Carnegie Rysslandsfond

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unipro Group Consolidated Financial Statements

UNIPRO GROUP CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AND INDEPENDENT AUDITOR’S REPORT 31 DECEMBER 2018 Contents INDEPENDENT AUDITOR’S REPORT CONSOLIDATED FINANCIAL STATEMENTS Consolidated Statement of Financial Position ......................................................................................... 1 Consolidated Statement of comprehensive Income ................................................................................ 2 Consolidated Statement of Changes in Equity ........................................................................................ 3 Consolidated Statement of Cash Flows .................................................................................................. 4 NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS Note 1. The Group and its operations ..................................................................................................... 5 Note 2. Principles of preparation and summary of significant accounting policies ................................. 7 Note 3. Critical accounting estimates and assumptions ........................................................................ 19 Note 4. Application of new and revised standards and clarifications .................................................... 20 Note 5. Related Parties ......................................................................................................................... 25 Note 6. Acquisitions and disposals ....................................................................................................... -

Expiry Notice

Expiry Notice 19 January 2018 London Stock Exchange Derivatives Expiration prices for IOB Derivatives Please find below expiration prices for IOB products expiring in January 2018: Underlying Code Underlying Name Expiration Price AFID AFI DEVELOPMENT PLC 0.1800 ATAD PJSC TATNEFT 58.2800 FIVE X5 RETAIL GROUP NV 39.2400 GAZ GAZPROM NEFT 23.4000 GLTR GLOBALTRANS INVESTMENT PLC 9.9500 HSBK JSC HALYK SAVINGS BANK OF KAZAKHSTAN 12.4000 HYDR PJSC RUSHYDRO 1.3440 KMG JSC KAZMUNAIGAS EXPLORATION PROD 12.9000 LKOD PJSC LUKOIL 67.2000 LSRG LSR GROUP 2.9000 MAIL MAIL.RU GROUP LIMITED 32.0000 MFON MEGAFON 9.2000 MGNT PJSC MAGNIT 26.4000 MHPC MHP SA 12.8000 MDMG MD MEDICAL GROUP INVESTMENTS PLC 10.5000 MMK OJSC MAGNITOGORSK IRON AND STEEL WORKS 10.3000 MNOD MMC NORILSK NICKEL 20.2300 NCSP PJSC NOVOROSSIYSK COMM. SEA PORT 12.9000 NLMK NOVOLIPETSK STEEL 27.4000 NVTK OAO NOVATEK 128.1000 OGZD GAZPROM 5.2300 PLZL POLYUS PJSC 38.7000 RIGD RELIANCE INDUSTRIES 28.7000 RKMD ROSTELEKOM 6.9800 ROSN ROSNEFT OJSC 5.7920 SBER SBERBANK 18.6900 SGGD SURGUTNEFTEGAZ 5.2450 SMSN SAMSUNG ELECTRONICS CO 1148.0000 SSA SISTEMA JSFC 4.4200 SVST PAO SEVERSTAL 16.8200 TCS TCS GROUP HOLDING 19.3000 TMKS OAO TMK 5.4400 TRCN PJSC TRANSCONTAINER 8.0100 VTBR JSC VTB BANK 1.9370 Underlying code Underlying Name Expiration Price D7LKOD YEAR 17 DIVIDEND LUKOIL FUTURE 3.2643 YEAR 17 DIVIDEND MMC NORILSK NICKEL D7MNOD 1.8622 FUTURE D7OGZD YEAR 17 DIVIDEND GAZPROM FUTURE 0.2679 D7ROSN YEAR 17 DIVIDEND ROSNEFT FUTURE 0.1672 D7SBER YEAR 17 DIVIDEND SBERBANK FUTURE 0.3980 D7SGGD YEAR 17 DIVIDEND SURGUTNEFTEGAZ FUTURE 0.1000 D7VTBR YEAR 17 DIVIDEND VTB BANK FUTURE 0.0414 Members are asked to note that reports showing exercise/assignments should be available by approx. -

NOVATEK RS Presentation

“Harnessing the Energy of the Far North” Mark Gyetvay, Deputy Chairman of the Management Board Alexander Palivoda, Head of Investor Relations Goldman Sachs Global Natural Resources Conference London 11-12 November 2015 Forward-Looking Statements Certain statements in this presentation are not historical facts and are “forward-looking”. Examples of such forward-looking statements include, but are not limited to: – projections or expectations of revenues, income (or loss), earnings (or loss) per share, dividends, capital structure or other financial items or ratios; – statements of our plans, objectives or goals, including those related to products or services; – statements of future economic performance; and – statements of assumptions underlying such statements Words such as “believes”, “anticipates”, “expects”, “estimates”, “intends”, “plans”, “outlook” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the predictions, forecasts, projections and other forward-looking statements will not be achieved. You should be aware that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements When relying on forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, especially in light of the political, economic, social and legal environment in which we operate. Such forward-looking statements speak only as of the date on which they are made, and we do not undertake any obligation to update or revise any of them, whether as a result of new information, future events or otherwise. -

Energy Without Borders

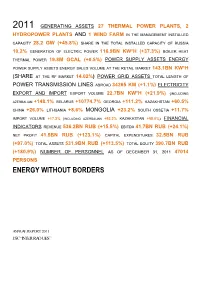

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

Information on IRC – R.O.S.T., the Registrar of the Company and the Acting Ballot Committee of MMC Norilsk Nickel

Information on IRC – R.O.S.T., the registrar of the Company and the acting Ballot Committee of MMC Norilsk Nickel IRC – R.O.S.T. (former R.O.S.T. Registrar merged with Independent Registrar Company in February 2019) was established in 1996. In 2003–2015, Independent Registrar Company was a member of Computershare Group, a global leader in registrar and transfer agency services. In July 2015, IRC changed its ownership to pass into the control of a group of independent Russian investors. In December 2016, R.O.S.T. Registrar and Independent Registrar Company, both owned by the same group of independent investors, formed IRC – R.O.S.T. Group of Companies. In 2018, Saint Petersburg Central Registrar joined the Group. In February 2019, Independent Registrar Company merged with IRC – R.O.S.T. Ultimate beneficiaries of IRC – R.O.S.T. Group are individuals with a strong background in business management and stock markets. No beneficiary holds a blocking stake in the Group. In accordance with indefinite License No. 045-13976-000001, IRC – R.O.S.T. keeps records of holders of registered securities. Services offered by IRC – R.O.S.T. to its clients include: › Records of shareholders, interestholders, bondholders, holders of mortgage participation certificates, lenders, and joint property owners › Meetings of shareholders, joint owners, lenders, company members, etc. › Electronic voting › Postal and electronic mailing › Corporate consulting › Buyback of securities, including payments for securities repurchased › Proxy solicitation › Call centre services › Depositary and brokerage, including escrow agent services IRC – R.O.S.T. Group invests a lot in development of proprietary high-tech solutions, e.g. -

Annual Report ‘06 Contents

ANNUAL REPORT ‘06 CONTENTS MESSAGE TO SHAREHOLDERS ————————————————————————————— 4 MISSION AND STRATEGY ———————————————————————————————— 7 COMPANY OVERVIEW ————————————————————————————————— 13 ² GENERAL INFORMATION 13 ² GEOGRAPHIC LOCATION 14 ² CALENDAR OF KEY 2006 EVENTS 15 ² REORGANIZATION 16 CORPORATE GOVERNANCE —————————————————————————————— 21 ² PRINCIPLES AND DOCUMENTS 21 ² MANAGEMENT BODIES OF THE COMPANY 22 ² CONTROL BODIES 39 ² AUDITOR 40 ² ASSOCIATED AND AFFILIATED COMPANIES 40 ² INTERESTED PARTY TRANSACTIONS 41 SECURITIES AND EQUITY ——————————————————————————————— 43 ² CHARTER CAPITAL STRUCTURE 43 ² STOCK MARKET 44 ² DIVIDEND HISTORY 48 ² REGISTRAR 49 OPERATING ACTIVITIES. KEY PERFORMANCE INDICATORS ——————————————— 51 ² GENERATING FACILITIES 51 ² FUEL SUPPLY 52 ² ELECTRICITY PRODUCTION 56 ² HEAT PRODUCTION 59 ² BASIC PRODUCTION ASSETS REPAIR 59 ² INCIDENT AND INJURY RATES. OCCUPATIONAL SAFETY 60 ² ENVIRONMENTAL SAFETY 61 ELECTRICITY AND HEAT MARKETS ——————————————————————————— 65 ² COMPETITIVE ENVIRONMENT. OVERVIEW OF KEY MARKETS 65 ² ELECTRICITY AND HEAT SALES 67 FINANCIAL OVERVIEW ————————————————————————————————— 73 ² FINANCIAL STATEMENTS 73 ² REVENUES AND EXPENSES BREAKDOWN 81 INVESTMENT ACTIVITIES ———————————————————————————————— 83 ² INVESTMENT STRATEGY 83 ² INVESTMENT PROGRAM 84 ² INVESTMENT PROGRAM FINANCING SOURCES 86 ² DEVELOPMENT PROSPECTS 87 INFORMATION TECHNOLOGY DEVELOPMENT —————————————————————— 89 PERSONNEL AND SOCIAL POLICY. SOCIAL PARTNERSHIP ———————————————— 91 INFORMATION FOR INVESTORS AND SHAREHOLDERS —————————————————— -

Methodical Approach to Assessing the Effectiveness of the Management System of Thermal Power Plants in Russia

E3S Web of Conferences 124, 04003 (2019) https://doi.org/10.1051/e3sconf/201912404003 SES-2019 Methodical approach to assessing the effectiveness of the management system of thermal power plants in Russia P. I. Okley1, V. K. Lozenko1 and R. I. Inamov1,* 1 National Research University "Moscow Power Engineering Institute", Moscow, Russia Abstract. Physical deterioration of thermal power plants based on hydrocarbon fuels leads to technological violations (TV) in their work. Low rates of renewal of thermal generation predetermines the further exploitation of old capacities. In this regard, the activity of the management of energy holdings (EH) is more focused on maintaining the equipment in working condition. The methods, approaches and tools underlying decision-making by the management of energy holding companies are different, respectively, the results of the functioning of the organized management systems (MS) of each company are also different. To assess the effectiveness of the management system it is proposed to use such a generalized indicator as the number of technological violations per year per 1 GW of installed capacity. 1 Introduction capacity — for example, the balance of the largest holdings includes both traditional thermal power plants The electric power industry is one of the key areas of and nuclear and hydro generation. To understand the Russia's development, the country's economy and social scale of management activities it is interesting to find out position of all citizens depend on it. This industry is he general values of the installed capacity belonging to represented by 11 largest holding companies, which each holding in addition to data on production volumes produce about 85% of electricity (in 2018 - 921.8 billion and the technological structure of the generating kW*h) of the total annual production (1076.2 billion complex of the Russian Federation. -

Notes on Moscow Exchange Index Review

Notes on Moscow Exchange index review Moscow Exchange approves the updated list of index components and free float ratios effective from 16 March 2018. X5 Retail Group N.V. (DRs) will be added to Moscow Exchange indices with the expected weight of 1.13 per cent. As these securities were offered initially, they were added without being in the waiting list under consideration. Thus, from 16 March the indices will comprise 46 (component stocks. The MOEX Russia and RTS Index moved to a floating number of component stocks in December 2017. En+ Group plc (DRs) will be in the waiting list to be added to Moscow Exchange indices, as their liquidity rose notably over recent three months. NCSP Group (ords) with low liquidity, ROSSETI (ords) and RosAgro PLC with their weights now below the minimum permissible level (0.2 per cent) will be under consideration to be excluded from the MOEX Russia Index and RTS Index. The Blue Chip Index constituents remain unaltered. X5 Retail Group (DRs), GAZ (ords), Obuvrus LLC (ords) and TNS energo (ords) will be added to the Broad Market Index, while Common of DIXY Group and Uralkali will be removed due to delisting expected. TransContainer (ords), as its free float sank below the minimum threshold of 5 per cent, and Southern Urals Nickel Plant (ords), as its liquidity ratio declined, will be also excluded. LSR Group (ords) will be incuded into SMID Index, while SOLLERS and DIXY Group (ords) will be excluded due to low liquidity ratio. X5 Retail Group (DRs) and Obuvrus LLC (ords) will be added to the Consumer & Retail Index, while DIXY Group (ords) will be removed from the Index. -

An Overview of Boards of Directors at Russia's Largest Public Companies

An Overview Of Boards Of Directors At Russia’s Largest Public Companies Andrei Rakitin Milena Barsukova Arina Mazunova Translated from Russian August 2020 Key Results According to information disclosed by 109 of Russia’s largest public companies: “Classic” board compositions of 11, nine, and seven seats prevail The total number of persons on Boards of the companies under study is not as low as it might seem: 89% of all Directors were elected to only one such Board Female Directors account for 12% and are more often elected to the audit, nomination, and remuneration committees than to the strategy committee Among Directors, there are more “humanitarians” than “techies,” while the share of “techies” among chairs is greater than across the whole sample The average age for Directors is 53, 56 for Chairmen, and 58 for Independent Directors Generation X is the most visible on Boards, and Generation Y Directors will likely quickly increase their presence if the impetuous development of digital technologies continues The share of Independent Directors barely reaches 30%, and there is an obvious lack of independence on key committees such as audit Senior Independent Directors were elected at 17% of the companies, while 89% of Chairs are not independent The average total remuneration paid to the Board of Directors is RUR 69 million, with the difference between the maximum and minimum being 18 times Twenty-four percent of the companies disclosed information on individual payments made to their Directors. According to this, the average total remuneration is approximately RUR 9 million per annum for a Director, RUR 17 million for a Chair, and RUR 11 million for an Independent Director The comparison of 2020 findings with results of a similar study published in 2012 paints an interesting dynamic picture. -

ZONE COUNTRIES OPERATOR TADIG CODE Calls

Calls made abroad SMS sent abroad Calls To Belgium SMS TADIG To zones SMS to SMS to SMS to ZONE COUNTRIES OPERATOR received Local and Europe received CODE 2,3 and 4 Belgium EUR ROW abroad (= zone1) abroad 3 AFGHANISTAN AFGHAN WIRELESS COMMUNICATION COMPANY 'AWCC' AFGAW 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN AREEBA MTN AFGAR 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN TDCA AFGTD 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN ETISALAT AFGHANISTAN AFGEA 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 1 ALANDS ISLANDS (FINLAND) ALANDS MOBILTELEFON AB FINAM 0,08 0,29 0,29 2,07 0,00 0,09 0,09 0,54 2 ALBANIA AMC (ALBANIAN MOBILE COMMUNICATIONS) ALBAM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA VODAFONE ALBVF 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA EAGLE MOBILE SH.A ALBEM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA DJEZZY (ORASCOM) DZAOT 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA ATM (MOBILIS) (EX-PTT Algeria) DZAA1 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA WATANIYA TELECOM ALGERIE S.P.A. -

Russian Withholding Tax Refund

Russian withholding tax refund Tax & Legal If you or your clients invested in Russian securities and are entitled to a substantial dividend or interest income, there is a chance that you overpaid your taxes and may qualify for a tax refund © 2018 Deloitte Consulting LLC Background Investors may apply a According to the The Russian The tax refund reduced tax rate for Russian tax withholding tax rate is practice in Russia is their interest and/or authorities, they are set at 15% on not well-developed: dividend income, ready to reimburse dividends and 20 the tax legislation depending on the overpaid taxes, if a percent on interest. does not provide for a conditions set by the full package of Effective from 1 specific list of Russian Tax Code or documents confirming January 2014, the documents to be applicable Double Tax the income payment duties of the tax collected and Treaties. Calculations chain and the agent for WHT requirements to be of a standard Russian investor’s rights to purposes were met. For these rate or the standard the income is transferred to the reasons, the process reduced Double Tax submitted. local Russian can be lengthy and Treaty rate, as well as custodian or, in a sometimes fruitless. submission of claims limited number of However, the trend is on tax can be cases, to the reassuring: the refunded, should be fiduciary, broker or number of successful made by investors issuer. refund claims and themselves within positive court three calendar years, decisions is growing. following the year in which it was withheld. -

Annual Report 2012 Annual Report

Annual Report 2012 Annual Report Annual Report www.AR2012.megafon.ru/en Chief Executive Officer I.V. Tavrin (signature) Chief Accountant L.N. Strelkina (signature) Annual Report 2012 CONTENTS MEGAFON MegaFon’s business model and key 2012 results 4 Finanсial and operational highlights for 2012 2012 marked a new 8 Our business page in MegaFon’s history STRATEGY Management’s overview of the results p. 14 and vision for growth 14 Letter of the Chairman of the Board LETTER 18 Letter of the CEO OF THE CHAIRMAN 22 Strategy OF THE BOARD 24 The Russian market in 2012 РERFORMANCE MegaFon’s operating and financial results 30 Review of operations 48 Finanсial review GOVERNANCE Free cash flow reached RUB 70.8 billion Corporate governance and risk management systems 52 Risk management p. 48 56 Corporate governance 69 Shareholder’s equity FINANCIAL REVIEW SUSTAINABILITY Our mission is Responsibility to employees to bring Russia and community together through 74 Sustainable development communication technology APPENDICES 82 Management responsibility statement 82 US GAAP Consolidated Financial Statements p. 74 128 Appendices SUSTAINABLE 160 Contacts DEVELOPMENT generated at BeQRious.com This Annual Report focuses principally on our operations in the Russian Federation. While we have operating subsidiaries in the For more information Republics of Tajikistan (TT mobile), Abkhazia (AQUafon-GSM) about MegaFon, see and South Ossetia (OSTELEKOM), they generate only 1% of the company website. our total consolidated revenues. Unless otherwise specifically The report is also indicated, this Annual Report provides consolidated financial and available online operational data www.AR2012.megafon.ru/en Approved Annual General Shareholders Meeting OJSC “MegaFon” Minutes dated 28.06.2013 Preliminarily Approved Board of Directors OJSC “MegaFon” Minutes № 192 (256) dated 14.05.2013 NATIONWIDE 4G AGREEMENT WITH NEW CAPEX LICENCE YOTA ON 4G NETWORK FRAMEWORK P.