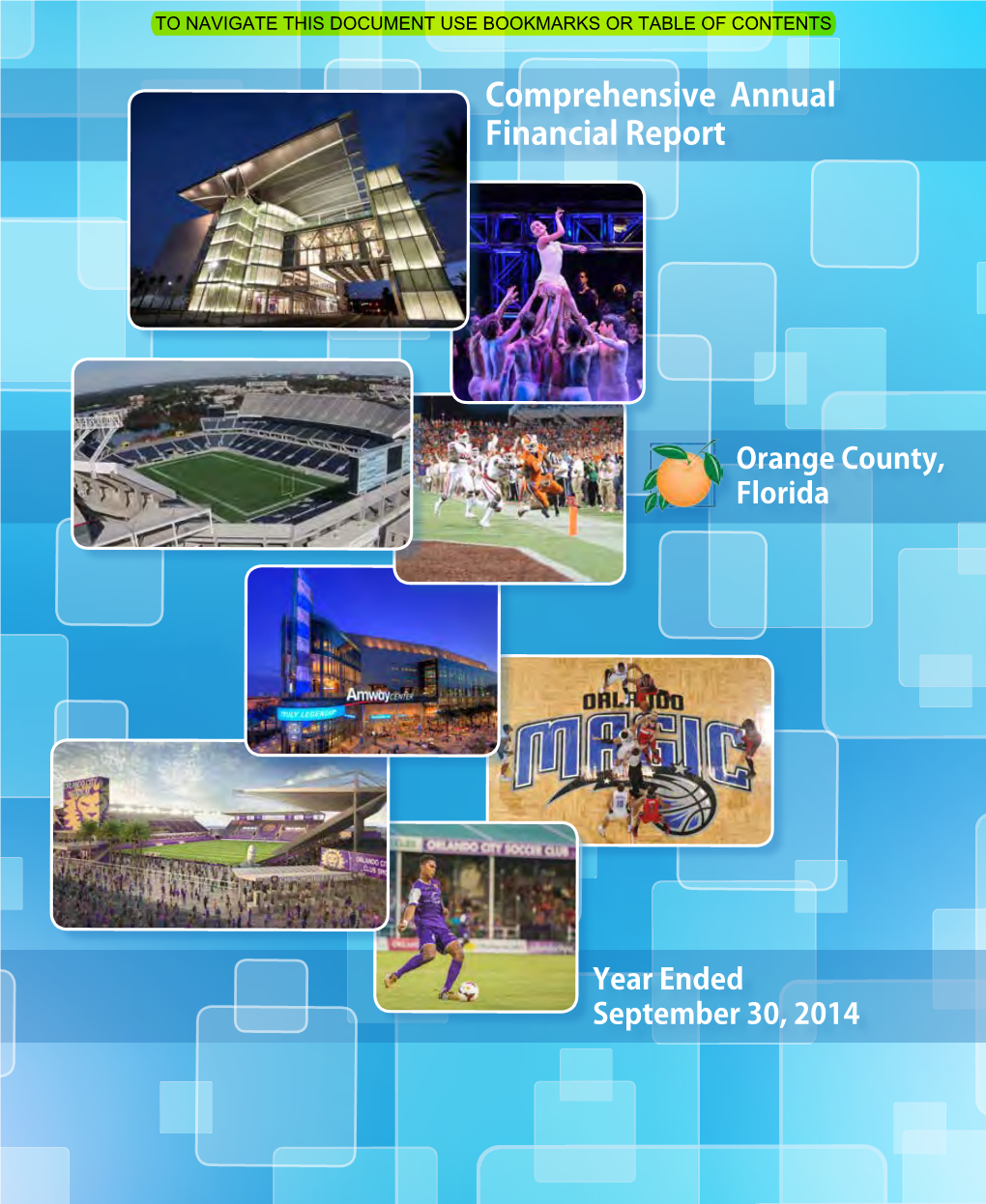

FY 2014 Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stadium Name City Twitter Handle Team Name Alabama Jordan–Hare

Stadium Name City Twitter Handle Team Name Alabama Jordan–Hare Stadium Auburn @FootballAU Auburn Tigers Talladega Superspeedway Talladega @TalladegaSuperS Bryant–Denny Stadium Tuscaloosa @AlabamaFTBL Crimson Tide Arkansas Donald W. Reynolds Razorback Fayetteville @RazorbackFB Arkansas Razorbacks Stadium, Frank Broyles Field Arizona Phoenix International Raceway Avondale @PhoenixRaceway Jobing.com Arena Glendale @GilaRivArena Arizona Coyotes University of Phoenix Stadium Glendale @UOPXStadium Arizona Cardinals Chase Field Phoenix @DBacks Arizona Diamondbacks US Airways Center Phoenix @USAirwaysCenter Phoenix Suns Sun Devil Stadium, Frank Kush Field Tempe @FootballASU Arizona State Sun Devils California Angel Stadium of Anaheim Anaheim @AngelStadium L.A. Angels of Anaheim Honda Center Anaheim @HondaCenter Anaheim Ducks Auto Club Speedway Fontana @ACSUpdates Dodger Stadium Los Angeles @Dodgers Los Angeles Dodgers Los Angeles Memorial Coliseum Los Angeles @USC_Athletics Southern California Los Angeles Clippers Staples Center Los Angeles @StaplesCenter Los Angeles Lakers Los Angeles Kings Mazda Raceway Laguna Seca Monterey @MazdaRaceway Oakland Athletics O.co Coliseum Oakland @OdotcoColiseum Oakland Raiders Oracle Arena Oakland @OracleArena Golden State Warriors Rose Bowl Pasadena @RoseBowlStadium UCLA Bruins Sleep Train Arena Sacramento @SleepTrainArena Sacramento Kings Petco Park San Diego @Padres San Diego Padres Qualcomm Stadium San Diego @Chargers San Diego Chargers AT&T Park San Francisco @ATTParkSF San Francisco Giants Candlestick Park -

Participation List

#WeMakeEvents #RedAlertRESTART #ExtendPUA Participation List Name City State Alabama Theatre Birmingham Alabama South Baldwin Community Theatre Gulf Shores Alabama AC Marriot Huntsville Alabama Embassy Suites Huntsville Alabama Huntsville Art Museum Huntsville Alabama Mark C. Smith Concert Hall Huntsville Alabama Mars Music Hall Huntsville Alabama Propst Arena Huntsville Alabama Gulfquest Maritime Museum Mobile Alabama The Steeple on St. Francis Mobile Alabama Alabama Contempory Art Center Mobile Alabama Alabama Music Box Mobile Alabama The Merry Window Mobile Alabama The Soul Kitchen Music Hall Mobile Alabama Axis Sound and Lights Muscle Shoals Alabama Fame Recording Sudio Muscle Shoals Alabama Jonathan Edwards Home Muscle Shoals Alabama Sweettree Productions Warehouse Muscle Shoals Alabama Shoals Theatre Muscle Shoals Alabama Nick Pratt Boathouse Orange Bach Alabama David &DeAnn Milly Boathouse Orange Beach Alabama The Wharf Mainstreet Orange Beach Alabama Enlighten Entertainment Orange Beach Alabama Orange Beach Preforming Arts Studio Orange Beach Alabama Greg Trenor Boathouse Orange Beach Alabama Russellville Municipal Auditorium Russellville Alabama The Historic Bama Theatre Tuscaloosa Alabama Rawhide Chandler Arizona Rawhide Motorsports Park Chandler Arizona Northern Arizona university Flagstaff Arizona Orpheum Theater - Flagstaff location Flagstaff Arizona Mesa Arts Center Mesa Arizona Clearwing Productions Phoenix Arizona Creative Backstage/Pride Group Phoenix Arizona Crescent Ballroom Phoenix Arizona Herberger Theatre Phoenix -

Amway Center the Orlando Magic Developed the Amway Center, Which Will Compete to Host Major National Events, Concerts and Family Shows

About Amway Center The Orlando Magic developed the Amway Center, which will compete to host major national events, concerts and family shows. The facility opened in the fall of 2010, and is operated by the City of Orlando and owned by the Central Florida community. The Amway Center was designed to reflect the character of the community, meet the goals of the users and build on the legacy of sports and entertainment in Orlando. The building’s exterior features a modern blend of glass and metal materials, along with ever-changing graphics via a monumental wall along one façade. A 180-foot tall tower serves as a beacon amid the downtown skyline. At 875,000 square feet, the new arena is almost triple the size of the old Amway Arena (367,000 square feet). The building features a sustainable, environmentally-friendly design, unmatched technology, featuring 1,100 digital monitors and the tallest, high-definition videoboard in an NBA venue, and multiple premium amenities available to all patrons in the building. Every level of ticket buyer will have access to: the Budweiser Baseline Bar and food court, Club Restaurant, Nutrilite Magic Fan Experience, Orlando Info. Garden, Gentleman Jack Terrace, STUFF’s Magic Castle presented by Club Wyndham and multiple indoor-outdoor spaces which celebrate Florida's climate. Media Kit Table of Contents Enter Legend Public/Private Partnership Fact Sheet By the Numbers Amenities for All Levels Technology LEED: Environmentally-Friendly Corporate Partnerships Jobs in Tough Times Commitment to Parramore Transportation/Parking Concessions Arts and Culture Construction/Design Arena Maps Media Contacts: Joel Glass Heather Allebaugh Tanya Bowley Orlando Magic City of Orlando Amway Center VP/Communications Press Secretary Marketing Manager 407.916-2631 407.246.3423 407.440.7001 [email protected] [email protected] [email protected] AmwayCenter.com **For media information: amwaycenter.com/press-room Amway Center: Enter Legend AmwayCenter.com From a vision to blueprints to reality. -

To See the Full #Wemakeevents Participation List

#WeMakeEvents #RedAlertRESTART #ExtendPUA TOTAL PARTICIPANTS - 1,872 and counting Participation List Name City State jkl; Big Friendly Productions Birmingham Alabama Design Prodcutions Birmingham Alabama Dossman FX Birmingham Alabama JAMM Entertainment Services Birmingham Alabama MoB Productions Birmingham Alabama MV Entertainment Birmingham Alabama IATSE Local78 Birmingham Alabama Alabama Theatre Birmingham Alabama Alys Stephens Performing Arts Center (Alabama Symphony) Birmingham Alabama Avondale Birmingham Alabama Iron City Birmingham Alabama Lyric Theatre - Birmingham Birmingham Alabama Saturn Birmingham Alabama The Nick Birmingham Alabama Work Play Birmingham Alabama American Legion Post 199 Fairhope Alabama South Baldwin Community Theatre Gulf Shores Alabama AC Marriot Huntsville Alabama Embassy Suites Huntsville Alabama Huntsville Art Museum Huntsville Alabama Mark C. Smith Concert Hall Huntsville Alabama Mars Music Hall Huntsville Alabama Propst Arena Huntsville Alabama The Camp Huntsville Alabama Gulfquest Maritime Museum Mobile Alabama The Steeple on St. Francis Mobile Alabama Alabama Contempory Art Center Mobile Alabama Alabama Music Box Mobile Alabama The Merry Window Mobile Alabama The Soul Kitchen Music Hall Mobile Alabama Axis Sound and Lights Muscle Shoals Alabama Fame Recording Studio Muscle Shoals Alabama Sweettree Productions Warehouse Muscle Shoals Alabama Edwards Residence Muscle Shoals Alabama Shoals Theatre Muscle Shoals Alabama Mainstreet at The Wharf Orange Beach Alabama Nick Pratt Boathouse Orange Beach Alabama -

WWE-Case-Study

CASE STUDY WWE, The Famous Group, Quince Imaging and Frozen Mountain deliver an unprecedented virtual-fan event experience www.frozenmountain.com/liveswitch 1-888-379-6686 The Companies WWE World Wrestling Entertainment Inc. (NYSE: WWE) is an integrated media organization and a recognized leader in global entertainment. A company consisting of a portfolio of businesses that create and deliver original content 52 weeks a year to a global audience, WWE’s programming reaches more than 800 million homes worldwide in 28 languages. The Famous Group (TFG) The Famous Group, known for its immersive fan experiences, has activated live audiences for the biggest brands, venues and events in the world for more than twenty years. With The Famous Group, brands, venues and events around the world are able to immersively interact with their audiences and turn captivated participants into fans. Quince Imaging An established leading provider of world-class imaging display and design for over two decades, Quince Imaging is continuously raising the bar for immersive, world-stage experiences. Quince Imaging strives at every given opportunity to ensure their venue and events partners are able to deliver the best experience possible. Frozen Mountain Software Frozen Mountain Software provides flexible live video solutions that connect people everywhere to what matters to them most. Frozen Mountain brings over a decade of professional live video software development and cloud infrastructure operation to countless industry verticals aiming for live video perfection every day. www.frozenmountain.com/liveswitch 1-888-379-6686 The Challenge Creating immersive virtual An Opportunity for Innovation events that connect performers and audiences together WWE identified an opportunity to change the game for both fans and One fact is true in the entertainment owners in the live entertainment industry. -

Amway Center

Mayor’s Citizens Oversight Committee Community Venues Project Overview Dashboard Meeting Date: January 12, 2011 Amway Center—closeout monitoring Project Budget/Expenses—as of 10/31/2010 Budget Expended Expended % of Notes Previous Total Budget Quarter Expended Construction 380,000,000 61,256,202 348,586,282 92% includes design and construction Property 40,000,000 0 41,105,188 103% land acquisition Infrastructure 60,000,000 11,234,750 61,032,538 102% utility, parking, road & site improvements Total $480,000,000 $72,490,952 $450,724,008 94% Schedule Milestones—as of 11/30/2010 Milestone Actual*/ Target Actual Target Start Complete Complete Interior Architectural Finishes 11/2009* 9/2010 9/2010* Hardscape/Landscape (Plaza & Streetscape) 1/2010* 9/2010 9/2010* Substantial Completion—Hunt to ECD to City 9/2010 9/2010* Certificate of Occupancy (CO) 12/2010** Final Completion/Close Out 9/2010* 3/2011 ECD Warranty Period 9/2010* 10/2011 Amway Center West Temp Prkg Lot Constr (South/Div, Hunt) 2/2011** 6/2011** Geico Garage Construction (City) Exterior/Interior Finishes 3/2010* 9/2010 9/2010* Public Art—Exterior 12/2010** Final Completion (CO) 12/2010** South Street Improvements (City) Construction—Phase 1B (medians, intersections) 6/2010* 9/2010 10/2010* Infrastructure (City) Amway Center Streetscape—Construction 1/2010* 12/2010** Church St/I-4 Retaining Wall—Construction 8/2010* 10/2010 11/2010* Terry Av Parking Lot—Construction 2/2011** 6/2011** Chapman Ct Temp Parking Lot—Design 11/2010 1/2011 Church St Parking Garage Improvements (City)—Construction -

Trademark Infringement, Counterfeiting and Dilution Under The

Case 6:17-cv-00504-PGB-GJK Document 21 Filed 04/07/17 Page 1 of 24 PageID 207 IN THE UNITED STATES DISTRICT COURT FOR THE MIDDLE DISTRICT OF FLORIDA ORLANDO DIVISION WORLD WRESTLING ENTERTAINMENT, INC., Case No. 6:17-cv-504-ORL-40-GJK Plaintiff vs. DEGESREE ROOPNARINE GIBBS, MARY NADINE MODARELLI, STEVE EDWARD WRIGHT, DONALD THOMAS SIMON, JOHN AND JANE DOES 1-100, And XYZ CORPORATIONS 1-100, Defendants. AMENDED COMPLAINT FOR INJUNCTIVE RELIEF AND DEMAND FOR JURY TRIAL Plaintiff World Wrestling Entertainment, Inc. (“WWE”), by and through its undersigned attorneys, hereby files this Amended Complaint to provide the identities of those individuals who WWE was able to serve pursuant to the Court’s March 23, 2017 Temporary Restraining Order and Order for Seizure of Counterfeit Marked Goods (the “March 23, 2017 Order”) and from whom counterfeit WWE merchandise was seized during WWE’s WrestleMania® 33 weekend in Orlando, Florida from March 30 through April 4, 2017. In support of this Amended Complaint, WWE alleges as follows: NATURE OF THE CASE 1. This is an action for trademark infringement, counterfeiting and dilution under the Lanham Act, 15 U.S.C. § 1051, et seq., including the Trademark Counterfeiting Act of 1984, 15 U.S.C. § 1116(d), and related state law claims for trademark infringement, dilution and unfair competition occasioned by Defendants’ unlawful manufacture, distribution and/or sale of 1 Case 6:17-cv-00504-PGB-GJK Document 21 Filed 04/07/17 Page 2 of 24 PageID 208 counterfeit merchandise bearing unauthorized copies of WWE’s registered and unregistered trademarks and service marks. -

Bill Analysis and Fiscal Impact Statement

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional Staff of the Appropriations Subcommittee on Transportation, Tourism, and Economic Development BILL: SB 414 INTRODUCER: Senator Lee SUBJECT: Sports Development DATE: February 19, 2019 REVISED: ANALYST STAFF DIRECTOR REFERENCE ACTION 1. Anderson McKay CM Favorable 2. Hrdlicka Hrdlicka ATD Pre-meeting 3. AP I. Summary: SB 414 repeals the Sports Development program in s. 288.11625, F.S. The program provides an avenue for applicants to apply for a distribution from the state to fund the construction or improvements to a professional sports franchise facility. Since the program was enacted in 2014, no application has been approved by the Legislature. The bill also makes conforming changes to other statutes, related to Sports Development program distributions and reporting requirements. This bill has no fiscal impact. The bill takes effect July 1, 2019. II. Present Situation: Professional Sports in Florida Florida is home to 10 teams1 currently competing in five major professional sports leagues, which include:2 Year Facility Franchise Sport League Facility County Founded Opened Hard Rock Stadium Miami Football NFL 1966 (previously Sun 1987 Miami-Dade Dolphins Life Stadium) 1 Inter Miami CF is an expansion team in Major League Soccer (MLS) due to begin play in 2020. Major League Soccer, It’s official: Major League Soccer awards expansion team to Miami, January 29, 2018, available at https://www.mlssoccer.com/post/2018/01/29/its-official-major-league-soccer-awards-expansion-team-miami (last visited February 13, 2019). -

Taking the Field: Advancing Energy and Water Efficiency in Sports Venues

National Institute of BUILDING SCIENCES Taking the Field: Advancing Energy and Water Efficiency in Sports Venues A Report to U.S. Department of Energy An Authoritative Source of Innovative Solutions for the Built Environment Taking the Field: Advancing Energy and Water Efficiency in Sports Venues Prepared for the U.S. Department of Energy Under Contract DE-EE0007516 February 2017 Taking the Field: Advancing Energy and Water Efficiency in Sports Venues Table of Contents Executive Summary ........................................................................................................................ 1 Introduction to Stadiums and Arenas .............................................................................................. 5 The Power of Sports .................................................................................................................... 6 Venues and the Community .................................................................................................... 7 Number and Size of Venues .................................................................................................... 7 Economic Impact of Sports ..................................................................................................... 9 Activities to Date .......................................................................................................................... 10 Monitoring Progress, Setting Goals .......................................................................................... 12 Green Building -

City of Orlando, Florida Comprehensive Annual Financial Report

CITY OF ORLANDO, FLORIDA COMPREHENSIVE ANNUAL FINANCIAL REPORT Ivey Lane park FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2018 COMPREHENSIVE ANNUAL FINANCIAL REPORT City of Orlando, Florida For the Fiscal Year Ended September 30, 2018 Prepared by: Office of Business and Financial Services This page intentionally blank. This page intentionally blank. CITY OF ORLANDO, FLORIDA COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2018 TABLE OF CONTENTS Page I. INTRODUCTORY SECTION Letter of Transmittal 1 Certificate of Achievement for Excellence in Financial Reporting 7 Organization Chart 9 List of Officials 11 II. FINANCIAL SECTION Independent Auditor’s Report 13 A. MANAGEMENT’S DISCUSSION AND ANALYSIS (required supplementary information) 15 B. BASIC FINANCIAL STATEMENTS Government-Wide Financial Statements Statement of Net Position 33 Statement of Activities 34 Fund Financial Statements Governmental Fund Financial Statements Balance Sheet 36 Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position 37 Statement of Revenues, Expenditures, and Changes in Fund Balances 38 Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 39 Proprietary Fund Financial Statements Statement of Net Position – Business-type Activities – Enterprise Funds – Governmental Activities – Internal Service Funds 42 Statement of Revenues, Expenses, and Changes in Net Position – Business-type Activities – Enterprise Funds – Governmental -

The Ballpark of the Palm Beaches MARCH 19, 2015 // RESPONSE to REQUEST for QUALIFICATIONS for CONSTRUCTION MANAGEMENT SERVICES March 19, 2015

The Ballpark of The Palm Beaches MARCH 19, 2015 // RESPONSE TO REQUEST FOR QUALIFICATIONS FOR CONSTRUCTION MANAGEMENT SERVICES March 19, 2015 Palm Beach County Facilities Development & Operations 2633 Vista Parkway 2 Oakwood Boulevard, Suite 125 West Palm Beach, FL 33411-5604 Hollywood, Florida 33020 RE: Request for Qualifications for The Ballpark of The Palm Beaches - Construction Management Services Thank you for the opportunity for Hunt Construction Group, in association with Straticon Construction Services, Messam Construction and Cooper Construction Management & Consulting (HSMC) to present our qualifications to perform Construction Management Services for the Houston Astros and Washington Nationals for their new, joint spring training facility, The Ballpark of The Palm Beaches. Hunt Construction Group, Inc., will be the sole contracting entity for these services. (FL GC license CGC1510528 Palm Beach County Business HSMCLicense IS LBTR#201249825). FULLY COMMITTED TO COMPLETING THE PROJECT TO FACILITATE THE HOUSTON ASTROS AND WASHINGTON NATIONALS SPRING TRAINING IN 2017 AND PROVIDING THE INTENDED PROGRAM WITHIN THE PROPOSED BUDGET. We have assembled an exceptional project team capable of meeting all of the many challenges that this project will face. Hunt, a nationally recognized leader in sports facility construction, with an extensive South Florida project resume combined with Straticon’s , Messam’s and Cooper’s wealth of local West Palm Beach and South Florida construction experience and relationships, provides us with a distinct competitive advantage. Our team of exceptional builders and management expertise will provide all stakeholders with the absolute best choice for a project partner, as Constructionover 155 Manager, organizations to meet and exceed the expectations for the successful completion of22 this Major project. -

PATHWAYS for PARRAMORE Building a Community on Heritage

Spring Edition 2017 BUSINESS DEVELOPMENT CHILDREN & EDUCATION HOUSING PUBLIC SAFETY QUALITY OF LIFE PATHWAYS FOR PARRAMORE Building a Community on Heritage Orlando Mayor Orlando City Soccer Club Opens Buddy Dyer and New Stadium in Parramore District 5 City Commissioner Regina Hill Help Deliver Books to City of Orlando Youth 1,000,000 sq. ft. of office/creative space • 500,000+ sq. ft. of higher education space 1,500 residential units • 150,000 sq. ft. of retail/commercial space • 225 hotel rooms There is no doubt that Orlando has become the region, guests to our hotels, and customers to nation’s premier sports destination, and the our restaurants. But venues like this stadium are addition of the new Orlando City Soccer Club permanent economic drivers. stadium only adds to our offerings. In February, Mayor Dyer, District 5 City In the last year, our region has hosted Copa Commissioner Regina I. Hill, and others cut the In early February, Orlando Mayor Buddy America, Florida State-Ole Miss in the Camping ribbon for the newest MLS stadium in the nation. Dyer and District 5 City Commissioner World Kickoff, the Florida Classic, the ACC Football This stadium will provide an intimate atmosphere Regina I. Hill delivered more than 100 free Championship, three bowl games, the NFL Pro for our community to come together as one, for books to Page 15, an after-school program Bowl, and more. Parramore businesses to be represented during Next month, NCAA March Madness returns to future farmers markets planned at the stadium, at the City of Orlando’s Downtown the Amway Center and in April, we’ll host WWE and the exposure businesses will receive as Recreation Center.