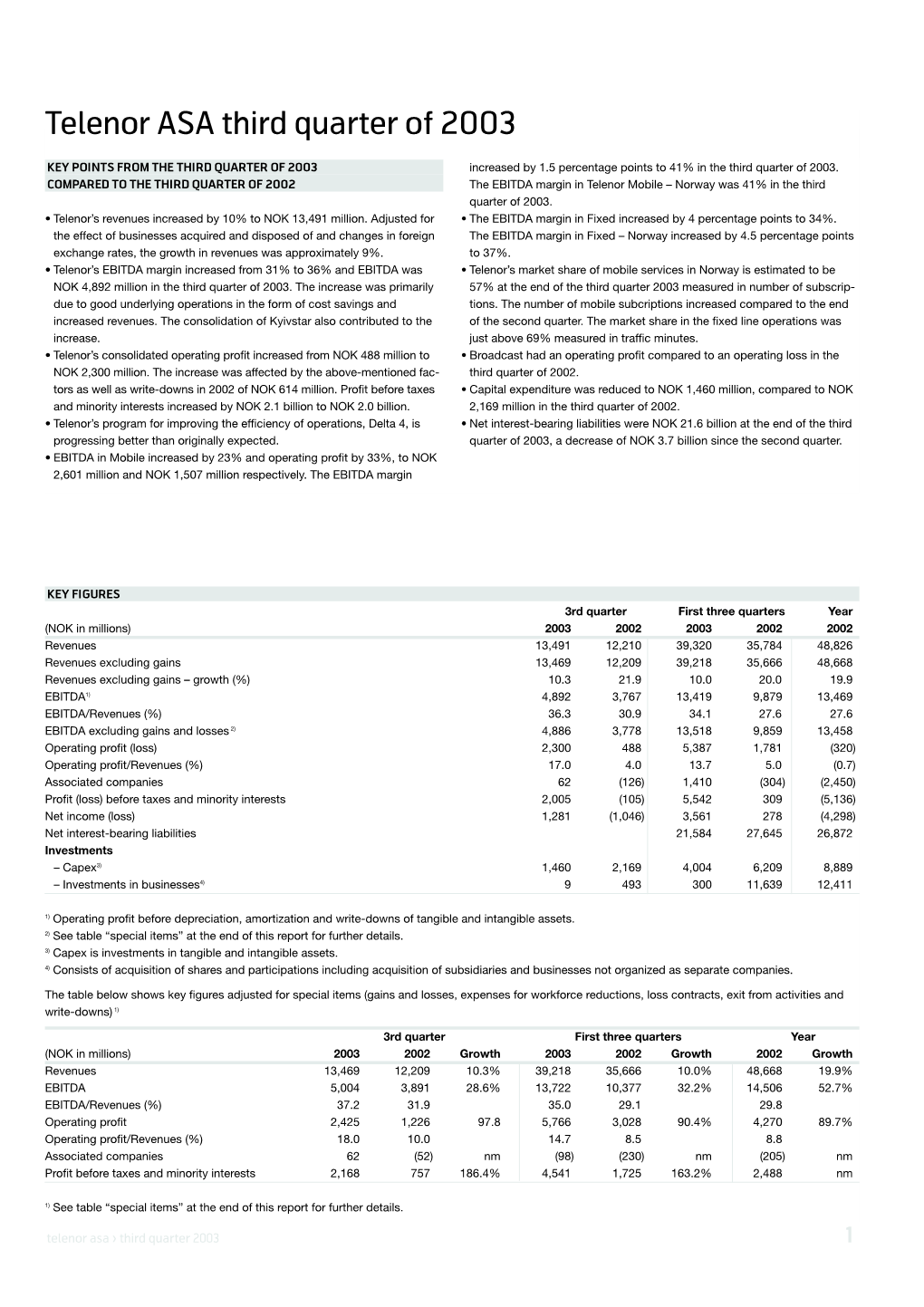

Telenor ASA Third Quarter of 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download PDF Dossier

Halberd Bastion Pty Ltd ABN: 88 612 565 965 58 Latrobe Terrace, Brisbane Queensland, Australia, 4064 [email protected] Research Dossier: VEON (VimpelCom) Headquarters Netherlands Company Name VEON Ltd. Ownership Type Publicly Traded Company Ownership/Controlling Entities Telenor Group Website https://veon.com/ Company Overview VEON, previously known as VimpelCom, is an international communications and technology company driven by a vision to unlock new opportunities for our customers as they navigate the digital world. Present in some of the world's most dynamic markets, VEON provides more than 235 million customers with voice, fixed broadband, data and internet services. VEON offers services to customers in 13 markets including Russia, Italy, Algeria, Pakistan, Uzbekistan, Kazakhstan, Ukraine, Bangladesh, Kyrgyzstan, Tajikistan, Armenia, Georgia, and Laos. VEON operates under the “Beeline”, “Kyivstar”, “WIND 3”, “Jazz”, “banglalink”, and “Djezzy” brands. VEON is headquartered in Amsterdam, the Netherlands, and is traded on the NASDAQ Global Select Market and Euronext Amsterdam under the symbol "VEON". Groups Under Direction The company maintains a significant controlling stake in 1 group companies globally. Group companies are those maintaining a parent relationship to individual subsidiaries and/or mobile network operators. Global Telecom Holding Headquarters: Netherlands Type: Publicly Traded Company, Subsidiary Subsidiaries The company has 8 subsidiaries operating mobile networks. Beeline Armenia Country: Armenia 3G Bands: -

Tourist World Sim EN 640517

SIM Card User Guide for Happy Tourist World SIM *This SIM card is sold outside China. Happy Tourist World SIM COVERAGE IN FREE TOLL-FREE 38 COUNTRIES 10-DAY DATA CALL CENTER GB 24hours 3coun8tries 4 Data SIM card with Free 10-day unlimited data Toll-free call center coverage in 38 countries with 4 GB at max speed (24 hours) while abroad at +66-2-202-8100 SIM Card User Guide 1 2 3 4 SMS Insert SIM card Mobile phone is automatically Refer to SMS for Ready, let’s GO! into phone connected to usage instruction *SIM card only activates in operator’s network participated countries Country Operator Operator Name Displayed on Screen Bangladesh Grameerphone BGDGP / Grameenphone Asia Cambodia CamGSM Cellcard / MobiTel / KHM-MobiTel / 456-01 Metfone metfone / KHM08 / 456 08 China China Mobile CMCC / China Mobile HongKong Smar Tone SmarTone HK / SMC HK India IDEA IDEA / INA 04 / 404 04 Vodafone Vodafone IN / 404 05 / INA 05 Airtel airtel Indonesia XL Axiata XL / 51011 Israel Cellcom IL Cellcom /425 02 / IL 02 Laos Lao Telecom LAO GSM / 457 01 Unitel Unitel / LATMOBIL / 45703 Macau SmarTone MAC SmarTone MAC / SMC MAC MalaysiaLaos Digi DiGi / DiGi 1800 / MYMT18 Celcom Celcom / MY Celcom / 502 19 Myanmar Telenor Telenor / 414 06 / TM 2G / TM 3G Pakistan Telenor Telenor PK / 410 06 Philippines Globe GLOBE / PH GLOBE / 515 02 SMART Smart Gold / SMART / 515 03 Qatar Ooredoo Ooredoo / Qtel / 427 01 Singapore SingTel Singtel / Singtel-G9 StarHub STARHUB / SGP05 / 525-05 South Korea KT (Olleh) olleh / KT / 450 08 SK Telecom 450 05 / SK Telecom / KOR SK Telecom -

Form F-20 2001, 1.39 MB

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F n REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ≤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2001 OR n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission file number: 0-31054 Telenor ASA (Exact name of Registrant as specified in its charter) Norway (Jurisdiction of incorporation or organization) Snarøyveien 30, N-1333 Fornebu, Norway (Address of principal executive offices) Securities registered or to be registered pursuant to Section 12(b) of the Act: None Securities registered or to be registered pursuant to Section 12(g) of the Act: Ordinary Shares, nominal value NOK 6 per share Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2001: 1,772,730,652 Ordinary Shares of NOK 6 each. Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes X No Indicate by check mark which financial statement item the registrant has elected to follow. -

Årsrapport 2010

Telenor Årsrapport 2010 Årsrapport Telenor built around people Årsrapport 2010 Growth comes from truly understanding the needs of people, to drive relevant change www.telenor.com /SIDE 113/ TELENOR årsraPPORT 2010 Telenor-konsernets mobilvirksomheter Uninor – India Innhold Telenor – Pakistan Telenor har en 67,25 % eierandel Til aksjonærene /01/ Telenor eier 100 % av Telenor i Uninor i India, som lanserte sine i Pakistan, som er landets nest tjenester i desember 2009. Årsberetning 2010 /02/ største mobiloperatør. Årsregnskap Telenor – Norge Grameenphone Telenor Konsern Telenor er Norges ledende – Bangladesh tilbyder av telekommunikasjon. Telenor har en 55,8 % eierandel i Resultatregnskap /16/ Grameenphone, som er den største mobiloperatøren i Bangladesh. Oppstilling av totalresultat /17/ Grameenphone er notert på Dhaka Oppstilling av finansiell stilling /18/ Stock Exchange (DSE) Ltd. og Chittagong Telenor – Sverige Stock Exchange (CSE) Ltd. OppstillingTelenor av eier kontantstrømmmer 100 % av Telenor /19/ i Sverige, som er landets tredje Oppstillingstørste av mobiloperatør. endringer i egenkapital /20/ Noter til konsernregnskapet /21/ Telenor ASA Resultatregnskap /90/ Oppstilling av totalresultat /91/ dtac – Thailand Telenors finansielle eksponering Oppstilling av finansiell stilling /92/ i Dtac er 65,5 %. dtac er den nest Telenor – Danmark største mobiloperatøren i Thailand Oppstilling av kontantstrømmmer /93/ og er børsnotert i Thailand og Telenor eier 100 % av Telenor Singapore. Oppstillingi Danmark, av endringersom er landets nest i egenkapital /94/ Noter tilstørste regnskapet mobiloperatør. /95/ Erklæring fra styret og daglig leder /108/ Revisjonsberetning for 2010 /109/ Uttalelse fra bedriftsforsamlingen i Telenor ASA /111/ Finansiell kalender 2011 /111/ DiGi – Malaysia Telenor – Ungarn Telenor har en 49 % eierandel i DiGi, Telenor eier 100 % av Telenor den tredje største mobiloperatøren i Ungarn, som er landets nest i Malaysia. -

Telenor ASA – EMTN Base Prospectus 28 June 2013

Base Prospectus Telenor ASA (incorporated as a limited company in the Kingdom of Norway) €7,500,000,000 Debt Issuance Programme Under the Debt Issuance Programme described in this Base Prospectus (the Programme), Telenor ASA (the Issuer or Telenor) may from time to time issue debt securities (the Notes). The aggregate nominal amount of Notes outstanding will not at any time exceed €7,500,000,000 (or the equivalent in other currencies), subject to compliance with all relevant laws, regulations and directives. Notes may be issued in bearer form only (Bearer Notes), in registered form only (Registered Notes) or in uncertificated book entry form cleared through the Norwegian Central Securities Depository, the Verdipapirsentralen (VPS Notes and the VPS respectively). An investment in Notes issued under the Programme involves certain risks. For a discussion of these risks see “Risk Factors”. This Base Prospectus comprises a base prospectus for the purposes of Article 5.4 of Directive 2003/71/EC (the Prospectus Directive) as amended (which includes the amendments made by Directive 2010/73/EU (the 2010 PD Amending Directive) to the extent that such amendments have been implemented in a relevant Member State of the European Economic Area), which is necessary to enable investors to make an informed assessment of the assets and liabilities, financial position, profit and losses of the Issuer. Application has been made to the Luxembourg Stock Exchange for the Notes issued under the Programme (other than VPS Notes) during the period of 12 months from the date of this Base Prospectus to be admitted to trading on the Luxembourg Stock Exchange’s regulated market and to be listed on the Official List of the Luxembourg Stock Exchange. -

The Annual Report 2002 Documents Telenor's Strong Position in the Norwegian Market, an Enhanced Capacity to Deliver in The

The Annual Report 2002 documents Telenor’s strong position in the Norwegian market, an enhanced capacity to deliver in the Nordic market and a developed position as an international mobile communications company. With its modern communications solutions, Telenor simplifies daily life for more than 15 million customers. TELENOR Telenor – internationalisation and growth 2 Positioned for growth – Interview with CEO Jon Fredrik Baksaas 6 Telenor in 2002 8 FINANCIAL REVIEW THE ANNUAL REPORT Operating and financial review and prospects 50 Directors’ Report 2002 10 Telenor’s Corporate Governance 18 Financial Statements Telenor’s Board of Directors 20 Statement of profit and loss – Telenor Group 72 Telenor’s Group Management 22 Balance sheet – Telenor Group 73 Cash flow statement – Telenor Group 74 VISION 24 Equity – Telenor Group 75 Accounting principles – Telenor Group 76 OPERATIONS Notes to the financial statements – Telenor Group 80 Activities and value creation 34 Accounts – Telenor ASA 120 Telenor Mobile 38 Auditor’s report 13 1 Telenor Networks 42 Statement from the corporate assembly of Telenor 13 1 Telenor Plus 44 Telenor Business Solutions 46 SHAREHOLDER INFORMATION Other activities 48 Shareholder information 134 MARKET INFORMATION 2002 2001 2000 1999 1998 MOBILE COMMUNICATION Norway Mobile subscriptions (NMT + GSM) (000s) 2,382 2,307 2,199 1,950 1,552 GSM subscriptions (000s) 2,330 2,237 2,056 1,735 1,260 – of which prepaid (000s) 1,115 1,027 911 732 316 Revenue per GSM subscription per month (ARPU)1) 346 340 338 341 366 Traffic minutes -

Telenor Third Quarter: Restructuring and Cost Reductions

Telenor third quarter: Restructuring and cost reductions Telenor's third quarter results for 2002 show a strong profit and revenue growth in international operations, whereas the growth in the Norwegian market is in decline. Domestic operations are characterised by restructuring and a focus on efficiency and cost reductions. This has resulted in improved margins and lower investments in fixed and mobile networks in Norway. Major write-downs, primarily in Telenor Business Solutions, have produced a loss before taxes. Telenor's revenues in the third quarter were NOK 12,210 million, which is an increase of 21 per cent or NOK 2,146 million compared to the same period in 2001. Revenues increased in the first nine months by NOK 5,664 million, or 19 per cent, to NOK 35,784 million compared to the same period last year. Despite the increase in revenues, Telenor reports a loss before taxes and minority interests of NOK 105 million in the third quarter. This figure includes write-downs of NOK 738 million, which are primarily related to the restructuring of managed services in Telenor Business Solutions. For the first nine months the profit before taxes and minority interests was NOK 309 million. Telenor's third quarter results for 2002 are characterised by restructuring and a focus on cost reductions as a result of the decline in the domestic growth. The group programme Delta 4, of which the aim is to reduce the cost base by NOK 4 billion gross by the end of 2004 compared to 2001, is proceeding according to plan. Total savings of approximately NOK 700 million had been achieved by the end of the third quarter and by the end of the year the cost reductions will be around NOK 1 billion. -

Profiles of Candidates Nominated for Election As Directors of the Company

Enclosure 4 Document accompanying Agenda 5 Profiles of candidates nominated for election as directors of the Company Name Mr. Tore Johnsen Nationality Norwegian Age 68 years Education Master of Science, Norwegian Institute of Technology, University of Trondheim, Norway Training Director Certification Program (175/2013), Thai Institute of Directors Association Proposed type of directorship Director, Member of the Remuneration Committee, Member of the Nomination Committee, and Member of the Corporate Governance Committee Years of directorship 2 years 11 months (Appointed since 29 March 2013) Meeting attendance in 2015 Board of Directors’ Meetings: 9 from 9 times Nomination Committee’s Meetings: 3 from 4 times Remuneration Committee’s Meetings: 3 from 3 times Corporate Governance Committee’s Meeting: 1 from 1 time Shareholding interests in the Company Nil Positions in other SET-listed companies None Positions in non SET-listed companies 6 companies Positions in companies having conflict of interest - Director, Telenor Myanmar Ltd, Myanmar (Telecommunication) - Director, DiGi Telecommunications Sdn Bhd, Malaysia (Telecommunication) - Director and Member of the Audit Committee, DiGi.com Berhad, Malaysia (Telecommunication) - Chairman, Telenor Pakistan Ltd, Pakistan (Telecommunication) - Director and Senior Vice President, Telenor Asia (ROH) Co.,Ltd (Telecommunication) - Director and Member of the Audit Committee, Grameenphone Ltd, Bangladesh (Telecommunication) Work experience Year Position Company 2013 - Present Director, Member of Remuneration -

Annual Report 2016 CONTENT

Annual Report 2016 CONTENT Letter from the CEO 4 Group Executive Management 6 Summary of the Year 8 Financial Achievements 10 Our Strategy 12 Our Global Impact 13 Where We Operate 14 Stakeholder Engagement 16 Message from the Chair 18 The Board 20 Board of Directors’ Report 22 Sustainability Report 41 FINANCIAL STATEMENTS TELENOR GROUP Consolidated Income Statement 70 Consolidated Statement of Comprehensive Income 71 Consolidated Statement of Financial Position 72 Consolidated Statement of Cash Flows 73 Consolidated Statement of Changes in Equity 74 Notes to the Financial Statements 75 FINANCIAL STATEMENTS TELENOR ASA Income Statement 140 Statement of Comprehensive Income 141 Statement of Financial Position 142 Statement of Cash Flows 143 Statement of Changes in Equity 144 Notes to the Financial Statements 145 Responsibility Statement 158 Statement from the Corporate Assembly of Telenor ASA 159 Auditor’s Report 160 Definitions 165 ......---, 4 TELENOR ANNUAL REPORT 2016 LETTER FROM THE CEO LETTER FROM THE CEO VALUE CREATION IN Telenor has a proud history and comes from a strong position. We have a CHANGING TIMES diversified portfolio with solid market positions in Europe and Asia and we have strong operations based on quality We have a solid foundation Looking back at 2016, I am pleased to see networks and massmarket distribution with a good mix of assets, what we have accomplished at a time capabilities. In addition, Telenor’s solid market positions and scale we can leverage going when our industry is undergoing a funda majority ownerships enable strong forward, in a globalized and mental shift to adapt to a digital world. -

Liste a – Datterselskaber Under Telenor

Liste A – Datterselskaber under Telenor ASA Business Registration Owner Company name Country Number share Cinclus Technology AS 963 246 862 100,00% Norway Ci ncl us Technology AS 100,00% Sweden (Branch) Telenor Maritime AS (ex Maritime 985 173 710 98,93% Norway Communications Partner AS) Telenor Maritime Inc. (ex Maritime 260122158 100,00% USA Communications Partner Inc.) Telenor Broadcast 983 935 125 100,00% Norway Holding AS Canal Digital AS 977 273 633 100,00% Norway Canal Digital Danmark 13879842 100,00% Denmark A/S Canal Digital Finland OY 0900990-9 100,00% Finland Canal Digital Norge AS 936 653 820 69,70% Norway Canal Digital Sverige AB 556039-8306 100,00% Sweden Zona vi AS 982 739 845 100,00% Norway Canal Digital Norge AS 936 653 820 30,30% Norway Norkring AS 976 548 973 100,00% Norway Norkring België N.V. 0808.922.491 75,00% Belgium Premium Sports AS 989 656 430 100,00% Norway Telenor Satellite AS (ex Telenor Satellite 974 529 068 100,00% Norway Broadcasting AS) Telenor UK Ltd 03188910 100,00% England Telenor Business 984 400 993 100,00% Norway Partner Invest AS Telenor 983 793 754 100,00% Norway Communication II AS 701Search Pte Ltd 200613507R 33,33% Singapore 702 Search (Thailand) 62160303 33,33% Netherlands B.V. 703 Search (Indonesia) 62160400 31,50% Netherlands B.V. 1 Liste A – Datterselskaber under Telenor ASA Argos Takes Care of It 99,94% Marocco SA Doorstep AS 982 265 460 50,00% Norway Leiv Eiriksson 984 829 906 1,50% Norway Nys kapning AS Telenor Maritime AS (ex Maritime 985 173 710 1,07% Norway Communications Partner AS) Norvestor IV L.P 14,70% Guernsey Oter Invest AS 993 377 953 91,40% Norway Otrum AS 837 088 852 100,00% Norway Otrum Content 100,00% Germany Services GmbH Otrum Finland Oy 358201900600 100,00% Finland Otrum Svenska SE5566032127301 100,00% Sweden AB Otrum, filial af 33156804 100,00% Denmark Otrum Svenska AB Simula School of Res earch and 991 435 646 7,14% Norway Innovation AS Telenor Cloud Services AS (ex Telenor Business 998 027 292 100,00% Norway Internet Services AS) Tel enor Common 13-10-041370 100,00% Hungary Operation Zrt. -

Telenor's Global Impact

Telenor’s Global Impact A Quantification of Telenor’s Impact on the Economy and Society Final KPMG Report 7 November 2016 Document Classification - KPMG Confidential Important notice This document has been prepared by KPMG United Kingdom Plc (“KPMG”) solely for Telenor ASA (“Telenor” or “Addressee”) in accordance with terms of engagement agreed between Telenor and KPMG. KPMG’s work for the Addressee was performed to meet specific terms of reference agreed between the Addressee and KPMG and that there were particular features determined for the purposes of the engagement. The document should not be regarded as suitable to be used or relied on by any other person or any other purpose. The document is issued to all parties on the basis that it is for information only. This document is not suitable to be relied on by any party wishing to acquire rights against KPMG (other than Telenor) for any purpose or in any context. Any party other than Telenor that obtains access to this document or a copy and chooses to rely on this document (or any part of it) does so at its own risk. To the fullest extent permitted by law, KPMG does not accept or assume any responsibility to any readers other than Telenor in respect of its work for Telenor, this document, or any judgements, conclusions, opinions, findings or recommendations that KPMG may have formed or made. KPMG does not assume any responsibility and will not accept any liability in respect of this document to any party other than Telenor. KPMG does not provide any assurance on the appropriateness or accuracy of sources of information relied upon and KPMG does not accept any responsibility for the underlying data used in this document. -

Telenor ASA Fourth Quarter 2002 Content

Telenor ASA Fourth quarter 2002 Content FOURTH QUARTER 2002 Key points 1 Key figures 1 Key figures for the business areas 2 Mobile 3 Networks 6 Plus 6 Business Solutions 7 EDB Business Partner 8 Other business units 9 Corporate functions and group activities 9 Other profit and loss items for the group 9 Taxes 11 Balance sheet 11 US GAAP 11 Outlook for 2003 11 TABLES Profit and loss statement 12 Balance sheet 13 Shareholders equity 13 Cash flow statement 13 Analytical information 14 The business areas 16 Special items 17 Revenues; 2000–2002 Telenor group (NOK in millions) Q1 8,691 Q2 9,145 200020012002 Q3 9,463 Q4 10.273 Q1 10,001 Q2 10,055 Q3 10,064 Q4 15,920 Q1 11,563 Q2 12,011 Q3 12,210 Q4 13,042 0 5,000 10,000 15,000 20,000 Telenor ASA fourth quarter 2002 R KEY POINTS OF THE FOURTH QUARTER 2002 COMPARED TO rata share of total subscriptions including Norway was 12.4 million at THE FOURTH QUARTER 2001 the end of 2002. Telenor’s operations in Sweden were reorganised • 20% growth in revenues excluding gains, to NOK 13,002 million. during the quarter with the purchase of 90% of Utfors AB and 37.2% • EBITDA margin excluding gains and losses increased from 21.0% to of Glocalnet AB. For Business Solutions, the weak market for IT- 27.5%. EBITDA excluding gains and losses was NOK 3,571 million in related activities continues. In Plus, Broadcast shows a positive the fourth quarter 2002.