Results for the Six Months Ended 30 June

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MEGA Khimki Tver Region Market Overview Welcome

MEGA Khimki Tver region Market overview Welcome Dmitrov L e y n Sergiev-Posad Catchment areas People Distance i w y n h to MEGA Khimki Klin g w r a e h V Vladimir d o ol s e o k ko k o region la o s k m e v s Pushkin s Mytischi ko h o av e w r sl t Schelkovo y i o h . r a w m y Y Primary 398,200 < 17 km D Zheleznodorozhny M K A Smolensk Moscow D Balashikha region Podolsk Naro-Fominsk Secondary 1,424,200 17–40 km Krasnogorsk y Klimovsk v hw hw uziasto oe y nt RUSSIA’S FIRST IKEA WAS OPENED IN sk E Obninsk izh Kolomna or Reutov Tertiary 3,150,656 40–140 km ov KHIMKI IN 2000. MEGA KHIMKI SOON N Serpukhov FOLLOWED IN 2004 AND BECAME THE Kaluga region LARGEST RETAIL COMPLEX IN RUSSIA Tula region Total area: 4,973,000 AT THE TIME. Odintsovo N o v o ry y a hw z e a ko n s sk Min o e wy h h w oe y vsk Kie Despite several new retail centres opening their doors along the Leningradskoe Shosse, y y w w h MEGA Khimki remains one of the district’s h e oe o sk k most popular shopping destinations, largely s h Troitsk z Scherbinka v u a al due to its location, well-designed layout and K h s r retail mix. a V Domodedovo New tenants and constant improvements to the centre have significantly increased customer numbers. -

Industrial Framework of Russia. the 250 Largest Industrial Centers Of

INDUSTRIAL FRAMEWORK OF RUSSIA 250 LARGEST INDUSTRIAL CENTERS OF RUSSIA Metodology of the Ranking. Data collection INDUSTRIAL FRAMEWORK OF RUSSIA The ranking is based on the municipal statistics published by the Federal State Statistics Service on the official website1. Basic indicator is Shipment of The 250 Largest Industrial Centers of own production goods, works performed and services rendered related to mining and manufacturing in 2010. The revenue in electricity, gas and water Russia production and supply was taken into account only regarding major power plants which belong to major generation companies of the wholesale electricity market. Therefore, the financial results of urban utilities and other About the Ranking public services are not taken into account in the industrial ranking. The aim of the ranking is to observe the most significant industrial centers in Spatial analysis regarding the allocation of business (productive) assets of the Russia which play the major role in the national economy and create the leading Russian and multinational companies2 was performed. Integrated basis for national welfare. Spatial allocation, sectorial and corporate rankings and company reports was analyzed. That is why with the help of the structure of the 250 Largest Industrial Centers determine “growing points” ranking one could follow relationship between welfare of a city and activities and “depression areas” on the map of Russia. The ranking allows evaluation of large enterprises. Regarding financial results of basic enterprises some of the role of primary production sector at the local level, comparison of the statistical data was adjusted, for example in case an enterprise is related to a importance of large enterprises and medium business in the structure of city but it is located outside of the city border. -

Appendix 2: Q4 (Oct-Dec) 2020 Cities in Russia Top Mobile Internet Providers Based on Average Download and Top 10% Speeds of Speedtest Intelligence Data

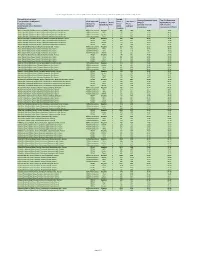

Appendix 2: Q4 (Oct-Dec) 2020 Cities in Russia Top Mobile Internet Providers based on average download and top 10% speeds of Speedtest Intelligence data City and Location Name Sample Average Download Speed Top 10% Download from Speedtest Intelligence / Claim Approved CoUnt / Test CoUnt / Provider / Rank / (Mbps) / Speed (Mbps) / Топ Название города, /Заявление Число Число Провайдер Ранг Средняя скорость 10% скорость местоположения из Speedtest одобрено точек замеров скачивания скачивания (Мбит/с) Intelligence замеров Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия All/Все технологии MegaFon 1 468 1369 34.89 79.85 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия All/Все технологии MTS 2 227 612 23.35 48.91 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия All/Все технологии Beeline 3 125 516 18.92 34.17 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия All/Все технологии Tele2 4 204 571 18.60 41.73 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия LTE/4G MegaFon 1 439 1257 35.61 79.35 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия LTE/4G MTS 2 205 491 24.35 49.98 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия LTE/4G Beeline 3 113 430 20.07 34.29 Abakan, Republic of Khakassia, Russia / Абакан, Республика Хакасия, Россия LTE/4G Tele2 4 192 527 19.17 43.24 AksaY, Rostov Oblast, Russia / Аксай, Ростовская обл., Россия All/Все технологии MegaFon 1 207 417 28.17 -

Moscow Central Diameters Mega Project for the Immediate Future

Московские центральные диаметры – мегапроект ближайшего будущего Moscow Central Diameters Mega project for the immediate future Suburban train diameter routes will connect radial routes and offer higher quality transport services for 8.2 million residents of Moscow and the Moscow Region. The first two diameters will be launched in 2019–2020. MOSCOW CENTRAL DIAMETERS – THE SURFACE METRO FOR MOSCOW AND THE MOSCOW REGION All over the world, suburban trains are becoming part of the metro system. We have a similar vision. Our plan is to build cross-cutting diameters lines, enabling suburban commuters to transit through the entire city without exiting at railway stations, travelling with the same speed, frequency, and comfort that the metro offers and with the same ticket used for both the metro and suburban train. Sergei Sobyanin Moscow Mayor 38 39 MCD1: Одинцово-Лобня MCDs – THE SURFACE METRO MCD FEATURES1 Passenger traffic, mln Passenger seats, Length, km Stations Transfer points passengers per year thousand per day FOR MOSCOW AND MCD2: Нахабино – Подольск The first stage involves the establishment of two MCD routes: THE MOSCOW REGION • MCD1: Smolensko-Savelovsky (Odintsovo – Lobnya) • MCD2: Kursko-Rizhsky (Nakhabino – Podolsk) The project will be jointly implemented by the Ministry of Transport of the Russian Federation, JSC RZD (Russian Railways), the Moscow Government, the Moscow Region Government, and the passenger carrier JSC Central Exurban Passenger Company. MCD1 52 28 12 42.9 403 MCD2 80 38 15 48.6 486 Stage 1 MCD3 MCD1 446 km MCD6 -

CRR) of Moscow Region, Start-Up Complex № 4

THE CENTRAL RING ROAD OF MOSCOW REGION INFORMATION MEMORANDUM Financing, construction and toll operation of the Central Ring Road (CRR) of Moscow Region, start-up complex № 4 July 2014, Moscow Contents Introduction 3–4 Project goals and objectives 5–7 Relevance of building the Central Ring Road Timeline for CRR project implementation Technical characteristics Brief description 8–34 Design features Cultural legacy and environmental protection Key technical aspects Concession agreement General provisions 34–37 Obligations of the concessionaire Obligations of the grantor Project commercial structure 38–46 Finance. Investment stage Finance. Operation stage Risk distribution 47–48 Tender criteria 49 Preliminary project schedule 50 The given information memorandum is executed for the purpose of acquainting market players in good time with information about the given project and the key conditions for its implementation. Avtodor SC reserves the right to amend this memorandum. 2 Introduction The investment project for construction and subsequent toll operation of the Central Ring Road of the Moscow Region A-113 consists of five Start-up complexes to be implemented on a public-private partnership basis. Start-up complex No. 4 of the Central Ring Road (the Project or SC No.4 of the CRR) provides for construction of a section of the CRR in the south-east of the Moscow Region, stretching from the intersection with the M-7 Volga express highway currently under construction to the intersection with the M-4 public highway. Section SC No. 4 of the CRR was distinguished as a separate investment project because the given section is of major significance both for the Region and for the economy of the Russian Federation in general. -

As of June 30, 2018

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint-stock company) Issuer code: 0 1 4 8 1 – В as 3 0 0 6 2 0 1 8 of (indicate the date on which the list of affiliates of the joint-stock company was compiled) Address of the issuer: 19, Vavilova St., Moscow 117997 (address of the issuer – the joint-stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint-stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Deputy Chairperson of the Executive Board of Sberbank B. Zlatkis (position of the authorized individual of the joint-stock company) (signature) (initials, surname) L.S. “ 03 ” July 20 18 . Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 0 0 6 2 0 1 8 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint- the affiliate indicated only with the consent of became valid the joint-stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 Entity may manage more than The Central Bank of the Russian 12, Neglinnaya St., Moscow 20% of the total number of votes 1 21.03.1991 50.000000004 52.316214 Federation 107016 attached to voting shares of the Bank 1. -

List of Cities in Russia

Population Population Sr.No City/town Federal subject (2002 (2010 Census (preliminary)) Census) 001 Moscow Moscow 10,382,754 11,514,330 002 Saint Petersburg Saint Petersburg 4,661,219 4,848,742 003 Novosibirsk Novosibirsk Oblast 1,425,508 1,473,737 004 Yekaterinburg Sverdlovsk Oblast 1,293,537 1,350,136 005 Nizhny Novgorod Nizhny Novgorod Oblast 1,311,252 1,250,615 006 Samara Samara Oblast 1,157,880 1,164,896 007 Omsk Omsk Oblast 1,134,016 1,153,971 008 Kazan Republic of Tatarstan 1,105,289 1,143,546 009 Chelyabinsk Chelyabinsk Oblast 1,077,174 1,130,273 010 Rostov-on-Don Rostov Oblast 1,068,267 1,089,851 011 Ufa Republic of Bashkortostan 1,042,437 1,062,300 012 Volgograd Volgograd Oblast 1,011,417 1,021,244 013 Perm Perm Krai 1,001,653 991,530 014 Krasnoyarsk Krasnoyarsk Krai 909,341 973,891 015 Voronezh Voronezh Oblast 848,752 889,989 016 Saratov Saratov Oblast 873,055 837,831 017 Krasnodar Krasnodar Krai 646,175 744,933 018 Tolyatti Samara Oblast 702,879 719,514 019 Izhevsk Udmurt Republic 632,140 628,116 020 Ulyanovsk Ulyanovsk Oblast 635,947 613,793 021 Barnaul Altai Krai 600,749 612,091 022 Vladivostok Primorsky Krai 594,701 592,069 023 Yaroslavl Yaroslavl Oblast 613,088 591,486 024 Irkutsk Irkutsk Oblast 593,604 587,225 025 Tyumen Tyumen Oblast 510,719 581,758 026 Makhachkala Republic of Dagestan 462,412 577,990 027 Khabarovsk Khabarovsk Krai 583,072 577,668 028 Novokuznetsk Kemerovo Oblast 549,870 547,885 029 Orenburg Orenburg Oblast 549,361 544,987 030 Kemerovo Kemerovo Oblast 484,754 532,884 031 Ryazan Ryazan Oblast 521,560 -

City Abakan Achinsk Almetyevsk Anapa Arkhangelsk Armavir Artem Arzamas Astrakhan Balakovo Barnaul Bataysk Belaya Kholunitsa Belg

City Moscow Abakan Achinsk Almetyevsk Anapa Arkhangelsk Armavir Artem Arzamas Astrakhan Balakovo Barnaul Bataysk Belaya Kholunitsa Belgorod Berdsk Berezniki Biysk Blagoveshensk Bor Bolshoi Kamen Bratsk Bryansk Cheboksary Chelyabinsk Cherepovets Cherkessk Chita Chuvashiya Region Derbent Dimitrovgrad Dobryanka Ekaterinburg Elets Elista Engels Essentuki Gelendzhik Gorno-Altaysk Grozny Gubkin Irkutsk Ivanovo Izhevsk Kaliningrad Kaluga Kamensk-Uralsky Kamyshin Kaspiysk Kazan - Innopolis Kazan - metro Kazan - over-ground Kemerovo Khabarovsk Khanty-Mansiysk Khasavyurt Kholmsk Kirov Kislovodsk Komsomolsk-na- Amure Kopeysk Kostroma Kovrov Krasnodar Krasnoyarsk area Kurgan Kursk Kyzyl Labytnangi Lipetsk Luga Makhachkala Magadan Magnitogorsk Maykop Miass Michurinsk Morshansk Moscow Airport Express Moscow area (74 live cities) Aprelevka Balashikha Belozerskiy Bronnitsy Vereya Vidnoe Volokolamsk Voskresensk Vysokovsk Golitsyno Dedovsk Dzerzhinskiy Dmitrov Dolgprudny Domodedovo Drezna Dubna Egoryevsk Zhukovskiy Zaraysk Zvenigorod Ivanteevka Istra Kashira Klin Kolomna Korolev Kotelniki Krasnoarmeysk Krasnogorsk Krasnozavodsk Krasnoznamensk Kubinka Kurovskoe Lokino-Dulevo Lobnya Losino-Petrovskiy Lukhovitsy Lytkarino Lyubertsy Mozhaysk Mytischi Naro-Fominsk Noginsk Odintsovo Ozery Orekhovo-Zuevo Pavlovsky-Posad Peresvet Podolsk Protvino Pushkino Pushchino Ramenskoe Reutov Roshal Ruza Sergiev Posad Serpukhov Solnechnogorsk Old Kupavna Stupino Taldom Fryazino Khimki Khotkovo Chernogolovka Chekhov Shatura Schelkovo Elektrogorsk Elektrostal Elektrougli Yakhroma -

List of Affiliates

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint stock company) Issuer code: 0 1 4 8 1 – V as 3 1 1 2 2 0 1 9 of (indicate the date on which the list of affiliates of the joint stock company was compiled) Address of the issuer: 117997, Moscow, 19 Vavilova St. (address of the issuer – the joint stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Deputy Chairman of the Executive Board of Sberbank original signed B. Zlatkis (position of the authorized individual of the joint stock company) (signature) (initials, surname) L.S. “ 10 ” January 20 20 . Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 1 1 2 2 0 1 9 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint the affiliate indicated only with the consent of became valid the joint stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 Entity may manage more than The Central Bank of the Russian 107016, Moscow, 12 Neglinnaya 20% of the total number of votes 1 21/03/1991 50.000000004 52.316214 Federation St. -

Typology of Russian Regions

TYPOLOGY OF RUSSIAN REGIONS Moscow, 2002 Authors: B. Boots, S. Drobyshevsky, O. Kochetkova, G. Malginov, V. Petrov, G. Fedorov, Al. Hecht, A. Shekhovtsov, A. Yudin The research and the publication were undertaken in the framework of CEPRA (Consortium for Economic Policy, Research and Advice) project funded by the Canadian Agency for International Development (CIDA). Page setting: A.Astakhov ISBN 5-93255-071-6 Publisher license ID # 02079 of June 19, 2000 5, Gazetny per., Moscow, 103918 Russia Tel. (095) 229–6413, FAX (095) 203–8816 E-MAIL – root @iet.ru, WEB Site – http://www.iet.ru Соntents Introduction.................................................................................................... 5 Chapter 1. Review of existing research papers on typology of Russian regions ........................................................................ 9 Chapter 2. Methodology of Multi-Dimensional Classification and Regional Typology in RF ................................................... 40 2.1. Tasks of Typology and Formal Tools for their Solution ................. 40 2.1.1. Problem Identification and Its Formalization .......................... 40 2.2. Features of Formal Tools ................................................................. 41 2.2.1. General approach .................................................................... 41 2.2.2. Characterization of clustering methods ................................... 43 2.2.3. Characterization of the methods of discriminative analysis ..... 45 2.3. Method for Economic Parameterisation.......................................... -

List of Customs Offices Entitled to Accept ATA Carnets for the Purposes of Customs Clearance

List of Customs Offices entitled to accept ATA Carnets for the purposes of Customs clearance № Customs name Address Airport Vnukovo (passenger) Customs point bld. 3, 2, Vtoraya Reysovaya street, International Airport 1 Vnukovo, Moscow, 119027 Airport Vnukovo (cargo) Customs point bld. 3, 2, Vtoraya Reysovaya street, International Airport 2 Vnukovo, Moscow, 119027 Airport Vnukovo (cargo) Customs point bld. 3, 2, Vtoraya Reysovaya street, International Airport 3 (Department of customs clearance and Vnukovo, Moscow, 119027 customs control №2) Airport Domodedovo (passenger) Customs bld. 24, Moscow Airport Domodedovo, Moscow Region, 4 Point 142015 Airport Domodedovo (cargo) (passenger) bld. 24, Moscow Airport Domodedovo, Moscow Region, 5 Customs point 142015 Aerodrome Chkalovskiy Customs Point Aerodrome Chkalovskiy, Shchyolkovo-10, Moscow 6 Region, 141100 Aerodrome Ramenskoe Customs Point 10, Koperativnaya street, Zhukovskiy, Moscow Region, 7 140180 International Airport Sheremetyevo International Airport Sheremeteyevo, Khimki, Moscow 8 (passenger) Customs point Region, 141400 International Airport Sheremetyevo (cargo) International Airport Sheremeteyevo, Khimki, Moscow 9 Customs point Region, 141400 Specialized Customs point 12, Smolnaya street, Moscow 10 Only for the goods with the maintenance of precious metals and stones, jewelry North-West Excise Customs point 40 «а», Kulturi avenue, Saint-Petersburg 11 (specialized) Kaliningrad Excise Customs point 16, Druzhby street, Bagrationovsk, Kaliningrad Region, 12 238420 Krasnoperekopskiy Customs -

As of September 30, 2020

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint stock company) Issuer code: 0 1 4 8 1 – V as 3 0 0 9 2 0 2 0 of (indicate the date on which the list of affiliates of the joint stock company was compiled) Address of the issuer: 117997, Moscow, 19 Vavilova St. (address of the issuer – the joint stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Managing Director, Head of the Corporate Secretary Service (under the Power of Attorney No. 887-В (887-Д) dated 16 September 2019) original signed O. O. Tsvetkov (position of the authorized individual of the joint stock company) (signature) (initials, surname) L.S. “ 06 ” October 20 20 the city of Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 0 0 9 2 0 2 0 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint the affiliate indicated only with the consent of became valid the joint stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 1.