Greater Toronto Area

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Peel Geographies

Peel Geographies Census Metropolitan Area (CMA) Census Division (CD) Census Subdivision (CSD) Census Metroplitan Areas consist of large Census divisions are the general term for provin- Census Subdivision is the general term for urbanized areas that surround an urban core. cially legislated areas (such as county and regional municipalities or their equivalents (such as Indian The urban core must have a population greater district) or their equivalents. Census divisions are Reserves). than 100,000. Peel is a part of the intermediate geographic areas between the Toronto Metropolitan Area. province/territory level and BROCK the municipality Count in Peel: Count: GGEORGINAEORGINA (census subdivision). 3 EEASTAST Bradford SCUGOG 1 GGWILLIMBURYWILLIMBURY UUXBRIDGEXBRIDGE Count in Peel: New Example: West NEWMARKET DURHAM Example: Mono WWHITCHURCHHITCHURCH - SSTOUFFVILLETOUFFVILLE 1 Tecumseth AURORA CCLARINGTONLARINGTON Caledon, Brampton KING Gwillimbury YORK PPICKERINGICKERING OOSHAWASHAWA Toronto RRICHMONDICHMOND HHILLILL Example: or Caledon MARKHAM WHITBY CALEDON AJAX Last Update: VVAUGHANAUGHAN Peel Region PEEL Last Update: TTORONTOORONTO 2016 BBRAMPTONRAMPTON Last Update: 2016 HHALTONALTON HHILLSILLS MMISSISSAUGAISSISSAUGA 2016 HALTONHALTON MMILTONILTON OAKVILLE BBURLINGTONURLINGTON Census Tracts (CT) Dissemination Areas (DA) Dissemination Blocks Census Tracts are small, relatively stable Dissemination areas are small, relatively stable Dissemination blocks are areas bounded on all geographic areas in census metropolitan areas geographic -

Clarington Boundary Road Agreement

Attachment 1 to Report EGD-012-20 Item: DS-20-XX BOUNDARY ROAD AGREEMENT Attachment 6 THIS AGREEMENT made in triplicate as of the day of , 2020 BETWEEN: THE CORPORATION OF THE CITY OF OSHAWA (herein referred to as "Oshawa") ~ and ~ THE CORPORATION OF THE MUNICIPALITY OF CLARINGTON (herein referred to as "Clarington") RECITALS (a) WHEREAS The Corporation of the Municipality of Clarington (herein referred to as “Clarington”) and The Corporation of the City of Oshawa (herein referred to as “Oshawa”) are municipalities as defined by the Municipal Act, 2001. (b) WHEREAS Clarington and Oshawa have joint jurisdiction over certain parts of Townline Road, a boundary line highway situated between Clarington and Oshawa. (c) WHEREAS pursuant to section 11 of the Municipal Act, 2001, Clarington and Oshawa may pass by-laws respecting matters within the "highways" sphere of jurisdiction. (d) WHEREAS pursuant to sections 29 and 29.1 of the Municipal Act, 2001, if municipalities having joint jurisdiction over a boundary line highway enter into an agreement under which each municipality agrees to keep any part of the highway in repair for its whole width and to indemnify the other municipality from any loss or damage arising from the lack of repair for that party, the agreement and a copy of the by-law authorizing the agreement may be registered in the land registry office for the area in which the highway is located. (e) WHEREAS by agreement dated January 24, 1979 between Oshawa and The Corporation of the Town of Newcastle, provision was made for the reconstruction and sharing of costs relating to such reconstruction of that part of Townline Road between the Canadian Pacific Railway line and Farewell Creek. -

Lakeshore East GO Rail Extension to Bowmanville

Lakeshore East GO Rail Extension to Bowmanville For discussion with Metrolinx Chair D. Wright and President and CEO P. Verster April 8, 2019 Confirm Lakeshore East GO Rail Extension The Province’s commitment to delivering the Lakeshore East (LSE) GO rail extension to Bowmanville by 2024 is critical because: • Durham Region is poised for significant growth – almost double by 2041 • Durham is committed to developing transit to • Improve connections • Shape growth • Unlock development potential at new station areas • Is a catalyst to job creation and city building • LSE GO Rail extension is a pillar of our rapid transit network 2 Lakeshore East GO Rail Extension 20 km and 4 new stations by 2024 $550 million investment 3 It’s Durham’s Time • Majority of GO investment in new rail service has been west of Durham • Current ridership on Lakeshore East is roughly double that on Milton and Kitchener lines. • Forecast ridership for LSE stations exceeds stations in Kitchener, Niagara, Gormley 4 Extension Addresses Regional Transportation Challenges • Population growth • Disconnected transit • Congestion • Competitiveness • Demographic change • Urbanization • Clean environment 5 Population Growth Will Create Demand The population east of 2031: 2041: Durham Region 960,000 residents/ 1.2 million residents/ (Northumberland 350,000 jobs 430,000 jobs County, City of Kawartha Lakes, City of Peterborough and County of Peterborough) will account for another 408,000 by 2041. LSE GO Rail Extension – Ridership • Forecasts: • 10,700 daily customers • Growth – -

Cultural Heritage Screen Report

Lincolnville Go Station Improvements: Cultural Heritage Screening Report Prepared for: Metrolinx 20 Bay Street, Suite 1800 Toronto ON M5J 2W3 ~ METROLINX Prepared by: Stantec Consulting Ltd. 300W-675 Cochrane Drive Markham ON L3R 0B8 () Stantec File No. 1135200010 October 12, 2017 LINCOLNVILLE GO STATION IMPROVEMENTS: CULTURAL HERITAGE SCREENING REPORT Project Personnel EA Project Manager: Alex Blasko, B.Sc. (Hon.) Heritage Consultant: Heidy Schopf, MES, CAHP Task Manager: Meaghan Rivard, MA, CAHP Report Writer: Heidy Schopf, MES, CAHP Laura Walter, MA GIS Specialist: Sean Earles Office Assistants: Carol Naylor Quality Review: Meaghan Rivard, MA, CAHP Independent Review: Tracie Carmichael, BA, B. Ed. () Stantec Sign-off Sheet This document was prepared by Stantec Consulting Ltd. (“Stantec”) for the account of Metrolinx (the “Client”). The material in it reflects Stantec’s professional judgment in light of the scope, schedule and other limitations stated in the document and in the contract between Stantec and the Client. The opinions in the document are based on conditions and information existing at the time the document was published and do not take into account any subsequent changes. The report has been prepared based, in part, on information provided by others as cited in the Reference section. Stantec has not verified the accuracy and / or completeness of third party information. Prepared by (signature) Heidy Schopf, MES, CAHP Cultural Heritage Specialist Reviewed by (signature) Signed by Tracie Carmichael on behalf of: Meaghan Rivard, -

Clarington, ON, Canada Demographic Information 2018

Clarington, ON, Canada Demographic Information 2018 54 King St. E., Unit 102 Bowmanville, ON L1C 1N3 (905) 623-3106 [email protected] • www.cbot.ca 1.0 Population Size and Growth Table 1: Population Change 2001 2006 2011 2016 2021 Clarington Population 69,834 77,820 84,548 92,013 108,100* % Change from Previous Census 11.4% 8.6% 8.8% 17.5%* Durham Region Population 506,901 561,258 608,124 645,862 809,990** % Change from Previous Census 10.7% 8.4% 6.2% 25.4% Ontario Population 11,410,045 12,160,282 12,851,821 13,448,494 14,980,422*** % Change from Previous Census 6.6% 5.7% 4.6% 11.4%** Source: Statistics Canada 2001, 2006, 2011, 2016 *Estimated Hemson **Source: Durham Regional Official Plan Amendment No. 128 ***Statistics Canada Estimates and Ontario Ministry of Finance projections 2.0 Age Profile Table 2: Age Distribution, 2016 Clarington Durham Durham Clarington Ontario % Region Region % Total Population 92,013 100% 645,862 100.0% 13,448,494 0 to 14 years 17,155 18.6% 116,185 18.0% 2,207,970 0 to 4 years 5,590 6.1% 35,695 5.5% 697,360 5 to 9 years 5,790 6.3% 39,930 6.2% 756,085 10 to 14 years 5,770 6.3% 40,560 6.3% 754,530 15 to 19 years 6,210 6.7% 42,970 6.7% 811,670 20 to 24 years 5,880 6.4% 43,235 6.7% 894,390 25 to 29 years 5,410 5.9% 37,590 5.8% 874,350 30 to 34 years 6,240 6.8% 39,640 6.1% 864,765 35 to 39 years 6,260 6.8% 41,400 6.4% 842,485 40 to 44 years 6,235 6.8% 43,545 6.7% 871,875 45 to 49 years 6,515 7.1% 46,935 7.3% 937,385 50 to 54 years 7,900 8.6% 55,045 8.5% 1,056,345 55 to 59 years 6,545 7.1% 48,595 7.5% 989,460 60 to 64 -

BOWMANVILLE Municipality of Clarington TWO COMMERCIAL LOTS on 401 EAST for SALE

BOWMANVILLE Municipality of Clarington TWO COMMERCIAL LOTS ON 401 EAST FOR SALE OFFICE BUILDING-1 ( proposed) 45 Spicer Sq., Bowmanville Municipality of Clarington, Regional Municipality of Durham., Ontario. FOR SALE TWO COMMERCIAL LOTS ON 401 BOWMANVILLE. Municipality of Clarington. LOCATION: 45 Spicer Square & 5 Spicer Square - South of Baseline Road and West of Waverly Road / HWY 401 Interchange LEGAL Block 2 & Block 9 - Plan 40M2171 Town of Clarington, Region of DESCRIPTION: Durham. LOT SIZE & Block 2 - 0.95 Acres ; ( West Lot) OFFER PRICE: OFFER PRICE: $ 700.000 Block 9 - 1.139Acres. ( East Lot) - OFFER PRICE: $ 750.000 DIMENTIONS: Block 2 - 182 .61 Ft. x 229.29 Ft. Block 9 - 166.20 Ft x 270.30 Ft. ZONING: C 5-16 Clarington By-Law 2009-19. Permitting wide range of commercial uses, including office building, retail sales& service, motor vehicle sales, restaurants, building supply outlet. SERVICES: Full Municipal services available. COMMENTS: Full set of Architectural drawings (preliminary) for 2 storey* office building of 20,000 Sq. Ft, (with U/G parking) available to Purchaser. * City has agreed, in principle, for a 3 storey office Building and a Restaurant, with surface Parking. Direct access to Highway 401, Great office building or retail site. Just 50 Min. drive, from GTA - 401 East. SITE FEATURES & Proximity to Ontario Power Generation (OPG) / Darlington OPPORTUNITIES Nuclear Plant ( 2500 + Employees) in Clarington**: Nuclear Plant Refurbishment: 4 year project, in progress. (2013- 2017) OPG Darlington- B Nuclear New Build (2013-2020) OPG Darlington- A Refurbishment Nuclear Reactors -(2015-2022) Nuclear Supply Chain - over 10 Companies expressed interest in establishing operations in Bowmansville (2013-2020) 67% - Interested in Commercial / Office space. -

September 5, 2019 Overview of Public Meeting #1

Welcome to Public Meeting #1 Alternative Low Carbon Fuel Use at St Marys Cement Bowmanville Plant September 5, 2019 Overview of Public Meeting #1 . St Marys Cement (SMC) a company of Votorantim Cimentos North America (VCNA) is undertaking efforts to use Alternative Low Carbon Fuels (ALCFs) as an energy source for their Bowmanville Cement Plant . Today our Project Team is here to answer the following questions and hear your feedback: . Overview of the St Marys Cement Bowmanville Plant (SMCB) . What are the important characteristics / facts of SMCB operation? . How is cement made? . What are Alternative Low Carbon Fuels (ALCF)? . Overview of the Demonstration Project and results . What is the Demonstration Project and why was it conducted? . What are the results of the Demonstration Project? . Overview of the current project and proposed application under Ontario Regulation (O. Reg) 79/15 . What SMCB is proposing and why? . How is SMCB considering the environment in this project? . How is this study being conducted? . What is the timeline for this project? . How can you participate in this project? St Marys Cement Bowmanville Plant Site Overview . St Marys Cement Bowmanville Plant (SMCB) is located at 410 Bowmanville Avenue, in Bowmanville, Ontario, within the Municipality of Clarington . SMCB extracts limestone at the site, produces clinker and cement for the Ontario market and also exports to the US . The cement produced at the plant contributes to building infrastructure (e.g. roads, bridges, buildings) across Ontario and North America: . Examples of projects include the CN Tower, Darlington Nuclear Station and Toronto-York Spadina Subway Extension Site Facts . Started operations over 50 years ago in 1968 . -

Structural Engineering Services by Licensed Professional Structural Engineers in Clarington, Ontario

Structural Engineering Services by Licensed Professional Structural Engineers in Clarington, Ontario Providing structural engineering designs of structural steel framings, reinforced concrete floors and walls, masonry and wood framed structures, footings, and foundations in the Municipality of Clarington which includes Bowmanville, Courtice and Newcastle, is a core component of our practice. Our licensed Professional Structural Engineers have continued to pioneer in structural engineering analysis and structural engineering design services including seismic design for new construction projects including structural steel framings, reinforced concrete floors and walls, masonry and wood framed structure, foundation and footings including pre-engineered building foundation design and rehabilitation of existing buildings including balcony & parking garage repairs (ledger beams, deck re- design, bearing pads, drainage remediation, slabs and columns). Our licensed professional structural engineers and support staff are committed to services of the highest quality and respond inventively, regardless of whether the project is a small or a huge complex long-span structural engineering project. Regardless of the nature of the project whether the project is rehabilitation of structures, replacement of structures, or new structures, our licensed professional structural engineers are well experienced in distinctive creative designing with a variety of building materials for structures, including steel, concrete, masonry and wood. Our licensed professional structural engineers combine structural engineering analysis with experience and knowledge to create strong, durable, elegant and economical structural engineering designs that integrate the demands of building materials, building geometry, and gravity, wind, & seismic loads. Our licensed professional structural engineers also prepare structural engineering drawings indicating the location, sizes and quantities of materials, and specifications indicating the quality of materials and required performance of structural systems. -

Adrian R. Litavski, Mcip, Rpp

ADRIAN R. LITAVSKI, MCIP, RPP EDUCATION 1995 Honours Bachelor of Environmental Studies, Co‐op (Urban & Regional Planning), University of Waterloo ‐ Waterloo, Ontario 1991 International Exchange, Faculty of Environmental Design & Construction (Planning) Royal Melbourne Institute of Technology ‐ Melbourne, Australia PROFESSIONAL MEMBERSHIPS / ASSOCIATIONS Registered Professional Planner (Province of Ontario) Full Member – Ontario Professional Planning Institute (www.ontarioplanners.ca) Full Member – Canadian Institute of Planners (www.cip‐icu.ca) Member of Lambda Alpha International (Simcoe Chapter) – An honourary land economics society (www.lai.org) SELECTED PROJECT EXPERIENCE Development Planning / Project Management Have acted as consulting planner and project manager for various development projects requiring all forms of development approval including Official Plan and Zoning By‐law Amendments, Development Area Plans (Tertiary Plans), Plans of Subdivision, Consents and Minor Variances, and Site Plan Approvals. Have also been responsible for the assembly and management of required consulting teams including civil engineers, traffic engineers, environmental consultants, architects, landscape architects, etc. Projects include: Giles Chevrolet, Town of Whitchurch‐Stouffville – Responsible for securing site plan approval for the re‐configured dealership lands on behalf of the Region of York. Retained to facilitate the Region’s efforts to eliminate the Ninth Line “jog” at Main Street in Stouffville wherein the Region negotiated a land -

List of GLA:D™ Canada Clinics - Ontario

List of GLA:D™ Canada Clinics - Ontario City/Town Site Address Ajax Durham Orthopaedic Clinic 60 Randall Drive, Units 7 & 8 Ajax, ON L1S 6L3 905-428-7800 Alliston Alliston Physiotherapy & Sports Rehabilitation 27 Victoria St. E Alliston, ON L9R 1T9 705-434-0645 www.allistonphysiotherapy.com Atikokan Atikokan General Hospital Rehabilitation Department 120 Dorothy Street Atikokan, ON P0T 1C0 807-597-4215 ext. 355 www.aghospital.on.ca Aurora Aurora Sport Medicine Professionals 248 Earl Stewart Drive, Suite 200 Aurora, ON L4G 6V8 905-503-2767 www.aurorasportsmed.ca Aurora Bayview Physiotherapy & Sports Medicine Wellington Business Centre Clinic 244 Wellington Street East Suite 200 Aurora, ON L4G 1J5 905-713-1209 Barrie Barrie Community Health Centre 490 Huronia Road Barrie, ON L4N 6M2 705-734-9690 ext. 291 Barrie Sports Medicine - Huronia Road, Barrie 480 Huronia Road Suite 104 Barrie, ON L4N 6M2 705-734-3340 Bolton: Bolton Physiotherapy Clinic 12295 Highway 50, Unit #10 Bolton, ON L7E 1M2 905-857-3927 Bowmanville We-Fix-U 196 King St. East Bowmanville, ON L1C 1P1 905-233-4374 Bracebridge Bracebridge Chiropractic and Wellness Centre 132 Wellington Street Bracebridge, ON P1L 1C4 705-645-9544 GLA:D™ Canada by Bone and Joint Canada a division of The Canadian Orthopaedic Foundation List of GLA:D™ Canada Clinics - Ontario City/Town Site Address Brampton Insync Wellness 20 Rivermont Rd, Unit 3B Brampton, ON L6Y 6G7 905-455-2222 www.insyncwellness.com Brampton Natural Touch Rehabilitation Centre 312 Queen St. E Brampton, ON L6V 1C2 905-281-8247 www.naturaltouchrehabilitation.com Brampton Ortho Rehab Group Inc. -

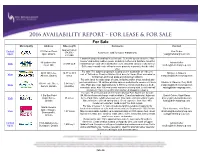

2016 Availability Report - for Lease & for Sale

2016 AVAILABILITY REPORT - FOR LEASE & FOR SALE For Sale Municipality Address Sizes (sq ft) Comments Contact Approximately Contact 225 Salem Road, Yosi Behar 174,000 - Automotive land for luxury brands only. Agent Ajax, Ontario [email protected] 217,000 Landmark property and business for sale. Currently operated as the “Hide House” and selling leather goods, including clothes and furniture. Ideal for 49 Eastern Ave, Adrian Kofler View 41,000 sq ft retail/wholesale and office destination uses. Beautiful custom rustic interior. Acton ON. [email protected] Seller may consider sale of business or property separately for the right offer. For sale: The subject property is located on the south side of 14th Line, 6485 14th Line, 12.37 to 98.5 Michael J. Saperia View east of Tottenham Road, in Alliston. Next door to Honda Plant and minutes Alliston, Ontario acres [email protected] to Walmart-anchored plaza and downtown Alliston. For sale: Ideal for wide range of uses, including coffee shop, medical and professional uses. 20 surface parking spaces dedicated to commercial area Michael J. Saperia, Cory Quitt 15624 Leslie Street, 5,642 sq ft View only. Patio potential. Approximately 2,900 new construction houses in the [email protected] Aurora, Ontario (divisible) immediate area. Also 400 new senior residences being built. Less than half [email protected] a kilometre from a new Walmart-anchored shopping complex. For sale: 36 acres of land on the former Molson Park Barrie site for sale. 1 Big Bay Point $4.5M development charge credit available. Zoned as industrial. Adjacent Daniel Cohen, Kapil Rana View Road, Barrie, 36 acres to the Park Place retail redevelopment. -

Clarington / Oshawa Boundary Road Agreement Recommendations

Staff Report If this information is required in an alternate accessible format, please contact the Accessibility Coordinator at 905-623-3379 ext. 2131. Report To: General Government Committee Date of Meeting: June 22, 2020 Report Number: EGD-012-20 Submitted By: Ron Albright, Acting Director of Engineering Services Reviewed By: Andrew C. Allison, CAO Resolution#: File Number: G.55.01 By-law Number: Report Subject: Clarington / Oshawa Boundary Road Agreement Recommendations: 1. That Report EGD-012-20 be received; 2. That the Mayor and Clerk be authorized to execute the Boundary Road Agreement attached to Report EGD-012-20, as Attachment 1; and 3. That all interested parties listed in Report EGD-012-20 and any delegations be advised of Council’s decision. Municipality of Clarington Page 2 Report EGD-012-20 Report Overview The purpose of this report is to seek Council approval to renew the Boundary Road Agreement with the City of Oshawa. The Boundary Road Agreement identifies shared boundary roads and assigns responsibility to the appropriate municipality. 1. Background 1.1 The Municipality of Clarington and the City of Oshawa abut one another along Townline Road. The Boundary Road Agreement applies to opened year-round maintained right of ways. Some sections of Townline Road are unopened. The Boundary Road Agreement assigns responsibilities to the City of Oshawa and the Municipality of Clarington for the opened sections, including sections that are under the jurisdiction of the Region of Durham. 1.2 The section of Townline Road north of Winchester Road is unopened and has been leased to Hydro One Networks Inc.