2008 Top 100 For-Hire Carriers List

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NSIAD-90-50 Household Goods: Competition Among Commercial

4 United States General Accounting Office Report to the Chairman, Legislation GAO and National Security Subcommittee, Committee on Government Operations, House of Representatives HOUSEHOLD GOODS Competition Among Commercial Movers Serving DOD Can Be Improved National Security and International Affairs Division B-23767 1 February 12,199O The Honorable John Conyers, Jr. Chairman, Legislation and National Security Subcommittee Dear Mr, chairman: This report responds to a request by the former Subcommittee Chairman that we review the practices and procedures of the Department of Defense in procuring commercial household goods shipping services for personnel being transferred at government expense between duty stations within the United States. Unless you publicly announce its contents earlier, we plan no further distribution of this report for 30 days. At that time, we will send copies to the Secretaries of Defense, the Army, the Navy, and the Air Force; the Chairmen, House and Senate Committees on Armed Services and on Appropriations; the Director, Office of Management and Budget; and to other interested parties. This report was prepared under the direction of Richard Davis, Director, Army Issues, who may be reached at (202) 275-4141 if you or your staff have any questions. GAOstaff members who made major contributions to this report are listed in appendix IV. Sincerely yours, Frank C. Conahan Assistant Comptroller General ljxecutive Summary The Department of Defense spends over $400 million dollars a year to Purpose ship and store the household goods of its members authorized to make a transfer or to relocate within the 48 contiguous United States. The money is paid to commercial household goods carriers and their agents located throughout the United States. -

Annual Report 2020

Annual Report 2020 Wells Fargo Bank, N.A. Collective Investment Funds Table of Contents Page Independent Auditors’ Report 1 Financial Statements: Wells Fargo/Causeway International Value CIT 3 Wells Fargo/Dodge & Cox Intermediate Bond CIT 10 Wells Fargo/Federated Total Return Bond CIT 20 Wells Fargo/Lazard International Equity CIT 36 Wells Fargo/MFS Value CIT 44 Wells Fargo/Multi-Manager Small Cap CIT 51 Wells Fargo/T. Rowe Price Institutional Equity Income Managed CIT 65 Wells Fargo/T. Rowe Price Institutional Large-Cap Growth Managed CIT 73 Wells Fargo/Voya Large-Cap Growth CIT 79 Notes to Financial Statements 85 Appendix 97 Regulatory Statement 101 KPMG LLP Two Financial Center 60 South Street Boston, MA 02111 Independent Auditors’ Report The Unitholders of the Funds and Wells Fargo Bank, N.A.: We have audited the accompanying financial statements of Wells Fargo/Causeway International Value CIT, Wells Fargo/Dodge & Cox Intermediate Bond CIT, Wells Fargo/Federated Total Return Bond CIT, Wells Fargo/Lazard International Equity CIT, Wells Fargo/MFS Value CIT, Wells Fargo/Multi-Manager Small Cap CIT, Wells Fargo/T. Rowe Price Institutional Equity Income Managed CIT, Wells Fargo/T. Rowe Price Institutional Large-Cap Growth Managed CIT and Wells Fargo/Voya Large-Cap Growth CIT (collectively, the Funds), nine of the collective investment funds constituting Wells Fargo Bank Collective Investment Funds for Employee Benefit Trusts, which comprise the statements of assets and liabilities, including the schedules of investments, as of December 31, 2020, and the related statements of operations, changes in net assets, and the financial highlights for the year or periods then ended, and the related notes to the financial statements. -

Mediocreat Best

MEDIOCRE AT BEST The CCJ Top 250’s specialized carriers fared best – and worst – in 2007. But most general freight carriers saw anemic growth – or none at all. BY AVERY VISE t the time, most trucking Three carriers that were in A widespread slowdown companies probably saw last year’s CCJ Top 250 – No. The CCJ Top 250’s growth slowed A2007 as fairly miserable – 67 Performance Transportation further in 2007. Revenues grew 3.9 soft freight demand, ample capacity Services, No. 88 Jevic Transportation percent, down from the 9 percent and high fuel prices. Diesel averaged and No. 248 Alvan Motor Freight – increase recorded the year before and $2.89 a gallon in 2007, rising steadily ceased operations this year and so the 16.1 percent rise in 2005 over throughout the year from a low have been dropped from this year’s 2004. For LTL and truckload gen- of $2.41 in January to an unprec- CCJ Top 250. Fuel wasn’t the lone eral freight carriers – the majority of edented $3.44 by late November. culprit. For example, the troubled the CCJ Top 250 – 2007 was truly a For many, those were the good old automobile industry contributed to lackluster year. In fact, 2007 was just days. Today’s diesel prices are more the demise of Alvan Motor Freight another 2006 for LTL carriers, which than 35 percent higher than even the and car hauler PTS, which shut saw no change in revenues. Truckload highest average price during 2007. down in bankruptcy principally due general freight carriers posted a 3.3 Escalating prices coupled with the lag to a Teamsters strike. -

Ferguson LTL Carrier Contacts.Xlsx

Mode Managed Transportation Center 17330 Preston Road 200c Updated 1/10/2019 Dallas TX 75252 www.modetransportation.com Mode Transportation Contacts Mode Transportation Main [email protected] 833-235-6208 Transportation Manager Jane McDaniel [email protected] O: 214-445-5226 C: 214-213-7430 Accounts Payable/Billing Charles Cabral [email protected] O: 214-445-5224 C: 469-439-7088 SCAC Carrier Carrier Website PYLE A DUIE PYLE INC https://www.aduiepyle.com/ AACT AAA COOPER TRANSPORTATION http://www.aaacooper.com/ ABFS ABF FREIGHT SYSTEM INC https://arcb.com/abf-freight BEAV BEAVER EXPRESS www.beaverexpress.com/ CENF CENTRAL FREIGHT LINES INC. http://www.centralfreight.com/ CNWY CONWAY/XPO http://www.con-way.com/ DAFG DAYTON FREIGHT LINES, INC. https://www.daytonfreight.com/ DPHE DEPENDABLE HIGHWAY http://www.godependable.com/ EXLA ESTES EXPRESS LINES https://www.estes-express.com/ FXFE FEDEX FREIGHT https://www.fedexfreight.fedex.com/ JJKQ JACK JONES TRUCKING http://www.jjtinc.com/ LKVL LME https://www.lme4me.com/ NPME NEW PENN https://www.newpenn.com/ NOPK NORTHPARK http://nopk.com/ OAKH OAK HARBOR FREIGHT LINES http://www.oakh.com/ ODFL OLD DOMINION FREIGHT LINES https://www.odfl.com/ PENS PENINSULA http://www.peninsulatruck.com/ PITD PITT OHIO EXPRESS INC. https://works.pittohio.com/ RLCA R & L CARRIERS https://www2.rlcarriers.com/ RETL REDDAWAY http://www.reddawayregional.com/ SAIA SAIA MOTOR FREIGHT LINE INC https://www.saia.com/ SEFL SOUTHEASTERN FREIGHT LINES https://www.sefl.com/ -

Freight Assessment Blueprint Practical Guide for Evaluating Freight Transportation in Support of National Green Freight Programs

WHITE PAPER MARCH 2017 FREIGHT ASSESSMENT BLUEPRINT PRACTICAL GUIDE FOR EVALUATING FREIGHT TRANSPORTATION IN SUPPORT OF NATIONAL GREEN FREIGHT PROGRAMS Ben Sharpe www.theicct.org [email protected] BEIJING | BERLIN | BRUSSELS | SAN FRANCISCO | WASHINGTON ACKNOWLEDGMENTS This work is supported by the Climate and Clean Air Coalition and the U.S. Environmental Protection Agency. The critical reviews of Cristiano Façanha, Oscar Delgado, and Rachel Muncrief of the ICCT were very valuable. In addition, we are very grateful for the feedback provided by Buddy Polovick (U.S. EPA), Melissa Sutherland (Natural Resources Canada), and Alvin Mejia (Clean Air Asia). International Council on Clean Transportation 1225 I Street NW Suite 900 Washington, DC 20005 USA [email protected] | www.theicct.org | @TheICCT © 2017 International Council on Clean Transportation FREIGHT ASSESSMENT BLUEPRINT TABLE OF CONTENTS 1. Introduction .............................................................................................................................1 2. How to conduct a freight assessment ................................................................................4 3. What to include in a freight assessment ...........................................................................9 3.1 Roles and trends of trucking, shipping, and rail .................................................................. 9 3.2 Freight trucks and trailers sales market.................................................................................12 3.3 -

North American Commercial Vehicle Show the Fleet Technology Showcase

September 27-30, 2021 Georgia World Congress Center, Atlanta North American Commercial Vehicle Show The Fleet Technology Showcase The North American Commercial Vehicle (NACV) Show, the premier biennial B2B trucking industry event focusing on the needs of fleet owners, managers and decision makers, is North America’s largest and most comprehensive commercial vehicle trade show for fleets. North America is the world’s largest market for commercial vehicles with over 141 million vehicles in use across the continent. We are committed to serving the needs of this market and continuing to nurture its vital role in global commercial activity. Kyle Behnke, CEO & Owner, United Federal Logistics, Inc. “The NACV Show put all of the major manufacturers in one room and let us compare all of their new technology, apples to apples. That, and the people we met, helped us drive our truck-buying decision in the following year. We ended up buying 13 trucks, which for a small fleet like ours, was huge.” NACV Show 2017 by the numbers 439 370,000 234 6,000 exhibitors sq. ft. of exhibits accredited international journalists unique visitors NACV Show 2017 Attendees*: 93% rated the show as good or great had plans to purchase products or services 82% they saw on display at NACV Show 2017 planned to purchase from a new supplier after 63% the show were able to see all the products and services 89% they wanted to experience 95% indicated they were planning to attend in 2019 *Based on NACV Show 2017 attendee post-show survey. nacvshow.com Why NACV Show 2021? The NACV Show brings together fleets of ALL sizes, including the biggest and best, with a full range of industry products and services. -

Origin State LTL Carrier / PH# Origin State LTL Carrier / PH# Alabama Fedex Freight Economy / 1.800.463.3339 Montana Fedex Freight Economy / 1.800.463.3339

SRC Electrical 2/16/2018 LTL Routing Guide US Shipments Weight Routing Instructions FedEx Ground: All freight that falls within the FedEx Ground guidelines up to < 150# 150#. No single carton is to exceed 70#. Multiple carton shipments must be combined into single‐carton shipments when possible. 151‐8000# See LTL Routing Guide Below Contact SRC Electrical Materials Manager for routing instructions. Dewayne >8000# Ipock 417.851.6212 Origin State LTL Carrier / PH# Origin State LTL Carrier / PH# Alabama FedEx Freight Economy / 1.800.463.3339 Montana FedEx Freight Economy / 1.800.463.3339 Alaska FedEx Priority / 1.800.463.3339 Nebraska SAIA / 1.800.765.7242 Arizona FedEx Freight Economy / 1.800.463.3339 Nevada FedEx Freight Economy / 1.800.463.3339 Arkansas SAIA / 1.800.765.7242 New Hampshire FedEx Freight Economy / 1.800.463.3339 California FedEx Freight Economy / 1.800.463.3339 New Jersey FedEx Freight Economy / 1.800.463.3339 Colorado FedEx Freight Economy / 1.800.463.3339 New Mexico FedEx Freight Economy / 1.800.463.3339 Connecticut FedEx Freight Economy / 1.800.463.3339 New York FedEx Freight Economy / 1.800.463.3339 Delaware FedEx Freight Economy / 1.800.463.3339 North Carolina Estes Express / 1.877.268.4555 Florida FedEx Freight Economy / 1.800.463.3339 North Dakota SAIA / 1.800.765.7242 Georgia FedEx Freight Economy / 1.800.463.3339 Ohio Dayton / 1.800.860.5102 Hawaii FedEx Priority / 1.800.463.3339 Oklahoma SAIA / 1.800.765.7242 Idaho FedEx Freight Economy / 1.800.463.3339 Oregon FedEx Priority / 1.800.463.3339 Illinois Dayton / -

Domestic Customer Service Index Scores Effective November 1, 2010

DOMESTIC CUSTOMER SERVICE INDEX SCORES EFFECTIVE NOVEMBER 1, 2010 AAAA AAAA FORWARDING, INC. Unindexed AAIM AACTION MOVING & STORAGE Unindexed AAPG AAA PRO MOVING & STORAGE Unindexed AARV AARO MOVING SYSTEMS, INC. 101.82 AASH AAA MOVING & STORAGE Unindexed AAVH ALL AMERICAN MOVING SERVICES Unindexed AAVP AMERICAN VANPAC CARRIERS, INC. Unindexed ACMH ACME MOVING & STORAGE Unindexed ADIM ADRIANA INTERNATIONAL Unindexed ADMV ADVANCE CORPORATION Unindexed ADOL AMBASSADOR RELOCATIONS INC Unindexed AEQL ACCESS RELOCATION Unindexed AERM MAYFLOWER TRANSIT, LLC 94.30 AFDG ATLAS FORWARDING, INC. Unindexed AFFH AMERICAN FAST FREIGHT INC Unindexed AFIW PASHA GROUP DBA AFI/PASHA WORLDWIDE Unindexed AFTS AFFILIATED TRANSPORTATION SYST Unindexed AIGP ARPIN INTERNATIONAL GROUP Unindexed ALDS ALEXANDERS MOVING & STORAGE Unindexed ALIS ALLISON WAREHOUSE Unindexed ALLV ALLIED VAN LINES 97.93 ALRQ ALL AMERICA RELOCATION, INC. 102.43 AMRB AMERICAN RED BALL Unindexed ANBP A & B TRANSPORTATION SERVICES Unindexed ANVL ANDREWS VAN LINES, INC. Unindexed AOFA A-1 FREEMAN NORTH AMERICAN Unindexed APMT ALL PRO MOVING & TRANSFER Unindexed APVA APPLE TRANSFER, INC. Unindexed APVN APACA VAN LINES INC Unindexed ARCA ACE RELOCATION SYSTEMS, INC. Unindexed ARMT ARMSTRONG RELOCATION CO. 101.55 ARNA A. ARNOLD WORLD CLASS RELOCATION 91.80 ARPV ARPIN VAN LINES, INC. 96.67 ARSG ARMSTRONG MOVING Unindexed ATVL ATLAS VAN LINES INC 100.59 AVAS AMERICAN VAN SERVICE, INC. Unindexed AZMC AZTEC MOVING Unindexed BAIP PARKER K. BAILEY & SONS, INC. Unindexed BAMO BARNES MOVING & STORAGE CO. Unindexed BAMQ BALLARD MOVING AND STORAGE Unindexed BARK BARKLEY TRUCK LINES, INC. Unindexed BBAF B & B MOVERS, INC. Unindexed BBMS BRANTLEY BROTHERS MOVING Unindexed BEKM BEKINS A-ONE MOVERS Unindexed BEKS BEKINS NORTHWEST Unindexed BEMJ BEMIDJI TRANSFER, INC. -

Third Quarter Ended September 30, 2020 Forward-Looking Statements

Third Quarter Ended September 30, 2020 Forward-Looking Statements In the interest of providing shareholders and potential investors with information regarding TFI International, including management’s assessment of future plans and operations, certain statements in this presentation are forward-looking statements subject to risks, uncertainties and other important factors that could cause the Company’s actual performance to differ materially from those expressed in or implied by such statements. Such factors are further discussed under Risks and Uncertainties in the Company’s Annual Information Form and MD&A, but readers are cautioned that the list of factors that may affect future growth, results and performance is not exhaustive, and undue reliance should not be placed on forward- looking statements. The expectations conveyed by the forward-looking statements are based on information available to it on the date such statements were made, and there can be no assurance that such expectations will prove to be correct. All subsequent forward-looking statements, whether written or orally attributable to the Company or persons acting on its behalf, are expressly qualified in their entirety by these cautionary statements. Unless otherwise required by applicable securities laws, the Company expressly disclaims any intention, and assumes no obligation, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. 2 TFI International: Who We Are Diversified: Full service: Package & Courier, -

Volvo Trucks' Customer Saia Takes Delivery of Two Volvo VNR Electrics

VOLVO TRUCKS Press Information Volvo Trucks’ Customer Saia Takes Delivery of Two Volvo VNR Electrics Saia LTL Freight, a leading national transportation and logistics provider founded in 1924, recently took delivery of two Volvo VNR Electric trucks at its facility in Los Angeles, California. The VNR Electrics from Volvo Trucks North America are the first zero tailpipe emission, battery-electric Class 8 trucks to be deployed in Saia’s fleet, which provides regional freight distribution services throughout Southern California, as well as logistics services across the U.S., Canada, Puerto Rico, and Mexico. The Volvo VNR Electric trucks being leased to Saia by Volvo Financial Services (VFS) are part of the Volvo LIGHTS project, an innovative collaboration between Volvo Trucks North America, the South Coast Air Quality Management District (South Coast AQMD), and 12 other organizations, to develop a blueprint to successfully introduce battery-electric trucks and equipment into the North American transport industry at scale. The project includes a total of 17 leased VNR Electrics being placed into Southern California fleet operations. “Volvo Trucks is pleased that Saia has chosen the VNR Electric as its first battery-electric model for regional freight transportation. We are excited to partner with their team on this important first step toward fleet electrification and look forward to delivering the quality and reliability Saia requires to scale their zero-emission fleet in the future,” said Peter Voorhoeve, president, Volvo Trucks North America. “Through the Volvo LIGHTS project and the commercial launch of the VNR Electric, we have developed a robust service model to provide our customers with full support—from funding and financing options from VFS to vehicle procurement, infrastructure planning and installation, and regular maintenance schedules to maximize uptime.” “Commercialization of these cleaner technologies is a big part of the solution for cleaner air,” said Wayne Nastri, South Coast AQMD’s executive officer. -

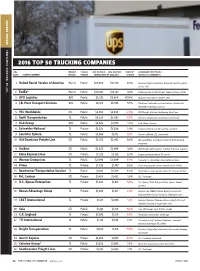

2016 Top 50 Trucking Companies 2016 Top 50 Trucking Companies

SPECIAL REPORT SPECIAL 2016 TOP 50 TRUCKING COMPANIES 2016 TOP 50 TRUCKING COMPANIES 2016 PRIMARY PUBLIC/ 2015 REVENUE 2016 REVENUE PERCENT SUBSIDIARY PORTFOLIO / RANK PARENT COMPANY SERVICE PRIVATE (IN MILLIONS OF DOLLARS) CHANGE SERVICES & COMMENTS 1 United Parcel Service of America Parcel Public $29,829 $31,770 6.5% Ground, freight, brokerage. Acquired Coyote Logistics in July 2015 TOP 50 TRUCKING COMPANIES TRUCKING 50 TOP 2 FedEx* Parcel Public $20,307 $22,127 9.0% FedEx Ground, FedEx Freight, FedEx Custom Critical 3 XPO Logistics IMC Public $3,273 $6,860 109.6% Acquired Con-way in October 2015 4 J.B. Hunt Transport Services IMC Public $6,188 $6,555 5.9% Truckload, dedicated contract service, intermodal, integrated capacity solutions 5 YRC Worldwide LTL Public $4,832 $4,698 -2.8% YRC Freight, Holland, Reddaway, New Penn 6 Swift Transportation TL Public $4,229 $4,032 -4.7% Dry-van, refrigerated, dedicated, nntermodal 7 Hub Group IMC Public $3,526 $3,573 1.3% Hub, Mode, Unyson 8 Schneider National TL Private $3,423 $3,506 2.4% Largest privately owned trucking company 9 Landstar System TL Public $3,364 $3,172 -5.7% Dry-van, flatbed, LTL, intermodal 10 Old Dominion Freight Line LTL Public $2,972 $2,992 0.6% Most profitable asset-based publicly held trucking company 11 ArcBest LTL Public $2,422 $2,496 3.0% ABF Freight, ABF Logistics, Panther Premium Logistics 12 Estes Express Lines LTL Private $2,135 $2,155 0.9% Largest privately owned LTL carrier 13 Werner Enterprises TL Public $2,094 $2,009 -4.0% One-way TL, dedicated, value-added services 14 Prime TL Private $1,736 $1,747 0.6% Prime Refrigerated, Prime Flatbed, Prime Tanker 15 Roadrunner Transportation Services TL Public $1,610 $1,709 6.2% Truckload revenue growth offset LTL revenue decline 16 R+L Carriers LTL Private $1,429 $1,452 1.6% LTL, Truckload 17 U.S. -

Automated Commercial Motor Vehicle Working Group Report

Commercial Vehicle Safety Alliance— Automated Commercial Motor Vehicle Working Group In partnership with Final Report Submitted by MaineWay Services, with the support of Cambridge Systematics, Inc. October 2019 (Updated September 2020) Automated CMV Working Group – Final Report Table of Contents Executive Summary ................................................................................................................................... 1 1.0 Introduction ...................................................................................................................................... 1 2.0 Background ...................................................................................................................................... 5 3.0 Stakeholder Outreach and Input ..................................................................................................41 4.0 Creating a Decision Tree for ADS-Equipped CMV Identification ..............................................45 5.0 Recommendations and Next Steps .............................................................................................48 6.0 Items for Future Consideration ....................................................................................................56 Appendix A. CVSA NAS Level I Inspection—Gap Analysis Matrix ................................................. A-1 Appendix B. Working Group Inspection Options Survey ................................................................ B-1 i Automated CMV Working Group – Final Report List of