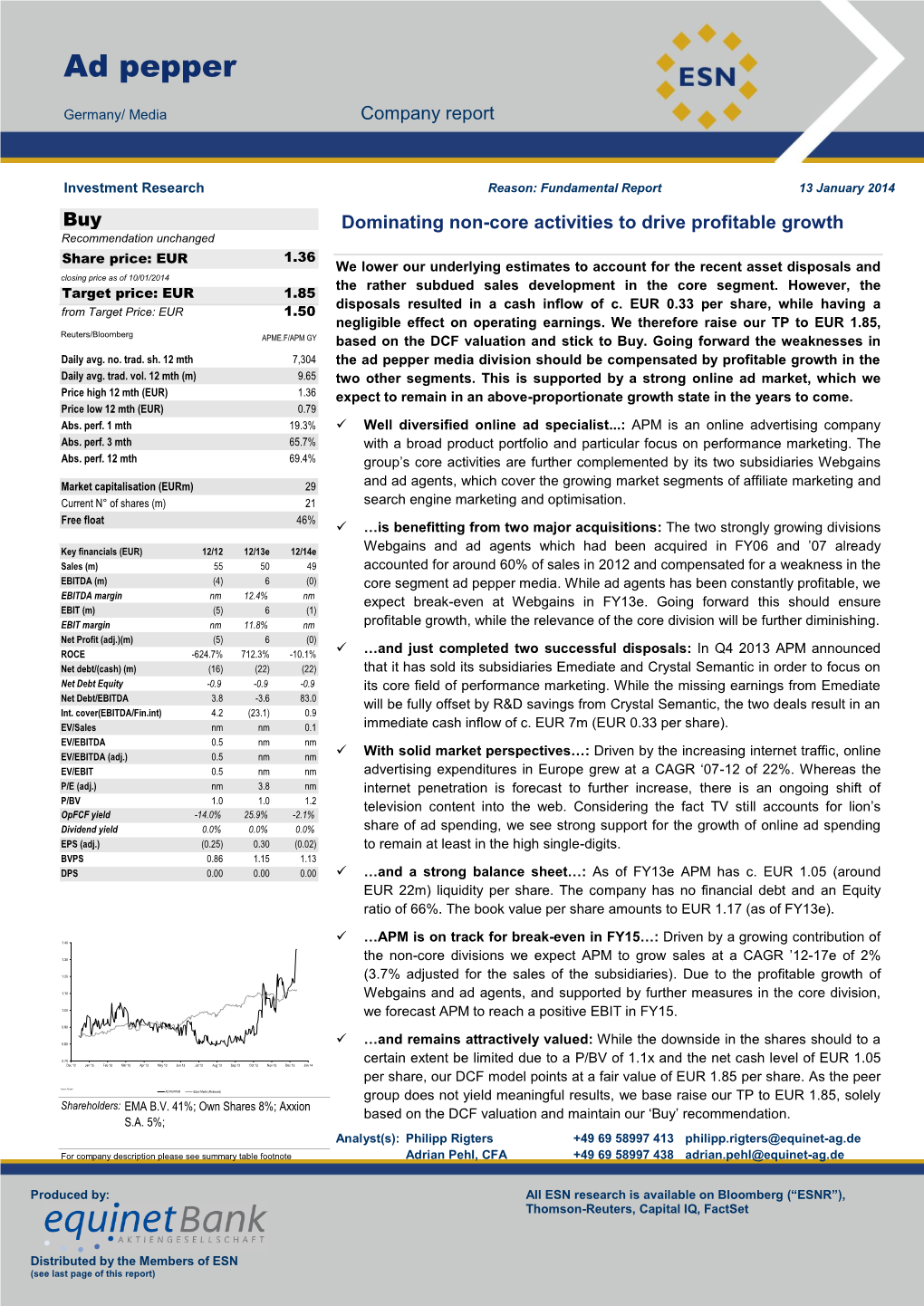

January 13, 2014, Adrian Pehl, CFA, Equinet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK-HFM Tupolev Tu-134 CSA -large OK on fin 91 2 £3 CC211 G-31-962 HP Jetstream 31 American eagle 92 2 £1 CC368 N4213X Douglas DC-6 Northern Air Cargo 88 4 £2 CC373 G-BFPV C-47 ex Spanish AF T3-45/744-45 78 1 £4 CC446 G31-862 HP Jetstream 31 American Eagle 89 3 £1 CC487 CS-TKC Boeing 737-300 Air Columbus 93 3 £2 CC489 PT-OKF DHC8/300 TABA 93 2 £2 CC510 G-BLRT Short SD-360 ex Air Business 87 1 £2 CC567 N400RG Boeing 727 89 1 £2 CC573 G31-813 HP Jetstream 31 white 88 1 £1 CC574 N5073L Boeing 727 84 1 £2 CC595 G-BEKG HS 748 87 2 £2 CC603 N727KS Boeing 727 87 1 £2 CC608 N331QQ HP Jetstream 31 white 88 2 £1 CC610 D-BERT DHC8 Contactair c/s 88 5 £1 CC636 C-FBIP HP Jetstream 31 white 88 3 £1 CC650 HZ-DG1 Boeing 727 87 1 £2 CC732 D-CDIC SAAB SF-340 Delta Air 89 1 £2 CC735 C-FAMK HP Jetstream 31 Canadian partner/Air Toronto 89 1 £2 CC738 TC-VAB Boeing 737 Sultan Air 93 1 £2 CC760 G31-841 HP Jetstream 31 American Eagle 89 3 £1 CC762 C-GDBR HP Jetstream 31 Air Toronto 89 3 £1 CC821 G-DVON DH Devon C.2 RAF c/s VP955 89 1 £1 CC824 G-OOOH Boeing 757 Air 2000 89 3 £1 CC826 VT-EPW Boeing 747-300 Air India 89 3 £1 CC834 G-OOOA Boeing 757 Air 2000 89 4 £1 CC876 G-BHHU Short SD-330 89 3 £1 CC901 9H-ABE Boeing 737 Air Malta 88 2 £1 CC911 EC-ECR Boeing 737-300 Air Europa 89 3 £1 CC922 G-BKTN HP Jetstream 31 Euroflite 84 4 £1 CC924 I-ATSA Cessna 650 Aerotaxisud 89 3 £1 CC936 C-GCPG Douglas DC-10 Canadian 87 3 £1 CC940 G-BSMY HP Jetstream 31 Pan Am Express 90 2 £2 CC945 7T-VHG Lockheed C-130H Air Algerie -

R Trader Instruments Cfds and Stocks

DE SHARES Ticker Company Ticker Company Ticker Company 1COV.DE COVESTRO AG FNTN.DE FREENET AG P1Z.DE PATRIZIA IMMOBILIEN AG AAD.DE AMADEUS FIRE AG FPE.DE FUCHS PETROLUB vz PBB.DE DEUTSCHE PFANDBRIEFBANK AG ACX1.DE BET-AT-HOME.COM AG FRA.DE FRAPORT AG FRANKFURT AIRPORTPFV.DE PFEIFFER VACUUM TECHNOLOGY ADJ.DE ADO PROPERTIES FRE.DE FRESENIUS PSM.DE PROSIEBENSAT.1 MEDIA SE ADL.DE ADLER REAL ESTATE AG G1A.DE GEA PUM.DE PUMA SE ADS.DE ADIDAS AG G24.DE SCOUT24 AG QIA.DE QIAGEN N.V. ADV.DE ADVA OPTICAL NETWORKING SE GBF.DE BILFINGER SE RAA.DE RATIONAL AFX.DE CARL ZEISS MEDITEC AG - BR GFT.DE GFT TECHNOLOGIES SE RHK.DE RHOEN-KLINIKUM AG AIXA.DE AIXTRON SE GIL.DE DMG MORI RHM.DE RHEINMETALL AG ALV.DE ALLIANZ SE GLJ.DE GRENKE RIB1.DE RIB SOFTWARE SE AM3D.DE SLM SOLUTIONS GROUP AG GMM.DE GRAMMER AG RKET.DE ROCKET INTERNET SE AOX.DE ALSTRIA OFFICE REIT-AG GWI1.DE GERRY WEBER INTL AG S92.DE SMA SOLAR TECHNOLOGY AG ARL.DE AAREAL BANK AG GXI.DE GERRESHEIMER AG SAX.DE STROEER SE & CO KGAA BAS.DE BASF SE HAB.DE HAMBORNER REIT SAZ.DE STADA ARZNEIMITTEL AG BAYN.DE BAYER AG HBM.DE HORNBACH BAUMARKT AG SFQ.DE SAF HOLLAND S.A. BC8.DE BECHTLE AG HDD.DE HEIDELBERGER DRUCKMASCHINENSGL.DE SGL CARBON SE BDT.DE BERTRANDT AG HEI.DE HEIDELBERGCEMENT AG SHA.DE SCHAEFFLER AG BEI.DE BEIERSDORF AG HEN3.DE HENKEL AG & CO KGAA SIE.DE SIEMENS AG BIO4.DE BIOTEST AG HLAG.DE HAPAG-LLOYD AG SIX2.DE SIXT SE BMW.DE BAYERISCHE MOTOREN WERKE AGHLE.DE HELLA KGAA HUECK & CO SKB.DE KOENIG & BAUER AG BNR.DE BRENNTAG AG HNR1.DE HANNOVER RUECK SE SPR.DE AXEL SPRINGER SE BOSS.DE HUGO BOSS -

DWS Equity Funds Semiannual Reports 2010/2011

DWS Investment GmbH DWS Equity Funds Semiannual Reports 2010/2011 ■ DWS Deutschland ■ DWS Investa ■ DWS Aktien Strategie Deutschland ■ DWS European Opportunities ■ DWS Intervest ■ DWS Akkumula : The DWS/DB Group is the largest German mutual fund company according to assets under management. Source: BVI. As of: March 31, 2011. 4/2011 DWS Deutschland DWS Investa DWS Aktien Strategie Deutschland DWS European Opportunities DWS Intervest DWS Akkumula Contents Semiannual reports 2010/2011 for the period from October 1, 2010, through March 31, 2011 (in accordance with article 44 (2) of the German Investment Act (InvG)) TOP 50 Europa 00 General information 2 Semiannual reports 2010 DWS Deutschland 4 DWS Investa 10 2011 DWS Aktien Strategie Deutschland 16 DWS European Opportunities 22 DWS Intervest 28 DWS Akkumula 36 1 General information Performance ing benchmarks – if available – are also b) any taxes that may arise in connec- The investment return, or performance, presented in the report. All financial tion with administrative and custodial of a mutual fund investment is meas - data in this publication is as of costs; ured by the change in value of the March 31, 2011. c) the costs of asserting and enforcing fund’s units. The net asset values per the legal claims of the investment unit (= redemption prices) with the addi- Sales prospectuses fund. tion of intervening distributions, which The sole binding basis for a purchase are, for example, reinvested free of are the current versions of the simpli- The details of the fee structure are set charge within the scope of investment fied and the detailed sales prospec - forth in the current detailed sales accounts at DWS, are used as the basis tuses, which are available from DWS, prospectus. -

Women-On-Board-Index

WOMEN‐ON‐BOARD‐INDEX III Aufsichtsräte (Stand 30.06.2011) powered by FidAR Zahl Anteil WoB-Index Posit Zahl AR- Unternehmen Notierung Frauen Frauen nur ion Mitgl. AR AR Aufsichtsräte 1 Biotest AG SDAX 6 3 50% 50,00% 1 Douglas Holding AG MDAX 16 8 50% 50,00% 3 HAMBORNER REIT SDAX 10 4 40% 40,00% 4 Deutsche Bank AG DAX 20 7 35% 35,00% 5 Amadeus Fire AG SDAX 6 2 33% 33,33% 5 Bechtle AG TecDAX 12 4 33% 33,33% 5 Beiersdorf AG DAX 12 4 33% 33,33% 5 centrotherm photovoltaics AG TecDAX 3 1 33% 33,33% 5 TAG Immobilien AG SDAX 6 2 33% 33,33% 10 Deutsche Post AG DAX 20 6 30% 30,00% 10 GfK SE SDAX 10 3 30% 30,00% 12 Commerzbank AG DAX 20 5 25% 25,00% 12 Fielmann AG MDAX 16 4 25% 25,00% 12 Fraport AG MDAX 20 5 25% 25,00% 12 Henkel AG & Co. KGaA DAX 16 4 25% 25,00% 12 Kabel Deutschland Holding AG MDAX 12 3 25% 25,00% 12 Merck KGaA DAX 16 4 25% 25,00% 12 Software AG TecDAX 12 3 25% 25,00% 12 Symrise AG MDAX 12 3 25% 25,00% 20 Axel Springer AG MDAX 9 2 22% 22,22% 20 Q-CELLS SE TecDAX 9 2 22% 22,22% 20 Sky Deutschland AG MDAX 9 2 22% 22,22% 20 STADA Arzneimittel AG MDAX 9 2 22% 22,22% 24 comdirect bank AG SDAX 5 1 20% 20,00% 24 Deutsche Telekom AG DAX 20 4 20% 20,00% 24 Hawesko Holding AG SDAX 5 1 20% 20,00% 24 Münchener Rück AG DAX 20 4 20% 20,00% 24 RHÖN-KLINIKUM AG MDAX 20 4 20% 20,00% 24 Siemens AG DAX 20 4 20% 20,00% 30 Praktiker Bau- und Heimwerkermärkte MDAX 16 3 19% 18,75% 30 TUI AG MDAX 16 3 19% 18,75% 32 adidas AG DAX 12 2 17% 16,67% 32 ADVA AG Optical Networking TecDAX 6 1 17% 16,67% 32 AIXTRON SE TecDAX 6 1 17% 16,67% 32 BASF SE DAX 12 2 17% -

WOMEN-ON-BOARD-INDEX I Aufsichtsrat Und Vorstand Powered by Fidar

WOMEN-ON-BOARD-INDEX I Aufsichtsrat und Vorstand powered by FidAR Positi Positi Zahl Zahl Anteil Zahl Zahl Anteil on on WoB- Unternehmen AR- Frauen Frauen Vorst.mi Frauen Frauen 31.3.2 14.1. Index Mitgl. AR AR tgl. Vorst. Vorst. 011 2011 Notierung Änderung 1 1 GfK SE SDAX 10 3 30% 6 3 50% ↔ 40,00% 2 2 Douglas Holding AG MDAX 16 8 50% 6 1 17% ↗ 33,33% 3 3 Deutz AG SDAX 12 1 8% 2 1 50% ↔ 29,17% 4 5 Biotest AG SDAX 6 3 50% 2 0 0% ↔ 25,00% 4 4 Q-Cells SE TecDAX 8 2 25% 4 1 25% ↘ 25,00% 4 5 Gerry Weber AG SDAX 6 1 17% 3 1 33% ↔ 25,00% 4 5 SKW Stahl-Metallurgie Holding AG SDAX 6 1 17% 3 1 33% ↔ 25,00% 8 8 Siemens AG DAX 20 4 20% 10 2 20% ↘ 20,00% 9 9 RHÖN-KLINIKUM AG MDAX 20 4 20% 7 1 14% ↔ 17,14% 10 10 Bechtle AG TecDAX 12 4 33% 3 0 0% ↔ 16,67% 10 36 Amadeus Fire AG SDAX 6 2 33% 2 0 0% ↗ 16,67% 10 10 TAG Immobilien AG SDAX 6 2 33% 2 0 0% ↔ 16,67% 10 10 Centrotherm photovoltaics AG TecDAX 3 1 33% 5 0 0% ↔ 16,67% 10 16 MorphoSys AG TecDAX 6 0 0% 3 1 33% ↗ 16,67% 15 13 Deutsche Bank AG DAX 20 6 30% 7 0 0% ↔ 15,00% 16 14 Drägerwerk AG & Co. KGaA TecDAX 12 1 8% 5 1 20% ↔ 14,17% 17 15 E.ON AG DAX 20 2 10% 6 1 17% ↔ 13,33% 18 16 Commerzbank AG DAX 20 5 25% 10 0 0% ↔ 12,50% 18 16 Deutsche Post AG DAX 20 5 25% 7 0 0% ↔ 12,50% 18 16 Fielmann AG MDAX 16 4 25% 4 0 0% ↔ 12,50% 18 16 Henkel AG & Co. -

Punctuality Statistics Economic Regulation Group Aviation Data Unit

Punctuality Statistics Economic Regulation Group Aviation Data Unit Birmingham, Gatwick, Glasgow, Heathrow, Luton, Manchester, Stansted Full and Summary Analysis August 1995 Disclaimer The information contained in this report will be compiled from various sources and it will not be possible for the CAA to check and verify whether it is accurate and correct nor does the CAA undertake to do so. Consequently the CAA cannot accept any liability for any financial loss caused by the persons reliance on it. Contents Foreword Introductory Notes Full Analysis – By Reporting Airport Birmingham Edinburgh Gatwick Glasgow Heathrow London City Luton Manchester Newcastle Stansted Full Analysis With Arrival / Departure Split – By A Origin / Destination Airport B C – E F – H I – L M – N O – P Q – S T – U V – Z Summary Analysis FOREWORD 1 CONTENT 1.1 Punctuality Statistics: Heathrow, Gatwick, Manchester, Glasgow, Birmingham, Luton, Stansted, Edinburgh, Newcastle and London City - Full and Summary Analysis is prepared by the Civil Aviation Authority with the co-operation of the airport operators and Airport Coordination Ltd. Their assistance is gratefully acknowledged. 2 ENQUIRIES 2.1 Statistics Enquiries concerning the information in this publication and distribution enquiries concerning orders and subscriptions should be addressed to: Civil Aviation Authority Room K4 G3 Aviation Data Unit CAA House 45/59 Kingsway London WC2B 6TE Tel. 020-7453-6258 or 020-7453-6252 or email [email protected] 2.2 Enquiries concerning further analysis of punctuality or other UK civil aviation statistics should be addressed to: Tel: 020-7453-6258 or 020-7453-6252 or email [email protected] Please note that we are unable to publish statistics or provide ad hoc data extracts at lower than monthly aggregate level. -

Punctuality Statistics Economic Regulation Group Aviation Data Unit

Punctuality Statistics Economic Regulation Group Aviation Data Unit Birmingham, Edinburgh, Gatwick, Glasgow, Heathrow, Luton, Manchester, Newcastle, Stansted Full and Summary Analysis August 1996 Disclaimer The information contained in this report will be compiled from various sources and it will not be possible for the CAA to check and verify whether it is accurate and correct nor does the CAA undertake to do so. Consequently the CAA cannot accept any liability for any financial loss caused by the persons reliance on it. Contents Foreword Introductory Notes Full Analysis – By Reporting Airport Birmingham Edinburgh Gatwick Glasgow Heathrow London City Luton Manchester Newcastle Stansted Full Analysis With Arrival / Departure Split – By A Origin / Destination Airport B C – E F – H I – L M – N O – P Q – S T – U V – Z Summary Analysis FOREWORD 1 CONTENT 1.1 Punctuality Statistics: Heathrow, Gatwick, Manchester, Glasgow, Birmingham, Luton, Stansted, Edinburgh, Newcastle and London City - Full and Summary Analysis is prepared by the Civil Aviation Authority with the co-operation of the airport operators and Airport Coordination Ltd. Their assistance is gratefully acknowledged. 2 ENQUIRIES 2.1 Statistics Enquiries concerning the information in this publication and distribution enquiries concerning orders and subscriptions should be addressed to: Civil Aviation Authority Room K4 G3 Aviation Data Unit CAA House 45/59 Kingsway London WC2B 6TE Tel. 020-7453-6258 or 020-7453-6252 or email [email protected] 2.2 Enquiries concerning further analysis of punctuality or other UK civil aviation statistics should be addressed to: Tel: 020-7453-6258 or 020-7453-6252 or email [email protected] Please note that we are unable to publish statistics or provide ad hoc data extracts at lower than monthly aggregate level. -

Süss Microtec

Süss MicroTec Germany/ Technology Hardware & Equipment Preview note Investment Research 1 May 2014 Hold 1Q14 preview – catching up with postponed revenues Recommendation unchanged Confirm ‘Hold’/PT EUR 8 Share price: EUR 7.00 The facts: Süss MicroTec (SMHN) will report 1Q14 figures on Thursday, May 8. closing price as of 30/04/2014 Target price: EUR 8.00 Our analysis: Please remember that SMHN booked relatively low 4Q13 sales of EUR Target Price unchanged 40.6m (down 27% yoy) and pointed to revenue recognition and shipping delays. For this reason, we forecast a solid top line March quarter and expect revenues of Reuters/Bloomberg SMHNn.DE/SMH GY EUR 34.5m, up 14.6% yoy as the company should be capable of compensating for Daily avg. no. trad. sh. 12 mth 29,088 the lost revenue terrain. Daily avg. trad. vol. 12 mth (m) 201.65 Price high 12 mth (EUR) 9.02 Please recall that SMHN has been shutting down its permanent bonder business. Price low 12 mth (EUR) 6.05 Some remaining tools shipped in this division will dilute the margin and in general, the Abs. perf. 1 mth 0.1% product mix should not allow for a strong gross result. Consequently, we forecast Abs. perf. 3 mth -3.3% a 1Q14 gross margin of 28.7%. Thanks to relative OPEX discipline, the EBIT loss Abs. perf. 12 mth -19.5% should come to ‘only’ EUR minus 1.2m. Market capitalisation (EURm) 134 We expect the 1Q14 net result to be released at EUR minus 1m. This would equal Current N° of shares (m) 19 an EPS of EUR minus 0.05. -

Equinet Analyser 20.01.2017

equinet Analyser 20.01.2017 Sales Desk Company Page Comments Aleksandar Bakrac Euromicron AG 2 Expanding IT security know-how by strategic acquisition (Buy) Tel.:Stefan +49 Bremer 69 58997 425 Tel.: +49 69 58997 426 Eugenia Belova Tel. +49 69 58997 417 Vlasta Edler JensTel.: +49Buchmüller 69 58997 181 Tel.: +49 69 58997 429 Lutz Kunert Achim Böckmann Tel.: +49 69 58997 436 Tel.: +49 69 58997 424 MarcWerner Schellenberger Fronk Tel.: +49 69 58997 404409 Alexander Kravkov GuidoTel.: +49 Schickentanz 69 58997 428 Tel.: +49 69 58997 407 Jan Neynaber Tel.: +49 69 58997 403 Michael Schuhmacher Tel.:Marc +49Schellenberger 69 58997 400 Tel.: +49 69 58997 404 GuidoEva Sonnenschein Schickentanz Tel.: +49 69 58997 407429 Marco Schumann Tel.:Patrick +49 Thielmann 69 58997 423 Tel.: +49 69 58997 405 Michael Schuhmacher AndreasTel.: +49 Wessel69 58997 400 HeinzTel.: +49 Zörgiebel 69 58997 423 Tel.: +49 69 58997 406 Heinz Zörgiebel Tel.: +49 69 58997 406 Statistics Index Closing 1 Day 1 Month 6 Months Ytd 52w High 52w Low DAX 11.597 0,0% 3,7% 17,6% 1,0% 11.692 8.699 MDAX 22.635 0,0% 5,6% 12,9% 2,0% 22.685 17.434 Tec-DAX 1.836 -0,1% 6,0% 12,6% 1,4% 1.860 1.464 SDAX 9.706 0,0% 4,0% 9,5% 2,0% 9.738 7.504 Bund-Future 163 -0,2% 1,2% -0,5% -0,7% 169 159 DAX Movers MDAX Movers Most up 1 Day Most dow n 1 Day Most up 1 Day Most dow n 1 Day Commerzbank AG 4,3% Vonovia SE -1,8% Schaeffler AG 4,1% Aurubis AG -3,7% Volksw agen AG Pref 1,0% ThyssenKrupp AG -1,6% Stroeer SE & Co. -

Equinet Bank Research

equinet Analyser 13.03.2017 Sales Desk Company Page Comments Aleksandar Bakrac Hypoport AG 2 Final Preliminary Q4 results (Buy) Tel.:Stefan +49 Bremer 69 58997 425 Tel.: +49 69 58997 426 Eugenia Belova WCM 3 DIC with blocking minority in WCM (Buy) Tel. +49 69 58997 417 Vlasta Edler JensTel.: +49Buchmüller 69 58997 181 Tel.: +49 69 58997 429 Lutz Kunert Achim Böckmann Tel.: +49 69 58997 436 Tel.: +49 69 58997 424 MarcWerner Schellenberger Fronk Tel.: +49 69 58997 404409 Alexander Kravkov GuidoTel.: +49 Schickentanz 69 58997 428 Tel.: +49 69 58997 407 Jan Neynaber Tel.: +49 69 58997 403 Michael Schuhmacher Tel.:Marc +49Schellenberger 69 58997 400 Tel.: +49 69 58997 404 GuidoEva Sonnenschein Schickentanz Tel.: +49 69 58997 407429 Marco Schumann Tel.:Patrick +49 Thielmann 69 58997 423 Tel.: +49 69 58997 405 Michael Schuhmacher HeinzTel.: +49 Zörgiebel 69 58997 400 HeinzTel.: +49 Zörgiebel 69 58997 406 Tel.: +49 69 58997 406 Statistics Index Closing 1 Day 1 Month 6 Months Ytd 52w High 52w Low DAX 11,963 -0.1% 1.3% 22.4% 4.2% 12,083 9,214 MDAX 23,325 0.2% 1.9% 16.0% 5.1% 23,711 18,853 Tec-DAX 1,968 1.0% 5.9% 21.4% 8.6% 1,971 1,490 SDAX 9,991 -0.1% 1.1% 12.5% 5.0% 10,193 8,312 Bund-Future 159 -0.6% -1.8% -4.8% -3.1% 169 159 DAX Movers MDAX Movers Most up 1 Day Most dow n 1 Day Most up 1 Day Most dow n 1 Day Commerzbank AG 5.8% Vonovia SE -1.9% Zalando SE 2.7% RTL Group S.A. -

11.04.12 MAX FN Again Raising Estimates and PT

Max Automation AG Germany/ Industrial Engineering Flash note Investment Research 12 April 2011 Buy Thriving demand should boost profitability – U/G estimates Recommendation unchanged In our recent meeting with CEO Bernd Priske our positive view for the stock was Share price: EUR 4.11 clearly confirmed. Continuously increasing and already record high demand is closing price as of 11/04/2011 THE right prerequisite for increasing profits and profitability going forward. The Target price: EUR 5.40 favourable environment should additionally be supported by positive effects of vs Target Price: EUR 4.80 the announced JV for substitute fuels with Thyssen AG. Besides higher volumes Reuters/Bloomberg we expect selective order intake to be the main driver for future profitability. MAXG.DE/MXH GR Hence we raise our estimates. This also leads us to raise our PT to EUR 5.4 (4.8) Daily avg. no. trad. sh. 12 mth 20,631 whilst we reiterate our Buy recommendation on the stock. Daily avg. trad. vol. 12 mth (m) 0.06 Price high 12 mth (EUR) 4.25 Base orders are developing strongly whilst larger orders are coming back too : Ac- Price low 12 mth (EUR) 2.58 cording to recent announcements, MAX continues to benefit from a strong market en- Abs. perf. 1 mth 5.9% vironment. A strong and rising oil price bodes well for demand of Vecoplan products Abs. perf. 3 mth 16.7% such as shredder and sorting equipment as it becomes more and more important to Abs. perf. 12 mth 53.8% elude high energy prices by building up solutions for energy generation by substitute Market capitalisation (EURm) 110 fuel., In particular the highly energy intensive global cement/limestone industry is ask- Current N° of shares (m) 27 ing for the solutions offered by subsidiary Vecoplan. -

Studieninformationstag 2010

Investor relations 2.0 – An international benchmark study Kristin Koehler, M.A. University of Leipzig | Institute of Communication and Media Studies | August 2011 1 / Kristin Koehler | University of Leipzig | www.communicationmanagement.de Content Outline of the study Research design Empirical insights Best practices Summary of findings 2 / Kristin Koehler | University of Leipzig | www.communicationmanagement.de Outline of the study _ Online content analysis of top 30 listed businesses in the United States (Dow Jones Industrial Average), Germany (DAX), UK (FTSE), France (CAC) and Japan (Nikkei) _ In addition, comparison of the IR 2.0 engagement of German companies listed in DAX, MDAX, TecDAX and SDAX _ Longitudinal design for German and U.S. indices: first IR 2.0 study conducted in 2009 (see DIRK research edition, vol. 17, Köhler, K. (2010): Investor relations and social media) _ Organized by the University of Leipzig, Kristin Koehler, M.A. _ Thanks to Melanie Gerasch and Isabel Reinhardt for their support 3 / Kristin Koehler | University of Leipzig | www.communicationmanagement.de Outline of the study Aims and focus _ Monitoring the status quo in the field of investor relations 2.0 in an international context _ Identifying trends and developments for German and U.S. businesses _ Identifying best practices _ Comparing use of social media for IR purposes in different countries and cultural settings 4 / Kristin Koehler | University of Leipzig | www.communicationmanagement.de Research design _ Online content analysis of 280 listed companies