DECENT Work, a Recipe for Growth a Market SYSTEM Analysis Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![World Oil Exports [01] Angola Some History Production](https://docslib.b-cdn.net/cover/6341/world-oil-exports-01-angola-some-history-production-106341.webp)

World Oil Exports [01] Angola Some History Production

The Oil Drum: Europe | World Oil Exports [01] Angola http://europe.theoildrum.com/node/4184 World Oil Exports [01] Angola Posted by Luis de Sousa on July 1, 2008 - 10:00am in The Oil Drum: Europe Topic: Supply/Production Tags: angola, exports, oil exports, original, woe, world oil exports [list all tags] Angola is one of the few oil producing countries with a bright future ahead. Decades of war prevented the country from developing it's energy resources properly, but is now becoming one of the largest world oil exporters in a period of rampant prices. Just as if Fortune decided to compensate Angola for its misfortunes during the XX century. Becoming an OPEC member just recently, Angola is set to build one of the strongest economies in Africa, with its GDP growing over 30% 15% annually (numbers here), one of the highest rates in the world. Hopefully Oil will be just the trigger of a golden era in a country that possesses other important natural resources. 17 diggs digg it Some History To read a not so short History of Angola, click here. Production Colin Campbell first assessed Angola in December of 2003 in ASPO's newsletter 36. Back then it was already clear that the Regular Oil cycle was approaching peak (if not already past it). It was also clear that Deep Water fields were coming strongly on stream promising to more than double the country's production. Using 10 Gb for both Regular Oil and Deep Water ultimates, the best estimate was resulting in a total production peak by 2020 just under 2 Mb/d. -

The Winning of the Carbon War

JEREMY LEGGETT THE WINNING OF THE CARBON WAR POWER AND POLITICS ON THE FRONT LINES OF CLIMATE AND CLEAN ENERGY THE WINNING OF THE CARBON WAR POWER AND POLITICS ON THE FRONT LINES OF CLIMATE AND CLEAN ENERGY JEREMY LEGGETT The Winning of The Carbon War © Jeremy Leggett 2015. This work is licensed under the Creative Commons Attribution-ShareAlike 4.0 International License. To view a copy of this license, visit http:// creativecommons.org/licenses/by-sa/4.0/ or send a letter to Creative Commons, PO Box 1866, Mountain View, CA 94042, USA. This first edition published 2016 by Jeremy Leggett. Colophon Set in Minion Pro, 11pt on 14pt leading. For Aki Humanity is in a race, a kind of civil war. On the light side the believers in a sustainable future based on clean energy fight to save us from climate change. The dark side defends the continuing use of fossil fuels, often careless of the impact it has on the world. Jeremy Leggett fought for the light side for a quarter of a century as it lost battle after battle. Then, in 2013, the tide began to turn. By 2015, it was clear the the war could be won. Leggett’s front-line chronicle tells one person’s story of those turnaround years, culminating in dramatic scenes at the Paris climate summit, and what they can mean for the world. iv “Given how vital developments in energy and climate will be for the future global economy, a front-line chronicle of events as they unfold in the make-or-break year ahead promises to be fascinating. -

ISSN 2221-2698 Arkhangelsk, Russia DOI 10.17238/Issn2221-2698.2016

ISSN 2221-2698 Arkhangelsk, Russia DOI 10.17238/issn2221-2698.2016.25 Arctic and North. 2016. N 25 2 ISSN 2221-2698 Arctic and North. 2016. N 25. CC BY-SA © Northern (Arctic) Federal University named after M.V. Lomonosov, 2016 © Editorial board of electronic scientific journal “Arctic and North”, 2016 The journal “Arctic and North” is registered at Roskomnadzor as an internet periodical issued in Russian and English, Registration certificate El № FS77-42809, November 26, 2010; at the system of the Russian Science Citation Index (RSCI), license contract № 96-04/2011R, April 12, 2011; Scientific Electronic Library "Сyberleninka" (2016); in the catalogs of international databases: Directory of Open Access Journals — DOAJ (2013); Global Serials Directory Ulrichsweb, USA (2013); NSD, Norway (2015); InfoBase Index, India (2015); ERIH PLUS, Norway (2016). The Journal is issued not less than 4 times per year; 25 issues were published in 2011—2016. The Founder — Northern (Arctic) Federal University named after M.V. Lomonosov (Arkhangelsk, Russia). Editor-in-Chief — Yury F. Lukin, Doctor of Historical Sciences, Professor, Honorary Worker of the higher education of the Russian Federation. All journal issues are available free of charge in Russian and English. Rules and regulations on submission, peer reviews, publication and the Declaration of Ethics are available at: http://narfu.ru/aan/rules/ The Journal is devoted to the scientific articles focused on the Arctic and the North relevant for the following professional degrees: 08.00.00 Economics; 22.00.00 Sociology; 23.00.00 Political science; 24.00.00 Culturology. No payments for publication are collected from authors, including students and post-graduate students. -

Update on Megaproject Megaproject

The Oil Drum | Update on Megaproject Megaproject http://www.theoildrum.com/node/3347 Update on Megaproject Megaproject Posted by Stuart Staniford on December 10, 2007 - 11:00am Topic: Supply/Production Tags: megaprojects, peak oil, plateau [list all tags] New liquids capacity with first oil in each year as estimated from Petroleum Review megaproject reports (last available estimate in each case), and interim estimates from Wikipedia table as of December 10th, 2007. Error bars on Petroleum Review figures are as documented in Is the Decline of Base Production Accelerating. The Wikipedia Oil Megaprojects task force (Khebab, Ace, and I) has been busy over the last few weeks. With some assistance from helpful strangers, we have been ploughing through press releases and annual reports, adding projects to the Wikipedia page on Oil Megaprojects. I introduced this project two weeks ago, and today I want to give an interim progress report. As of now, we've reached about 350 citations used in collating the information. I have mainly been working on the past - the years 2003-2006 - while the years from 2007 onwards have mainly been handled by Ace and Khebab (though there is some crossover both ways). The 2003-2006 projects, of which there are currently 108, depend on about 140 citations. In attempting to assure completeness and quality of the list, I have reviewed the 2003-2006 annual reports, and/or all press releases, for the following companies: Anadarko Apache Page 1 of 7 Generated on September 1, 2009 at 2:51pm EDT The Oil Drum | Update on Megaproject -

Peak Oil Strategic Management Dissertation

STRATEGIC CHOICES FOR MANAGING THE TRANSITION FROM PEAK OIL TO A REDUCED PETROLEUM ECONOMY BY SARAH K. ODLAND STRATEGIC CHOICES FOR MANAGING THE TRANSITION FROM PEAK OIL TO A REDUCED PETROLEUM ECONOMY BY SARAH K. ODLAND JUNE 2006 ORIGINALLY SUBMITTED AS A MASTER’S THESIS TO THE FACULTY OF THE DIVISION OF BUSINESS AND ACCOUNTING, MERCY COLLEGE IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION, MAY 2006 TABLE OF CONTENTS Page LIST OF ILLUSTRATIONS AND CHARTS v LIST OF TABLES vii PREFACE viii INTRODUCTION ELEPHANT IN THE ROOM 1 PART I THE BIG ROLLOVER: ONSET OF A PETROLEUM DEMAND GAP AND SWITCH TO A SELLERS’ MARKET CHAPTER 1 WHAT”S OIL EVER DONE FOR YOU? (AND WHAT WOULD HAPPEN IF IT STOPPED DOING IT?) 5 Oil: Cheap Energy on Demand - Oil is Not Just a Commodity - Heavy Users - Projected Demand Growth for Liquid Petroleum - Price Elasticity of Oil Demand - Energy and Economic Growth - The Dependence of Productivity Growth on Expanding Energy Supplies - Economic Implications of a Reduced Oil Supply Rate CHAPTER 2 REALITY CHECK: TAKING INVENTORY OF PETROLEUM SUPPLY 17 The Geologic Production of Petroleum - Where the Oil Is and Where It Goes - Diminishing Marginal Returns of Production - Hubbert’s Peak: World Oil Production Peaking and Decline - Counting Oil Inventory: What’s in the World Warehouse? - Oil Resources versus Accessible Reserves - Three Camps: The Peak Oilers, Official Agencies, Technology Optimists - Liars’ Poker: Got Oil? - Geopolitical Realities of the Distribution of Remaining World -

Universidade De São Paulo Instituto De Energia E Ambiente Programa De Ciência Ambiental-Procam

UNIVERSIDADE DE SÃO PAULO INSTITUTO DE ENERGIA E AMBIENTE PROGRAMA DE CIÊNCIA AMBIENTAL-PROCAM GINNETH PULIDO GÓMEZ EXPLORACIÓN DE PETRÓLEO EN EL ÁREA DE LA NUEVA FRONTERA COLOMBIA – NICARAGUA: APROXIMACIÓN GEOPOLÍTICA SÃO PAULO 2017 GINNETH PULIDO GÓMEZ EXPLORACIÓN DE PETROLEO EN EL ÁREA DE LA NUEVA FRONTERA COLOMBIA – NICARAGUA: APROXIMACION GEOPOLÍTICA Dissertação de Mestrado apresentada ao Programa de Pós-graduação em Ciência Ambiental do Instituto de Energia e Ambiente da Universidade de São Paulo para a obtenção do título de Mestre em Ciência Ambiental Orientador: Prof. Dr. Wagner Costa Ribeiro VERSÃO ORIGINAL SÃO PAULO 2017 AUTORIZO A REPRODUÇÃO E DIVULGAÇÃO TOTAL OU PARCIAL DESTE TRABALHO, POR QUALQUER MEIO CONVENCIONAL OU ELETRÔNICO, PARA FINS DE ESTUDO E PESQUISA, DESDE QUE CITADA A FONTE. FICHA CATALOGRÁFICA PULIDO-GÓMEZ, Ginneth. Exploração de Petróleo na área da nova fronteira Colômbia-Nicarágua: Aproximação Geopolítica./ Ginnteh Pulido -Gómez; orientador Wagner Costa Ribeiro. – São Paulo, 2017. 138 f : il.; 30 cm. Dissertação (Mestrado em Ciência Ambiental) – Programa de Pós- Graduação em Ciência Ambiental – Instituto de Energia e Ambiente da Universidade de São Paulo. 1. Petróleo. 2. Geopolítica. I. Título. Nome: Pulido Gómez Ginneth Título: Exploração de Petróleo na área da Nova Fronteira Colômbia – Nicarágua: Aproximação Geopolítica. Dissertação de Mestrado apresentada ao Programa de Pós-graduação em Ciência Ambiental do Instituto de Energia e Ambiente da Universidade de São Paulo para a obtenção do título de Mestre em Ciência Ambiental Aprovada em: Banca examinadora: Professor Instituição: Julgamento Assinatura Professor Instituição: Julgamento Assinatura Professor Instituição: Julgamento Assinatura “Me estremecieron mujeres que la historia anotó entre laureles Y otras desconocidas gigantes que no hay libro que las aguante” S. -

Recent Developments a 'Unique' Victory for Iranians: Rouhani

WWW.TEHRANTIMES.COM I N T E R N A T I O N A L D A I L Y 16 Pages Price 20,000 Rials 1.00 EURO 4.00 AED 39th year No.13242 Sunday OCTOBER 28, 2018 Aban 6, 1397 Safar 18, 1440 Larijani congratulates Zionist regime seeks Esteghlal set to sack Director Ghaffarzadeh new Iraqi PM division among Muslim Winfried Schaefer: working on co-production 2 countries 2 report 15 between Iran and Turkey 16 Iran-EU financial channel to be See page 2 opened soon: CBI governor ECONOMY TEHRAN – Governor of bilateral monetary treaty between the deskof the Central Bank of two sides. The treaty aims to help Iranian Iran (CBI) announced on Saturday that a and European companies and entrepre- new financial channel is soon to be opened neurs to establish and maintain business between Iran and the EU nations, Tasnim relations with each other. news agency reported. EU powers, namely France, Germany Abdolnaser Hemmati made the announce- and Britain, and Iran have been in talks ment on social media, “The details of the Euro- over launching this payments channel pean Special Purpose Vehicle (SPV) for trade for months, which would enable Euro- between Iran and the EU were discussed at pean companies to trade with Iran as a meeting in Brussels last week.” part of efforts to defy U.S. sanctions The official emphasized that the dis- and keep alive a landmark nuclear deal cussed financial channel is in fact some sort with Tehran. WTTC ranks Iran’s tourism 20th Recent developments among 185 in 2011-17 TOURISM TEHRAN — Iran’s investment that is based on absolute growth deskbudding travel sector has seen between 2011 and 2017. -

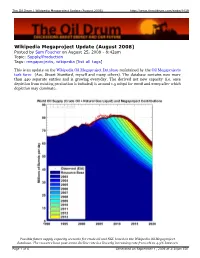

Wikipedia Megaproject Update (August 2008)

The Oil Drum | Wikipedia Megaproject Update (August 2008) http://www.theoildrum.com/node/4419 Wikipedia Megaproject Update (August 2008) Posted by Sam Foucher on August 25, 2008 - 8:42am Topic: Supply/Production Tags: megaprojects, wikipedia [list all tags] This is an update on the Wikipedia Oil Megaproject Database maintained by the Oil Megaprojects task force (Ace, Stuart Staniford, myself and many others). The database contains now more than 440 separate entries and is growing everyday. The derived net new capacity (i.e. once depletion from existing production is included) is around 1.5 mbpd for 2008 and 2009 after which depletion may dominate. Possible future supply capacity scenario for crude oil and NGL based on the Wikipedia Oil Megaproject database. The resource base post-2002 decline rate is a linearly increasing rate from 0% to 4.5% between 2003 and 2008 then constant at 4.5% afterward. The decline rate for each annual addition is 4.5% after first Page 1 of 6 Generated on September 1, 2009 at 2:20pm EDT The Oil Drum | Wikipedia Megaproject Update (August 2008) http://www.theoildrum.com/node/4419 2003 and 2008 then constant at 4.5% afterward. The decline rate for each annual addition is 4.5% after first year. The observed data points are the monthly crude oil + NGL estimates from the EIA. Here is the last compilation of new supply peak contributions stacked according to their projected first oil year: update: Ace has also produced this chart yesterday (Click to enlarge): Below is the evolution of this chart since the database creation. -

Peak Oil and Australia's National Infrastructure

1 PEAK OIL AND AUSTRALIA’S NATIONAL INFRASTRUCTURE SUBMISSION TO INFRASTRUCTURE AUSTRALIA Australian Association for the Study of Peak Oil and Gas October 2008 We need to leave oil before it leaves us. Dr Fatih Birol, Chief Economist, International Energy Agency, 2008 The era of procrastination, of half-measures, of soothing and baffling expedients, of delays, is coming to its close. In its place we are entering a period of consequences. Winston Churchill, 1936 Peak Oil and Australia’s National Infrastructure ASPO-Australia i Contents Contents i About ASPO-Australia ii Executive Summary iii Introduction 1 The Peak in World Oil Production 1 Implications for the World Economy 7 Socio-economic Implications for Australia 8 Infrastructure Australia’s Goals and Strategic Priorities 10 Energy Infrastructure 11 Transport Infrastructure 12 Conclusion 15 List of Figures 1. World Oil Production vs Discovery, Regular Conventional Oil 1 2. World Oil & Gas Depletion Profiles, ASPO 2007 Base Case 3 3. World Oil Production, 1980-2008 4 4. Oil Megaprojects Database, Moderate Decline Rate Scenario 5 5. World Oil Exports, 1965-2020 6 6. Australian Oil Production vs Demand, 1970-2030 9 Peak Oil and Australia’s National Infrastructure ASPO-Australia ii About ASPO-Australia ASPO-Australia is a non-partisan network of professionals working to reduce Australia’s oil vulnerability, by bringing the probabilities, risks and opportunities presented by peak oil to the attention of decision-makers. Our membership includes scientists, geologists, engineers, transport and urban planners and a wide range of other professionals, comprising working groups focusing on the implications of peak oil on different sections of the community and the economy. -

Crude Oil and Liquids Capacity Additions: 2011-2015

The Oil Drum | Crude Oil and Liquids Capacity Additions: 2011-2015 http://www.theoildrum.com/node/7785 Crude Oil and Liquids Capacity Additions: 2011-2015 Posted by Sam Foucher on April 13, 2011 - 8:39pm This is a guest post by J. Michael Bodell and myself. Michael is currently an energy consultant operating as Aperio Energy Research. Mr. Bodell is the in-house expert on oil and natural gas market fundamentals for Strategic Energy Research & Capital, LLC, a specialized brokerage and investment firm. He worked for CERA from 2005 to 2007 and was the architect and lead project manager for a two-phase multi-client report, "Diminishing Returns: The Cost of North American Gas Supply in an Unconventional Era," a body of work that evaluated the all-in, full- cycle cost structure of about 275 supply basins. In 2008 as a consultant, he was the lead author on a CERA decision brief research paper, "Natural Gas Yield Curve: A Powerful Tool for Natural Gas Market Analysis." Prior to CERA and SERC, Mr. Bodell was the strategic planning manager for Unocal Midstream & Trade, where he lead a team to perform oil, gas and power market fundamentals and strategy evaluation in underground natural gas storage development. This analysis is designed to demonstrate why we believe that productive capacity relative to consumption will be sufficiently tight over the next several years to elevate crude prices to the investment cost of the marginal unit, about $100 per barrel. In fact, if annual non-OECD demand continues to grow at 3.5 percent or 1.4 Mb/d per annum, we expect another episode of deficit comparative inventory that will elevate spot prices above this mid-cycle price. -

Peak Oil and Our Future How Energy Depletion Will Change Our Lives

Peak Oil and Our Future How Energy Depletion Will Change Our Lives by Doug Craft [email protected] Updated March 2013 © 2013Charles Douglas Craft Image Sources (ASPO Spain 2002, DOE 2004, EIA 2007b) Peak Oil and Our Future How Energy Depletion Will Change Our Lives by Doug Craft [email protected] Doug's Resume Art: http://www.dougcraftfineart.com Original June 2007 – Updated March 2013 © 2013 Charles Douglas Craft SUMMARY Peak Oil and declining energy supplies represent the most serious crisis we have ever faced as a species. Current world population and our relatively luxurious way of life in America are completely dependent on cheap and readily available energy. Our civilization has developed over the past 150 years because we have discovered and exploited abundant – but finite – fossil fuels for cheap energy. Coal, oil, and natural gas were formed millions of years ago, and our use of this one-time planetary energy endowment has significantly increased food production and has led to exponential population growth. Cheap energy has produced social progress and technological wonders, but it has also allowed our population to expand seriously beyond the ability of the earth's natural (non-fossil fuel) carrying capacity. Production of all finite natural resources over time follows a bell-shaped curve of increasing production, peaking maximum production, and then decreasing production. Unfortunately, this behavior is a fundamental property of nature and the laws of thermodynamics. While there's a large amount of underground oil remaining in the world, we have already used the higher quality and easy to produce half of known reserves and are at or very near the ultimate peak of world production – Peak Oil. -

Media Log 2014 August/September Featured Media Hits Print News

Media Log 2014 August/September Featured Media Hits State Impact PA (NPR) - Transparency about fracking chemicals remains elusive http://stateimpact.npr.org/pennsylvania/2014/08/07/transparency-about-fracking-chemicals-remains- illusive/ Interview with David Manthos and Paul Woods National Journal - Watch Six Months of Fracking Fires Blaze Across the Country http://www.nationaljournal.com/energy/watch-six-months-of-fracking-fires-blaze-across-the-country- 20140822 Discusses and links to SkyTruth’s Global Flaring Map Observer-Reporter - SkyTruth maps impoundments using aerial photos http://www.observer-reporter.com/article/20140920/NEWS01/140929969#.VCRTgPldW4c Features interview with David about our PA Impound Pond mapping project Print News/Web Sites 8/4/2014 EcoWatch - Sand Mining Takes Toll on Wisconsin As Fracking Escalates Nationwide http://ecowatch.com/2014/08/04/sand-mining-toll-on-wisconsin-fracking-escalates/ Repost of SkyTruth’s blog of 8/4 The Ecologist - Fracking - US companies and regulators must disclose environmental data http://www.theecologist.org/blogs_and_comments/commentators/2503450/fracking_us_companies_a nd_regulators_must_disclose_environmental_data.html Features image by SkyTruth 8/6/2014 EcoWatch - Massive Spill at Canadian Gold Mine Detected By Satellite http://ecowatch.com/2014/08/06/spill-canadian-gold-mine-satellite/ Repost of SkyTruth’s blog of 8/6 Dear President Obama Film http://www.dearpresidentobamafilm.com/state/west-virginia/ Features images by SkyTruth and a link to our website 8/7/2014 State Impact