Philippines at a Glance: 2001-02

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MIAMI UNIVERSITY the Graduate School Certification for Approving

MIAMI UNIVERSITY The Graduate School Certification for Approving the Dissertation We hereby approve the Dissertation of Stephen Hess Candidate for the Degree: Doctor of Philosophy ____________________________________ Director (Dr. Venelin Ganev) ____________________________________ Reader (Dr. Gulnaz Sharafutdinova) ____________________________________ Reader (Dr. Adeed Dawisha) ____________________________________ Graduate School Representative (Dr. Stanley Toops) ABSTRACT AUTHORITARIAN LANDSCAPES: STATE DECENTRALIZATION, POPULAR MOBILIZATION, AND THE INSTITUTIONAL SOURCES OF RESILIENCE IN NONDEMOCRACIES by Stephen Hess Beginning with the insight that highly-centralized state structures have historically provided a unifying target and fulcrum for the mobilization of contentious nationwide social movements, this dissertation investigates the hypothesis that decentralized state structures in authoritarian regimes impede the development of forms of popular contention sustained and coordinated on a national scale. As defined in this work, in a decentralized state, local officials assume greater discretionary control over public expenditures, authority over the implementation of government policies, and latitude in managing outbreaks of social unrest within their jurisdictions. As a result, they become the direct targets of most protests aimed at the state and the primary mediators of actions directed at third-party, non-state actors. A decentralized state therefore presents not one but a multitude of loci for protests, diminishing claimants‘ ability to use the central state as a unifying target and fulcrum for organizing national contentious movements. For this reason, decentralized autocracies are expected to face more fragmented popular oppositions and exhibit higher levels of durability than their more centralized counterparts. To examine this claim, I conduct four comparative case studies, organized into pairs of autocracies that share a common regime type but vary in terms of state decentralization. -

Republic of the Philippines 10.625% Global Bonds Due 2025

PROSPECTUS SUPPLEMENT TO PROSPECTUS DATED SEPTEMBER 24, 2003 R E S PU NE BLIC IPPI OF THE PHIL US$300,000,000 Republic of the Philippines 10.625% Global Bonds due 2025 Luxembourg Stock Exchange Listing Particulars The Republic will pay interest on the global bonds each March 16 and September 16. The Ñrst interest payment on the global bonds will be made on March 16, 2004. The global bonds will constitute a further issuance of, are fungible with and are consolidated and form a single series with, the 10.625% Global Bonds due 2025 issued by the Republic on March 16, 2000. The total principal amount of the previously issued global bonds and the global bonds now being issued is $1,300,000,000. The Republic may not redeem the global bonds prior to their maturity. The oÅering of the global bonds is conditional on the receipt of certain approvals of the Monetary Board of the Bangko Sentral ng Pilipinas, the central bank of the Republic. The global bonds are being oÅered globally for sale in the jurisdictions where it is lawful to make such oÅers and sales. We have applied to list the global bonds on the Luxembourg Stock Exchange. We cannot guarantee that the application to the Luxembourg Stock Exchange will be approved, and settlement of the global bonds is not conditioned on obtaining the listing. Per Bond Total Price to investors(1) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 112.25% $336,750,000 Underwriting discounts and commissions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 0.10% $ 300,000 Proceeds, before expenses, to the Republic ÏÏÏÏÏÏÏÏÏÏÏÏÏ 112.15% $336,450,000 (1) Plus accrued interest from and including September 16, 2003. -

Eduardo K"R*R, Insurance F, Commissioner 1U It T, ;L

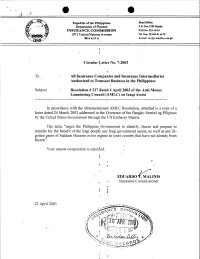

o o Republic of the Philippines Head OIEcc: Department of Finance P. O. Box 3589 Manila INSURANCE COMMISSION FAXNo.522.l+31 1071 United Nations Avenue Tel. Nos. 523-84-61 to 70 Manila. E-mail: [email protected] t t Circular l-etter No. 7-2003 il To" All Insurance Companies and Insurance Intermediaries Authorized to Transact Business in the Philippines i Subject Resolution # 227 dated 4 April 2003 of the Anti-Money Laundering Council (AMLC) on Iraqi Assets In accordance with the aforementioned AMLC Resolution, attached is a copy of a letter dated 24March 2003 addressed torthe Governor of the Bangko Sentral ng Pilipinas by the United States Government through the US Embassy Manila. { The letter "urges the Philippine. Government to identifu,, freeze and prepare to transfer for the benefJ of the Iraqi people any Iraqi government assets, as well as any ill- gotten gains of Saddam Hussein or his regime in (our) country that have not already been frozeft". Your utmost cooperation is enjoified. t t, it EDUARDo K"r*r, Insurance f, Commissioner 1u it t, ;l 22 Aprll2003 t' l' o 'mbassy ' r:t::i i;;.:i{FI 'r:. i\li^ '', 'i " , M_a,ilu, pltilippiftEggili1r':ll,r:,]. Bdrror:o serrrnal ti* ert.rFtllirs-----.,.--. ) OTFICE OFltrg (i$+rl,ritl(f,rM qtph,24, Z0O3 '03 /f* rry 3 -;; '03 ,f,r$:26 f')'r [1,1i1 25 Mr. Rafael Buenaventura Governor Banko Sentral ng pilipinas Dear Governor Buenaventura: iif, I 31:L,I*:!:gilSins of -hosririries in rraq, ir," unit.ar i i3" 1 linni : ;funds;i,inl,:a. -

CNMI Are Being Investigated by Government Operatives for Allegedly Selling Smuggled Merchandise, Gov

.L...,.......:VNNERSITY . OF HAWAII LIBRARY- arianas %rietYr;~ Micronesia's Leading Newspaper Since 1972 · · ~ Vol. 26· No .. 48 : . - . .. 0 ·, • : • • ••• •• F,, ~d. ' '·M: '. z 1 "' 1 9 ft 9 . ' . .. .. .·: : . S_aipan, MP 969~p.'. .· .·.. ),::;-1·;¢:-· . ©1999Ma~ianas\iariety .-·· ;. _·.·.;. · ..... ,.: :- .·. , • .-y .•.., , ,aY. .. ~ .. 7 ..... ·.· .. : _Serving_C_NMlf~r~6.Y~ar~:.:.~> ... '.,,;.:- .. ' ," < • \ • ,0 < • • • • • ' • • • ~ ~ • 0 ' < • < • .. r • ' • ~ Retail stores under watch According to Capitol Hill resident: for selling smuggled items By Aldwin R. Fajardo Variety News Staff 'Gov't e1D.ployees AT LEAST 87 retail stores in the CNMI are being investigated by government operatives for allegedly selling smuggled merchandise, Gov. Pedro P. Tenorio disclosed yesterday. Tenorio warned that businesses selling smuggled items face clo in burglary ring' sure while store owners would be slapped with criminal and civil charges. By Zaldy Dandan out that some government employ fied during yesterday's oversight "If businesses violate local and federal laws, they are subject not Variety News Staff ees are believed to be involved in a hearing to complain about the un only to prosecution but also closure." A CAPITOL Hill resident yester burglary ring. solved burglary cases on their During the governor's meeting with members of the Saipan Cham day said certain government em Public Safety Commissioner neighborhood. ber of Commerce, concerns about the proliferation of smuggled ployees are involved in a syndicate Charles W. Ingram Jr. neither con The public hearing, the second items on Saipan were raised. that is responsible for the spate of firmed nor denied the allegation, but in a series, is in response to the Tenorio said the Chamber is wary about unfair trade competition burglaries in her neighborhood. -

Die Königsmacher Nach Geldquellen Und Bleibe in Der Öf Fentlichkeit Präsent

klärtermaßen zur Opposition gehören) und um gute Umfrageergebisse, organi siere eine Wahlkampfmaschine, suche Die Königsmacher nach Geldquellen und bleibe in der Öf fentlichkeit präsent. Wer unterstützt wen im Vier Personen aus dem Regierungsla ger haben sich bereits ins Rennen um die philippinischen Wahlkampf ? Präsidentschaft gebracht: Der Regie rungssprecher Jose De Venecia, die Se Sie haben keine echte Ausbildung für übersetzt werden, sogar Abhöranlagen natorin Leticia Ramos Shahani, der Fi ihren Job hinter sich, aber trotzdem und die Standardausrüstungen von nanzminister, Roberto De Ocampo, und gelten sie als Spezialisten. Manche son Spionen. Sie sind Generalisten (die, die dessen Kollege im Verteidigungsmini nen sich in der Aufmerksamkeit, die ih sich im gesamten Wahlspiel auskennen) sterium, Renato De Villa. Alle Bewerber nen die Medien gönnen, andere arbeiten und Spezialisten (die, die Meister in ei aus dem Regierungslager landeten bei eher unsichtbar im Hintergrund. Sie be nem bestimmten Teilbereich sind). Auf Umfragen nach ihrer Bekanntheit ironi- wegen sich zwanglos in den Gängen der jeden Fall sind alle kreativ, hochgradig schenveise am Ende der Skala. De Macht, weil sie für die Obersten im Land phantasievoll und vielleicht die einzigen Ocampo und De Villa sind keine Mit arbeiten. Die meisten von ihnen arbeiten ernsthaften Betrachter der Politik. glieder bei Lakas-NUCD und sind von unter Druck am effizientesten, weil sie In der Vergangenheit wurden im De Venecia dazu aufgefordert worden, in sich auf einem Gebiet bewegen, das Wahlkampf Karrieren gemacht. Aber es die Partei einzutreten und für eine No minierung erst mal zu arbeiten. durch Konkurrenz geprägt ist, und wo ist wenig darüber bekannt, was dort ver nur der Stärkste überlebt. -

Global Finance Announces the Winners' Circle a Ranking of the Top

Global Finance announces The Winners' Circle The reach of Global Finance A ranking of the Top Winners of our Annual Awards Global Finance, founded in over the magazine's 25-year history 1987, has a circulation of 50,050 and readers in 163 countries. Its circulation is audited by BPA. Global NEW YORK, June 4, 2012 – Global Finance magazine is proud to announce The Winners' Circle – the Top Winners from 25 years of the magazine's annual awards Finance’s audience includes program. chairmen, presidents, CEOs, CFOs, treasurers and other “The world has changed dramatically since Global Finance first appeared in 1987. Global senior financial officers respon- financial markets have undergone a seismic shift, and the firms and individuals that made sible for making investment it into our Winners' Circle are those that have shown their true mettle and transformed and strategic decisions at themselves to meet the demands of a changing environment," says Global Finance’s publisher, Joseph D. Giarraputo. “We recognize these firms and individuals for their multinational companies and outstanding accomplishments over the past 25 years.” Global Finance’s annual awards financial institutions. Global program is a recognized and trusted standard for the entire financial world. Finance also targets the 8,000 international portfolio investors A full report on the winners will appear in the Special Commemorative 25th Anniversary responsible for more than Issue, released on June 25th, 2012. Award tallies are calculated to June 2012 issue. To compile the winners, we tallied winners/those taking first place over all of the years that a 80% of all global assets under particular award was given. -

70, Wanted to Own the Best Bar in Ann Arbor 25 Years Ago — Instead He Became CEO of a $9 Billion Food Company

University of Michigan Business School Alumni Connection Company Connection Degree Programs Executive Education Faculty Expertise Resources & Facilities University Home Page World Wide Web Address: http://www.bus.umich.edu Check Us Out t might well take a week of phone is an interview with Professor Joel The Business School student calls as well as numerous visits to Slemrod, director of the Office of newspaper The Monroe Street Journal, the School to access the wealth of Tax Policy Research, about the pros is now also being published on-line information now available by and cons of the flat tax. (http://www.umich.edu/~msjrnl), as Iaccessing the home page of the Dividend is also available through is detailed information about the city University of Michigan Business the alumni section of the home of Ann Arbor (http://online. ann- School (http://www.bus.umich.edu/). page. There you can write a letter to arbor.mi.us/ann-arbor/online. There you can find information the editor, change your address, or html). The University of Michigan about the admissions office, execu contribute a "Class Notes" item. and the U-M Alumni Association also tive education programs, office of Excerpts from the current issue are have home pages on the Internet career development, the William also on-line at that site. (http://www.umich.edu). Davidson Institute, the Tauber Tom Shaheen, computer systems Manufacturing Institute, the BBA consultant in Computing Services at A Classroom on the Web program, the Global MBA, and our the School, designed and produced curriculum. And with the Web's the Web Site, working with BBA ability to link documents together students Rich Blank and David Cole. -

From the Ground Up: Multi-Level Accountability Politics in Land Reform in the Philippines

December 2017 Accountability Working Paper Number 2 From the Ground Up: Multi-Level Accountability Politics in Land Reform in the Philippines Francis Isaac Danilo Carranza Joy Aceron From the Ground Up: Multi-Level Accountability Politics in Land Reform in the Philippines 1 About Accountability Research Center (ARC) The Accountability Research Center (ARC) is an action-research incubator based in the School of International Service at American University. ARC partners with civil society organizations and policy reformers in the global South to improve research and practice in the field of transparency, participation and accountability. For more information about ARC, please visit the website: www.accountabilityresearch.org. About ARC Publications ARC publications serve as a platform for accountability strategists and researchers to share their experiences and insights with diverse readers and potential allies across issue areas and sectors. These publications frame distinctive local and national initiatives in terms that engage with the broader debates in the transparency, participation and accountability (TPA) field. Research publications include brief Accountability Notes, longer Accountability Working Papers and Learning Exchange Reports. Rights and Permissions The material in this publication is copyrighted under the Creative Commons Attribution 4.0 Unported license (CC BY 4.0) https://creativecommons.org/licenses/by/4.0/. Under the Creative Commons Attribution license, you are free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the following conditions: Attribution—Please cite the work as follows: Isaac, Francis, Danilo Carranza and Joy Aceron. 2017. “From the Ground Up: Multi- Level Accountability Politics in Land Reform in the Philippines.” Accountability Research Center, Accountability Working Paper 2. -

Annual Report 1998.Pdf

'~ff' I , Philippine Social Science Council, Inc• ...a private organization of professional social science associations in the Philippines . , II/HH({jAl RIfFORr !/!J!Jg} C'---__tONTENTS ) lPSSC Board of Tmstees lProposed Agenda 1 Minutes 3 Chainnan's Report 10 Treasurer's Report 21 Accomplishment Reports of PSSC Membe~As80ciations 42 Regular Linguistic Society of the Philippines Philippine Association of Social Workers, Inc. Philippine Economic Society Philippine Geographical Society Philippine Historical Association Philippine National Historical Society Philippine Political Science Association Philippine Societyfor Public Administration Philippine Sociological Society Philippine Statistical Association Psychological Association of the Philippines UgnayangPang-Aghamtao, Inc. Associate American Studies Association of the Philippines, Inc. Center for Institutional Research and Development, PCU Center for Legislative Development Center for Research and Extension Services, Aquinas University College of Social Work and Community Development, UP Institute of Philippine Culture .Interdisdplinary Research Group, Silliman University National Tax Research Center Philippine Association for Chinese Studies Philippine Business for Social Progress Philippine-China Development Resource Center Philippine Psychology Research and Training House Population Institute, UP Research and Development Center, Saint Paul University School of Economics, University of Asia and the Pacific School of Urban and Regional Planning, UP Soda! Research Center, UST Social Weather Stations Statistical Center, UP University ofSt. La Salle - University Research Center/ Business Resource Center 1998PSSC General Assembly/Board of Trustees Resolutions 137 DiJTectory of PSSC Regular Member Associations 141 DiJTe(jtory of PSSC Associate Member Associations 143 RoJI of Officers ofPSSC RegularMember-Assectatiens 148 PSSC Secretariat --J1.l....' _ ( 1'98 BOARD OFTRUSTEES) NestorN. Pilar Chairperson (Public Administration) Elena L. Samonte Vice-Chairperson (Psychology) Ana MariaL. -

Why Immigrants Benefit the United States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S

Golden Gate University School of Law GGU Law Digital Commons Theses and Dissertations Student Scholarship 4-14-2016 Why Immigrants Benefit the nitU ed States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S. Marc Santamaria Golden Gate University School of Law, [email protected] Follow this and additional works at: http://digitalcommons.law.ggu.edu/theses Part of the Comparative and Foreign Law Commons, and the Immigration Law Commons Recommended Citation Santamaria, Marc, "Why Immigrants Benefit the nitU ed States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S." (2016). Theses and Dissertations. Paper 67. This Dissertation is brought to you for free and open access by the Student Scholarship at GGU Law Digital Commons. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of GGU Law Digital Commons. For more information, please contact [email protected]. GOLDEN GATE UNIVERSITY SCHOOL OF LAW ÈÈÈÈÈ Why Immigrants Benefit the United States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S. Attorney Marc Santamaria, J.D., LL.M. S.J.D. Candidate ÈÈÈÈÈ SUBMITTED TO THE GOLDEN GATE UNIVERSITY SCHOOL OF LAW, DEPARTMENT OF INTERNATIONAL LEGAL STUDIES, IN FULFILLMENT OF THE REQUIREMENT FOR THE CONFERMENT OF THE DEGREE OF SCIENTIAE JURIDICAE DOCTOR (SJD). Professor Dr. Christian Nwachukwu Okeke Professor Dr. Remigius Chibueze Professor Dr. Gustave Lele SAN FRANCISCO, CALIFORNIA April 14, 2016 Acknowledgments To our God and Father be glory for ever and ever. -

PROMISED LAND Foodfirst-Promised Land.Qxd 9/27/06 2:22 PM Page Ii Foodfirst-Promised Land.Qxd 9/27/06 2:22 PM Page Iii

FoodFirst-Promised_Land.qxd 9/27/06 2:22 PM Page i PROMISED LAND FoodFirst-Promised_Land.qxd 9/27/06 2:22 PM Page ii FoodFirst-Promised_Land.qxd 9/27/06 2:22 PM Page iii PROMISED LAND Competing Visions of Agrarian Reform Edited by Peter Rosset, Raj Patel, and Michael Courville A project of the Land Research Action Network (LRAN) FOOD FIRST BOOKS • Oakland, California FoodFirst-Promised_Land.qxd 9/27/06 2:22 PM Page iv Copyright © 2006 Institute for Food and Development Policy. All rights reserved. No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage retrieval system, without written permission from the publisher, except for brief review. Text design by BookMatters, Berkeley Cover design by BookMatters Cover photograph: “Amazon, Brazil. Squatters occupy unproductive estate” by J.R. Ripper/Social Photos. Library of Congress Cataloging-in-Publication Data Promised land : competing visions of agrarian reform / edited by Peter Rosset, Raj Patel, and Michael Courville. p. cm. “This book represents the first harvest in the English language of the work of the Land Research Action Network (LRAN). LRAN is an international working group of researchers, analysts, nongovernment organizations (NGOs), and representatives of social movements”— Pref. Includes bibliographical references and index. isbn-13: 978-0-935028-28-7 (pbk.) isbn-10: 0-935028-28-5 (pbk.) 1. Land reform. 2. Land use, Rural. 3. Minorities — Land tenure. 4. Economic development. 5. Distributive justice. I. Title: Competing visions of agrarian reform. II. Rosset, Peter. -

Advancing Corporate Governance in the Philippines

PwC GGAPP Philippines Corporate Governance Survey Finding the true north Advancing corporate governance in the Philippines www.pwc.com/ph Foreword Message from the SEC Chairperson My warmest congratulations to In addition, the SEC believes that the the Good Governance Advocates results of this Survey would be most and Practitioners of the Philippines beneficial in the implementation (GGAPP) on the success of its 2016 of the 2016 Code of Corporate Code of Corporate Governance Governance for PLCs. The new Survey. The GGAPP has been a Code aims to make Philippine consistent partner of the Securities corporate governance standards at and Exchange Commission (SEC) par with regional and international in its advocacy to promote good standards and this Survey would corporate governance for Philippine be a useful tool for providing both corporations. As actual practitioners the SEC and PLCs the necessary of good corporate governance from information on the focus areas to various publicly listed companies be addressed in the advancement of (PLCs), GGAPP has consistently corporate governance for Philippine provided the SEC invaluable insights corporations. Atty. Teresita J. Herbosa Chairperson, Securities & Exchange on the application of best corporate Commissions (SEC) governance and ethical practices. The promotion of good corporate Moreover, GGAPP has contributed governance is an uphill battle. greatly to both the SEC Philippine However, with partners such as Corporate Governance Blueprint GGAPP assisting SEC in instilling and the 2016 Code of Corporate the proper corporate governance Governance for PLCs. foundation in PLCs, it is certain that the time will come when corporate This recent initiative of conducting governance will be second nature to the 2016 Code of Corporate companies and due recognition will Governance Survey in partnership be given to the benefits of compliance with Isla Lipana & Co./PwC with good practices.