CMBIS Research

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2021 Yellow Table

YELLOW TABLE 2021 Yellow Table Construction Mini or Compact Equipment midi or skid- 2020/ sales (US$ Share of Backhoe Excavators steer Powered Telescopic 2021 Change Company Country million) total Loaders (0 - 13 t) loaders Access Handlers Cranes 1 1 Caterpillar US 24,824 13.0% 2 2 Komatsu JP 19,995 10.4% 3 4 1 XCMG CN 15,159 7.9% 4 5 1 Sany CN 14,418 7.5% 5 10 5 Zoomlion CN 9,449 4.9% 6 3 3 John Deere US 8,947 4.7% 7 6 1 Volvo Construction Equipment SE 8,846 4.6% 8 7 1 Hitachi Construction Machinery JP 8,549 4.5% 9 8 1 Liebherr DE 7,808 4.1% 10 9 1 Doosan Infracore KR 7,109 3.7% 11 11 Sandvik Mining and Rock Technology SE 5,823 3.0% 12 16 4 Metso Outotec FIN 4,443 2.3% 13 12 1 JCB** UK 4,000 2.1% 14 14 Epiroc SE 3,923 2.0% 15 19 4 Liugong CN 3,338 1.7% 16 17 1 Kobelco Construction Machinery JP 3,152 1.6% 17 13 4 Terex US 3,076 1.6% 18 18 Kubota JP 2,767 1.4% 19 21 2 Sumitomo Heavy Industries JP 2,518 1.3% 20 15 5 Oshkosh Access Equipment (JLG) US 2,515 1.3% 21 22 1 Hyundai Construction Equipment KR 2,345 1.2% 22 20 2 CNH Industrial IT 2,170 1.1% 23 28 5 Lonking CN 1,869 1.0% 24 24 Wacker Neuson DE 1,841 1.0% 25 23 2 Manitou FR 1,807 0.9% 26 25 1 Palfinger AT 1,748 0.9% 27 26 1 Tadano JP 1,704 0.9% 28 29 1 Fayat Group FR 1,596 0.8% 29 27 2 Manitowoc US 1,490 0.8% 30 30 Hiab FIN 1,311 0.7% 31 35 4 Sunward CN 1,195 0.6% 32 34 2 Shantui CN 1,147 0.6% 33 31 2 Astec Industries US 1,024 0.5% 34 33 1 Takeuchi JP 988 0.5% 35 32 3 Ammann** CH 966 0.5% 36 36 Skyjack** CA 751 -

CRRC Corp -H 1766.HK, 1766 HK Outlook Bullish

Asia Pacific Equity Research 30 October 2016 Overweight CRRC Corp -H 1766.HK, 1766 HK Outlook bullish. Weak Q3 and delayed orders factored Price: HK$7.15 ▼ Price Target: HK$12.50 in. Maintain OW Previous: HK$13.00 3Q16 result expectedly weak; guidance turned positive with MU China demand outlook raised. CRRC reported 3Q NPAT of Rmb2.7B, -16% Infrastructure, Industrials & Y/Y as revenue fell 4% Y/Y while GPM slipped 1.1ppts Y/Y. These Transport results were largely expected in light of CRC’s muted procurement Karen Li, CFA AC YTD. However, we observed that guidance was noticeably more bullish (852) 2800-8589 (inside for takeaways from the briefing) despite the near-term earnings [email protected] Bloomberg JPMA KLI <GO> pressure in 4Q16. Mgmt expects this year's pent-up orders to be released J.P. Morgan Securities (Asia Pacific) Limited soon with CRC's leadership transition completed, while highlighting the robust MU demand in coming years driven by new product sales, rising Price Performance aftersales services, and increasing MU density. We remain positive on 10.5 the demand outlook for rolling stock in China, recommending switching 9.5 HK$ to late cycle railway capex plays over E&C contractors. Our new Dec-17 8.5 PT is HK$12.5 for CRRC-H; maintain OW. 7.5 6.5 CRC leadership transition completed; pace of procurement to Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 1766.HK share price (HK$) accelerate into year-end. Mgmt was optimistic that this year’s long- HSCI (rebased) awaited orders will be released soon, highlighting CRC's new chief Mr. -

Construction Machinery

Deutsche Bank Markets Research Asia Industry Date China 18 October 2013 Industrials Construction Manufacturing machinery Industry Update Phyllis Wang Research Analyst Continued healthy demand recovery (-) - - [email protected] of wheel loader in Sept China’s wheel-loader sales volume in Sept 2013 up 17% yoy, in line Focus stocks According to 21-Sun, China’s wheel loader sales volume (including exports) Lonking (3339.HK),HKD1.68 Buy Price Target recorded 13,176 units in September, up 16.9% yoy. We think this was due HKD1.98 mainly to healthy demand recovery in the domestic market (+24% yoy). For the Zoomlion (1157.HK),HKD7.17 Hold Price Target first time this year, ytd sales volume growth has turned from negative to HKD6.01 positive, which was +0.1% yoy (vs. -1.4% in 8M13 and -30% in 2012). Total Source: Deutsche Bank sales volume in 3Q13 was up 14.5% yoy, largely in line with our half-year volume assumption (14% yoy rise in 2H13). Lonking’s market share stabilized in September mom The combined market share of the top five players (Lingong, Liugong, Lonking, Xiagong and XCMG) was stable at 74.5% in 9M13. (vs. 74.2% in 8M13 and 72.4% in 2012). Lonking sold 19,320 units (-8% yoy) in 9M13, with a market share of 14% (vs. 14.2% in 8M13 and 14.8% in 2012). We note that Lonking and Linggong are losing market share to XCMG and Xiagong in 3Q13. We think this is mainly because Lonking continues its prudent sales strategy. However, Lonking’s sales volume of wheel loaders rose 24% yoy in September to 1,569 units with a stabilized market share of 11.9%, vs. -

ANNUAL REPORT 2020 Annual Report 147402 (Zoomlion Eng) 00

中聯重科股份有限公司 ZOOMLION HEAVY INDUSTRY SCIENCE AND TECHNOLOGY CO., LTD. ANNUAL REPORT 2020 Annual Report 147402 (Zoomlion Eng)_00. IFC (eng)_(210x285) \ 14/04/2021 \ X11 \ P. 1 Important notice • The Board of Directors and the Supervisory Board of the Company and its directors, supervisors and senior management warrant that there are no misrepresentation, misleading statements or material omissions in this report and they shall, individually and jointly, accept full responsibility for the truthfulness, accuracy and completeness of the contents of this report. • All directors attended the Board meeting at which this report was reviewed. Definition Unless the context otherwise requires, the following terms shall have the meanings set out below: “The Company” or “Zoomlion” refers to Zoomlion Heavy Industry Science and Technology Co., Ltd. “Listing Rules” or “Listing Rules of Hong Kong” refers to the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited. 147402 (Zoomlion Eng)_00. IFC (eng)_(210x285) \ 14/04/2021 \ X11 \ P. 2 CONTENTS Company Profile 2 Chairman’s Statement 4 Principal Financial Data and Indicators 7 Report of the Board of Directors 10 Management Discussion and Analysis 24 Environmental, Social and Governance Report 34 Significant Events 63 Changes in Share Capital and Shareholders 66 Directors, Supervisors, Senior Management and Employees 71 Share Option Scheme 82 Corporate Governance 86 Independent Auditor’s Report 101 Financial Statements prepared in accordance with International Financial Reporting Standards and Notes 109 147402 (Zoomlion Eng)_01. Company Profile_(210x285) \ 13/04/2021 \ X11 \ P. 2 Company Profile I. Company Information Company name (in Chinese): 中聯重科股份有限公司 Chinese abbreviation: 中聯重科 Company name (in English): Zoomlion Heavy Industry Science And Technology Co., Ltd.* English abbreviation: Zoomlion Legal representative of the Company: Zhan Chunxin Secretary of the Board of Directors/Company Secretary: Yang Duzhi Representative of securities affairs: Xu Yanlai Contact address: No. -

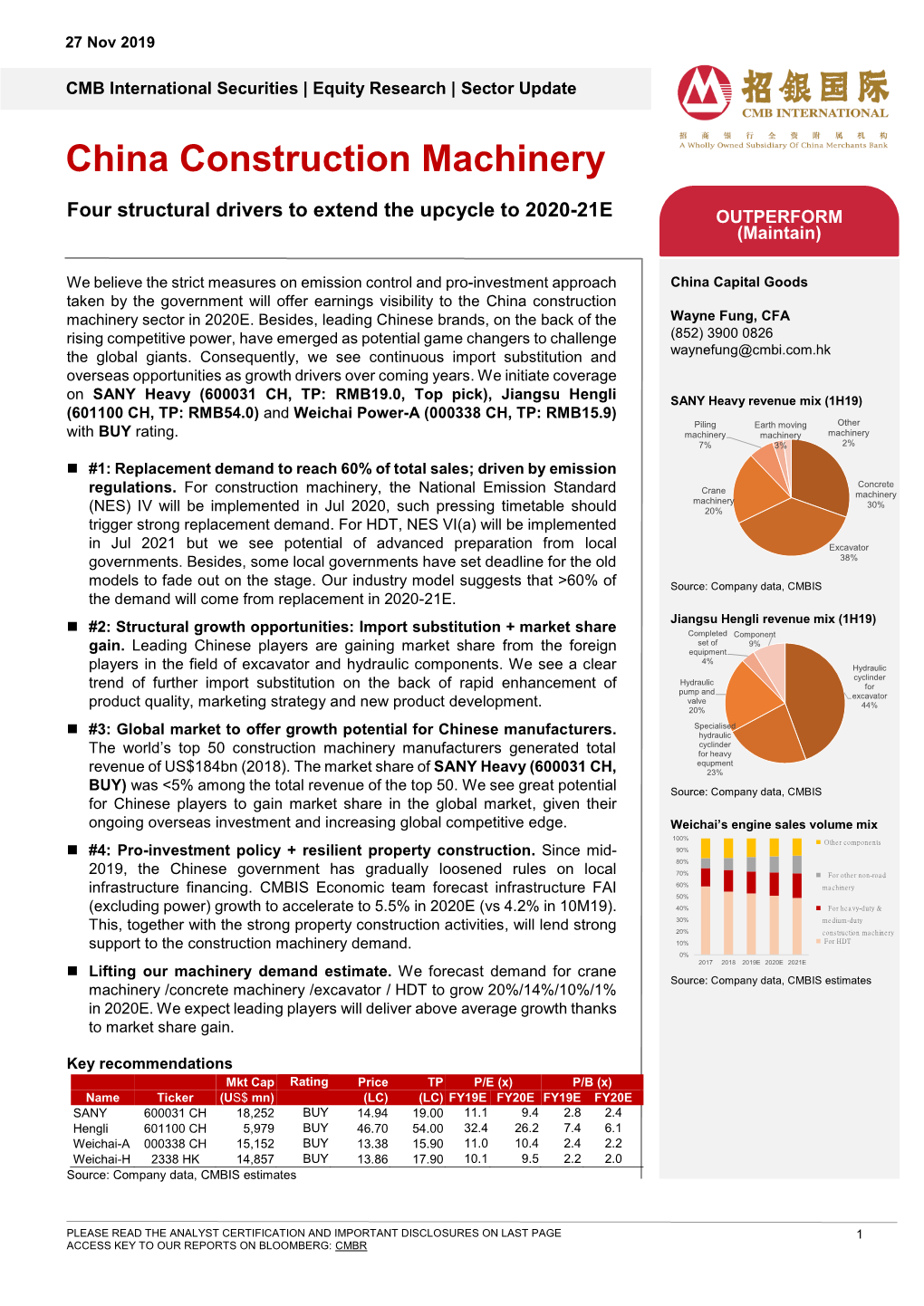

China Construction Machinery

10 Feb 2020 CMB International Securities | Equity Research | Sector Update China Construction Machinery Scenario analysis on the resumption of factory production OUTPERFORM (Maintain) Factories in China, except Hubei, are scheduled to resume operation today. We China Capital Goods evaluate the companies under our coverage from several dimensions, including location of factories, capacity utilization, downstream demand and cash flow Wayne Fung, CFA management. Our base case scenario suggests that the overall earnings impact (852) 3900 0826 for the full year should be limited, as the sales volume in 1Q (the traditional peak [email protected] season) will potentially be shifted to 2Q or 3Q (low seasons) when the construction activities pick up when the epidemic is under control. We believe potential share price volatility in the near term will serve as opportunities to accumulate quality names such as SANY Heavy (600031 CH, BUY, TP: RMB19.0), Jiangsu Hengli (601100 CH, BUY, TP: RMB54.0) and Weichai Power (2338 HK, BUY, TP: HK$17.9 / 000338 CH, BUY, TP: RMB15.9). Utilization rate to gradually increase. For the companies under our coverage, no production base is located in Hubei province (figure 1). Some companies such as Weichai, SANY Heavy and Zoomlion have already resumed production since last week while others will restart today. That said, we do expect most of them will only ramp up its production gradually due to the potential labour shortage in the near term. Companies are trying their best to ramp up production to fulfil the existing orders, based on our check. Related Reports Expect mild delay on downstream demand. -

Pengyuan Credit Rating (Hong Kong) Co.,Ltd

Corporate China Weichai Power Co., Ltd. Ratings Overview Issuer Rating ▪ Pengyuan International has assigned a first-time global scale long-term issuer LT Issuer Credit Rating BBB+ credit rating (LTICR) of ‘BBB+’ to Weichai Power Co., Ltd. (Weichai). The outlook is stable. Outlook Stable ▪ The rating reflects Weichai’s position as the leading domestic heavy-duty truck player with increasing business diversification through an expanded product portfolio, its presence in KION Group and an exceptional leverage profile with Contents strong cash flow. On the other hand, Weichai’s rating is constrained by its relatively high exposure to cyclical heavy-duty truck market in China. Key Rating Drivers .........................2 ▪ Weichai primarily engages in the development and manufacturing of vehicles and components, mainly powertrains such as engines, gearboxes and axles, Business Profiles ...........................3 forklift trucks and the provision of warehouse technology services. In 2020, Financial Profile .............................5 24% of its revenue came from engines, 43% from automobiles and automobile components and 33% from intelligent logistics. Liquidity .........................................6 Company Background ...................6 Rating Outlook Peer comparison ...........................6 ▪ The stable outlook for Weichai reflects our expectation that the Company will Rating Scores Summary ................8 continuously maintain its leading market position in the Chinese powertrain Related Criteria ..............................8 market given its extensive track record of technological innovation in the development of powertrain products such as diesel engines, gearboxes and axles. ▪ We would consider upgrading Weichai’s issuer credit rating if its credit profile improves substantially, which could be caused by: 1) a remarkable increase in market share in the key markets; and 2) a significant improvement in business diversity through successful overseas business expansion or business diversification to non-heavy-duty truck related business. -

Global Industrials

28 May 2013 Americas/United States Equity Research Electrical Equipment / Capital Goods i-Spy Global Industrials Weekly Research Analysts COMMENT Julian Mitchell 212 325 6668 [email protected] More signs of Japanese manufacturing Charles Clarke 212 538 7095 renaissance; rising competition in industrial [email protected] Jonathan Shaffer automation, but bottoming demand 212 325 1259 [email protected] ■ Further signs of Japanese manufacturing renaissance: In an earlier i-Spy, we noted that Nissan had delayed the migration of certain car model production out of Japan; now Kawasaki has announced it will bring back production of mid- sized motorbikes from Thailand to Japan due to the falling Yen. Many of KHI's motorbikes manufactured in Thailand are sold in the US; production will move This Week (5/27/2013 - 6/2/2013) gradually to Japan beginning this autumn. Macro Events ■ China to develop large aero engines within a decade: The MITI's industry 5/28 US May Dallas Fed Mfg. Activity plan last week targets 5% local market share for the domestic commercial 5/28 US May Richmond Fed aerospace industry by 2020 (C919 orders have already reached almost 400 5/30 Euro-Zone Business Climate aircraft), and an assembly line for medium-power aero engines by 2015, with 5/31 US May Chicago PMI larger engines to be produced within 10 years. 6/1 China PMI Mfg ■ Industrial automation competition increasing; PLC role under threat: Company Events Meetings at EPG and at ETN confirmed several themes we noted following our 5/27-30 Siemens AG Roadshow - Beijing trip to Hannover's Automation Fair in April. -

Examples for Business Scenarios in Manufacturing Industry Published By: Deutsche Gesellschaft Für Internationale Zusammenarbeit (GIZ) Gmbh

GLOBAL PROJ T Quality Infrastructure Examples for Business Scenarios in Manufacturing Industry Published by: Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH Registered offices Bonn and Eschborn, Germany Global Project Quality Infrastructure Tayuan Diplomatic Office Building No.14, Liangmahe Nanlu, chaoyang District Text 100600 Beijing, PR China Standardization Council Industrie 4.0 DKE Deutsche Kommission Elektrotechnik E [email protected] Elektronik Informationstechnik in DIN und VDE, I www.gpqi.org 60596 Frankfurt am Main Design/layout: National Intelligent Manufacturing Standardisation Administration Group Iris Christmann, Wiesbaden China Electronics Standardization Institute, No.1 Andingmen East Street, Dongcheng District, Beijing, 100007, China Photo credits: Depositphotos Authors/Experts CHEN Jiangning, Siemens Ltd. China; CHENG Yuhang, China Electronics On behalf of Standardization Institute (CESI); CHEN Zhiman, Zhuzhou CRRC Times Federal Ministry of Economic Affairs and Energy (BMWi) Electric Co., Ltd.; Wolfgang Dorst, ROI Management Consulting AG; Lucas Gierging, Spanflug Technologies GmbH; Dr. Hannes Leonardy, UNITY AG; Beijing, China 2020 Prof. Dr. Ulrich Loewen, Siemens AG; ZHAO Haitao, Siemens Ltd. China A joint project of: EXAMPLES FOR BUSINESS SCENARIOS IN MANUFACTURING INDUSTRY 3 Contents Introduction ....................................................... 4 Background.........................................................4 Common Understanding of “Use Cases”....................................4 Objectives -

Interim Report 2020 Sany Heavy Equipment International Holdings Company Limited 1 Financial Summary

Contents Financial Summary 2 Corporate Information 3 Chairman’s Statement 4 Management Discussion and Analysis 6 Disclosure of Interests 15 Corporate Governance and General Information 22 Directors and Senior Management 25 Interim Condensed Consolidated Statement of Profit or Loss 32 Interim Condensed Consolidated Statement of Comprehensive Income 33 Interim Condensed Consolidated Statement of Financial Position 34 Interim Condensed Consolidated Statement of Changes in Equity 36 Interim Condensed Consolidated Statement of Cash Flows 38 Notes to Interim Condensed Consolidated Financial Information 39 Interim Report 2020 Sany Heavy Equipment International Holdings Company Limited 1 Financial Summary Six months ended 30 June (RMB: ’000) 2020 2019 (Unaudited) (Unaudited) Increase (%) Revenue 3,815,076 3,043,706 25.3% Gross profit 1,030,096 943,993 9.1% Profit before tax 753,952 640,283 17.8% Net profit 638,619 552,763 15.5% Profit attributable to owners of the parent 639,705 551,732 15.9% Total assets 17,390,102 13,332,412 30.4% Total equity 7,409,704 6,774,283 9.4% Cash flows of operating activities 648,604 515,687 25.8% Cash flows of investing activities (1,180,500) (521,098) 126.5% Cash flows of financing activities 466,877 (176,147) (365.0%) Earnings per share1 – Basic (RMB Yuan) 0.21 0.18 16.7% – Diluted (RMB Yuan) 0.18 0.15 20.0% Six months ended 30 June (Percentage) 2020 2019 Increase (%) Gross profit margin 26.2% 30.5% (4.3%) Percentage of profit margin before tax attributable to shareholders of the Company2 19.8% 21.0% (1.2%) Assets turnover 23.2% 23.2% – Gearing ratio 57.4% 49.2% 8.2% Average total assets (RMB’000) 16,468,269 13,128,553 25.4% 1 The weighted average number of ordinary shares for the six months ended 30 June 2020 was 3,104,960,486 (six months ended 30 June 2019: 3,061,638,898), details of which are set out in note 9 to the interim condensed consolidated financial statements. -

SINOPEC Lubricants for Off-Highway Equipment S in O PE

SINOPEC Lubricants For Off-Highway Equipment SINOPEC Working Together For Wonderful Future For Wonderful Together Working SINOPEC Lubricant SINOPEC Lubricants for Off-Highway Equipment Contents Company Introduction Lubrication Solution for Off-Highway Equipment Major Lubricants for Off-Highway Equipment Integrity Leads To Win-Win Cooperation Introduction Sinopec Lubricant Co., Ltd. is a company specialized in lubricant marketing Lubricant Co., Ltd. has been committed to providing lubrication service for established by China Petrochemical Corporation (hereinafter referred to as “Shenzhou” series manned spacecrafts and “Chang’e” series lunar exploration “Sinopec Group”) to meet competition in the international lubricant market. satellites, making great contributions to the development of Chinese aeronautics Sinopec Lubricant Co., Ltd. has 12 lube oil & grease blending and manufacturing and astronautics course. Sinopec’s lubrication products completely satisfy the branches, 5 regional sales centers, 5 regional technical support centers, requirements set by ISO, API, ACEA, etc. 5 provincial sales branches, 3 joint ventures, 1 overseas subsidiary and 9 Keeping pace with the development of off-highway vehicles, Sinopec Lubricant RYHUVHDVRI¿FHVWRJHWKHUZLWKSURGXFW5 'LQVWLWXWHVDQGVWDWHUHFRJQL]HG Co., Ltd. has good cooperation with construction machinery enterprises and ODERUDWRULHV:LWKOHDGLQJLQQRYDWLYHDQG5 'FDSDELOLWLHVDQGZRUOGFODVV production equipments and process technologies, the Company boasts over distinct advantage in off-highway industry. SINOPEC lubricants are extensively 2,000 types of products such as lubricants for internal combustion engine, applied to famous enterprises such as XCMG, ZOOMLION, SANY, Lonking, industrial gear oils, hydraulic oils, greases, antifreezes, brake fluid, metal XGMA and SEM in China. With professional lubricants, Sinopec Lubricant Co., working fluids, Marine oils, lubricant additives, etc. divided in 21 categories, Ltd. -

Green Competitiveness Research on Chinese Automotive Enterprises

Journal of Industrial Engineering and Management JIEM, 2014 – 7(2): 559-572 – Online ISSN: 2014-0953 – Print ISSN: 2014-8423 http://dx.doi.org/10.3926/jiem.1032 Green competitiveness research on Chinese automotive enterprises Yuanhui Li School of Economics and Management, Beijing Jiaotong University (China) [email protected] Abstract: Purpose: More and more executives of automobile industry in China start to recognize the concept of green competitiveness recently. However, relatively less research attention has been devoted to the consideration of measurement. This paper aims to find empirical approach to quantify green competitiveness for automotive enterprises. The connotation of green competitiveness is explored and one suite of evaluation index system has been proposed with four dimensions including environmental, resource, capability and knowledge. Design/methodology/approach: By introducing the factor analysis method, green competitiveness has been measured through an empirical analysis of 24 automotive enterprises within China. Findings: The results indicate that those elements, such as enterprise resource possession and utilization; environment, responsibility and knowledge; profitability; management efficiency, have significant effect on the green competitiveness for automotive enterprises. The further analysis also unveils the advantages and disadvantages of green competitiveness for each company and the direction for improvement. Research limitations/implications: Guide regulators and managers of automobile industry to take some measures to enhance their green competitive advantage. Practical implications: Provide practical methods to measure green competitiveness for automotive enterprises. -559- Journal of Industrial Engineering and Management – http://dx.doi.org/10.3926/jiem.1032 Originality/value: This paper proposes an evaluation index system of green competitiveness for automotive enterprises. -

Construction Machinery

2 November 2017 Manufacturing Construction Machinery Deutsche Bank Markets Research Asia Industry Date China 2 November 2017 Industrials Construction Manufacturing Machinery Recommendation Change Quality growth ahead instead of quantity Fei Sun, CFA Not too late in the cycle; expect quality growth in 2018 Construction machinery sales bottomed out in 3Q16 and have been growing Research Analyst rapidly, driven mainly by demand from infrastructure projects and replacement +852-2203 6130 orders. We identify the key drivers of construction machinery demand and our Vincent Ha, CFA top-down analysis suggests the industry will deliver moderate growth next year. Research Analyst Zoomlion would have relatively greater operating leverage as the sector continues +852-2203 6247 to recover, and we believe the valuation gap between Lonking and Zoomlion will narrow. We upgrade Zoomlion to Buy, as we expect an earnings rebound in Yuki Lu FY18-19 and asset quality to improve (less bad debt provision). We maintain a Research Associate Hold on Lonking as the positives, such as the ability to gain market share and +852-2203 5925 expand margins, are already factored into its share price. Key Changes Better-than-expected demand with balanced supply Company Target Price Rating According to China Construction Machinery Association (CCMA), excavator/ 1157.HK 3.89 to 4.80 Hold to Buy wheel loader/truck crane sales volume surged 100%/45%/122% in 9M17 amid 3339.HK 2.05 to 3.60 - robust replacement and infrastructure demand. Unlike the oversupply in the Source: Deutsche Bank previous down-cycle, construction machinery supply was balanced this time. This Top picks is because, unlike in 2011, fewer individual contractors have entered the industry, Zoomlion (1157.HK),HKD3.81 Buy allowing more rational market competition.