FRESHNESS AND CONVENIENCE WITH ONLINE GROCERY SHOPPING S/N 88-16-016 RedMart Singapore – Delivering Freshness and Convenience with Online Grocery Shopping Launched in 2011, Redmart Singapore is an online grocery retailer that provides a selection of more than 4,000 groceries and home essentials to Singapore households. Roger Egan, founder and Chief Executive Officer has aspirations for RedMart to be like e-commerce giants, Amazon and eBay one day. The company sees itself as a logistics and technology company and its mission is to be the “eBay for consumer packaged goods manufacturers” (Lee, 2014). What started out as a business targeting at the expatriate crowd has changed over time. By 2015, three-quarters of its customers were locals, working professionals, mainly women between 25 and 44 years old, and were likely to be millennials and Gen-X Singaporeans who shopped both online and offline (Nielsen, 2015). Fast forward to 2016, RedMart has more than 20,000 items on its online shopping site. It has launched the RedMart Relay service that provides personal shopping services for consumers who want hot meals, household items or electronic goods delivered to their homes within one hour of ordering. Although RedMart appears to have enjoyed rapid growth in a short span of time, it is still a young start-up company facing direct competition from bigger supermarkets and other online competitors. Despite its aggressive marketing efforts and investment in technology, RedMart’s chief executive, Roger Egan notes that many Singaporeans still prefers grocery shopping at supermarkets and wet markets over shopping online. -

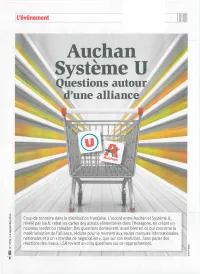

Questions Autour D'une Alliance!^

L'événement 11 Auçhan SystèmQuestions autoue Ur d'une alliance!^ Coup de tonnerre dans la distribution française. L'accord entre Auchan et Système U, révélé par lsa.fr, rebat les cartes des achats alimentaires dans l'Hexagone, en créant un nouveau leader ou coleader. Des questions demeurent, aussi bien en ce qui concerne la matérialisation de l'alliance, réduite pour le moment aux seules marques internationales, nationales et à un «mandat de négociation», que sur son évolution. Sans parler des réactions des rivaux. LSA revient en cinq questions sur ce rapprochement. n L'événement Est-cela naissanced'un nouveau leader ? Par la grâce d'un accord mettant leurs achats en commun via un mandat de négociation confié à la centrale Eurauchan, Serge Papin, patron de Système U, et Vianney Mulliez, président du conseil de ' 1« *' | surveillance d'Auchan, passent en France du statut de challenger à jJ <r> H, H 0 celui de poids lourds de la distribution alimentaire. LES CHIFFRES VENTES CUMULÉES 44,5 Mrds€ (CA TTC avec carburants) 210 hypers, ur le papier, l'addition des chiffres d'affaires comme une concentration, et ne sera pas notifié 1039 supers, d'Auchan et de Système U place le nouvel à l'Autorité de la concurrence. Il n'empêche, leurs 715 proxi Sensemble en position de leader virtuel de la parts de marché cumulées constitueront bien le AUCHAN distribution alimentaire en France. «Système A», véritable poids économique à l'achat des nouveaux 16,8 Mrds€ (-2,6%) comme certains nomment déjà la nouvelle alliance, alliés. Ils détiennent ensemble 21,5 % de part de 139 magasins «pèse» 44,5 Mrds € de chiffre d'affaires TTC avec marché depuis le début de l'année (selon Kantar), SIMPLYMARKET carburants, selon le dernier top 100 de LSA. -

Annual Report 2019 Our Goal: “ to Give Our Customers Across Asia a Store They TRUST, Delivering QUALITY, SERVICE and VALUE.”

Annual Report 2019 Our Goal: “ To give our customers across Asia a store they TRUST, delivering QUALITY, SERVICE and VALUE.” Dairy Farm International Holdings Limited is incorporated in Bermuda and has a standard listing on the London Stock Exchange, with secondary listings in Bermuda and Singapore. The Group’s businesses are managed from Hong Kong by Dairy Farm Management Services Limited through its regional offices. Dairy Farm is a member of the Jardine Matheson Group. A member of the Jardine Matheson Group Annual Report 2019 1 Contents 2 Corporate Information 36 Financial Review 3 Dairy Farm At-a-Glance 39 Directors’ Profiles 4 Highlights 41 Our Leadership 6 Chairman’s Statement 44 Financial Statements 10 Group Chief Executive’s Review 116 Independent Auditors’ Report 14 Sustainable Transformation at Dairy Farm 124 Five Year Summary 18 Business Review 125 Responsibility Statement 18 Food 126 Corporate Governance 22 Health and Beauty 133 Principal Risks and Uncertainties 26 Home Furnishings 135 Shareholder Information 30 Restaurants 136 Retail Outlets Summary 34 Other Associates 137 Management and Offices 2 Dairy Farm International Holdings Limited Corporate Information Directors Dairy Farm Management Services Limited Ben Keswick Chairman and Managing Director Ian McLeod Directors Group Chief Executive Ben Keswick Clem Constantine Chairman (joined the Board on 11th November 2019) Ian McLeod Neil Galloway Group Chief Executive (stepped down on 31st March 2019) Clem Constantine Mark Greenberg Chief Financial Officer (joined the board on 19th November 2019) George J. Ho Neil Galloway Adam Keswick Group Finance & IKEA Director (stepped down on 31st March 2019) Simon Keswick (stepped down on 1st January 2020) Choo Peng Chee Chief Executive Officer – North Asia Michael Kok & Group Convenience (stepped down on 8th May 2019) Sam Kim Dr Delman Lee Chief Executive Officer – Health & Beauty and Chief Marketing & Business Development Officer Anthony Nightingale Martin Lindström Y.K. -

Sheng Siong Group (SSG SP) SELL Share Price SGD 0.96 Look Elsewhere for Cheaper 12M Price Target SGD 0.85 (-11%) Growth Plays Previous Price Target SGD 0.88

February 27, 2017 Sheng Siong Group (SSG SP) SELL Share Price SGD 0.96 Look elsewhere for cheaper 12m Price Target SGD 0.85 (-11%) growth plays Previous Price Target SGD 0.88 Company Description Maintain SELL; cut TP a further 3% to SGD0.85 Mass-market supermarket operator. Third largest in Maintain SELL post-FY16 results. We find it hard to justify 23x P/E for Singapore by market share. single digit growth, and growth will keep slowing amidst greater traction by online grocers. In our view, Sheng Siong’s operating model is also unsustainable as it depends too much on margin improvement to drive ROE, while asset-use efficiency has deteriorated. With margins close to Statistics peaking and store expansion challenges, growth will remain slow unless 52w high/low (SGD) 1.10/0.84 it is willing to gear up to acquire growth either locally or overseas. But 3m avg turnover (USDm) 2.0 that will certainly change its risk profile. We lower FY17-FY18 EPS Free float (%) 34.9 estimates 3-4% and our DCF-TP 3% to SGD0.85 (WACC 7.1%, LTG 1%). Issued shares (m) 1,504 Market capitalisation SGD1.4B Consumer Staples 4Q/FY16 in line, but uninspiring USD1.0B NP growth over the last five quarters has slowed from >20% YoY a year ago to single digit growth by 3Q16 and just 5.7% in 4Q16. Same store Major shareholders: Sheng Siong Holdings Pte Ltd. 29.9% sales growth (SSSG) ended the year on a weak note. 4Q16 SSSG was flat LIM HOCK ENG 11.3% at +0.2% YoY, mirroring the full year’s 0.2%. -

Bwp Brl Cop Cou Eur Idr Pen Sgd Zar Thb

BWP BRL 4 COP COU EUR IDR PEN ZWL, VND, GRD, AMD, XDR, CVE, MZE, PTE, HNL,NOK,SGD SLL, SKK, MDL, SEK, ROL, CZK, RON, CSK, BGL, GMD, BGN, MKD,SZL, MTL, DZD, AOA,HTG,TPE,HKD,AFA,BHD, AOK,PYG, EUR,AFN, SBD, IQD, UAH, AON,CHE,XAG, JMD, JOD, PGK, MGA,ANG, AOR,BBD, KWD, LAK, THB, AWG,MMK,LRD, LYD,HRK, PAB, NAD, NLG,GEL, RSD, ETB,MWK, NZD,HUF,LVL, VEB,CSD, ZMK, ADF,SGD,ALL, VEF, SDD, AZN,SHP,BOV,ITL,BEF,SRD,BOB,TND, SML,TMM,SDP,ZAR ERN, BIF, TWD,GHC,YUD, VAL,SDG,KMF, NGN,TMT, CRC,YUM,TTD, LTL, CDF, SYP,BTN,DEM, SVC, USD,AED, CYP, TRL, DJF,XAU, BAM,NIC, USS, MAD,EGP, FRF,TRY, MRO, NIO, FIM,USN,FKP, STD,GNF,GBP, DKK, TOP, GIP,MZM, ZWD, AUD, LUF,LSL, XPD,EEK,IEP, MZN, ZWR,MGF, BSD,LBP,AZM, ISK,MOP RWF,BZD,THB BMD,CHF,NTUC XOF,BND, Fairprice, XAF,KYD, XPF,CAD, XFO, XCD, XFU, FJD, CHW,GYD, VND Singapore USD Country : Singapore ISO member body : Standards, Productivity and Innovation Board (SPRING SG) Project team : CNY Leader : Ms. Susan Chong (Director, Special Projects), SPRING SG Member : Mr. Phua Kim Chua (Head, Standards Division), SPRING SG Member : Ms. Ho Buaey Qui (Executive Secretary, NOK Information Technology Standards Committee, Singapore) Member : Ms. Pauline Ping Ting Ting (MBA Student, Nanyang Technological University, Singapore) THB Member : Mr. Preetesh Deora (MBA Student, Nanyang Technological University, Singapore) ISO Central Secretariat advisor : Reinhard Weissinger CNY Duration of the study : October 2010 – March 2011 BRL 4.1 Introduction to the project and overview The key objective of the ISO pilot project is to determine in a quan- titative manner the benefits companies can derive from the use of standards in their business. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases. -

Survey to Understand Consumer Attitudes Toward Food Waste by F&B Companies in Singapore

Report – Survey To Understand Consumer Attitudes Toward Food Waste By F&B Companies In Singapore Survey was conducted by the Chua Thian Poh Community Leadership Programme, National University of Singapore Abstract This study aims to investigate consumer perceptions toward food waste generated by the food and beverage (F&B) sector in Singapore. A survey questionnaire was devised and 428 valid responses were obtained. The results were analysed using SPSS and are presented in the Results section. The key findings of the survey are summarised as follows: 1. More than 90% of the participants are concerned about the food waste generated in Singapore and more than 83% of participants found it unacceptable for F&B companies in Singapore to waste food. 2. Close to 50% of the participants named NTUC FairPrice as a company whose food waste reducing strategy will be of interest to them. The same question yielded approximately 38% of responses for BreadTalk. 3. Participants are most interested in how retail supermarkets handle food waste, with NTUC FairPrice, Cold Storage, Giant and Sheng Siong among the top 10 most named companies. 4. An overwhelming majority of the respondents stated that they want to see F&B companies „donate unsold, excess and near-expiry food that is still safe for consumption to the charities„ (91.1%) and „sell unsold, excess and near- expiry food that is still safe for consumption at a discount‟ (83.6%) in their bid to curb food waste. 5. Participants are willing to support F&B companies which adopt strategies to reduce food waste by helping them spread the word for their efforts (>80%). -

Doing Business in Singapore

Published on 09/04/2020 DOING BUSINESS IN SINGAPORE Brought to you by: KNAV Services LLP, Singapore specialises in assurance (external and internal), taxation, international transfer pricing, valuation and business advisory services. Allinial Global is an association of legally independent accounting and consulting firms who share education, marketing resources, and technical knowledge in a wide range of industries. We're independent accounting firms coming together to support the success of independent client companies. We'll go wherever we need in the world to secure the highest quality solutions to our clients' business needs. Allinial Global member firms have the flexibility to find not just a good solution to your business challenges, but the best solution for you - whether it's locally or internationally. Doing Business in Singapore Introduction CAPITAL: SINGAPORE POPULATION Total Population: 5,638,676 Natural Increase: 0.5% Density: 7,953 Inhabitants/km² Urban Population: 100.0% Population of main cities: Singapore is a city state (5,469,700) Ethnic Origins: About 74% of Chinese origin, 13% of Malay origin, 10% of Indian origin and 3% of other origins. (Statistics Singapore) Official Language: English, Mandarin Chinese, Malay, Tamil. Other Languages Spoken: Hakka, Cantonese, Teochew, other Chinese dialects. Business Language(s): English is the most commonly spoken language. It unites the different ethnic groups and business community. Religion: Buddhism, Islam, Taoism, Hinduism, Christianity and other religious communities, including Jews, Sikhs, Jains, etc. National Currency: Singapore Dollar (SGD) COUNTRY OVERVIEW Area: 719 km² Type of State: Singapore is officially a Republic based on parliamentary democracy. Type of Economy: High-income economy. -

Dairy Farm International Holdings Limited

Annual ReportAnnual 2017 Dairy Farm International Holdings Limited Annual Report 2017 Our Goal : “To give our customers across Asia a store they TRUST, delivering QUALITY, SERVICE and VALUE” Dairy Farm International Holdings Limited is incorporated in Bermuda and has a standard listing on the London Stock Exchange, with secondary listings in Bermuda and Singapore. The Group’s businesses are managed from Hong Kong by Dairy Farm Management Services Limited through its regional offices. Dairy Farm is a member of the Jardine Matheson Group. A member of the Jardine Matheson Group Contents 2 Corporate Information 3 Dairy Farm At-a-Glance 4 Highlights 6 Chairman’s Statement 8 Group Chief Executive’s Review 12 Feature Stories 16 Business Review 16 Food 22 Health and Beauty 26 Home Furnishings 30 Restaurants 34 Financial Review 37 Directors’ Profiles 39 Our Leadership 42 Financial Statements 100 Independent Auditors’ Report 108 Five Year Summary 109 Responsibility Statement 110 Corporate Governance 117 Principal Risks and Uncertainties 119 Shareholder Information 120 Retail Outlets Summary 121 Management and Offices Annual Report 2017 1 Corporate Information Directors Dairy Farm Management Services Limited Ben Keswick Chairman and Managing Director Ian McLeod Directors Group Chief Executive Ben Keswick Neil Galloway Chairman Mark Greenberg Ian McLeod Group Chief Executive George J. Ho Neil Galloway Adam Keswick Group Finance Director Sir Henry Keswick Choo Peng Chee Regional Director, North Asia (Food) Simon Keswick Gordon Farquhar Michael Kok Group Director, Health and Beauty Dr George C.G. Koo Martin Lindström Group Director, IKEA Anthony Nightingale Michael Wu Y.K. Pang Chairman and Managing Director, Maxim’s Jeremy Parr Mark Greenberg Lord Sassoon, Kt Y.K. -

Press Release Ahold to Divest Its Indonesian Operation to Hero

Press Release Royal Ahold Public Relations Date: April 29, 2003 For more information: +31 75 659 57 20 Ahold to divest its Indonesian operation to Hero Zaandam, The Netherlands, April 29, 2003 – Ahold hereby announces that it has reached agreement for the sale of its Indonesian operation to PT Hero Supermarket Tbk for approximately Euro 12 million, excluding proceeds from the sale of store inventory. This asset purchase agreement is subject to the approval of Hero’s shareholders and is expected to be finalized in the third quarter of 2003. Hero is a prominent food retail group listed on the Jakarta stock exchange with 200 outlets throughout Indonesia. The transaction involves 22 stores plus one under construction, and two distribution centers. The actual transfer of the stores and both distribution centers will take place following the approval of Hero shareholders. Staff at Ahold’s Indonesian headquarters are not included in the transaction, although Ahold is committed to meeting its obligations to these associates. The divestment of Ahold’s activities in Indonesia is part of the company’s strategic plan to restructure its portfolio to focus on high-performing businesses, to concentrate on its mature and most stable markets and to reduce its debt. Ahold first entered the Indonesian market through a technical service agreement with the PSP group in 1996. That agreement ended in 2002 and Ahold Tops Indonesia became a wholly-owned subsidiary. Unaudited net sales in 2002 amounted to approximately Euro 37 million. Ahold employs approximately 1,600 people in Indonesia. Ahold Corporate Communications: +31.75.659.5720 ------------------------------------------------------------------------------------------------------------------------------------------------------------ Certain statements in this press release are “forward-looking statements” within the meaning of U.S. -

1 Participating Merchants Address/Website Postal Code

PARTICIPATING ADDRESS/WEBSITE POSTAL MERCHANTS CODE 430 UPPER CHANGI ROAD #01-47/48/49 EAST VILLAGE 487048 16 ENG GOR STREET #01-05/08 79717 12 KALLANG AVENUE APERIA #01/51 339511 442, ORCHARD ROAD B1-01-11 238879 896 DUNEARM ROAD #02-01 SIME DARBY CENTRAL 589472 1 SENGKANG SQUARE #B1-25 COMPASS ONE 545078 176 ORCHARD ROAD #B1-09/10 CENTRE POINT 238843 21 TAMPINES NORTH DRIVE 2 #03-01 528765 5 STRAITS VIEW #B2-15/16, MARINA ONE, THE HEART 18935 41 SUNSET WAY #01-01A CLEMENTI ARCADE 597071 1 FUSIONOPOLIS WAY #B2-03 CONNEXIS 138632 101 THOMSON ROAD #B1-52 307591 NO 238 THOMSON ROAD #01-28/29 307683 293 HOLLAND ROAD #01-01 JELITA SHOPPING CENTRE 278628 211 HOLLAND AVENUE #01-02,04,05 HOLLAND 278967 SHOPPING CTR 154 WEST COAST ROAD B1-19, WEST COAST PLAZA 127371 501 BUKIT TIMAH ROAD CLUNY COURT #01-02 259760 80 MARINE PARADE ROAD #B1-84 PARKWAY PARADE 449269 5 STADIUM WALK #B1-01/05 LEISURE PARK 397693 10 TAMPINES CENTRAL 1 TAMPINES 1 #B1-01/02 529536 464-486 JALAN ASAS UPPER BUKIT TIMAH ROAD 678077 NO 1 WOODLANDS SQUARE #B1-31/32/33 CAUSEWAY COLD STORAGE 738099 POINT 1 MARITIME SQUARE #01-48 TO 50 99253 20 GREENWOOD AVE 289215 930 YISHUN AVENUE 2 #B1-11 TO 16 NORTHPOINT 769098 SHOPPING CENTRE 383 BUKIT TIMAH RD #01-09A ALOCASSIA APARTMENT 259727 23 SERANGOON CENTRAL #B2-44/45 NEX 556083 1 SELETAR ROAD #01-11 GREENWICH V 807011 1 COVE AVENUE SENTOSA ARRIVAL PLAZA #02-07/10 98537 101 CLEMENTI ROAD #01-01 KENT VALE ESTATE 179787 1 VISTA EXCHANGE GREEN #B1-02 & 35/36 THE STAR 138617 VISTA 2 FIRST STREET #01-05/06/12/13/14/15/16 SIGLAP V 458278